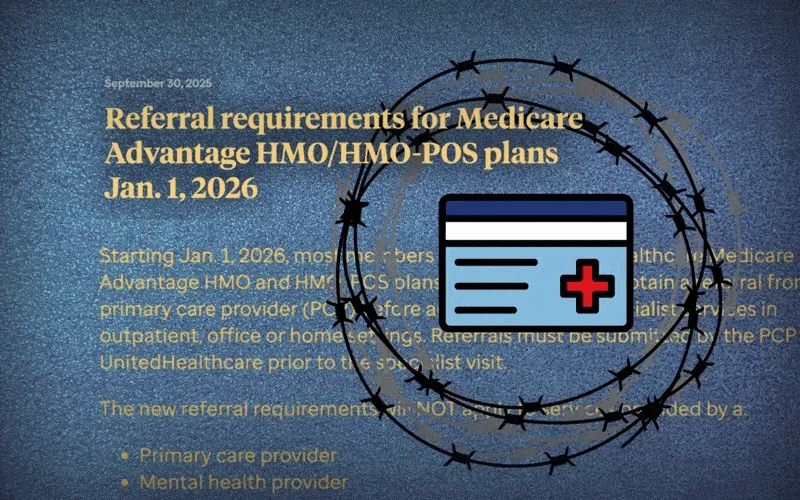

New referral requirement for HMO and HMO-POS plans alarms patients and doctors, who predict bureaucratic delays and reduced access to care.

Theresa Schwartz, a 66-year-old Milwaukee plumber, says she’s one of those people who never went to a doctor before she was 40. That has changed in the second half of her life as she has dealt with major health issues, including lung cancer and rheumatoid arthritis.

In recent years, her regular visits to the Milwaukee Rheumatology Center have been covered, without hassle, by her Medicare Advantage insurance provided through the nation’s largest health insurer, UnitedHealthcare. But Schwartz was surprised and became upset during her most recent visit there when she was told that — because of a new UnitedHealthcare policy — she will now need a referral from a primary care physician to be covered.

Schwartz said she’s never had a primary care physician.

“I’m just spinning the hamster wheel,” said Schwartz, who said in a phone interview that she is already confused and frustrated by the new policy and has little patience or interest in finding a UnitedHealthcare in-network physician. She even offered to pay cash for her visits, which the Milwaukee clinic said it cannot accept for Medicare patients.

Schwartz’s discontent over the new UnitedHealthcare policy — which launched at the beginning of the year, with reimbursements for visits without referrals to certain types of specialists set to stop after April 30 — is hardly unique. Health care advocates say the policy change affects a large pool of senior citizens in the insurer’s HMO and HMO-Point of Service (POS) Medicare Advantage plans. This is a healthy chunk of the estimated 8.5 million seniors who get their Medicare Advantage coverage through UnitedHealthcare — one of every four MA enrollees.

“I have patients in their 90s who are now facing this, if you can imagine,” said Nilsa Cruz, the tireless patient advocate for Milwaukee Rheumatology Center who frequently speaks out at the Wisconsin state capitol and elsewhere about health care issues. “And they don’t understand their insurance cards, anyway.”

Cruz predicted “a total disaster” when the UnitedHealthcare policy, which is currently in a sort of soft-launch mode, takes full effect in May, as both patients — many who’ve been seeing a specialist for 15 or 20 years without ever needing a referral — and their doctors struggle to adapt to an onerous new system.

The change, which is likely to have the effect of reducing specialist visits and thus saving UnitedHealthcare millions if not billions of dollars, isn’t taking place in a vacuum. Rather, it’s one more assault on seamless and efficient health care coverage. Patient inconvenience seems to be a cornerstone of this icon of Big Insurance’s plan for dealing with what its executives claimed last year were $6.5 billion in annual higher costs.

In recent months, UnitedHealthcare has dropped as many as 180,000 enrollees from its Medicare Advantage plans in targeted geographic areas and plans to drop more than a million by the end of this year. It has also “narrowed” its provider networks, relegating certain clinical practices, such as rheumatology clinics, which provide costly infusion therapies, to out-of-network status.

Some analysts had predicted a kinder, gentler UnitedHealth after a tragedy that made national headlines — the murder in New York of UnitedHealthcare CEO Brian Thompson in December 2024 — focused new attention on the company’s aggressive use of prior authorization to deny coverage for medically necessary care. Instead, the giant insurer has doubled down on ways to drive the highest-cost patients and providers from its system, making it necessary for millions of seniors to scramble to find either new MA insurers or new doctors. Many undoubtedly will go untreated.

