Cartoon – I don’t want to change

It is easier than ever to buy stuff. You can purchase almost anything on Amazon with a click, and it is only slightly harder to find a place to stay in a foreign city on Airbnb.

So why can’t we pay for health care the same way?

My research into the economics of health care suggests we should be able to do just that, but only if we say goodbye to our current system of private insurance – and the heavy administrative burden that goes along with it. Republican efforts to repeal the Affordable Care Act (ACA) would take us in the wrong direction.

In a way, the reason buying health care is different than shopping for a garden gnome or short-term apartment seems obvious. Picking the right doctor, for example, involves a lot more anxiety and uncertainty and concerns matters of life and death.

But that’s not really the reason we can’t purchase health care the same way we buy an iPhone. In 1969, this would almost be true (for a rotary phone anyway). Back then, the bill for a birth in a New Jersey hospital looked a lot like the receipt you’d get for buying pretty much anything else: customer name, amount and a box to be checked for payment by check, charge or money order.

Today, paying for even the simplest office visit can become a nightmare, requiring insurance preauthorization, reimbursements adjusted for in-network or out-of-network copays and deductibles and the physician “tier” (or how your prospective doctor is evaluated for cost and quality by the insurance company).

Prescriptions require even more authorizations, while follow-up care necessitates coordinated review – and it goes without saying that many forms will have to be completed. And this doesn’t end when you arrive at the doctor’s office. A large chunk of any visit is spent with a beleaguered nurse, or even the physician, filling out a required checklist of insurance-mandated questions.

The growing complexity of health care finance explains why it’s becoming more and more expensive even though there has been little or no improvement in quality. Since 1971, the share of our national income spent on health care has doubled.

We can blame a significant part of the soaring cost of health care on the ever-increasing burden of administrative complexity, whose cost has climbed at a pace of more than 10 percent a year since 1971 and now consumes over 4 percent of GDP, up from less than 1 percent back then.

So if the rising cost of administration is a primary force driving health care inflation, why don’t we do something about it?

That’s because administrative complexity and waste are no accident but rather are baked into our private health insurance system and made worse by continuing attempts to use competitive market processes to achieve social ends other than maximizing profit.

Paying a doctor was relatively simple in the 1960s. Most people had the same insurance policy, issued by Blue Cross and Blue Shield, which back then was a private company but operated like a non-profit under strict regulation.

But in hopes of controlling steadily rising costs, policymakers encouraged insurers besides Blue Cross to enter health insurance markets, beginning with the HMO Act of 1973. The proliferation of for-profit companies with competing plans raised billing costs for health care providers, which now had to submit claims to a multitude of different insurers, each with its own codes, forms and regulations.

Not only that, but insurers quickly discovered the dirty secret of health care finance: Sick people are expensive and make up most costs, while healthy people are profitable.

In other words, the vital lesson for an insurer looking to make money is to identify the few sick people and get them to go away (“lemon dropping”) and find the healthy majority and do things that attract them to your plan (“cherry picking”).

Insurers are happy to offer discounts on fitness club memberships to attract healthy people, for example. But they punish the sick with higher copays and deductibles, as well as increasingly restrictive and intrusive regulations on preauthorization.

Economists call it adverse selection. Regular people call it paperwork hell. Whatever the name, it’s the purpose of increasingly complicated insurance plans and reimbursement forms.

The public and government authorities figured this out quickly, but too often the cures have been as bad as the disease.

We could, and I believe should, have abandoned the use of for-profit private insurance to adopt a simple single-payer system, in which a government agency would provide coverage to everyone in the U.S. Instead, in forging the ACA and in every other health reform enacted in the past 40 years, policymakers decided to work with private insurance while trying to fix some of its evils.

We adopted the “Patient’s Bill of Rights” around the turn of the century and created processes to allow patients and providers to appeal medical decisions made by insurers. State health commissioners now have considerable power to supervise insurers, while the ACA mandates certain essential benefits be provided in all insurance plans.

Yet each of these efforts to protect the sick from abuses inherent in the for-profit insurance system only added to the administrative burden, and the costs, on the entire industry.

Some perceived the problem as a lack of market competition so governments freed hospitals and other health care providers from regulations on prices and restrictions on mergers, advertising and other practices. Far from reducing administrative complexity or lowering prices, research has shown that deregulation made both problems worse by allowing the formation of networks of hospitals and providers who use advertising and other business and financial practices to **control markets and stifle competition.

Simply put, each attempt to fix a problem has led to more administration because we have kept intact the system of private health insurance – and for-profit medicine – that is at the root of at the dual problems of rising health care costs and growing complexity.

Clearly, our experiment in market-driven health care has gone awry.

