Tariff drama and tax cuts! AI spending and AI-spurred job losses! New Federal Reserve leadership! It is on track to be a big year across all the key policy areas of interest to economy-watchers.

The big picture:

Seismic changes have been set in motion by the Trump administration’s sweeping policy agenda and a mega-wave of investment in artificial intelligence — likely to determine the fate of the economy in 2026.

1. The AI economy

The biggest macro questions are whether the alarm bells about AI and the labor market will start to ring true — and whether the productivity effects move from just anecdotes to the economic data.

Last year, much evidence pointed to AI as a marginal part of the labor market slowdown. Some economists (and officials inside the White House) argue that broader adoption of the technology would boost the labor market, at least in the short term.

Of note:

AI spending buoyed economic growth, at least in the first nine months of 2025. It is also lifting the stock market, which might help support spending among wealthier consumers.

Whether this turns out to be a bubble that pops — and the extent such a risk poses to the broader financial system as the Fed rolls back regulations — is the related theme to watch.

That said, any correction in AI investment looks more likely to be a down-the-road story than a 2026 issue.

2. Tax cut boost

The One Big, Beautiful Bill Act, signed into law in July, is set to have its maximum economic punch in the early months of 2026, a likely tailwind for overall economic growth.

But how large, how broad-based and how sustained that boost will turn out to be remains to be seen.

Zoom in:

Fiscal policy is on track to add about 2.3 percentage points to first-quarter GDP growth, per data from the Hutchins Center Fiscal Impact Measure from the Brookings Institution.

On the individual tax side, beneficiaries of policies like a deduction for tip income, Social Security payments and expanded deductibility of state and local tax are on track to generate super-sized tax refunds this spring,

On the corporate side, businesses are enjoying new tax incentives for capital spending, especially on factories.

Federal spending on immigration enforcement, meanwhile, is ramping up due to the legislation.

3. Trade uncertainty (maybe) resolving

Any day now, the Supreme Court will hand down a decision that might scramble the centerpiece of President Trump’s economic agenda: the ability to impose huge tariffs unilaterally.

If the court strikes down the bulk of Trump’s tariffs, fiscal revenues could be put at risk, resulting in a chaotic refund process.

That said, the ruling will help create some guardrails on what kinds of legal authority the president has to impose unilateral tariffs. That, in turn, could lead to a more stable tariff picture (albeit with much higher rates than pre-2025).

While there are other authorities the president can use to enact tariffs besides the sweeping authority under the International Emergency Economic Powers Act he has claimed, they require a more deliberative process than the kind of whipsawing that importers faced last year.

4. Future of the Fed

Fed chair Jerome Powell’s term is up in May, and Trump’s selection of his successor is imminent, with Kevin Hassett and Kevin Warsh the leading job candidates.

Zoom out:

Whoever takes the reins will face immense pressure from Trump to lower interest rates to rock-bottom levels — amid continued high inflation — and how they handle that pressure may determine the future of the central bank’s independence from the White House.

Trump expects the future Fed chair to consult with him on rates, while casting the intention to lower rates as a key qualification for the next leader.

The question is whether the next Fed chair can resist that political pressure and whether financial markets believe that is the case. If bond markets lose confidence that the Fed will raise short-term rates if necessary to combat an inflation surge, it could paradoxically drive up long-term rates.

Another huge question: the makeup of the influential Fed board, with the Supreme Court also set to decide whether Trump can fire governor Lisa Cook and, by extension, other Biden-appointed governors.

5. Affordability and the midterms

With voters going to the polls in November, the cost of living is emerging as a core battleground.

Democrats seeking to take control of Congress are making political hay about the affordability crisis.

Trump has called the term affordability a “con job,” but said recently that he believes “pricing” will be a major election issue.

Flashback:

The Consumer Price Index is up a moderate 2.7% over the last 12 months, but that increase came on top of the Biden-era inflation surge.

The index is up 23.7% since January 2021, even more for some often-purchased subcategories, including groceries (up 24.6%).

Over the holiday break, the administration quietly shelved plans to impose levies on imported pasta and furniture.

It’s a hint that the White House is eager to avoid trade levies that might flow directly to prices consumers pay, as opposed to affecting input costs for businesses.

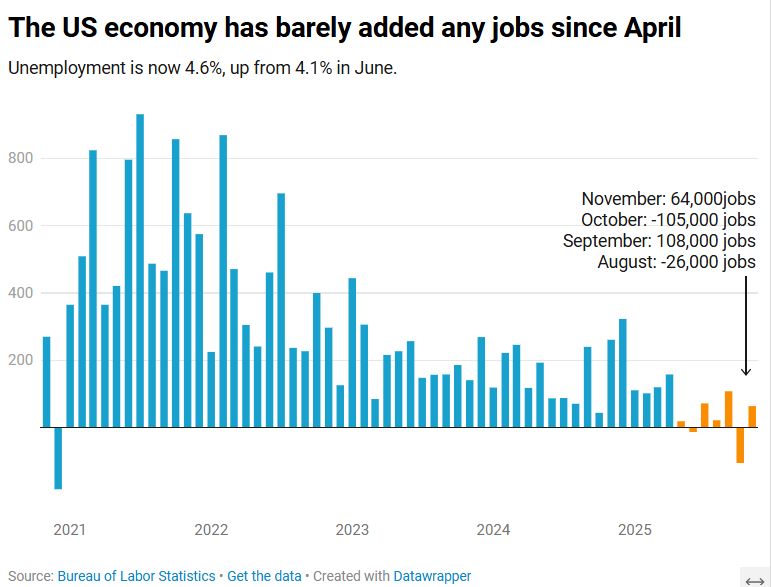

The US economy added 64,000 jobs in November, according to the Bureau of Labor Statistics.

The US economy added 64,000 jobs in November as the unemployment rate crept up to 4.6%, according to Labor Department data published Tuesday.

The unemployment rate is now at its highest level since September 2021.

The November jobs report, originally scheduled to be published Dec. 5 before the 43-day government shutdown delayed multiple economic data releases, comes as Americans stress over rising layoffs and a frozen job market that can feel impossible to break into. Tuesday’s report suggested those conditions persisted toward the end of the year.

Economists surveyed by Bloomberg had expected a gain of 50,000 jobs. The healthcare sector, which has fueled job growth this year, added 46,000 positions for the month.

November’s data additionally showed that the number of people employed part-time for economic reasons rose to 5.5 million in November, an increase of 909,000 over September. Meanwhile, the long-term unemployment rate, or the share of unemployed people who have been without jobs for 27 weeks or more, was 24.3% in November, down from August’s high of 25.7% but higher than the rate of 23.1% seen a year ago.

