Happy New Year

Policymakers and advocates often promote drug price transparency to lower costs and improve equity. While transparency is an important first step toward accountability and informed public budgeting, it does not guarantee affordable prices or fair access to medicines.

Transparency Has Some Benefits

Drug price transparency helps show how and why medicines cost what they do along the supply chain (i.e., from the manufacturer to the pharmacy), which makes it easier to identify where costs can be reduced or better regulated. By making this information public, transparency allows patients, payers, and policymakers to make more informed decisions and encourage manufacturers to prices drugs more fairly. Ultimately, it supports a fairer system where patients can better afford and obtain the treatments they need, improving access to care.

States with Drug Transparency Laws

While federal policy to improve price transparency is lacking, the states have moved to make things clearer for patients and payers. Vermont was the first U.S. state to enact a drug price transparency law in 2016. Since then, many others have followed suit. At least 14 states have passed some version of transparency legislation, though the details and their enforcement of these laws differ widely.

For example, only Vermont and Maine require drug companies or insurers to disclose the actual prices paid after discounts (called the “net price”). Alternately, Oregon and Nevada require drug manufacturers to publicly report their profit to state government agencies. And Connecticut, Louisiana, and Nevada mandate pharmacy benefit managers (PBMs) to report the total rebates they receive, but not the amounts for each specific drug. Despite these efforts, no state has yet achieved full transparency across the entire drug supply chain.

Transparency is Not Enough

Even with clear pricing, Americans still pay about 2.6 times more for prescription drugs than people in other wealthy countries. Early evidence suggests that these laws have done little to curb drug prices. To date, only four states – California, Maine, Minnesota, and Oregon – have published analyses of their own laws. These reports share common concerns: difficulty tracking pricing across the supply chain and uncertainty about whether state agencies have the authority (or the will) to act when data is incomplete or unreliable.

Most transparency laws fall short on requiring detailed cost or profit data, focusing instead on broad price trends. As a result, this narrow scope makes it difficult to identify the exact drivers of high drug prices. Even when transparency discourages manufacturers from raising prices, these policies do not directly control pricing or define what constitutes an ‘unjustified’ price increase. Manufacturers can simply adjust by setting higher launch prices or implementing smaller, more frequent increases to stay below reporting thresholds. Still, the result is a system where drug costs can vary by as much as $719 for the same 30-day prescription even when prices are publicly listed.

What can also be done?

Creating a consistent national framework could replace the current patchwork of state laws and improve oversight of how drugs are priced. For example, the Drug Price Transparency in Medicaid Act (H.R. 2450) could do just that: it would standardize reporting requirements and reveal how drug prices are set, rebated, and reimbursed. But transparency alone can’t lower costs—it only shows the problem.

To make transparency meaningful, policymakers must address the underlying contracts and incentives that drive high prices.

Hidden rebate deals and opaque pricing structures between PBMs and drugmakers often inflate costs and limit patients from seeing savings. Transparency legislation should also be paired with value-based pricing that links payments to clinical benefits. Federal programs like the Medicare Drug Negotiation Program provide additional leverage, but broader reforms are needed to reach the commercial market (i.e., where most Americans get their prescription drugs and still face high prices).

Still, transparency can have downsides, especially globally. Fully public drug prices could push companies to stop offering lower prices in low- and middle-income countries. To avoid cross-country comparisons, they could raise prices across the board, making medicines less affordable where they’re needed most. To make transparency more equitable, policymakers should combine disclosure with protections that preserve affordability worldwide.

Conclusion

In short, transparency is necessary but an incomplete fix for America’s drug pricing system. Simply shining a light on how prices are set isn’t enough. Policymakers need to be paired with other reforms, such as removing the incentives that encourage high prices, holding PBMs and manufacturers accountable, extending the negotiating power beyond Medicare, and protecting prescription drug access both at home and abroad. Without these other steps, transparency laws risk highlighting unfairness without actually improving it.

Millions of ACA enrollees will face steep premium hikes in 2026 as insurer rate increases collide with the expiration of enhanced federal subsidies.