The unwelcome requirement for many of UnitedHealth’s Medicare Advantage patients to get primary-doctor referral for treatments they’ve often been getting for years from a specialist looks to be one more way the company is nickel-and-diming a path back to higher profits on the backs of patients with chronic health issues.

Needless to say, UnitedHealthcare, whose financial performance has disappointed investors for more than a year, doesn’t portray the change that way. In announcing the move late last year the company hailed it as a way to improve communication between its affiliated providers and prevent unnecessary tests or procedures, or visits to a specialist that aren’t really necessary.

“The goal of this referral process is to help increase primary care provider (PCP) engagement with patients and help foster collaborative partnerships between PCPs and specialists,” is the upbeat jargon UnitedHealthcare used to explain the change on its provider portal.

Since Jan. 1, the change has been in what UnitedHealthcare considers “a trial period,” which means that while it wants patients to begin getting primary-care referrals before seeing certain types of specialists, visits without a referral are still covered for now. That will no longer be the case after April 30.

The policy does exempt more than a dozen specialists or types of visits — most notably oncology, as well as mental health treatment, physical therapy, and some other common medical treatments. It also won’t affect MA enrollees in California, Texas, and Nevada where referrals were already required.

Madelaine Feldman, M.D., the New Orleans-based immediate past president of the Coalition of State Rheumatology Organizations, said she imagines dire scenarios in which a patient with a sudden flare-up cannot get speedy treatment because of the inability to get a speedy referral, or visits that aren’t covered because the referral is mishandled.

“So the fact that UnitedHealthcare has decided that rheumatologists are not capable of deciding when a patient needs to be seen is ludicrous, capricious, and most importantly, dangerous,” Feldman said. She added that situations that are harmful for patient care “will be seen more and more as a result of policies enacted to improve UnitedHealthcare’s bottom line.”

But for people enrolled in the company’s HMO and HMO-POS Medicare Advantage plans, the new policy seems less a way of improving communication than an additional and unwanted barrier to receiving care.

“Today I found out about it, and I don’t think it’s fair,” said Pamela Matias, a 63-year-old infusion-therapy patient at the Milwaukee Rheumatology Center who filmed a video after learning of the change. “I’ve been getting this medication for 20 years and never needed a referral.”

Unlike Schwartz, Matias does see a primary care doctor, but she still worries that the extra hassles of getting a referral — and making sure it goes through properly — have longtime rheumatoid arthritis patient alarmed. “Without my medication, I would not be able to walk,” she said. “I’ll be in 100% pain all day long.”

Cruz, the center’s patient advocate, said that during this trial period, it’s not just patients who are disoriented. An early problem she’s seen with the program is that doctors’ offices are often faxing or attempting to call in patient referrals when UnitedHealthcare is only recognizing those that are made electronically through its online portal. What’s more, she said doctors need to specify how many visits are covered during a six-month window.

Cruz said even one of the largest health care practices in Wisconsin was improperly faxing the referrals. “I think they were faxing up until the other day — you know, a month and a half, almost, into this thing,” she said. “So that tells you something. Andrimary care physicians were not all fully informed.” Even if they are trained, primary-care doctors don’t always know how many specialist visits a patient will need until they are reevaluated by the specialist and begin their treatments.

If doctors don’t understand the new UnitedHealthcare policy, she worries, then how will elderly Medicare patients — including some with major disabilities — be able to follow the rules? Furthermore, if a patient’s current primary-care doctor retires or relocates, it often takes months in today’s frenzied health care environment to get an appointment with a new one, which could delay critical care.

As a rabble-rousing patient advocate, Cruz seems somewhat ahead of the curve in anticipating a crisis. Many specialists are just beginning to absorb the changes and won’t feel a real impact until May, when UnitedHealthcare stops paying specialists for their patients who didn’t obtain referrals.

But Cruz said she is already lobbying the Coalition of State Rheumatology Organizations, where she is a highly active member, to take a stand against UnitedHealthcare’s new policy, noting that it targets only the lowest-cost Medicare Advantage HMO plans and not the higher-end PPO policies, let alone its commercial insurance customers. To her mind, that is discrimination. “They’re doing the HMO — the sickest patients,” she said. “The sickest.”

This and other moves from UnitedHealthcare and its competitors have the effect of pushing the sickest and most expensive patients off their rolls, either by dropping customers outright or making it harder for them to access the medical care they so desperately need. Forcing sick people to make extra doctor visits to get treatment undoubtedly will cause many to delay or even forgo care — which, sadly, seems to be what UnitedHealthcare is going for as it tries to get back into Wall Street’s good graces.