“The US economy is in a hiring recession,” Heather Long, chief economist at the Navy Federal Credit Union, wrote in a post on X.

“Almost no jobs have been added since April,” Long added. “Wage gains are slowing. 710,000 more people are unemployed now versus November 2024.”

Nancy Vanden Houten, lead US Economist at Oxford Economics, said in a statement that the government shutdown appears to have contributed to the increase in the unemployment rate.

“The number of permanent job losers, which had been ticking higher, declined. Labor force growth also contributed to the increase,” she said.

Partial data for October, also published Tuesday, showed a loss of 105,000 positions. The unemployment rate for the month will not be released. Bank of America economist Shruti Mishra had noted that October’s payroll numbers would be affected by the delayed impact of DOGE-led government job cuts, since many federal employees who opted for the “deferred resignation program” officially left their positions Sept. 30.

The federal government lost 162,000 jobs in October and 6,000 in November, according to the Labor Department.

A striking thing about this week’s flow of news out of the Federal Reserve is how normal it was — at least compared to some of the possibilities that appeared in play last month for a breakdown in the institution’s longstanding norms.

Why it matters:

In the Fed’s decision to cut interest rates on Wednesday, and the unanimous reappointment of 11 of 12 reserve bank presidents announced yesterday, it was clear that Powell has retained his ability to steer a seemingly fractious organization toward consensus.

The next chair may yet shift the institution toward a process with more open dissent and count-the-votes proceduralism, as is seen at the Bank of England and as some Trump associates have advocated.

But for now, Powell looks clearly in charge despite lame-duck status (his term is up in May).

State of play:

Just a few weeks ago, it looked plausible that there would be the most open dissent from the Fed’s December interest rate decision in decades. Five officials of 12 Federal Open Market Committee voting members had expressed significant reservations about a rate cut.

Three officials who were publicly skeptical of cutting rates further — reserve bank presidents Susan Collins (Boston) and Alberto Musalem (St. Louis), and governor Michael Barr — elected to follow the leader when it was time to cast their vote.

While there were three dissents — two opposing the cut, one favoring going further — that’s not terribly abnormal. There were three dissents in September 2019, for example, also in opposite directions.

What they’re saying:

“After the high drama/psychodrama from the October press conference onwards, the end result was more business-as-usual on the part of the Powell Fed,” wrote Krishna Guha and colleagues at Evercore ISI in a note.

In his news conference, “Powell was calm and poised, not on the ropes as in October, with a governance crisis averted,” they wrote.

The big picture:

Fed watchers were braced for the possibility that the every-five-years process of reappointing reserve bank presidents would generate fireworks, an opportunity for Trump-appointed governors to try to create some upheaval at the Fed (or at least make some noise).

It came and went yesterday without signs of public dissent, as the board announced that 11 of 12 reserve bank presidents had been reappointed with “unanimous concurrence” by members of the Board of Governors.

Not only were the 11 officials re-upped, the three Trump-appointed governors did not object.

The odd man out, Atlanta Fed president Raphael Bostic, had previously announced his retirement at the end of his term in February. But one bank president stepping down at the end of a term is not unheard of; it last happened at the end of 2015 with Minneapolis Fed president Narayana Kocherlakota.

Between the lines:

On paper, the Fed chair holds only one vote out of seven on the Board of Governors and one of 12 on the FOMC. Their ability to lead the institution depends on a mix of hard and soft power.

In the hard power department, the chair oversees the staff and sets meeting agendas. In the soft power department, they must persuade their colleagues to line up with the policy path they believe is correct.

Powell has been skilled at using both — and displayed those skills this week.