As health insurance premium costs have taken center stage this fall, you may have seen seemingly conflicting reports about how much premiums are increasing, especially for ACA marketplace plans. This isn’t a reporting error. Instead, it reflects a double whammy of increases that more than 20 million ACA enrollees are poised to face in 2026.

To understand what’s happening, it helps to think of ACA premium increases as a one-two punch.

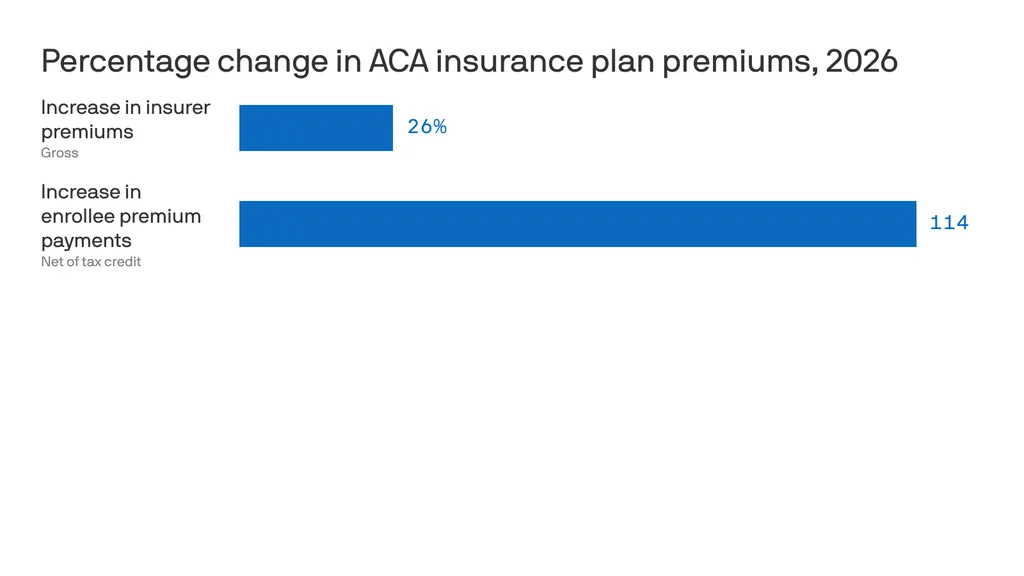

The first hit comes from the overall increase in health insurance premiums for 2026. On average, insurers raised premiums for ACA marketplace plans by roughly 26 percent from 2025 to 2026. This increase reflects a rise in the total cost of coverage, the full premium paid jointly by enrollees and the federal government through subsidies, not just what individuals pay out of pocket.

Premium increases are not new. Insurers raise rates every year. But the 2026 hike is striking: more than three times the 7 percent increase in 2025 and the 6 percent increase in 2024. Insurers have attributed roughly four percentage points of this increase to the anticipated expiration of the enhanced premium tax credits, arguing that enrollment will decline and that sicker, higher-cost enrollees will make up a larger share of the risk pool. Insurers also cite provider consolidation and high pharmaceutical prices as drivers of higher premiums.

These explanations deserve scrutiny. As Wendell Potter recently documented, the seven largest private insurance corporations have collectively taken in more than $10 trillion in revenue since 2014 with revenues steadily increasing each year. Against that backdrop, claims that today’s premium spikes are unavoidable or purely defensive ring hollow.

The second hit falls directly on consumers who currently rely on enhanced premium subsidies (in the form of tax credits) to make coverage affordable. Those enhanced subsidies, first made available during the pandemic, are set to expire at the end of 2025, and Congress appears poised to let them lapse without an extension. If that happens, many enrollees will see the tax credits that lower their monthly premiums shrink dramatically or disappear altogether. Taking this into account, the amount people pay out of pocket for ACA premiums is expected to increase by an estimated 114 percent in 2026. And that is just for the premiums. People enrolled in ACA plans will also have to spend hundreds if not thousands of dollars out of their own pockets in deductibles and copays before their coverage kicks in.

