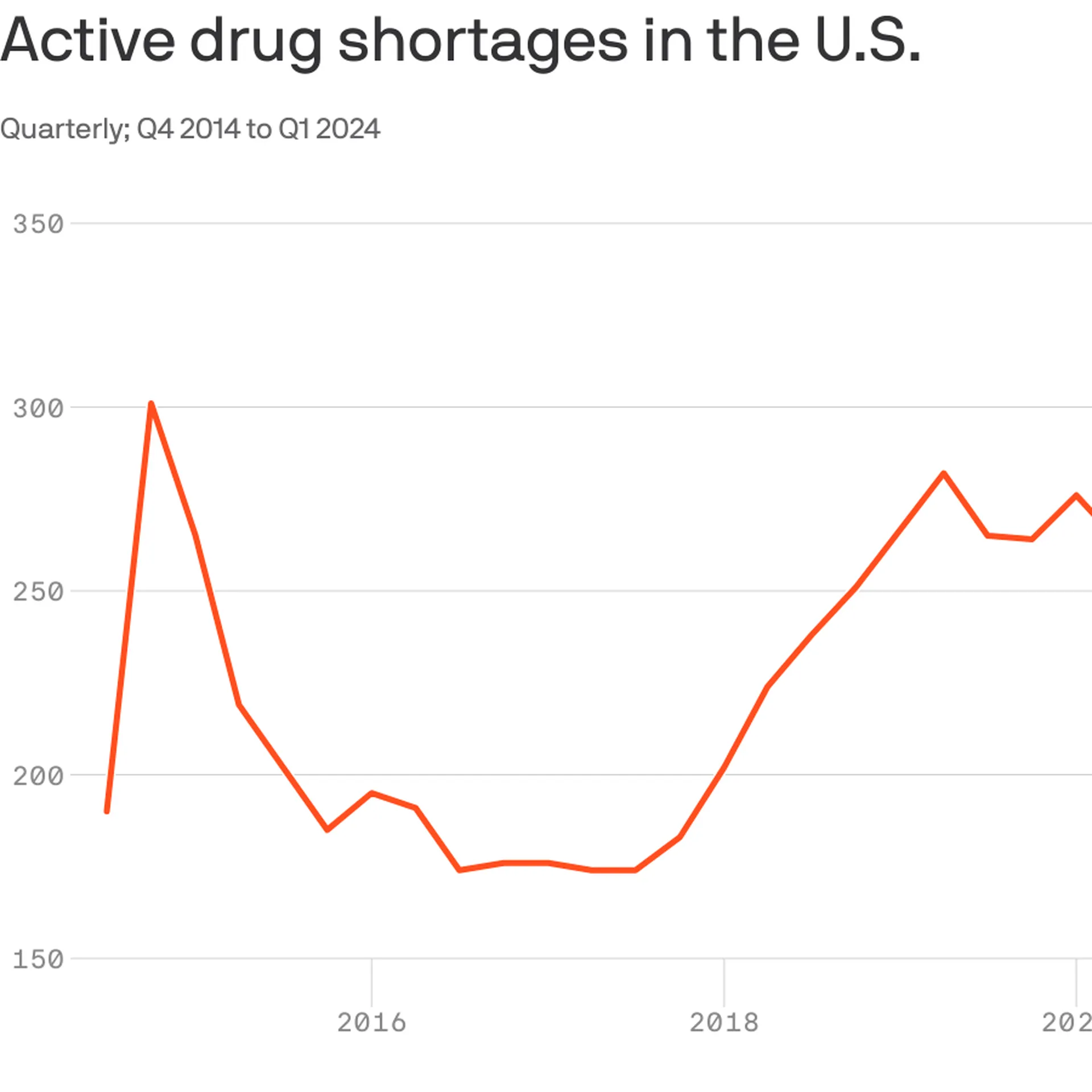

With 323 medicines in short supply, U.S. drug shortages have risen to their highest level since the American Society of Health-System Pharmacists began tracking in 2001.

Why it matters:

This high-water mark should energize efforts in Congress and federal agencies to address the broken market around what are often critical generic drugs, the organization says.

The Biden administration last week issued a drug-shortage plan that called on Congress to pass legislation that would reward hospitals for maintaining an adequate supply of key drugs, among other measures.

As a “first step,” Medicare yesterday proposed incentives for roughly 500 small hospitals to establish and maintain a six-month buffer stock of essential medicines.

The big picture:

Many of the issues behind shortages are tied to low prices for generics that leave manufacturers competing on price.

“It’s been a race to the bottom. We need more transparency around quality so that buyers have a reason to not chase the lowest price,” said Michael Ganio, senior director at the ASHP.

Drugmakers that can demonstrate safer, higher-quality manufacturing practices should earn a higher price, he said.

Manufacturing quality concerns in particular have fueled shortages of chemotherapy drugs and some antibiotics.

Between the lines: Other factors are also driving drug shortages.

Controlled substances, such as pain and sedation medications,account for12% of active shortages, which are tied to recent legal settlements and Drug Enforcement Administration changes to production limits, per ASHP.

Not surprisingly, the blockbuster category of anti-obesity drugs known as GLP-1s are in shortage largely because of outsized demand.