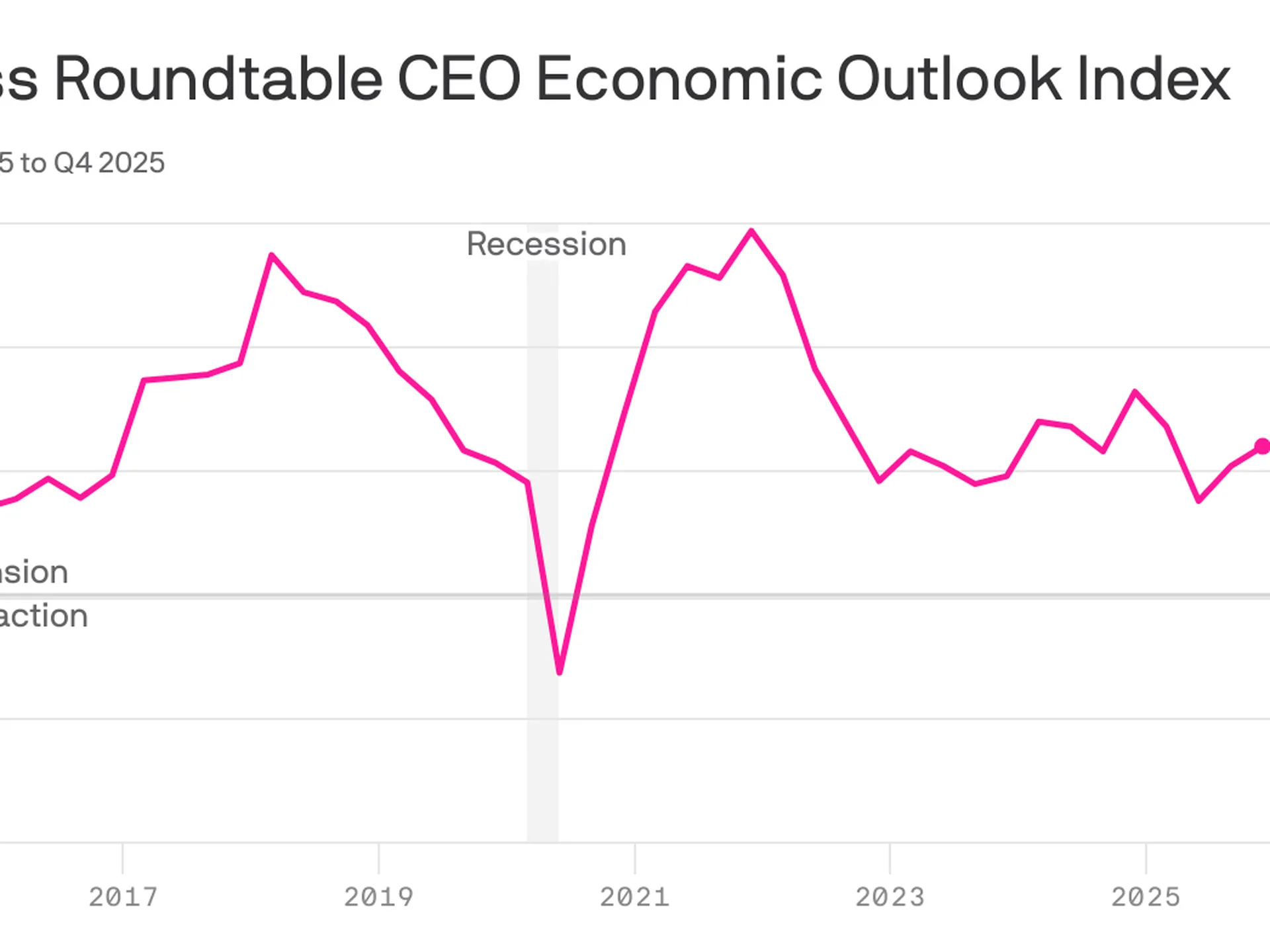

CEO sentiment increasedfor the third consecutive quarter, even as America’s most prominent executives expect underlying job market conditions to remain weak.

Why it matters:

The economic outlook among CEOs has steadily improved since plunging in the aftermath of President Trump’s initiation of the global trade war.

Under the hood, however, there is evidence that structural economic changes — including the proliferation of AI — are weighing on hiring intentions, a warning sign for the labor market.

By the numbers:

The Business Roundtable’s CEO Economic Outlook Index rose by 4 points in its fourth-quarter survey, which was fielded from the final weeks of November through earlier this month.

The index is still shy of the highest level of the Trump 2.0 era and slightly below the historical average of 83.

Zoom in:

The increase reflects a more upbeat view of company revenue in the next six months: Expectations for sales rose 6 points, though the survey does not ask respondents to adjust for the prospect of higher prices.

Plans for capital expenditures — investments in equipment, buildings or software — ticked up 2 points, following a 10-point surge in the previous quarter.

Hiring plans also improved relative to last quarter — up 4 points — though it is the survey’s lone indicator below the level that signals growth.

What they’re saying:

“Notably this quarter, more CEOs plan to reduce employment than increase it for the third quarter in a row – the lowest three-quarter average since the Great Recession,” Business Roundtable CEO Joshua Bolten said in a statement.

About one-quarter of CEOs say they will increase hiring, while 35% say employment will shrink at their respective firms. The remaining 40% plan to keep hiring steady.

A smaller share of CEOs plan to slash workers relative to last quarter, but the figures still show a notable shift among top executives.

Consider the results from this time last year: A similar share of CEOs expected no change in employment levels, but just 21% said they anticipated cutting jobs, while 38% planned to increase hiring.

“CEOs’ softening hiring plans reflect an uncertain economic environment in which AI is driving sizeable [capital expenditures] growth and productivity gains while tariff volatility is increasing costs, particularly for tariff-exposed companies, including small businesses,” Bolten said today.

The big picture:

The in-the-dumps hiring plans signaled by big firm CEOs — alongside a string of layoff announcements in recent months — signal a possible shift for the steady-state labor market that has persisted in recent years.

Powell raised the possibility that the labor market might be even weaker than government data suggests.

The economy has added a monthly average of 40,000 payroll jobs since April. But “we think there’s an overstatement in these numbers, by about 60,000, so that would be negative 20,000 per month,” Powell said at yesterday’s press conference.

“The labor market has continued to cool gradually, maybe just a touch more gradually than we thought,” he added.

The bottom line:

CEOs feel more optimistic, though that confidence boost is not expected to translate into more hiring — an unusual dynamic for the economy.

“Although the results signal that CEOs are approaching the first half of 2026 with some caution, they are starting to see opportunities for growth,” Cisco CEO Chuck Robbins, who chairs the Business Roundtable, said in a statement.

“With the Index near its average, it reflects the resilience of the U.S. economy,” he added, citing pro-growth tax policies and fewer regulations.

As we approach the end of 2025, it’s a good time to take stock of the US economy. There’s justifiable concern that this year has entrenched a K-shaped economy, where the have-mores leave the haves and have-nots behind. But there are more than two stories going on right now.

First, the vibes are bad (just ask anyone coming out of a grocery store). Second, the real economy—prices, jobs, and consumer and business spending, among other factors—is worse than it was a year ago,but holding up OK (4.4 percent unemployment, GDP growth over 2 percent, and inflation around 3 percent is hardly the stuff of recession). Third, a small number of people and companies are doing extremely well.

Depending on where you stand, you’re hearing very different things about the economy, but a pretty consistent theme is an administration that has not delivered on promises made to voters—while delivering to the president’s family and friends.

Under the Hood, the Story Gets More Complicated

It’s been a predictably rough year for the US economy. Tariffs have raised goods prices and hit manufacturing jobs, immigration crackdowns have crippled the labor force, and reversing energy policies dramatically has unwound an energy investment boom. As a result, the job market is softer, prices are still high, and inflation is up and apparently rising based on the data flow that has (finally) started to trickle back in.

That said, if the data are weaker, the economic mood of the country is, in a word, awful.Consumer sentiment in October was only exceeded by lows from the worst of the early 1980s recession, the peak of the 2022 inflation, and the months following the “Liberation Day” tariff announcement this year. Since January, consumer sentiment has plunged, giving up essentially all gains from a steady rise after the inflation peak of 2022.

That pessimism isn’t purely emotional—it reflects months of higher grocery and utility bills. In fact, across both the major household expectations surveys, families expect inflation to keep going up next year—which most economists expect as well. And roughly twice as many consumers surveyed by the Conference Board expect the jobs picture to be weaker rather than stronger in the next six months.

This view is both pessimistic and realistic given the data we’ve seen so far this year. It’s unmistakably true that the labor market and the inflation picture are weaker than last fall. What’s worrying to the wonkier economy watchers, however, is that the pressures on both inflation and unemployment are in the wrong direction. There are real risks that both inflation and the jobs picture could get worse, but (short of policy reversals) few predictable shocks are likely to make either improve in the near term.

Job growth has stayed positive but slowed dramatically, from an average 167,000 jobs a month in January to just 109,000 in September (and will likely be revised down further with annual revisions early next year). Over 87 percent of all jobs added this year are in health care and social assistance (a given in an aging country), while the rest of the economy has added just 71,000 jobs all year. And there’s little sign that tariffs are about to bring down prices, nor are there signs that the demand side of the economy is about to pick up.