This double whammy will have drastic, and potentially deadly, consequences for millions of Americans. I am already seeing panic from people in my own community and across the country, echoed daily on social media. Yet Congress has taken no action to cushion the blow. The Republicans leading both the House and the Senate are leaving Washington without extending the enhanced tax credits, even as the clock runs out.

This is an abdication of Congress’s responsibility to represent the people it serves, people who have been clear about what they want and need: health insurance they can actually afford. Rather than getting bogged down in partisan gridlock or abstract market ideology, Congress must act now to extend the enhanced premium tax credits. That extension should be treated as an urgent bridge to a real fix to our health care system; one that reduces dependence on Big Insurance, lowers costs for patients, and ensures that no one is forced to go without care.

2025 was one of the most turbulent years in modern U.S. healthcare. The headlines were explosive, the rhetoric dramatic and the controversies nonstop. Yet for all the hoopla and upheaval, the medical care Americans received this month looked almost identical to what they experienced on January 1 — except more expensive.

That yearlong pattern (of intense disruption followed by little improvement) played out across nearly every major healthcare storyline.

Luigi Mangioli is preparing to stand trial almost exactly twelve months after the fatal shooting of UnitedHealth CEO Brian Thompson. The killing sparked fears for major health insurers and raised questions about the fragility of the nation’s largest payer. In a February article, I called it a defining moment for UnitedHealth: an opportunity for the company to start competing on health, not denials. But despite the initial shock and ongoing scrutiny, nothing has shifted in how UnitedHealth pays for (or denies) medical care.

Then, in late fall, the nation endured the longest government closure in U.S. history, driven largely by conflicts over healthcare spending and the Affordable Care Act’s health exchanges. However, the eventual resolution to reopen the government came with no respite for the 24 million Americans currently enrolled in an exchange.

For a broader view of the year, here are five major areas of healthcare that generated chaos, confusion and conflict in 2025 – but little meaningful improvement.

No aspect of healthcare saw more volatility in 2025 than in the political arena. The tone was set in January when President Trump returned to office and began reshaping federal health agencies with unprecedented speed.

Within days, he issued a record flurry of executive orders targeting the Affordable Care Act, Medicaid waivers, Medicare Advantage oversight, prior-authorization rules and federal nutrition standards.

He replaced long-entrenched leaders at HHS, NIH, CDC and FDA with political outsiders, many of whose views on vaccines, chronic disease and scientific evidence diverged sharply from the career experts they superseded. The nomination of RFK Jr. to lead HHS became a flashpoint. His reluctance to confront the measles outbreak in Texas, combined with mixed messaging on vaccine policy, have deepened concern for public health.

The result has been rapid turnover of expert clinicians and a revolving door of leaders in the FDA, CDC and NIH. Senior scientists continue to resign, key programs remain stalled and career staff report growing political interference in decisions that previously rested on data and expert consensus.

Beneath the political theatrics of 2025 was a sobering reality: Americans will once again pay far more for healthcare next year than the year before. And for many, the financial protections that once softened those increases are disappearing.

Insurers on the Affordable Care Act (ACA) marketplace requested median premium hikes of 18% for 2026, the steepest jump since 2018 and well above this year’s 7% hike. If Congress fails to extend the enhanced ACA subsidies, families who once paid affordable monthly premiums will see their costs double or even triple.

The broader economic picture makes these pressures unavoidable. The United States is now spending $5.6 trillion annually on healthcare. National health expenditures are projected to climb another 7.1% this year, far outpacing economic growth. At the same time, federal debt service continues to soar, consuming more of the national budget than Medicaid itself.

The result is an economic crisis hiding in plain sight, one that will increasingly strain the financial, physical and mental health of Americans in the year to come.

This year shook the foundations of America’s public-health architecture and left yawning gaps where trust, clarity and expert oversight once stood. Politics has replaced science as the primary driver of healthcare policy.

The Centers for Disease Control and Prevention lost its director just weeks after her confirmation. Within days, top-level scientists and center heads resigned en masse, citing political interference and a collapse of scientific independence. Months later, there still is no permanent CDC head.