Mississippi, one of the country’s poorest and least healthy states, could soon become the next to expand Medicaid.

Why it matters:

It’s one of several GOP-dominated states that have seriously discussed Medicaid expansion this year, a sign that opposition to the Affordable Care Act coverage program may be softening among some holdouts 10 years after it became available.

A new House speaker who strongly backs expansion and growing fears that the state’s rural hospitals can’t survive without it have kept up momentum in Mississippi’s legislature this year.

As many as 200,000 low-income adults could gain coverage if lawmakers clinch a deal in the closing weeks of the Mississippi session.

State of play:

Mississippi’s House and Senate this week began hashing out differences between two very different plans passed by each chamber.

The House bill is the traditional ACA expansion, extending coverage to adults earning 138% of the federal poverty level, or about $21,000.

The Senate’s version, which leaders have dubbed “lite” expansion, covers people earning up to the poverty line and wouldn’t bring in the more generous federal support available for full expansion.

Both plans include a work requirement, but only the House version would still allow expansion to take effect without it. The Biden administration opposes work rules, but former President Trump could revive them in a second term.

Zoom out:

State lawmakers in Alabama and Georgia gave serious consideration to Medicaid expansion this year, though they ultimately dropped it. Kansas’ Gov. Laura Kelly, a Democrat, is trying again to expand Medicaid, but the GOP-run legislature remains opposed.

Shuttering rural hospitals and an acknowledgementthat the ACA is unlikely to be repealedhave made Republicans more willing to take a closer look at expansion, Politico reported earlier this year.

The fact that the extra federal funding from the ACA expansion could lift state budgets as pandemic aid dries up has also piqued states’ interest, said Joan Alker, executive director of the Georgetown University Center on Children and Families.

Zoom in:

Mississippi’s expansion effort has advanced further than other states this year largely becausenew House Speaker Jason White has made it a priority. Lt. Gov. Delbert Hosemann, who presides over the Senate, has also pushed the issue.

“We see an unhealthy population that’s uncovered. And we see this as the best way” to insure them, White told Mississippi Today this week.

“I just think it’s time for us to realize that there’s not something else coming down the pipe.”

The state’s crumbling health infrastructure has also made expansion more urgent, said Democratic state Sen. Rod Hickman. More than 40% of the state’s 74 rural hospitals are at risk of closing, a report last summer found.

“The dire need of our hospital systems and the state finally recognizing that Medicaid expansion could assist in those issues is what has kind of brought that to the forefront,” he told Axios.

Yes, but:

Republican Gov. Tate Reeves has reportedly pledged to oppose any Medicaid expansion deal that may emerge before the legislature adjourns in early May,so lawmakers would likely need a veto-proof majority to approve an expansion.

Austin Barbour, a Republican strategist who works in Mississippi politics, said he expects lawmakers will reach a deal.

But if they don’t, “I know this will be an issue that’ll pop right back up next session,” he said.

Health system operating margins improved in 2023 after a tumultuous 2022. Increased revenue from rebounding patient volumes helped offset the high costs of labor and supplies for many systems, but some continue to face challenges turning a financial corner.

In a Feb. 21 analysis, Kaufman Hall noted that too many hospitals are losing money but high-performing hospitals are faring far better, “effectively pulling away from the pack.”

Average operating margins have see-sawed over the last 12 months, from a -1.2% low in February 2023 to 5.5% highs in June and December. In February, average operating margins dropped to 3.96% before the Change Healthcare data breach, which has impacted claims processing.

Here are 42 health systems ranked by operating margins in their most recent financial results.

Editor’s note: The following financial results are for the 12 months ending Dec. 31, 2023, unless otherwise stated.

Revenue: $20.55 billion Expenses: $18.31 billion Operating income/loss: $2.5 billion (*Includes grant income and equity in earnings of unconsolidated affiliates) Operating margin: 12.2%

*Results for the first six months ending Dec. 31 Revenue: $2.1 billion Expenses: $2 billion Operating income/loss: $22.9 million Operating margin: 1.1%

On March 8, 2024, FDA approved Wegovy (semaglutide)opens in a new tab or window to treat cardiovascular disease risks — heart attack, stroke, and death — for obese or overweight adults with a history of cardiovascular disease, making it the first anti-obesity medication (AOM) to obtain such approval.Studies showopens in a new tab or window that semaglutide reduces heart disease risks when accompanied by blood pressure and cholesterol management and healthy lifestyle counseling. FDA noted that this approval is “a major advance in public health.”

Less than 2 weeks after FDA approved the new indication (semaglutide is also approved for chronic weight management and type 2 diabetes), CMS issued a memorandumopens in a new tab or window stating that Medicare Part D plans may cover AOMs if they are FDA approved for an additional medically accepted indication beyond only weight management. CMS’ guidance is prospective and is not limited to semaglutide. The guidance applies to all AOMs that may be approved in the future to treat other conditions. To ensure that AOMs are used for medically accepted indications, CMS clarified that Part D sponsors may employ common utilization management tools like step therapy and prior authorization.

Notably, FDA’s approval of semaglutide for cardiovascular disease is likely a harbinger of similar approvals in the near future — along with their coverage by Medicare. While the benefits are substantial, so too may be the costs as more and more drugs and patients receive coverage.