It’s Not Great, but There’s Plenty of Time to Panic Later

The closer you are to the data, the less pessimistic you probably are right now. But, as we can see in recent Fed meeting minutes, the debate is largely between two camps: The first is those who think the labor market is middling and the risks of rising inflation are serious. The second is those who think the risks of rising inflation are less worrisome than the chances the labor market deteriorates further.

It’s clearly too soon to panic about a recession, and the best labor market data we have say things are holding up well by historical standards—September’s 4.4 percent unemployment is better than about 80 percent of months since 2000—it’s just that there’s little to suggest things are about to improve significantly.

That said, the economy continues to chug along on the strength of spending by resilient, yet quite frustrated, consumers. The final reading on second quarter GDP shows US consumer spending keeping the economy going, even as savings deplete.

Early holiday spending numbers look strong, so it seems like US consumers are going to muddle through tariffs. The distribution of consumer spending remains pretty narrow—high earners are doing much more of the broad-based spending in the economy

However, if you get your news from stock markets, or even from retirement statements, the world is different entirely, and much more optimistic—at least from a high level. After a massive swoon in April, the US stock market has had a great year, powered by tax cuts for corporations and the wealthy and an AI investment boom that looks bubble-like to some inside it.

Yet, like in the real economy, the more you dig into the data the farther from the extremes your views can go. Job and corporate earnings growth are concentrated in increasingly narrow slices of the economy. Corporate earnings are notoriously concentrated at this point, with the top 1.4 percent of S&P 500 companies accounting for almost all of stock market gains this year—just seven companies are now one-third of the value of S&P 500.

How Do We Square These Takes?

Overall, the data are on a more even keel than either the awful vibes most Americans are feeling from an affordability crisis or the anxiously warm vibes of investors. We’re not living through the economic boom tech investors see everywhere, nor the near-term dystopia consumers are feeling. The economy is weaker than last year and likely to continue to soften a bit more over the first part of next year, but the good news is at least for now things are not as bad in the data as in the headlines. The bad news is . . . that’s the good news.

The economic fortunes of mom-and-pop businesses are diverging from those of their larger counterparts — a pre-existing gap that now appears to be getting bigger, faster.

Why it matters:

The evidence is in the private-sector labor market, that in recent months, has been propped up by large companies as smaller firms — typically responsible for 40% of U.S. employment — shed workers.

The big picture:

Larger businesses have been able to adapt to a tough economic backdrop — historic tariffs, high interest rates and a more cautious consumer — in ways far more challenging for small companies with fewer resources.

“It’s evident that medium and large firms are better positioned to weather what’s going on,” said ADP chief economist Nela Richardson.

“They can set prices, they can change suppliers. They can hire contractors instead of permanent employees in a more sophisticated way. They can hire globally, not just in their local region. They have more tools in the toolbox,” Richardson said.

By the numbers:

The hiring gap between small and big businesses is getting worse, a fresh sign that small business firings are holding down jobs growth across the economy.

As we mentioned yesterday, the private sector shed 32,000 jobs in November, according to payroll processor ADP. Small firms — those with fewer than 50 employees — accounted for all of the losses.

Those businesses reported a net loss of 120,000 jobs, the most small businesses have cut since the pandemic’s onset. Larger businesses grew, but not enough to offset the cuts elsewhere.

“Small business hiring reallystarted to slow in April and I attribute some of this to tariffs and the higher cost of doing business that small companies are much less able to absorb,” Peter Boockvar, chief investment officer at One Point BFG Wealth Partners, wrote in a note.

“The natural reaction is to cut costs elsewhere and we know that labor is their biggest cost,” Boockvar added.

The intrigue:

Bloomberg recently reported that there are more small businesses filing for bankruptcy under a special federal program this year than at any point in the program’s six-year history.

Subchapter V filings, which allow firms to shed debt faster and cheaper, are up 8% from last year, according to data from Epiq Bankruptcy Analytics.

Chapter 11 filings — a process used by larger businesses — are up roughly 1% over the same time frame.

Threat level:

Main Street is bearing the brunt of an economic slowdown in ways that might make it even harder for small shops to compete with larger companies.

One bright spot: Despite that pain, applications to start new businesses — ones likely to employ other people — remain notably higher than in pre-pandemic times, according to the latest data available from the Census Bureau.

What to watch:

The Trump administration shrugged off the ADP data that indicated a hiring bust. Commerce Secretary Howard Lutnick told CNBC that the cuts were due to factors unrelated to tariffs, like immigration crackdowns.

That hints at a debate among monetary policymakers, who are trying to gauge how much weak jobs growth is a byproduct of fewer available workers.

But ADP had earlier told reporters that small businesses generally had less demand for workers — not that staff weren’t available for hire.