At the Food and Drug Administration, career reviewers say they’ve been forced to reconsider or abandon scientific best practices. Across both the CDC and FDA, advisory committees that once evaluated evidence through rigorous, peer-driven processes now rely on anecdote and ideology. One striking example is the FDA’s decision to stop requiring hepatitis B vaccination at birth, a move that public-health experts warn could lead to tens of thousands of additional infections for a disease that had been reduced to fewer than 20 annual cases.

Meanwhile, the administration’s sweeping “health-freedom agenda” (under the banner Make America Healthy Again) has identified food packaging, additives, school-lunch standards and “ultra-processed” diets as public-health priorities. But the proposals to improve nutrition remain largely unformed, as the likelihood of meaningful improvements fade.

What remains at year’s end is a set of agencies still functioning, but with public trust weakened and no clear path to rebuilding it.

No field generated more excitement, or exposed more contradictions, in 2025 than generative artificial intelligence.

In the broader economy, GenAI models transformed finance, logistics, law, retail and customer service. New large language models, including GPT-5, DeepSeek and Gemini 3, demonstrated near-expert performance on clinical reasoning, interpretation of complex symptoms and risk prediction. Ambient listening matured into a reliable documentation tool, and with the emergence of Artificial General Intelligence (AGI), Americans are relying on large language models when they have medical questions.

Yet inside traditional medicine, progress remains stalled. Clinicians continue to be encouraged to use AI for administrative shortcuts (coding, charting, prior authorization claims) but national specialty organizations haven’t pushed them to use GenAI for diagnosing disease, reducing medical errors or improving clinical outcomes.

Fear of liability has discouraged technology companies from offering GenAI tools that would allow patients to evaluate symptoms or manage their chronic diseases. Yet usage continues to grow. In polling I conducted this fall, 77% of patients and 63% of healthcare professionals reported using a generative-AI tool in the past three months for health-related information or decision support. Meanwhile, medical schools still teach pre-AI workflows, even as medical students and residents turn to GenAI for clinical knowledge and case analysis. The divide between institutional practice and the behaviors of patients and the next generation of physicians is expanding at an accelerating pace.

If 2025 revealed anything about American healthcare, it was a widening cultural rift: between younger patients and medical professionals, and between science and public belief.

This rift is felt particularly among Gen Z and Millennials, generations that grew up online, accustomed to second-screen verification and skeptical of traditional authority. As I wrote in 3 Ways Doctors Can Win Back Gen Z And Millennial Patients, younger Americans expect shared decision-making, transparency and digital-first convenience — expectations medicine failed to fulfill in 2025.

At the same time, disinformation and political rhetoric seeped deeper into public life. Social media spread half-truths faster than public-health leaders could correct them. Vaccine skepticism rose thanks to political disinformation. Basic nutritional science became partisan, too. And the public’s confusion only intensified.

By year’s end, one truth became impossible to ignore: despite unprecedented political turmoil, economic instability, scientific breakthroughs and cultural upheaval, the basic structure of American healthcare remained unchanged.

The incentives driving the system, the chronic diseases afflicting the population and the unaffordability confronting families all persist as we enter 2026. At the same time, as generative AI transforms nearly every other sector of the economy, the fax machine remains the most common method physicians use to exchange vital medical information.

The question now is whether mounting economic, political and cultural pressures will finally force American medicine to transform care delivery next year. For more on that, follow me on Forbes and look for my next article on January 5, featuring my healthcare predictions for 2026.

There’s a good chance your health insurance premiums are going up next year, regardless of where you get coverage.

Why it matters:

The spike in what millions of Affordable Care Act plan enrollees pay will be acute, but workplace insurance is getting more expensive, too — and all at a time when affordability is prominently on Americans’ minds.

ACA premiums have dominated the political discourse in Congress for weeks, but there’s no real sign that any relief is coming from Washington.

The big picture:

Health insurance gets more expensive almost every year, keeping up with increases in the costs of procedures, tests, drugs and more. But some years see bigger jumps than others, and 2026 is looking like one of those years.

By the numbers:

ACA insurers themselves are raising premiums by an estimated 26%, in part due to rising hospital costs, higher demand for pricey GLP-1 drugs like Ozempic, and the threat of tariffs.