Analyses have foundopens in a new tab or window extraordinarily high prices for Wegovy , with a list price up to $1,349 and a net price (received by the manufacturer) of $701 for a 4-week supply. It is estimated that 6.6 million Americans opens in a new tab or window would benefit from medications like semaglutide for cardiovascular event reduction. Because AOMs are so costly, increasing their coverage and use could result in substantial Medicare spending, as well as higher premiums and cost-sharing for enrollees.

In 2022, Medicare gross total spending on semaglutide and tirzepatide for diabetes reached $5.7 billionopens in a new tab or window, up from $57 million in 2018. With FDA’s approval of these drugs as AOMs, Medicare spending for new indications can be expected to increase dramatically in the next few years.

In March 2024, the Congressional Budget Office (CBO) found that Medicare coverage of AOMs would result in considerable demand for and use of AOMsopens in a new tab or window by enrollees. CBO expects that generic competition, which could moderate prices and lead to higher rebates, would start in earnest only in the second decade of a policy allowing Medicare Part D to cover AOMs. However, even that assumption is not certain as pharmaceutical companies seek to “evergreen”opens in a new tab or window patent protection and market exclusives. CBO also acknowledges the possibility of new drugs that are more effective, have fewer side effects, or can be taken less often, which could translate to higher prices. Furthermore, if AOMs are stopped, weight then increases, meaning that these medications may have to be taken lifelong.

Arguably, reducing obesity rates could reduce the incidence of many chronic diseases such as diabetes and heart disease, potentially creating a net benefit in the long term. And even in the near-term, the Inflation Reduction Act (IRA) may help curb costs.

The IRA also has other mechanisms that may help address the high costs. The IRA’s rebate program, for example, ensures cost containment by requiring manufacturers of drugs that don’t have competitors to pay rebates to HHS if the prices of those drugs increase faster than the inflation rate. The IRA also caps out-of-pocket spending for prescription drugs at $2,000 starting in 2025opens in a new tab or window. (Although a $2,000 cap helps limit costs, spending that amount of money is still burdensome, especially for people of low socioeconomic status who are disproportionately impacted by obesity.)

In short, the IRA may alleviate, but not eliminate, Medicare spending concerns. The IRA’s ability to address the cost concerns of AOM coverage depends on various factors, and it is likely that those cost containment measures will take many years to materialize. As AOMs continue to be approved for new uses, the intense demand for these drugs coupled with their high costs are likely to place pressures on Medicare spending for years to come.

Takeaways

CMS has made clear that Medicare should cover semaglutide or other AOMs only when needed to avert cardiovascular or other serious diseases. This rule will have to be rigorously enforced and monitored.

Savvy Medicare enrollees could try to game the system, using medications primarily for weight loss purposes — which would be inconsistent with CMS’s approval. Some physicians might also engage in dishonest prescribing. Also, given the racial and ethnic disparities in access to obesity treatment, marginalized groups are unlikely to reap equal benefit from AOMs. For those reasons, robust and thoughtful strategies are needed to ensure that coverage for such drugs is not exploited. Without clear limits on the use of AOMs, Medicare could be overwhelmed with costs.

Beyond Medicare spending, there are wider equity concerns about access to drugs that treat medical conditions associated with obesity. Even if marginalized individuals can gain access to the medication, obtaining optimal health benefits of AOMs is likely to remain a challenge. FDA notes that semaglutide is most effective when it is taken together with other lifestyle or behavioral changesopens in a new tab or window, such as diet and exercise. Because healthy lifestyles and behaviors are mostly influenced by broader social and commercial determinants, the full health benefits of AOMs may elude those most at risk. To harness the public health benefits, AOMs must be seen as part of a broader approach to address health risks associated with obesity; they should not detract from the interventions targeted at socio-structural determinants of health that shape individual and population health outcomes.

To some, semaglutide and other AOMs are a miracle of modern science. Yet, we should entertain some skepticism about miracle solutions to deeply complex health threats. Medicare should extend coverage for AOMs under criteria that meaningfully considers the competing concerns and tradeoffs. Meanwhile, public health professionals and clinicians should continue to use all the tools at our disposal to reduce the burdens of disease caused by overweight and obesity, while also fighting against the stigma, shaming, and discrimination that are widely prevalent in our society.

If a picture is worth a thousand words, a video, if done well, can be worth thousands more.

Regular readers of HEALTH CARE un-covered know we have published lots of words about the barriers health insurance companies have erected that make it harder and harder for patients to get the care their doctors know they need.

It’s a perfect example of how something that was designed to protect patients from inappropriate and unnecessary care has been weaponized by health insurers to pad their bottom lines.

Prior authorization in today’s world all too often serves as a bureaucratic barrier, requiring patients and their doctors to obtain approval in advance from insurers before certain treatments, medications, or procedures will be covered.

While insurance companies argue that prior authorization helps control costs and ensure appropriate care, the reality is far grimmer.

Both patients and their health care providers suffer the consequences. Patients frequently face delays in receiving necessary treatments or medications, exacerbating their health conditions and causing unnecessary stress and anxiety. Many forgo needed care altogether due to the complexities and frustrations of navigating the prior authorization process. This practice not only undermines patients’ trust in their health care providers but also compromises their health, often leading to worsened conditions and, tragically, sometimes irreversible harm.