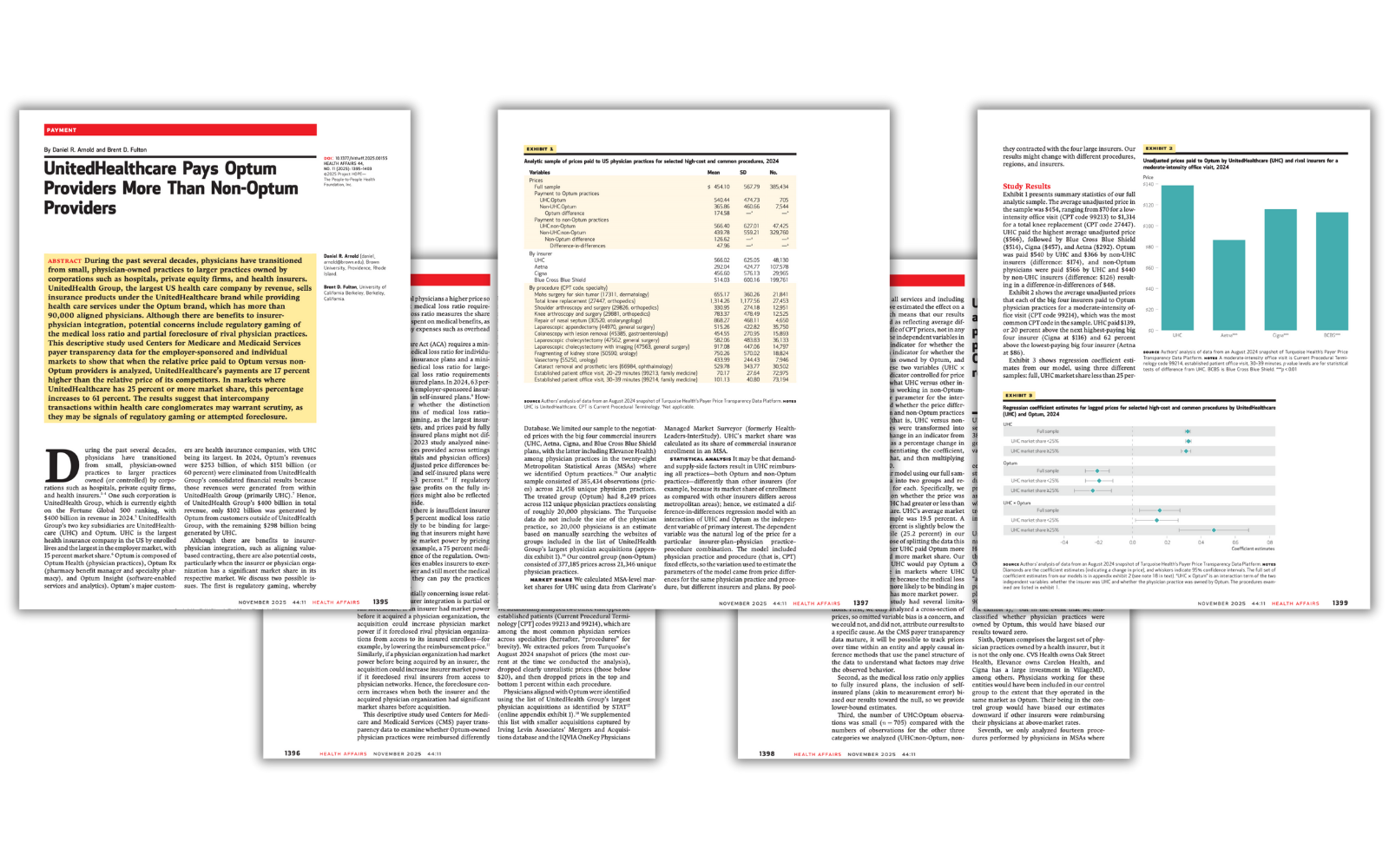

Research suggests UnitedHealth may be running a shell game — one that lets insurers flout regulations and obscure the harmful consequences of their vertical integration strategies.

A new Health Affairs study has confirmed that UnitedHealth Group — the nation’s largest health care conglomerate — is doing more than dominating the market; it’s playing by a different set of rules.

Researchers Daniel Arnold of Brown University and Brent Fulton of UC Berkeley analyzed new federal “Transparency in Coverage” data and found that UnitedHealth’s insurance arm, UnitedHealthcare, pays its own Optum physicians 17% more on average than it pays other doctors for the same services. And in markets where UnitedHealthcare holds a large share — 25% or more — that gap explodes to 61%.

The Affordable Care Act’s medical loss ratio (MLR) rule requires insurers to spend at least 80–85% of premium revenue on patient care, rather than on administrative expenses and profits, but if an insurer can funnel “medical spending” to its own subsidiaries — in this case, the thousands of subsidiaries that now comprise Optum — it can appear to comply with the law while actuallyshifting massive amounts of revenue from one pocket to another.

Under the MLR rule, insurers are required to send rebate checks to their customers if they don’t comply with the MLR requirement. The Health Affairs research suggests that UnitedHealth may be flouting that rule by deliberately overpaying the health care delivery operations it owns to comply with the letter of the law if not the intent. Because physician practices and other provider entities are exempt from the MLR rule, regardless of ownership, UnitedHealth can avoid sending its customers the rebates they otherwise would get and pad the conglomerate’s bottom line.

As the researchers put it:

“The results suggest that intercompany transactions within health care conglomerates may warrant scrutiny, as they may be signals of regulatory gaming or attempted foreclosure.”

Another way to game the system

This study also highlights another consequence: independent physician practices are being squeezed out. When UnitedHealth pays Optum doctors more — and non-Optum doctors less — it creates an uneven playing field that could drive small and mid-sized practices out of business.

The authors warn that this pattern “could lead to independent practices closing or joining larger groups such as Optum”. Over the past decade, Optum has quietly amassed more than 90,000 doctors under its control — more than any other private organization in the country.

And it’s not just doctors – UnitedHealth owns nearly 2,700 entities – a pharmacy benefit manager, a data analytics firm, home health companies and even surgery centers. The study notes that in 2024, Optum reported $253 billion in revenue, but 60% of that was simply money moving internally from UnitedHealthcare. In other words, UnitedHealth’s empire is built on being able to feed itself by self-dealing.

The point

This research provides some of the strongestevidence yet that UnitedHealth’s “vertical integration” strategy is distorting the market — not to improve care but to maximize profits under the guise of “compliance.”

For regulators at the Department of Justice, the Department of Labor (which has jurisdiction over employer-sponsored plans administered by UnitedHealth and other insurers) and the Centers for Medicare and Medicaid Services, this should be a wake-up call. As the authors conclude, even a 1% artificial price increase through these internal transfers could significantly reduce the rebates insurers owe consumers under the medical loss ratio rule. That’s billions of dollars that patients, taxpayers and employers are entitled to but that never leave the company’s bank account – except to reward shareholders and top executives. During just the first nine months of this year, UnitedHealth reported making nearly $19 billion in profits on revenues of more than $334 billion. Both revenues and profits likely would have been considerably less if not for the apparent gaming the Health Affairs researchers uncovered.

In what political pundits called a sweeping win by Democrats in Tuesday’s elections, affordability and costs of living emerged as the issues that mattered most to voters. It’s no surprise.

Since 2019 before the pandemic, prices have increased for American businesses and households due to inflation:

Personal Consumption Expenditures (PCE) inflation which measures monthly business spending increased 3.5% annually. The Consumer Price Index (CPI), which measures monthly changes in household spending increased 3.87% annually over the same period (2019-2025).

But in the same period, prices for healthcare services–hospitals, physician services, insurance premiums and long-term care–have taken an odd turn: for businesses, they’ve decreased but for consumers, they increased.

It reflects the success whereby businesses have shifted health benefits costs to employees or suspended benefits altogether, and it explains why consumers are bearing more direct responsibility for healthcare costs and are increasingly price sensitive.

A proper interpretation of PCE and CPI data points to a bigger problem: household exposure to increased prices hits younger, middle-income households hardest because their housing costs consume 36-60% of their disposable income. Food costs are an additional 13-20%. That doesn’t leave much room for healthcare when child care, student debt and transportation costs are factored.

