Key Takeaways:

- 2026 is a pivotal year for U.S. healthcare.

- Structural, regulatory and competitive changes will alter the landscape.

- 10 areas will likely be the foci.

Last week…

- the stock market took a dive largely due to tech company volatility resurrecting fears of an A.I. bubble.

- reports from the Departments of Labor and Commerce confirmed mixed signals about the economy: job growth was relatively strong but inflation (3%) remained stubbornly above its 2% target and consumer confidence slid.

- Target warned Black Friday sales later this week will likely signal softness in consumer spending, and

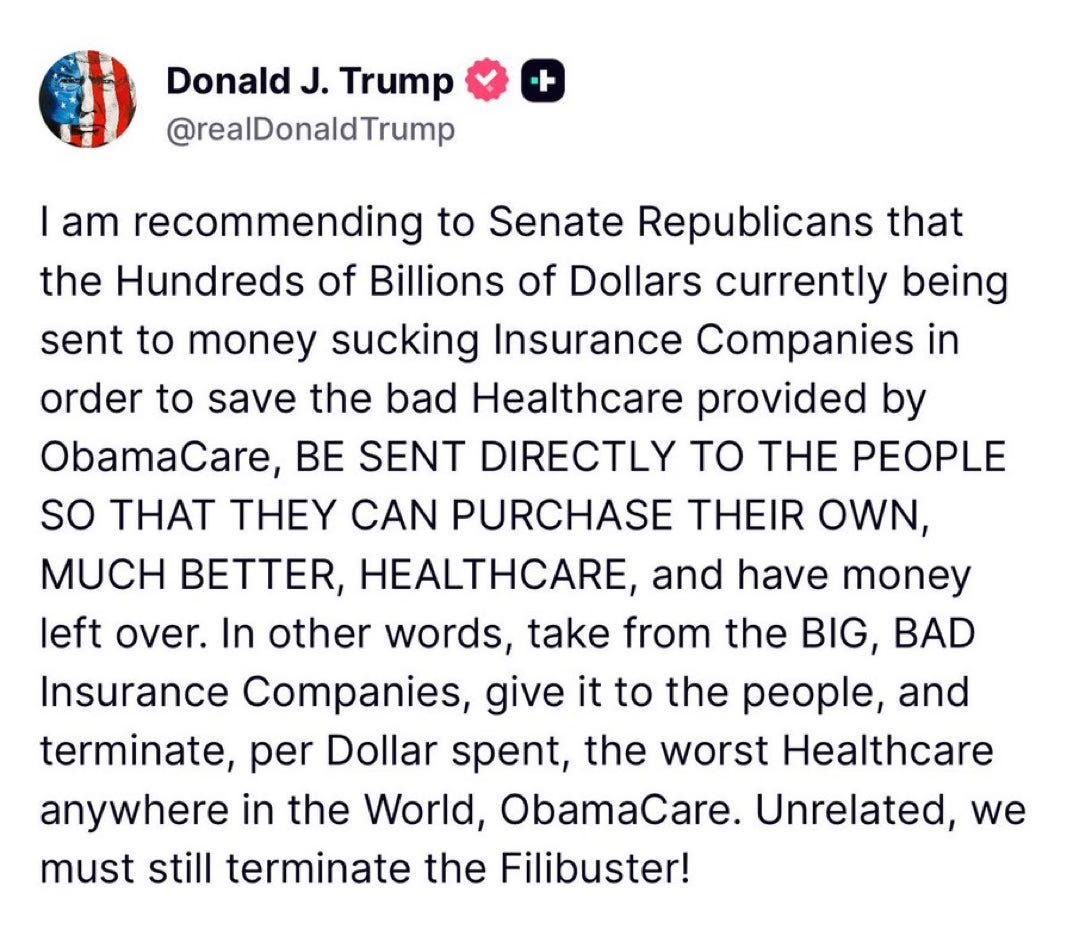

- Congress returned to DC after its 43-day shutdown that ended with no agreement on extension of insurance tax credits that expire at year end.

This week, Thanksgiving will likely slow down things on the U.S. domestic front but not for healthcare. Unlike just about every other industry in the economy, we operate 24/7/365. And like some industries, demand for our services is hard to predict– acts of God, accidents, court decisions, regulatory policy changes, social media “experts” et al. make predictions educated guesses at best. New technologies, clinical innovations, A.I. and private capital keep planners off-balance. Short-terms plans are more defensible; longer-term plans more challenging.