The burden of prior authorization falls heavily on clinicians and their office staff who must spend valuable time and resources navigating the bureaucratic red tape imposed by insurers. This administrative burden not only detracts from patient care but also contributes to physician burnout, dissatisfaction and moral crisis, according to many doctors.

Ultimately, the health insurance industry’s prioritization of profit over patient well-being is evident in its insistence on maintaining these barriers to care, perpetuating a system that defaults to financial gain at the expense of human lives.

The New York Times video cuts to the chase. Prior authorization, as practiced today by insurance companies, is “medical injustice disguised as paperwork.”

If Congress in the next year or two succeeds in transforming Medicare into something that looks like a run-of-the mill Medicare Advantage plan for everyone – not just for those who now have the plans – it will mark the culmination of a 30-year project funded by the Heritage Foundation.

A conservative think tank, the Heritage Foundation grew to prominence in the 1970s and ’80s with a well-funded mission to remake or eliminate progressive governmental programs Americans had come to rely on, like Medicare, Social Security and Workers’ Compensation.

Some 30 million people already have been lured into private Medicare Advantage plans, eager to grab such sales enticements as groceries, gym memberships and a sprinkling of dental coverage while apparently oblivious to the restrictions on care they may encounter when they get seriously ill and need expensive treatment. That’s the time when you really need good insurance to pay the bills.

Congress may soon pass legislation that authorizes a study commission pushed by Heritage and some Republican members aimed at placing recommendations on the legislative table that would end Medicare and Social Security, replacing those programs with new ones offering lesser benefits for fewer people.

In other words, they would no longer be available to everyone in a particular group. Instead they would morph into something like welfare, where only the neediest could receive benefits.

How did these popular programs, now affecting 67.4 million Americans on Social Security and nearly 67 million on Medicare, become imperiled?

As I wrote in my book, Slanting the Story: The Forces That Shape the News, Heritage had embarked on a campaign to turn Medicare into a totally privatized arrangement. It’s instructive to look at the 30-year campaign by right-wing think tanks, particularly the Heritage Foundation, to turn these programs into something more akin to health insurance sold by profit-making companies like Aetna and UnitedHealthcare than social insurance, where everyone who pays into the system is entitled to a benefit when they become eligible.

The proverbial handwriting was on the wall as early as 1997 when a group of American and Japanese health journalists gathered at an apartment in Manhattan to hear a program about services for the elderly. The featured speaker was Dr. Robyn Stone who had just left her position as assistant secretary for the Department of Health and Human Services in the Clinton administration.

Stone chastised the American reporters in the audience, telling them: “What is amazing to me is that you have not picked up on probably the most significant story in aging since the 1960s, and that is passage of the Balanced Budget Act of 1997, which creates Medicare Plus Choice” – a forerunner of today’s Advantage plans.

“This is the beginning of the end of entitlements for the Medicare program,” Stone said, explaining that the changes signaled a move toward a “defined contribution” program rather than a “defined benefit” plan with a predetermined set of benefits for everyone. “The legislation was so gently passed that nobody looked at the details.”

Robert Rosenblatt, who covered the aging beat for the Los Angeles Times, immediately challenged her. “It’s not the beginning of the end of Medicare as we know it,” he shot back. “It expands consumer choice.”

Consumer choice had become the watchword of the so-called “consumer movement,” ostensibly empowering shoppers – but without always identifying the conditions under which their choices must be made.

When consumers lured by TV pitchmen sign up for Medicare Advantage, how many of the sellers disclose that once those consumers leave traditional Medicare for an Advantage plan, they may be trapped. In most states, they will not be able to buy a Medicare supplement policy if they don’t like their new plan unless they are in super-good health.

In other words, most seniors are stuck. That can leave beneficiaries medically stranded when they have a serious, costly illness at a time in life when many are using up or have already exhausted their resources. I once asked a Medicare counselor what beneficiaries with little income would do if they became seriously ill and their Advantage plan refused to pay many of the bills, an increasingly common predicament. The cavalier answer I got was: “They could just go on Medicaid.”

The push to privatize Medicare began in February 1995 when Heritage issued a six-page committee brief titled “A Special Report to the House Ways and Means Committee”, which was sent to members of Congress, editorial writers, columnists, talk show hosts and other media. Heritage then spent months promoting its slant on the story. Along with other right-wing groups dedicated to transforming Medicare from social insurance to a private arrangement like car insurance, Heritage clobbered reporters who produced stories that didn’t fit the conservative narrative.

The right-wing Media Research Center singled out journalists who didn’t use the prescribed vocabulary to describe Heritage plans. Its newsletter criticized CBS reporter Linda Douglas when she reported that the senior citizens lobby had warned that the Republican budget would gut Medicare. The group reprimanded another CBS reporter, Connie Chung, for reporting that the House and Senate GOP plans “call for deep cuts in Medicare and other programs.” Haley Barbour, then Republican National Committee chairman, vowed to raise “unshirted hell” with the news media whenever they used the word “cut.” He wined and dined reporters, “educating” them on the “difference” between cuts and slowing Medicare’s growth. Former Republican U.S. Rep. John Kasich of Ohio, who chaired the House budget committee, called reporters warning them not to use the word “cut,” later admitting he “worked them over.”