Before we introduced competition and deregulation into health care, things were relatively simple, with most revenue going to providers. We could save a lot of money if we went backwards and adopted a single-payer system like Canada’s, where insurers do not engage in systematic preauthorization or utilization review and hospitals and pharmaceutical companies do not form monopolies to profit at the expense of the public.

Largely by reducing administrative costs within the insurance industry and to providers, a single-payer program could save enough money to provide health care to all Americans.

Compared with Canada’s single payer system, American doctors and hospitals have nearly twice as many administrative staff workers.

So whether the ACA remains in force or it’s replaced by something else, I believe we won’t be able to control health costs – and make health care affordable for all Americans – until we revamp the system with something like single payer.

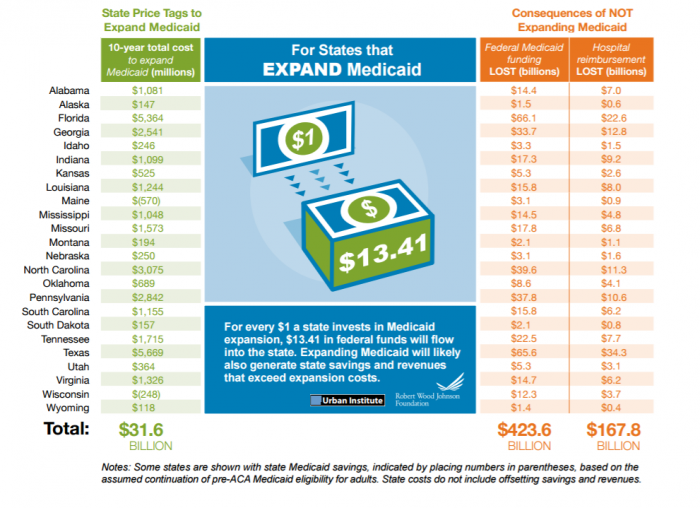

California risks losing $114.6 billion in federal funds within a decade for its Medicaid program under the Senate health care bill, a decline that would require the state to completely dismantle and rebuild the public insurance program that now serves one-third of the state, health leaders said Wednesday.

The reductions in the nation’s largest Medicaid program would start at $3 billion in 2020 and would escalate to $30.3 billion annually by 2027, according to an analysis released by the state departments of finance and health care services.

“It is not Medicaid reform,” Jennifer Kent, director of the state Department of Health Care Services, said in an interview. “It is not entitlement reform. It is simply a huge funding reduction in the Medicaid program. We are deeply concerned what that means for the long-term viability of the program as it stands today.”

Medicaid covers a staggering 13.5 million low-income Californians — children, people with disabilities, nursing home residents and others. About 3.8 million of them, many of whom are chronically ill, became eligible for coverage under the Affordable Care Act, informally known as Obamacare.

California would face the biggest losses of any state, according to a report issued Wednesday by the consulting firm Avalere Health. Federal funding would drop by 26 percent over 10 years, the report said. Many states, including Alabama, Georgia, Texas and Florida, would face a drop of less than 10 percent.

The Senate bill to repeal and replace the ACA would be a “massive and significant fiscal shift” of responsibility from the federal government to states, according to the analysis. It would force difficult decisions about who and what to cover and how much to pay doctors, hospitals and clinics, the report said.

In addition to expanding its Medicaid population early and vigorously under Obamacare, the state began covering undocumented immigrant children last year. California’s program, known as Medi-Cal, also provides dental care and other services that are optional under federal Medicaid rules.

The state’s Medicaid director, Mari Cantwell, said Republican proposals present a fundamental problem that can’t be solved by making cuts around the edges.

“Nothing is safe — no population, no services,” Cantwell said. “It is really disheartening and honestly horrifying to think about the world under this Senate bill and what it would mean.”

Healthcare CEOs made the rounds of news shows in this week to air their grievances with the Better Care Reconciliation Act, the Senate GOP bill intended to replace Obamacare.

The American Hospital Association, American Medical Association, AARP, and several other organizations have registered their opposition to the proposed bill.

But, it’s healthcare CEOs who are working to mitigate the anticipated changes who are anticipating how the proposed legislation would affect their organizations.

Among healthcare chief executives weighing in on the topic in recent days are Cleveland Clinic CEO Toby Cosgrove, MD, New York Presbyterian CEO Steven J. Corwin, MD, and Kaiser Permanente CEO Bernard Tyson.

Cleveland Clinic CEO Toby Cosgrove

With the anticipated greater numbers of uninsured patients coming into hospitals, “you’re going to have hospitals that are in very deep financial trouble,” Cosgrove told CNBC’s “Squawk Box” on Wednesday. “And this is particularly true of rural hospitals and safety net hospitals, which are very dependent on Medicare and Medicaid for their returns.”