Thus, the industry is understandably focused on 2026. Here are assumptions:

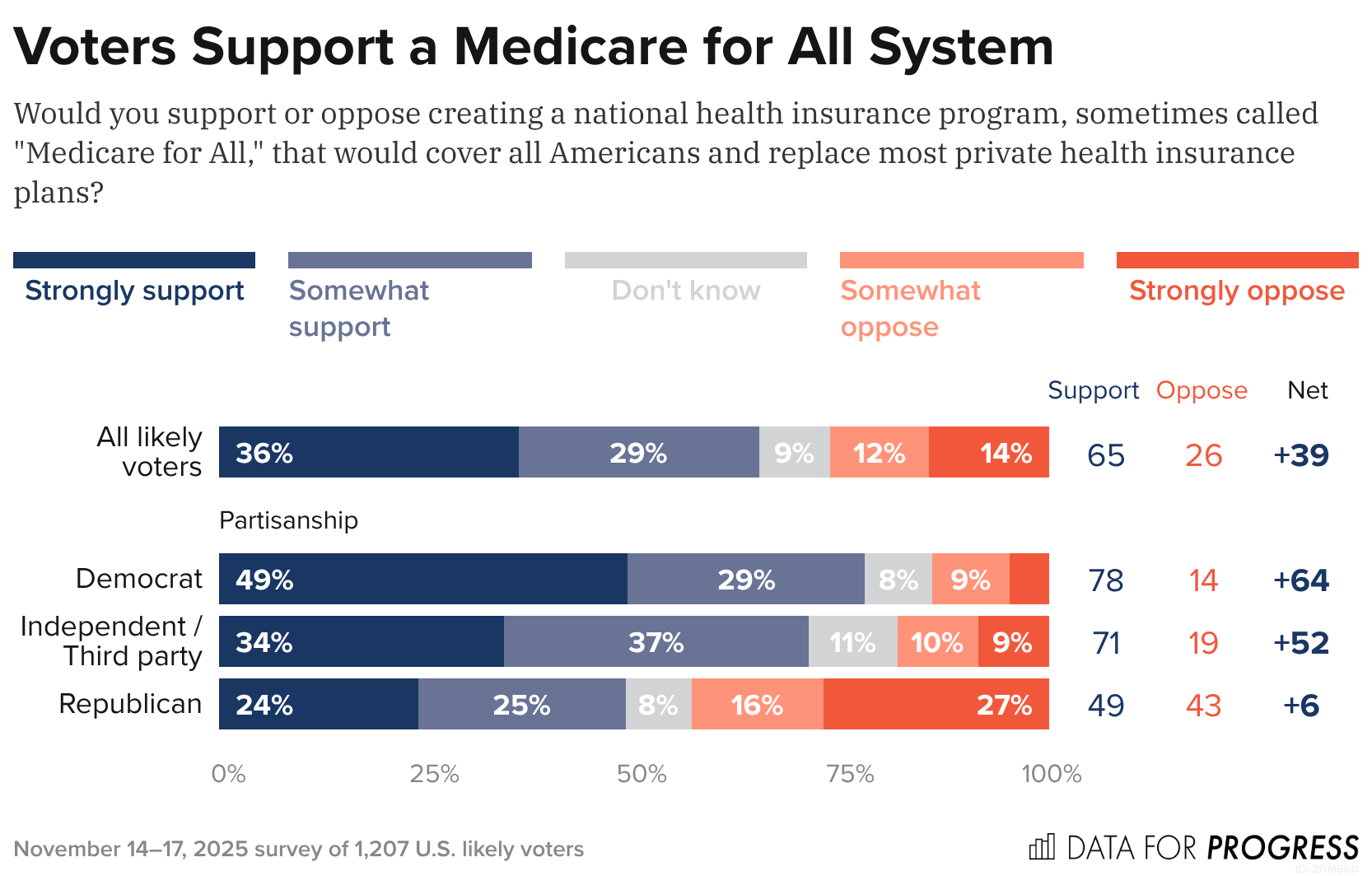

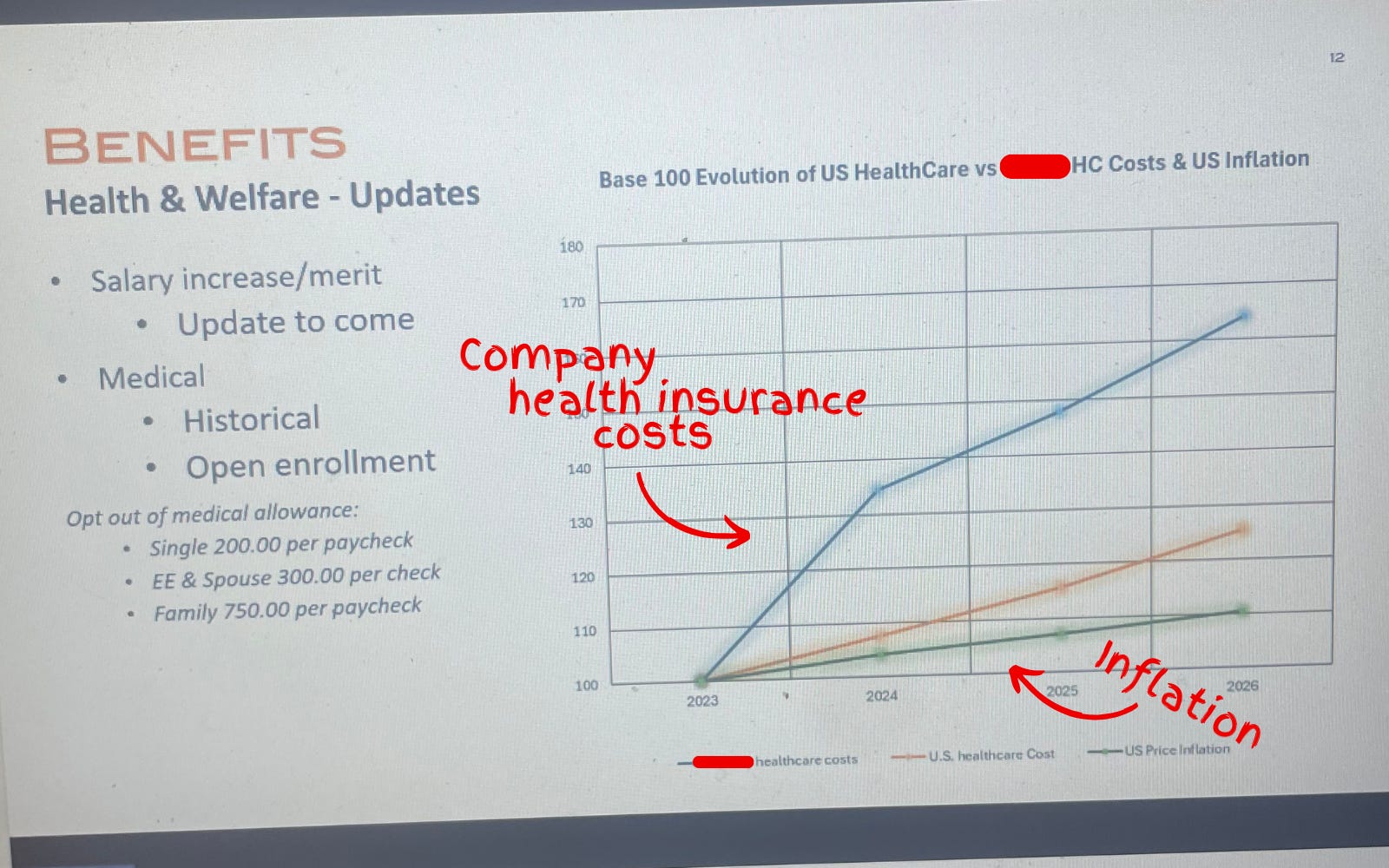

- Affordability for groceries, transportation, housing and healthcare (premiums and out-of-pocket) will drive media attention, public opinion and voting November 3, 2026.

- Congress will not extend tax credits that expire at year-end prompting a spike in the uninsured and under-insured populations. In tandem, large private insurers will raise premiums and increase leverage with providers to reduce competitive threats.

- Media coverage of healthcare will feature sensationalism, soundbites and hyper-simplification: costs (affordability), prices, disparities, executive compensation, outcomes, community benefits, workforce dissatisfaction, profitability and business practices will be foci.

- Warfare between hospitals, insurers, and drug manufacturers will intensify. Each will assert their systemic reform proposals serve the greater good best by protecting themselves against unwelcome threats.

- States will be the epicenters of health system transformation. Federal changes will be paralyzed by partisan-brinksmanship and posturing for 2026 and 2028 elections.

- Trust and confidence in the health system will decrease (further) to record levels of discontent.

And, reflecting on the current state of affairs in U.S. healthcare, here are 10 healthcare headlines you MIGHT see next year:

- Employed physicians win class action challenge to hospital employment agreements citing clinical independence, excessive administrative costs concerns

- IRS cuts not for profit health systems tax exemptions. Private investments, community benefits, executive compensation cited

- UnitedHealth Group completes acquisition of HCA: sets stage for new era of competition in U.S. healthcare

- EPIC completes interoperability agreement with CMS: public-private oversight board named

- Congress passes most favored nation pricing for biologics, specialty drugs as states enact price controls

- Large employers drop employee coverage due to costs, systemic flaws in system

- Health and wellbeing services consolidated under HHS to integrate social services and health

- Primary care physicians, nurse practitioners, community pharmacists launch national society to advance primary and preventive health services

- CMS capitates, expands primary care services in restructured MSSP program

- National coalition launched to design transformed system of health that’s accessible, affordable, comprehensive, efficient and effective

And, I’m confident, many others.

2026 is a mid-term election year. In 2016 (Trump 45 Year One), Republicans controlled 31 governorships and 68 legislative chambers. This January, the GOP will control 26 governorships and 57 legislative chambers– a 15% reduction on both. Politics is divided, affordability matters most to voters and healthcare is a high-profile target for campaigns so humility, thoughtful messaging backed by demonstrable actions will be an imperative for every healthcare organization.

2026 is a HUGE year for U.S. healthcare. The outcome is unknown.