As I wrote at the time, by fall of that year reporters had fallen in line. Douglas, who had been criticized all summer, got the words right and reported that the Republican bill contained a number of provisions “all adding up to a savings of $270 billion in the growth of Medicare spending.”

Fast forward to now. The Heritage Foundation’s Budget Blueprint for fiscal year 2023 offered ominous recommendations for Medicare, some of which might be enacted in a Republican administration. The think tank yet again called for a “premium support system” for Medicare, claiming that if its implementation was assumed in 2025, it “would reduce outlays by $1 trillion during the FY 2023-2032 period.” Heritage argues that the controversial approach would foster “intense competition among health plans and providers,” “expand beneficiaries’ choices,” “control costs,” “slow the growth of Medicare spending,” and “stimulate innovation.”

The potential beneficiaries would be given a sum of money, often called a premium support, to shop in the new marketplace, which could resemble today’s sales bazaar for Medicare Advantage plans, setting up the possibility for more hype and more sellers hoping to cash in on the revamped Medicare program. Many experts fear that such a program ultimately could destroy what is left of traditional Medicare, which about half of the Medicare population still prefers.

In other words, most seniors are stuck.

That can leave beneficiaries medically stranded when they have a serious, costly illness at a time in life when many are using up or have already exhausted their resources. I once asked a Medicare counselor what beneficiaries with little income would do if they became seriously ill and their Advantage plan refused to pay many of the bills, an increasingly common predicament. The cavalier answer I got was: “They could just go on Medicaid.”

The push to privatize Medicare began in February 1995 when Heritage issued a six-page committee brief titled “A Special Report to the House Ways and Means Committee”, which was sent to members of Congress, editorial writers, columnists, talk show hosts and other media. Heritage then spent months promoting its slant on the story. Along with other right-wing groups dedicated to transforming Medicare from social insurance to a private arrangement like car insurance, Heritage clobbered reporters who produced stories that didn’t fit the conservative narrative.

The right-wing Media Research Center singled out journalists who didn’t use the prescribed vocabulary to describe Heritage plans. Its newsletter criticized CBS reporter Linda Douglas when she reported that the senior citizens lobby had warned that the Republican budget would gut Medicare. The group reprimanded another CBS reporter, Connie Chung, for reporting that the House and Senate GOP plans “call for deep cuts in Medicare and other programs.” Haley Barbour, then Republican National Committee chairman, vowed to raise “unshirted hell” with the news media whenever they used the word “cut.” He wined and dined reporters, “educating” them on the “difference” between cuts and slowing Medicare’s growth. Former Republican U.S. Rep. John Kasich of Ohio, who chaired the House budget committee, called reporters warning them not to use the word “cut,” later admitting he “worked them over.”

As I wrote at the time, by fall of that year reporters had fallen in line. Douglas, who had been criticized all summer, got the words right and reported that the Republican bill contained a number of provisions “all adding up to a savings of $270 billion in the growth of Medicare spending.”

Fast forward to now. The Heritage Foundation’s Budget Blueprint for fiscal year 2023 offered ominous recommendations for Medicare, some of which might be enacted in a Republican administration. The think tank yet again called for a “premium support system” for Medicare, claiming that if its implementation was assumed in 2025, it “would reduce outlays by $1 trillion during the FY 2023-2032 period.” Heritage argues that the controversial approach would foster “intense competition among health plans and providers,” “expand beneficiaries’ choices,” “control costs,” “slow the growth of Medicare spending,” and “stimulate innovation.”

The potential beneficiaries would be given a sum of money, often called a premium support, to shop in the new marketplace, which could resemble today’s sales bazaar for Medicare Advantage plans, setting up the possibility for more hype and more sellers hoping to cash in on the revamped Medicare program. Many experts fear that such a program ultimately could destroy what is left of traditional Medicare, which about half of the Medicare population still prefers.

In a Republican administration with a GOP Congress, some of the recommendations, or parts of them, might well become law. The last 30 years have shown that the Heritage Foundation and other organizations driven by ideological or financial reasons want to transform Medicare, and they are committed for the long haul. They have the resources to promote their cause year after year, resulting in the continual erosion of traditional Medicare by Advantage Plans, many of which are of questionable value when serious illness strikes.

The seeds of Medicare’s destruction are in the air.

The program as it was set out in 1965 has kept millions of older Americans out of medical poverty for over 50 years, but it may well become something else – a privatized health care system for the oldest citizens whose medical care will depend on the profit goals of a handful of private insurers. It’s a future that STAT’s Bob Herman, whose reporting has explored the inevitable clash between health care and an insurer’s profit goals, has shown us.

In the long term, the gym memberships, the groceries, the bit of dental and vision care so alluring today may well disappear, and millions of seniors will be left once again to the vagaries of America’s private insurance marketplace.

Wall Street has fallen out of love with big insurers that depend heavily on the federal government’s overpayments to the private Medicare replacement plans they market, deceptively, under the name, “Medicare Advantage.”

I’ll explain below. But first, thank you if you reached out to your members of Congress and the Biden administration last week as I suggested to demand an end to the ongoing looting by those companies of the Medicare Trust Fund.

