The Texas lawsuit could end some of the ACA’s protections for employer coverage.

The Trump administration’s refusal to defend portions of the Affordable Care Act is shocking enough. Equally shocking is how little it seems to care what happens if it gets what it’s asking for.

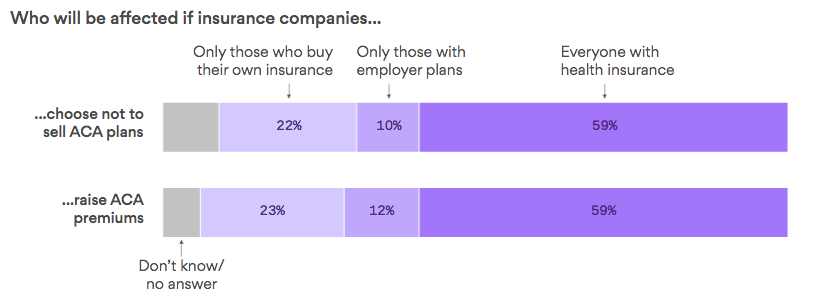

One question in particular: what about legal protections for the 160 million people who get insurance through their employers? Will their insurance still cover their preexisting conditions, even if they switch jobs? I honestly have no idea.

In its brief, the Justice Department argues that the community rating and guaranteed issue provisions of the ACA must be invalidated. But it never mentions that those provisions apply not only to individual health plans, but also to employer plans.

So should those rules give way across the board? Or only for individual insurance plans?

Maybe it should be the latter. The mandate isn’t critical to securing the health of the employer market, so the ACA rules that protect employees aren’t inextricably linked to the mandate and shouldn’t be invalidated. But it could also plausibly be the former: if the rules governing community rating and guaranteed issue are inseverable, maybe the court shouldn’t do micro-surgery to save some subpart of those rules.

But guess what? In its brief, the Justice Department doesn’t say which approach it endorses.

Actually, it’s worse than that. When the Justice Department identifies the rules governing community rating and guaranteed issue, it doesn’t cite the ACA itself (Public Law 111-948). Instead, it cites parts of the U.S. Code that codify portions of the ACA (e.g., 42 U.S.C. 300gg). The implication is that the Justice Department wants the court to enjoin those code provisions.

But the code provisions were on the books long before the ACA was adopted. Prior to the ACA, they listed protections for employer-sponsored plans that had been adopted in the Health Insurance Portability and Accountability Act. Among other things, HIPAA limited the circumstances under which an employer could refuse to cover an employee’s preexisting conditions. The protections weren’t perfect, but they were something. The ACA patched HIPAA’s gaps by amending those code provisions.

So if the U.S. Code provisions are enjoined altogether—which, again, is what the Justice Department appears to be asking for—some of the HIPAA-era protections would be wiped from the books too.* Is that really what the Justice Department wants? Because that’s the thrust of its brief.

The confusion may reflect a basic legal mistake, one that Tobias Dorsey highlighted in Some Reflections on Not Reading the Statutes: the U.S. Code is a codification of existing laws, but it’s not itself the law. That’s why code provisions shouldn’t themselves be the target of any injunction. Any injunction should run against the ACA itself. If that’s what the Justice Department really wants, then it has to clarify what it’s really asking for. Failing to do so could wreak havoc in the employer-sponsored market.

Even if the injunction only runs against portions the ACA, however, that still wouldn’t resolve whether the ACA’s protections would still apply to employer-sponsored plans. If they don’t, that’s a big deal: HIPAA’s protections are porous.

So far, however, the Trump administration hasn’t said a word—leaving 160 million people in the lurch.