Increased attention to household affordability and costs of living is uncomfortable in the healthcare industry. The good news is that expenses for health services represents a small fraction of spending; the bad news is those expenses are increasing along with competing categories and they’re sometimes unpredictable.

The fundamental operating model in healthcare is ‘Business to Business/B2B’ transactions between producers (physicians, hospitals, drug and device makers), middlemen (insurers, PBMs, employers) and users (consumers) reinforced by state and federal regulation that protect the status quo. And ‘users’ are treated as patients or enrollees, not a market that makes buying decisions based on value and costs. Thus, lack of price transparency in healthcare coupled with lack of predictability when services are used lends to public confusion or, in extreme cases, contempt. The public reaction to the murder of UnitedHealth Executive Brian Thompson last year surfaced the public’s latent animosity toward healthcare’s business practices that treat consumers as pawns on a complicated chessboard.

Shifting direct financial responsibility to consumers is the blunt instrument touted by economists who rightly argue informed decision-making by consumers is necessary to lower costs and improved value from the system. It won’t happen overnight if at all, and the system’s affordability in working age households will be the impetus.

The near-term implications are clear:

Increased household discretionary spending for necessities (food, transportation, and housing) will shrink discretionary spending for healthcare products and services:

Consumers believe their basic needs—food, shelter, transportation–are easier to predict and manage than their out-of-pocket bills for insurance premiums, co-pays, deductibles, over-the-counter products and more. 60% are financially insecure, and unanticipated medical costs is their biggest concern.

Consumers think the healthcare system is ‘dominated by ‘Big Business’ that prioritizes profit before everything else. The majority of consumers in every age, income, education, ethnic and partisan affiliated cohort share this view and are dissatisfied. Elected officials in both parties believe consolidation in health services has increased prices and reduced competition for consumers. The frontline healthcare workforce is demoralized by its corporatization and resentful of leaders they consider overpaid and accountable for financial results only.

Consumers (voters) will support policy changes to the health system that increase its accountability for affordability.

Among providers, momentum for price controls, price transparency, executive compensation limits, justification for tax exemptions, revenue cycle management practices, will be strong especially in state legislatures.

Among insurers, claims data accessibility, standardization & justification of coverage, denials, prior auth and network adequacy, premium pricing, administrative cost accountability, executive compensation, will be foci of regulation.

Among suppliers to the health services industry—drug companies, device makers, information technology solution providers, consultants and professional services advisors, supply chain middlemen et al—disclosure of business relationships and transparency re: direct and indirect costs will be mandated.

Final thought:

Throughout my career, ‘patient centeredness” has been the fundamental presumption on which service delivery by providers has been justified. Affordability has been neglected though increasingly acknowledged in rhetoric. Executives in healthcare services are not compensated for setting household affordability targets and publicly reporting results. Most compensation committees and Boards have marginal understanding of household economics in their communities and depend on “revenue cycle management” to address consumer payment obligations at arms-length. Even the medical community is not immune: one in 5 medical students is food insecure, 4 of 5 medical residents is financially insecure, and their career choices are increasingly dependent on their earning potential. So, calls for greater attention to affordability in healthcare will originate from insiders and outsiders tired of excuses and lip service.

Insecurity about household finances is significant and growing. Per the University of Michigan Index of Consumer Sentiment (50.3 in November 2025) is near an all-time low. It’s reality in the majority of U.S. households. The federal shutdown, discontinuance of SNAP benefits, cuts to ACA subsidies for insurance, corporate layoffs and higher costs for child care, groceries, gas and housing are a tsunami to American households.

Last week, voters elected: Zohran Mamdani, 34 (NYC); Abigail Spanberger, 46 (VA); and Mikie Sherrill, 53 (NJ) in races touted as a weather-vane for elections in 2026 and beyond. It is bigger than partisan elections. Voters in both parties and across the country are worried about affordability. It’s especially true among younger generations who worry about making ends meet and think institutions like the political system, higher education, organized religion and healthcare are outdated.

Healthcare service providers can ill afford to neglect affordability. It more than measuring medical debt, posting prices and referencing concern on websites. It’s about earning the trust and confidence of future generations through concrete actions that increase household financial security beginning with healthcare spending.

Paul

PS As never before, the voices of younger generations are being heard across the country though social media and demonstrations. The health system is among their major concerns as they ponder how they’ll be able to pay for their bills While Medicare seems the focus to policymakers and beltway pundits who rightly recognize seniors as its most costly population, the working age population has been taken for granted. Here’s a voice I follow closely. Fresh Perspective Is Sometimes Needed – by K. Pow

“The true character of society is revealed in how it treats its children.”- Nelson Mandela

Elected officials of both parties have proposed new and better government support for families with children. President Trump’s One Big Beautiful Bill Act includes some of these proposals, but overall, because of the law’s benefit cuts for working class and lower-income families, it will likely end up hurting roughly as many families with children as it helps.

Parts of the law increase help for families with children: The maximum Child Tax Credit was increased from $2,000 to $2,200 per child; however, the increase remains only partially refundable and thus will not be available to many low-wage working families. In addition, on a much smaller scale and with some questions remaining about its workability in practice, the One Big Beautiful Bill Act (OBBBA) created a new type of child savings, “Trump Accounts,” and a temporary program of $1,000 payments for each child born in President Trump’s presidential term. The adoption credit has also been improved. In each of these provisions, there are further changes that could enable these programs to help more children and more families.

However, many of the law’s most substantial changes will reduce help to children, particularly those in working class and poor families. The law imposes new legal and bureaucratic filing requirements to previously bipartisan programs, particularly the Supplemental Nutrition Assistance Program (SNAP, formerly known as “food stamps”) and Medicaid, that will keep many families from getting benefits, including benefits for which they are eligible.

Overall, OBBBA will likely end up reducing benefits for roughly as many families as it helps, with the greatest losses concentrated among the least well-off. By 2030 the 40% lowest-income households will experience a net loss on average, and the middle quintile will have roughly no net change; there will be ongoing net gains for the top 40% of households.

This note describes some key changes embedded in OBBBA, some related proposals by Democrats, and some improvements that might be made in the future.

Is child policy becoming bipartisan?

Politicians of both parties, who once made a show of kissing babies, have progressed to making a range of proposals to improve children’s lives and prospects. In some cases, perhaps frustrated by ongoing political polarization, they’ve chosen to support the same or similar approaches, including extra tax credits or actual payments for children and child savings accounts. For example, both Senator Ted Cruz (R-TX) and Senator Cory Booker (D-NJ) have proposed savings accounts be started for every child at birth.