As I wrote on March 26, the Center for Medicare and Medicaid Services was scheduled to announce this week how much more taxpayer dollars it would send to Medicare Advantage companies next year. On January 31, CMS said it planned to increase the amount slightly to account for the increased cost of health care, based on how much more the government likely would spend to cover people enrolled in the traditional Medicare program. It uses traditional Medicare as a benchmark.

Big insurers like UnitedHealthcare, Humana and Aetna, owned by CVS, howled when CMS released its preliminary 2025 rate notice that day. They claimed they wouldn’t be getting enough of taxpayers’ dollars. So they launched a high-pressure campaign to get CMS to give them more money. They demanded extra billions because, they said, their Medicare Advantage enrollees had used more prescription drugs and went to the doctor more often in 2023 and January of this year than the companies had expected.

CMS announced after the market closed Monday that it was sticking to its plan to increase payments to Medicare Advantage plans by 3.7% – more than $16 billion –from 2024 to 2025. That would mean that it would pay companies that operate MA plans between $500 and $600 billion next year, considerably less than insurers wanted.

Shocked investors began running for the exits right away. When the New York Stock Exchange closed at 4 p.m. ET on Tuesday, more than 52 million shares of the companies’ stock had been traded–many millions more than average–driving the share prices of all of them way down. And the carnage has continued throughout this week.

By the end of trading yesterday, UnitedHealth, Humana and CVS/Aetna had lost nearly $95 billion in market capitalization. To put that in perspective, that’s more than the entire market cap of CVS, which fell to $93 billion yesterday.

All seven of the big for-profit companies with Medicare Advantage enrollment had a bad week, although Cigna, where I used to work and which announced recently it is getting out of the Medicare Advantage business next year, suffered the least. Its shares were down a little more than 1% as of yesterday afternoon.

Humana, the second largest MA company, which last year said it was getting out of the commercial insurance business to focus more fully on Medicare Advantage, by contrast, was the biggest loser of the bunch–and one of the biggest losers on the NYSE. Its shares fell more than 13% on Tuesday. As of yesterday, they were still down nearly 12%.

Noting that Humana’s stock has fallen 40% this year, he wrote:

Last fall, the insurer Humana was on top of the world. The stock was trading above $520 per share, as the company’s major bet on Medicare Advantage—the privately-run, publicly-funded insurance program for U.S. seniors—seemed to be paying off.

Long a darling of Wall Street’s analyst class, the stock had returned nearly 290% since the start of 2015, handily outperforming the S&P 500 over the same period.

Over the past five months, that position has crumbled. Humana shares were down to $308 Tuesday morning, as the outlook for Medicare Advantage and, by extension, for Humana’s business, has grown dimmer and dimmer.

Humana shares dived 12.3% early Tuesday, after the latest blow to the future prospects for the profitability of the Medicare Advantage business. Late Monday, the Centers for Medicare and Medicaid Services announced Medicare Advantage payment rates for 2025 that fell short of investor expectations.

The other companies also had a disastrous week. Shares of UnitedHealth, the biggest of the group in terms of Medicare Advantage enrollment (and overall revenues and profits), had fallen by 7% by the end of the day yesterday. CVS/Aetna’s shares were down 7.1%; Elevance’s were down 3.37%; Molina’s were down 7.15%; and Centene’s were down 7.33%.

When I was at Cigna, one of my responsibilities was to handle media questions when the company announced quarterly earnings, mergers and acquisitions, and whenever there was a major event like the CMS rate notice. The worst days of my 20-year career in the industry were when some kind of news triggered a stock selloff. I had to try to put the best spin possible on the situation. But my job was relatively easy compared to what the CEO, CFO and the company’s investor relations team had to do.

You can be certain they have been on the phone and in Zooms all week with Wall Street financial analysts, big institutional investors and even the company’s big employer customers in attempts to persuade them that the sky has not fallen.

You can also be certain that the companies will now shift their focus to the political arena. To keep this from happening again, they will begin pouring enormous sums of your premium dollars into campaigns to help elect industry-friendly candidates for Congress and the presidency this November. We provided a glimpse of where they’re already sending those donations in a story last November. We will continue to monitor this in the months ahead.

Last Monday, CMS announced the base payment rate it will pay Medicare Advantage plans in 2025: plans will see an average 3.7%, or $16 billion, increase in payments once risk scores are factored in but a cut to base payments of 0.16% since 2025 risk scores were expected to be 3.86%. That’s the math.

It came as a surprise to insurers and investors who had imagined CMS would modify its November proposed rule to increase payments as has been the precedent in prior years. Per Bloomberg:

Then on Wednesday, CMS released a 1327-page final rule with sweeping directives about how Medicare Advantage plans should operate starting next year:

“This final rule will revise the Medicare Advantage (Part C), Medicare Prescription Drug Benefit (Part D), Medicare cost plan, and Programs of All-Inclusive Care for the Elderly (PACE) regulations to implement changes related to Star Ratings, marketing and communications, agent/broker compensation, health equity, dual eligible special needs plans (D-SNPs), utilization management, network adequacy, and other programmatic areas. This final rule also codifies existing sub-regulatory guidance in the Part C and Part D programs.”