For employer health insurance, there’s no comprehensive data yet for 2026, but estimates from earlier this year put the increases in the high single digits.

Between the lines:

Just this month, Gallup polling found that approval of the ACA has hit an all-time high of 57%, including more than 6 in 10 independents but only 15% of Republicans.

The bottom line:

Get ready to hear a lot more about health care costs over the next year — while potentially also experiencing your own premium increase.

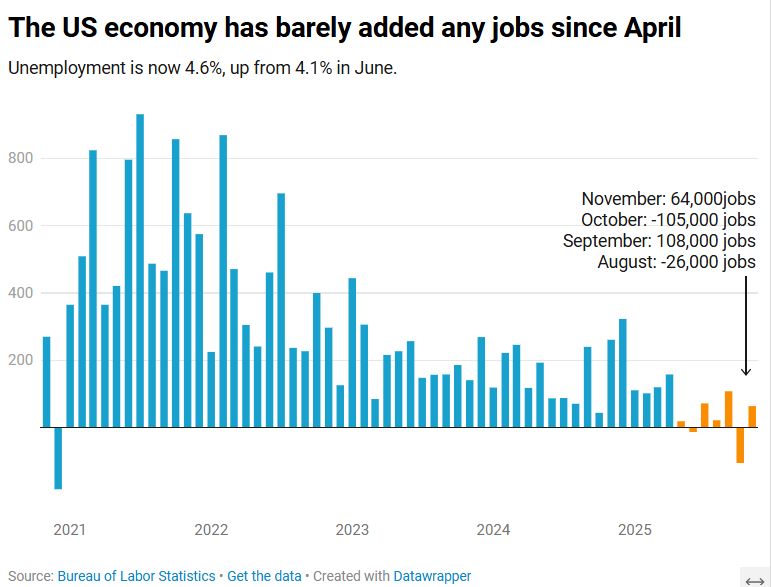

The US economy added 64,000 jobs in November, according to the Bureau of Labor Statistics.

The US economy added 64,000 jobs in November as the unemployment rate crept up to 4.6%, according to Labor Department data published Tuesday.

The unemployment rate is now at its highest level since September 2021.

The November jobs report, originally scheduled to be published Dec. 5 before the 43-day government shutdown delayed multiple economic data releases, comes as Americans stress over rising layoffs and a frozen job market that can feel impossible to break into. Tuesday’s report suggested those conditions persisted toward the end of the year.

Economists surveyed by Bloomberg had expected a gain of 50,000 jobs. The healthcare sector, which has fueled job growth this year, added 46,000 positions for the month.

November’s data additionally showed that the number of people employed part-time for economic reasons rose to 5.5 million in November, an increase of 909,000 over September. Meanwhile, the long-term unemployment rate, or the share of unemployed people who have been without jobs for 27 weeks or more, was 24.3% in November, down from August’s high of 25.7% but higher than the rate of 23.1% seen a year ago.

“The US economy is in a hiring recession,” Heather Long, chief economist at the Navy Federal Credit Union, wrote in a post on X.

“Almost no jobs have been added since April,” Long added. “Wage gains are slowing. 710,000 more people are unemployed now versus November 2024.”

Nancy Vanden Houten, lead US Economist at Oxford Economics, said in a statement that the government shutdown appears to have contributed to the increase in the unemployment rate.

“The number of permanent job losers, which had been ticking higher, declined. Labor force growth also contributed to the increase,” she said.

Partial data for October, also published Tuesday, showed a loss of 105,000 positions. The unemployment rate for the month will not be released. Bank of America economist Shruti Mishra had noted that October’s payroll numbers would be affected by the delayed impact of DOGE-led government job cuts, since many federal employees who opted for the “deferred resignation program” officially left their positions Sept. 30.

The federal government lost 162,000 jobs in October and 6,000 in November, according to the Labor Department.

The last official reading of the labor market, published in November, was pushed back by several weeks and had only offered data for September, showing an unexpected uptick in jobs after the economy actually lost jobs in August and June, marking the first negative employment months since 2020.