As he sees it, legislators are not looking at the “root cause of the problem.” It’s not how you divide the money,” he said. “The problem really is the rising cost of healthcare.”

“I think if we came together and dealt with the root cause there’d be plenty of money to go around to look after people,” Cosgrove said. “But if we don’t deal with it now, we’re going to have the same problem going 10 years from now.”

“We’re really headed in the wrong direction,” Cosgrove said. We’re talking about payment reform; we’re not talking healthcare reform.”

Kaiser Permanente CEO Bernard J. Tyson

Bernard J. Tyson, chairman and CEO of Oakland, Calif.-based Kaiser Permanente, wrote in a LinkedIn post that although the ACA – also known as Obamacare – is an imperfect legislation, future healthcare reform must build on its progress, rather than undo it.

“We need to pause and ask policymakers to answer the most fundamental question: What does progress on healthcare look like for the people in America?”

In his view, it should cover more people, not fewer people; be affordable.

Without question, we must make healthcare more affordable; provide the best quality of care and best health outcomes.

Tyson points out that the U.S. has among the poorest health outcomes compared to the other developed nations. The healthcare industry can improve quality if “we commit to moving from a predominantly ‘sick care,’ episodic, fee-for-service model to a predominantly preventive model with incentives for value, integrated care and, most important, keeping people healthy.”

“The draft bill does not expand coverage; it does not do enough to protect people in need of care, nor does it provide enough assistance to those who need help in paying for health care and coverage,” he writes.

NewYork-Presbyterian CEO Steven J. Corwin

Speaking to Bloomberg on Tuesday, Steven J. Corwin, CEO of NewYork-Presbyterian said, “Just remember this: One in three children in this country is insured by Medicaid. One in three.”

Corbin noted that two-thirds of the expense of Medicaid are for people who are in nursing homes.

“So, you can work all your life, be a grandma, or ma, and then go through your assets, and then you have to be on Medicaid to go into a nursing home,” he said. “This is going to be devastating to so many people.”

Asked whether he would prefer having something concrete done in Congress or just see the proposed bill go away, Corbin said: “I’d like to see it go away. And, I’d like to see the Medicaid expansion remain, and I’d like to see the insurance market stabilized.”

The future of the Affordable Care Act is up for debate after Donald Trump’s surprise victory, but value-based care is likely to remain a guiding force in the healthcare industry.

Love it or loathe it, the United States is headed for four years of drastic policy changes under a Donald Trump administration, giving lawmakers another good chance to repeal, replace, or revise the Affordable Care Act.

The landmark healthcare legislation was the centerpiece of one of the most contentious campaigns in American history. Staring down anticipated premium hikes of up to 25 percent on the public health insurance exchanges, millions of concerned citizens voted for the candidate they felt was most likely to make positive changes to a system that has never quite managed to address their needs.

The impact of a Republican Congressional majority, a Republican President, and a vacant seat on a Supreme Court that already struck down one of the ACA’s major provisions is as of yet unknown, but a conservative twist to our national drama will certainly bring the future of the healthcare coverage framework into question.

For healthcare provider organizations, the plot will thicken even further. Thanks to provisions that require payers to cover patients with preexisting conditions and adhere to premium caps that have reduced their profitability, the ACA has incentivized a quick shift towards value-based care.

Eager to trim costs, pay for fewer services, and attract as many patients as possible in a competitive and confusing marketplace, payers have incentivized providers to abandon the traditional fee-for-service reimbursement structure and look to population health management strategies as a way to stem the financial bleeding.

Will significant changes to the Affordable Care Act free up payers to return to more lucrative business practices, or will commercial insurers, Medicare, and Medicaid stay the course?

How can healthcare providers position themselves for success in what will undoubtedly be another turbulent episode in the healthcare saga, and what are the nation’s options for developing a new path forward while still delivering the best possible care to its patients?

The number of consumers failing to pay full patient financial responsibility to hospitals increased 15 percentage points from 2015 to 2016, a study showed.

About 68 percent of patients with medical bills of $500 or less did not fully pay their patient financial responsibility to hospitals in 2016, according to a recent TransUnion Health study.

The proportion of individuals failing to pay off full medical bill balances increased from 53 percent in 2015 and 49 percent in 2014.

“There are many reasons why more patients are struggling to make their healthcare payments in full, the most prominent of which are higher deductibles and the increase in patient responsibility from 10% percent to 30 percent over the last few years,” stated Jonathan Wiik, TransUnion Principal for Healthcare Revenue Cycle Management. “This shift in healthcare payments has been taking place for well over a decade, but we are seeing more pronounced changes in how hospital bills are paid during just the last few years.”