When first proposed in November, insurers pushed back. In response, most of the 3463 comment letters received by CMS said they needed more time to modify their plans. CMS replied: “We appreciate the commenter’s concern regarding the plans having enough time to understand the impact of finalized regulations. We will take their recommendation into consideration for future rulemaking.” P20). Accordingly, all MA plans must get approvals from CMS reflecting these changes on or before June 3, 2024.

Arguably, CMS took this hardline approach because bona fide studies by MedPAC, USC Shaeffer and others found widespread risk-score upcoding by Medicare Advantage plans that resulted in 6%-20% annual overpayments by Medicare.

Recent high-profile missteps by two of the biggest and most profitable MA players no doubt reinforced CMS’ get tougher posture: UnitedHealth Group’s Change Healthcare cybersecurity breech and Cigna’s $172 million Fraud and Abuse penalty for inflating its MA risk coding.

So, the transition from Medicare Advantage circa 2024 to Medicare Advantage 2025 will be its most significant since Medicare Choice was included in the Balanced Budget Act of 1997. In 2024, Medicare Advantage experienced enrollment growth and profitability to which its players were accustomed despite a late-year spike in utilization:

33.8 million Medicare enrollees (or 51% of total Medicare enrollment) get their coverage from Medicare Advantage plans—up 6.4% from 2023.

The average Medicare beneficiary has access to 43 Medicare Advantage plans in 2024, the same as in 2023, but more than double the number of plans offered in 2018. The majority of options do not require an extra payment above what Medicare pays private issuers on their behalf and the majority offer supplemental benefits including dental, eyecare, wellness et al.

And Medicare Advantage insurers entered the year on solid financial footing: the biggest issuers posted strong profits in 2023 i.e. UnitedHealth Group: $22.4 billion, CVS (Aetna) Health: $8.3 billion, Elevance Health: $6 billion, Cigna Group: $5.2 billion, Centene: $2.7 billion, Humana: $2.5 billion

In 4Q 2023, pent-up demand for services by Medicare Advantage enrollees pushed utilization of doctors, hospitals and other providers up 8.1% above prior year levels including 4Q 2023 increases for outpatient surgery 14.4%, outpatient visits excluding ER and surgery 8.7%, physician visits 6.0%, inpatient adult care 5.3%, Part B drugs 5% and ER visits 4%.

But 2025 will be different. The 4Q spike in utilization and impact of the new rules will have profound impact on Medicare Advantage: the biggest players like United and Humana will adapt and be OK, but others downstream will be disrupted or impaired:

Smaller MA plan sponsors and their lobbyists: AHIP, ACHP, BCBSA, Better Medicare Alliance and the army of lobbyists deployed to defeat these rules took a hit. Members pay dues for results. These rules were disappointing (though it could have been worse).

MA brokers, agents and marketing organizations: The limits on compensation, constraints on MA marketing tactics and enrollee protections around transparency may reduce revenues for many third-party marketing organizations that sell their services to the plans. A shakeout is likely.

Supplemental services providers: lower payments by CMS will force some to reduce/eliminate supplemental benefits that are valued less by enrollees. Dental and prescription drug benefits appear safe but others (i.e. fitness programs) might be cut by some.

Hospitals and physicians: Cuts by CMS to MA plans will trickle-down as reimbursement cuts to direct providers of care. Hardest hit will be smaller and rural providers in communities with large MA enrollment.

MA enrollees: Though the rule adds behavioral health benefits, data privacy protections and equity considerations in utilization management decisions by the plans, the likely impact of the rate cut is fewer plan options for enrollees and higher premiums. Margin compression for MA plans will hurt bigger plans who will adapt but incapacitate smaller plans unable to survive.

The Presidential campaigns: MA sponsors must submit their proposed 2025 plans to CMS on or before June 3, 2024—in the midst of Campaign 2024. And open enrollment will begin in October as MA plans launch marketing for their newly-revised offerings. No doubt, the Campaigns will opine to Medicare security in their closing rhetoric recognizing MA covers more than half its enrollees.

My take:

These rules are a big deal. CMS appears poised to challenge the industry’s formidable strengths and force changes.

Together, these rules will disrupt day to day operations in every MA plan, intensify friction with providers over network design, coverage and reimbursement negotiations and confuse enrollees who might have to pay more or change plans.

Medicare Advantage remains a work-in-process. Stay tuned.

Of late, private equity investors in healthcare services have faced intense criticism that their business practices have compromised patient safety and raised costs for consumers. March 5, the FTC, DOJ and HHS announced the launch of an investigation into the inner workings of PE in healthcare. It comes on the heels of U.S. Senate investigations in their Finance, HELP and Budget Committees to explore legislative levers they might pull to address their growing concerns about affordability, competition and accountability in the industry.

PE funds don’t welcome the spotlight.

Their business model lends to misinformation and disinformation: company takeovers by new owners are rarely treated as good news unless the circumstance under prior ownership was dire. Even then, attention shifts quickly to the fairness of the PE business model playbook: acquire the asset on favorable terms, replace management, reduce operating costs, grow and the sell in 5-7 years at a profit using debt to finance the deal along the way. In exchange, the PE fund’s General Partner gets an annual management fee of 2% plus 20% of the value they create when they sell the company or take it public, and favorable tax treatment (carried interest) on their gain.