Although the recently enacted OBBBA was in no way bipartisan, it included some proposals endorsed by both Republicans and Democrats. At the same time, however, the Act reduced the scope of the previously bipartisan SNAP safety net program and of Medicaid.

Furthermore, despite claims by representatives of both parties to support working families with children, the changes in OBBBA overwhelmingly help families that are already better off. After the temporary tax benefits end, roughly half of U.S. families will be worse off, with most benefits of the bill going to the top 40% of the income distribution.

Below, we discuss two kinds of assistance for families for children: those that provide immediate resources and those that support saving for children’s futures.

Money for children now: Child income tax credits, baby bonus checks

Congress has subsidized children through the tax code for at least a century, starting with dependent exemptions from income1 and following with the Earned Income Tax Credit in 1975 and the Child Tax Credit (CTC) in 1997. By far the most significant action benefitting some children in OBBBA is an increase in the CTC. However, most low-income children are excluded from these higher benefits. At the same time, the Act would dramatically reduce other previously bipartisan safety net programs that support low-income children, particularly SNAP.

Child Tax Credit

The CTC is a tax credit for families with children. It was originally conceived as an anti-poverty program, though for much of its history most of the CTC’s benefits have gone to middle class or wealthier families. The CTC phases in with earnings and the credit is only partially refundable, meaning that if the credit exceeds a filer’s tax liability, families can receive a portion of the credit as a tax refund. Approximately 60 million children benefit from the current credit. In response to the COVID-19 recession, for one year the credit provided families with as much as $3,600 per child and allowed low-earnings families to get the full benefit, but that expired and the maximum returned to the pre-OBBBA maximum of $2,000. Because of the phase-in and other limitations on refundability, an estimated 17 million children in families with low incomes receive less than the full $2,000-per-child credit or no credit at all.

OBBBA Changes

Under OBBBA, the maximum credit was raised to $2,200 per child and then indexed to inflation. Because the bill did not make any changes to the CTC’s refundability or phase-in with earnings, this change will not benefit any of the estimated 17 million children who were left out under pre-OBBBA law. Furthermore, the act’s increase in the standard tax deduction and other changes will increase the number of children whose families don’t get the full credit.

The OBBBA CTC expansion primarily benefits families with above average income. As this graph from the The Budget Lab shows, the bottom 40% receive little or no benefit.

CTC “Baby Bonus”: Make the full creditavailable for all newborns, so that every newborn child’s family would get the full credit for their first year. This could be considered a CTC-based “baby bonus”.

Allow full refundability as long as parent earnings are above the minimum ($2,500/year).

Allow full refundability for families with multiple children.

Adoption Credit

Under current law, adoption expenses of up to $17,280 per child can be credited against income taxes. In practice, few families get the full credit because the credit is nonrefundable and few families have an income tax bill greater than this amount.

OBBBA Changes

Under OBBBA2 up to $5,000 of qualified adoption expenses will be refundable, thereby increasing the available adoption credit for approximately 45,000 children per year.3

Possible Improvements

Congress could broaden the benefits of the adoption credit by reducing the total credit and increasing the refundable amount, e.g., reducing the maximum to $12,000 while increasing the refundable amount to $6,000.

Direct cash grants: “Baby Bonuses,” SNAP, etc.

Some observers, concerned about declining birthrates, have proposed a cash payment for newborns soon after birth. Although President Trump has expressed support for a $5,000 “baby bonus”, the administration made no specific proposal and none was included in any version of the OBBBA. (A baby bonus could be implemented via a change in the CTC, as described above.)

Important safety net programs affecting children were cut by OBBBA

There are many federal safety net programs that provide cash or in-kind benefits to families based on having children and the number of children. The largest near-cash program, SNAP, will be cut back very substantially by OBBBA. An Urban Institute report estimated that the SNAP cuts would affect 3.3 million families with children and reduce their benefits by an average of $840 per year.

With multiple rationales, policymakers with varying perspectives have concluded that children and their families would benefit from starting life with a nest egg, a savings account to be created early in a child’s life, to be then held and used well in the future for education, homebuying, or other purposes. States, cities, counties, and nonprofits have started programs that both establish child savings accounts and provide a starter contribution to those accounts. According to the Congressional Research Service, over 100 such programs had been started by 2023, in addition to the education savings account programs operated by many states under Section 529 of the Internal Revenue Code.

These programs draw from work in the early 1990s by academic Michael Sherraden which proposed a national program of “Individual Development Accounts” for the poor. This led to local programs in many cities and some states. A similar approach using the term “baby bonds” was proposed by scholars in 2010 as a means to reduce racial gaps in wealth, and this proposal was adapted into the American Opportunity Accounts Act introduced by Senator Cory Booker (D-NJ) in 2018. Under those proposals every child would receive a grant at birth, with additional government grants to children in poorer families in later years. Some child investment programs, such as New York City’s RISE program also incorporate philanthropic gifts.

The approach became bipartisan this year when Senator Ted Cruz (R-TX) proposed that each newborn child receive a one-time $1,000 grant in an “Invest America Account.” Cruz’s rationale was less about reducing wealth disparities and more that such accounts would give children a stake in the future and an understanding of investment markets. In place of ongoing government contributions, he proposed that parents, employers, philanthropies, and others could contribute to the child accounts. The Cruz proposal was, with modifications, adopted in OBBBA.

What are the benefits of child savings accounts?

Advocates of these accounts see several advantages. First, they note with some evidence that having a personal account early in life that can only be accessed later substantially increases a child’s and family’s interest in education and personal betterment. Some believe that these accounts will also improve financial literacy and understanding of the economy and investment.

Other advocates, noting that disparities in wealth are associated with differences in educational opportunities, attainment, and future income and that wide racial differences in wealth persist, believe these programs could reduce wealth disparities at the start of life. The original child savings programs focused on this rationale, with payments or participation incentives that favored the poor. There is research that finds higher wealth associated with better educational and health outcomes, as well as stronger protection against material hardship following disruptive events, suggesting that policies that facilitate wealth-building could have profound effects.

OBBBA’s Trump Accounts & $1,000 contribution pilot program

OBBBA permits4 the secretary of the Treasury and/or private financial institutions to offer “Trump accounts,” savings accounts for children under 18 that offer some limited tax benefits if invested and not used until age 18. Contributions to these accounts, limited to $5,000 per year from family members, would be taxed as ordinary income. In addition, there is a 10% penalty for withdrawals before age 59½, with certain exceptions for education, home buying, adoption, disaster relief, etc. Contributions are also permitted from employers, up to $2,500 per year, and as part of a general program from government or philanthropies supporting all children in an approved geographic area.