• 63 percent of hospital medical bills were $500 or less between 2014 and 2016 and 68 percent of these bills were not paid in full by 2016

• 14 percent of hospital medical bills between 2014 and 2016 were $3,000 or more and hospitals did not receive full patient financial responsibility for 99 percent of the bills in 2016

• 10 percent of hospital medical bills were between $500 and $1,000 from 2014 to 2016 and patients did not pay the full balance on 86 percent of them in 2016

The TransUnion Health analysis confirmed that as patient out-of-pocket costs increase, hospital patient financial responsibility collection rates drop. A recent Crowe Horwath study also revealed that patient collection rates for accounts with balances exceeding $5,000 were four times lower than patient collection rates for accounts with low-deductible health plans.

For patient balances between $1,451 and $5,000, hospitals reported a 25.5 percent collection rate. In contrast, hospitals saw collection rates drop to just 10.2 percent for patient balances between $5,001 and $7,500.

Consequently, patients are more likely to partially pay hospitals for their financial responsibility. The TransUnion Health analysis showed that the proportion of individuals making partial payments toward their hospital medical bills rose from about 89 percent in 2015 to 77 percent in 2016.

Hospitals may see these patient collection trends continue, researchers stated. They projected the percentage of individuals neglecting to fully pay their patient financial responsibility to grow to 95 percent by 2020.

Researchers pointed to the popularity of high-deductible health plans as the primary driver of increased hospital patient collection challenges. In 2015, almost one-quarter of all workers belonged to a high-deductible health plan with a savings options versus just 8 percent in 2009, a 2016 Health Affairs blogpost stated.

The number of employees enrolled in high-deductible health plans is likely to increase, the blogpost continued. More than four of ten employers are considering offering only high-deductible health plans over the next three years.

Provider organizations continue to feel the pressure from increased patient financial responsibility under high-deductible health plans. About 72 percent of providers in a recent InstaMed survey cited patient financial responsibility and collection as their top healthcare revenue cycle management concerns in 2016.

The greatest challenge impacting healthcare revenue cycle management was the growth of patient financial responsibility with 29 percent of respondents, followed by cash flow issues with 21 percent, longer days in accounts receivable with 14 percent, and rise in bad medical debt due to insufficient patient collections with 8 percent.

With unpaid patient financial responsibility reducing hospital revenue, TransUnion Health researchers reported that hospitals wrote off about $35.7 billion as bad medical debt or charity care in 2015. Although overall uncompensated care costs declined in 2015, they added.

“Higher deductibles and the increase in patient responsibility are causing a decrease in patient payments to providers for patient care services rendered,” stated John Yount, TransUnion Vice President for Healthcare Products. “While uncompensated care has declined, it appears to be primarily due to the increased number of individuals with Medicaid and commercial insurance coverage.”

Warren Buffett is attacking the Republican Party’s plans to repeal and replace ObamaCare, claiming bills in the House and Senate would provide tax cuts for the rich.

Legislation passed by the House, he said, should be called “Relief for the Rich Act.”

Buffett, one of the wealthiest men in the country, claimed his tax bill would have been reduced by $679,999, or 17 percent, from the House bill.

“There’s nothing ambiguous about that. I will be given a 17 percent tax cut. And the people it’s directed at are couples with $250,000 or more of income. You could entitle this, you know, Relief for the Rich Act or something,” he said in an interviewwith PBS.

Buffett made the comments are a question about the GOP plan to do away with an ObamaCare surcharge on people earning a higher income.

Buffett also suggested that the bill would give many lawmakers a tax cut.

The annual salaries for lawmakers are much lower, he noted, at around $174,000 a year.

“But most of them have — if you look at the disclosures, they have substantial other income,” he said.

“If they get to higher than $250,000, as a married couple, or $200,000 as a single person, they have given themselves a big, big tax cut, if they — if they voted for this.”

The Senate on Tuesday decided to delay action on their draft healthcare bill until after the July 4 recess following criticism from conservatives and centrists in the conference.

https://www.axios.com/what-we-know-about-the-senate-health-care-bill-2-0-2450356848.html

What we’re hearing:

What’s becoming a big problem: Cruz is pushing to allow insurers offering ACA-compliant plans to also offer non-compliant plans, which wouldn’t be required to meet the ACA’s pre-existing conditions protections or other insurance regulations. Cruz wants to include that in the revised bill to cut the cost of individual insurance, and says sick people could still get subsidies that would protect them from premium hikes.

But that’s off the table, senior GOP aides say, because most Republican senators have already decided they don’t want to undermine the ACA’s pre-existing condition protections in any way.