Concern about PE in healthcare services comes at a particularly delicate time: hospitals. nursing homes, outpatient care, medical practices, clinics et al) are still feeling the after-effects of the pandemic, proposed reimbursement bumps by Medicare for hospitals and physicians do not offset medical inflation and the Change Healthcare cybersecurity breach February 21 has created cash flow issues for all.

Concern about PE ownership was high already.

Innovations funded through PE-backed organizations have been drowned out by the steady drip of peer reviewed and industry-sponsored studies a causal relationship between PE ownership decreased quality and patient safety and increased prices and worker discontent. Nonetheless, PE-owns 4% of hospitals (among 36% that are investor-owned, 13% of medical practices and 6% of nursing homes today and they’re increasing in all cohorts of health services.

Here are the facts:

Private equity enjoys significant influence in public policy including healthcare. Direct lobbying activity by PE funds in Congress and state legislatures is well-funded and effective, especially by the It is increasingly 20 global fund sponsors that control 46% of assets under management. Cash on hand and fund-raising by PE are strong and healthcare remains an important but non-exclusive target of PE investing.

2023 was a down year for PE, 2024 will be strong: the IPO market and sponsor- to sponsor transactions dipped, and deal values shrank. Even with interest rates remaining high, returns exceeded overall growth in the stock market for deals consummated. At the same time, PE raised $1.2 trillion last year and has $2.6 trillion of dry powder to invest. Healthcare services will be a target as PE deal activity increases in 2024.

In U.S. healthcare, PE investments are significant and increasing. Technology-enabled services that lower unit costs and AI-based solutions that enable standardization and workforce efficiency will garner higher valuations and greater PE interest than traditional services. Valuations will recover from record 2023 lows and dry powder will be deployed for roll-ups despite antitrust concerns and government investigations. Congress will investigate the impact on PE on patient safety, prices and competition and, in tandem with FTC and DOJ issue guidance: compliance will be mandated and financial penalties added. But displacement of PE in health services is unlikely.

Some notable data:

Private equity funds have $2.49 trillion of cash on hand to invest—up 7% from 2022. They raised $1.2 trillion globally in 2023. 26% of its global dry powder is more than 4 years old—undeployed.

Private equity groups globally are sitting on a record 28,000 unsold companies worth more than $3tn. 40% of the companies waiting to be sold are at least four years old. Last year, the combined value of companies that the industry sold privately or on public markets fell 44% and the value of companies sold to other buyout groups fell 47%.

Private equity investments in almost every sector in healthcare are significant, and until lately, increasing. Last year, deals were down 16.2% (from 940 to 788) cutting across every sector. In some sectors, like physician services, PE deals were tuck-in’s to their previous platform investments increasing from 75 deals in 2012 to 484 deals in 2021.

PE investments in US healthcare exceeded $1 trillion in the last 10 years. Investments in healthcare services i.e. acute, long-term, ambulatory and physician services– have been less profitable to investors than PE investments in technology, devices and therapeutics (based on the ratio of Enterprise Value to EBITDA) but exceed equity-market returns overall.

Peer reviewed studies have shown causal relationships between private equity ownership of hospitals, nursing homes and medical practices with lower operating costs, higher staff turnover, high prices and higher profits.

My take:

Like it or not, private equity investment in healthcare is here to stay. The likelihood of higher taxes paid by employers and individuals to fund the health system is nil. The majority (69%) of the public think it wasteful and inefficient (See Polling below). The majority believe it puts its profits above all else. The majority think it needs major change. That’s not new, but it’s felt more intensely and more widely than ever.

That means accommodation for private capital, including private equity, is not a major concern to voters: the prices they pay matters more than who owns the organization.

Tighter regulation of private equity, including more rights given to the Limited Partners who invest in the PE funds and limitations on public officials who become fund advisors, are likely. Bad actors will be vilified by regulators and elected officials. Media scrutiny of specific PE funds and their GPs will intensify as PE public reporting regulations commence. And investments made by not-for-profit multi-hospital systems and independent hospitals will be critical elements in upcoming Congressional and regulatory policy setting about their community benefit accountability and tax exemptions.

The public’s major concern about its healthcare industry is affordability. To the extent PE-backed solutions offer lower-cost, higher-value alternatives on a playing field that’s level with respect to equitable access and demand-management, they will be at the table.

To the extent PE-backed solutions cherry-pick the system’s low-hanging fruit at the expense of patient safety and affordability sans any regulatory restriction, they’ll breed public discontent from those they choose to ignore.

So, the reality is this: PE’s focus is generating profits for its GP and their LPs. Doing business in a socially responsible way is a fund’s prerogative. Some do it better than others.

PE is part of healthcare’s solution to its poorly structured, perpetually inadequate and mal-distributed funding. But creating a level playing field through meaningful regulatory reform is necessary first.

PS Among the stickier issues facing hospitals is site-neutral payments. Hospitals oppose the proposal reasoning the overhead structure for their outpatient services (HOPD) include indirect & direct costs for services provided those unable to pay i.e. emergency services. Proponents of the change argue that what’s done is the key, not where it’s done, and uniform pricing is common sense. Leavitt Partners has advanced a compromise: a Unified Ambulatory Payment System for HOPDs, ASCs and physician clinics that would be applied to 66 services starting