The act also creates a pilot program of $1,000 government grants for any child born in the years 2025-28 (with a Social Security number) if the parent or Treasury elects5 and if there is an account established for that child. Although the government funds to be provided are given only at birth and are generally much smaller than the CTC, if made universally available they will reach some poor families with children that the Child Tax Credit does not.

Will Trump Accounts work?

While both Republicans and Democrats have endorsed at least the outlines of child savings accounts and a universal starting grant, there are many potential supporters who have questioned the design of Trump Accounts as enacted by Congress. A comprehensive review of child savings accounts systems undertaken by the Aspen Institute’s Financial Security Program raised a series of challenges, only some of which were responded to by the Congress. The Aspen publication noted ominously that similar program in the U.K. had been regarded as a failure and had in effect “poisoned the well” so that other efforts were unlikely to be considered for many years. That may have been a warning for Trump accounts.

Making Trump Accounts and the $1,000 per newborn pilot program work will require:

Treasury to encourage all new parents to sign upfor (“elect”) the $1,000 grant and/or the Treasury can do so itself. OBBBA does not auto-enroll children. It requires either the parent or the Treasury to “elect” newborn participation in the grant program.

Treasury to establish and pay for the millions of accountsfor all newborns. Although the law permits private financial institutions to establish these accounts, in practice they are unlikely to do so on their own. The administrative costs of setting up millions of individual private accounts will be large and, after receiving the $1,000 initial grant, many families will conclude that they cannot afford further contributions. Private firms will see little benefit in maintaining millions of individual accounts holding $1,000 with little prospect for more contributions. For that reason alone, Treasury will likely need to set up the program at least initially, perhaps by managing the funds in a single investment pool and having the individual accounts administered centrally. Treasury may also have to subsidize at least part of account administrative costs.For those families that can afford additional contributions, the existing nationwide programs of tuition savings accounts (“529 Plans”) are likely to be preferred: Investment earnings within Trump Accounts will be taxed at the ordinary income tax rate (plus a possible 10% penalty unless used for approved purposes), whereas proceeds from 529 plans if used for tuition expenses are not taxed at all.

Possible changes

Since the program has the president’s name on it, Treasury is likely to make every effort to help Trump Accounts succeed and be widely adopted and used. Some changes have already been suggested:

Provide additional government contributions for children of less well-off working families.This could be done several ways: Under the approach proposed by Senator Booker, the government could make smaller grants annually to children in families below an income limit. Alternatively, this could be done by allowing a full refund of the Child Tax Credit regardless of income while requiring the increased refund be invested in a Trump Account or something similar.

Ensure that child savings don’t penalize other public support. Retirement accounts and tuition assistance 529 program savings are generally not considered assets in setting eligibility for SNAP and other programs, and they are given preferential treatment in determining student loans. Trump Accounts could get similar treatment, as the Aspen Institute working group proposed for early wealth building policies.

Consolidate the many different tax-favored savings accounts into a single account type.(Muresianu & Cluggish, 2025) Since the Trump accounts are in some respects tax-disadvantaged compared to 529 school savings and also to several retirement accounts, a way to ensure the success of the effort might be to incorporate those accounts into the Trump account program.

What’s the right balance between helping children now versus saving for the future?

Unsurprisingly, there are differences of opinion whether additional resources should be devoted to immediate financial relief (using the CTC or a child grant) or instead to child savings accounts and wealth building for the longer term. There are advocates of both approaches and both have been shown to benefit children and families. However, there isn’t yet enough experience with child savings accounts to form judgments about the appropriate balance of resources between them.

We can do better

Given the broad public support to help children and families with children, elected officials from both parties will claim their efforts do so. As the distinctly non-bipartisan experience with OBBBA shows, however, many programs fall short of the rhetoric: overall, OBBBA seems likely to harm as many families with children as it helps.

Future bipartisan efforts can and should do better, supporting all families with children, including those who are more in need.

“Value-based care” in UnitedHealth’s Optum division apparently means fewer doctors for fatter margins.

UnitedHealth Group announced last week that it plans to cut thousands of doctors from its network, a move CEO Stephen Hemsley said will increase profits for the country’s richest health care conglomerate.

UnitedHealth assembled a network of nearly 90,000 physicians across the country as it bought hundreds of physician practices, began managing the Medicaid program in many states and became the biggest Medicare Advantage company. It also owns one of the nation’s largest pharmacy benefit managers, Optum Rx.

Of those 90,000 doctors, the company says fewer than 10,000 are currently directly employed by UnitedHealth. The company has been gobbling up a broad range of medical facilities in recent years, buying or creating nearly 2,700 subsidiaries and gaining direct control or affiliation with 10% of doctors working in the U.S. in the process.

The announcement by Hemsley came during a third-quarter earnings call with investors last week, when UnitedHealth announced it made $4.3 billion in profit in the last three months by generating revenues of $113 billion.

Read more here on how they did that. Spoiler alert: It involves raising health care premiums and collecting billions more from the Medicare Trust Fund and seniors.

Hemsley said the company’s health care services division, Optum Health, needed to consolidate its physician rolls to improve its bottom line.

He passed questions about how that will be done to Optum’s CEO Patrick Conway, who said too many doctors in the network weren’t aligned with UnitedHealth’s business model, which he called “value-based care.”

“We are moving to employed or contractually dedicated physicians wherever possible,” Conway said.

Overseeing an empire that offers health insurance, pharmacy benefits and doctors who provide care and write prescriptions, UnitedHealth has become America’s third-richest company behind Walmart and Amazon. There are 29.9 million Americans enrolled in UnitedHealthcare’s commercial plans, 8.4 million in its Medicare Advantage plans and 7.5 million in state-run Medicaid programs.

In 2024, the company brought in more than $400 billion in revenue, according to its financial filings.

Americans’ health care premiums are expected to rise drastically in 2026 after climbing as much as 6% on average this year compared to 2024.

UnitedHealth’s decision to remove doctors from networks means that many of its patients will have to find new, in-network physicians unless they change their insurers.

UnitedHealth isn’t alone in taking steps to trim its medical expenses to boost its bottom line. Both CVS Health, which owns Aetna, the PBM CVS Caremark and more than 9,000 retail pharmacies, and Cigna, which owns the PBM Express Scripts, also told investors they are implementing plans to improve earnings next year.

CVS Health is just behind UnitedHealth at No. 5 on the country’s Fortune 500 list, bringing in nearly $373 billion in revenue last year. Cigna is 13th with $247 billion in revenue.

{kind=link}