There are a lot of eye-popping statistics that capture the burden high health care costs put on so many Americans. Nearly three in 10 adults say they have problems paying medical bills. More than 40% say they skip medications because of the cost.

The stat that always stops me in my tracks is the fact that Americans have nearly $200 billion in unpaid medical bills in collections,according to one recent estimate. The average consumer facing collections in 2020 had more medical debt than all other sources of debt — credit cards, phone, utilities — combined.

“If a debt collector is calling you up or is knocking on your door, more than half of the time, it’s for medical debt,” said Neale Mahoney, a Stanford University economist and one of the nation’s leading scholars on medical debt.

Mahoney has spent two decades studying the scale of the country’s medical debt problem, as well as the effectiveness of policies intended to relieve people’s medical debt. From 2022-2023, he worked in the Biden administration on regulations to remove unpaid medical bills from people’s credit reports.

We talked with Mahoney about the fate of those regulations under the Trump administration, and what we’ve learned about the best way to protect people from getting medical debt in the first place.

Here are a few of the takeaways:

The Trump administration is rolling back Biden’s regulation of medical debt. Credit agencies sued to prevent the federal government from banning overdue medical bills from credit reports, and the White House declined to defend it. New guidance under Trump also challenged state protections for medical debt.

Nonprofits — and some local governments — have paid off medical debt for millions of Americans, in hopes of easing stress and improving people’s health. Mahoney’s research points to bigger improvements in health outcomes for patients who got debt relief sooner rather than later. One recent study showed patients who got their bills cleared within a few weeks of getting care were more likely to get diagnosed and treated for heart disease and diabetes than those who didn’t get help. However, an analysis of people who had their debts wiped after carrying them for years found no improvements to self-reported physical or mental health.

Mahoney believes helping patients avoid medical debt through health insurance or hospital financial assistance, which wipes out some or all of a patient’s bill, is the most effective approach. Many people, however, struggle to take advantage of either due to obstacles like restrictions from insurers and extensive applications to get help from hospitals. Patients caught up in what Mahoney has dubbed “the annoyance economy” often end up in money-losing fights. “For too many of us, navigating the U.S. health care system can feel like a second job,” Mahoney said, “at the precise moment when we don’t have the time and energy to take on a second job.”

One promising option to prevent people from falling into medical debt, Mahoney said, is for hospitals to auto-enroll eligible patients for financial assistance — a process known as “presumptive eligibility.” California, Illinois, Oregon and North Carolina have adopted auto-enrollment requirements for hospitals, and more states are considering it. “I would be eager to see hospitals working on this and sharing best practices,” Mahoney said, “so that we can provide relief to people who need it while still recovering payments from people who can afford it.”

One of those reasons is the growing number of states looking to require hospitals to auto-enroll patients in financial assistance programs. I’ve been reporting on this idea of presumptive eligibility for years, and for the last few months, I’ve been working on a special series diving deep into the pros and cons of forcing hospitals to provide more charity care. Those stories will drop this fall.

The Federal IDR Operations final rule introduces vital changes to fees, batching, and eligibility, but a lack of federal enforcement leaves providers battling payers for post-decision payments.

KEY TAKEAWAYS

The final rule slashes administrative fees and relaxes batching constraints to make pursuing lower-dollar claims much more financially viable for providers.

Payers must now provide essential claim details upfront to streamline eligibility determinations and reduce administrative friction.

Revenue cycle leaders should advocate for legislative action to hold payers accountable because the new rule lacks mechanisms to enforce post-decision payments.

While there is a significant administrative lift that comes with navigating the Federal Independent Dispute Resolution (IDR) process comes with a heavy administrative lift, the system has proven to be a significant driver of recovered revenue for providers.

To address operational friction for all parties, federal regulators have finalized the Federal IDR Operations rule. This update includes adjustments designed to standardize data, clarify timelines, and streamline the process.

For revenue cycle leaders, understanding these updates is essential to maintaining compliance and optimizing cash flow without adding unnecessary overhead.

Open Negotiation and Communication

The final rule mandates that all parties use the federal open negotiation portal to initiate the dispute process.

This requires providers to submit standardized data elements, creating a uniform communication channel. By centralizing the exchange, regulators aim to move away from the chaotic web of emails and spreadsheets that have often complicated early-stage resolutions.

Clarifying Eligibility

Determining IDR eligibility has been a time-consuming step for revenue cycle teams, but the final rule shifts more responsibility to payers.

Payers must now provide essential claim details at the time of the initial payment or denial. This includes the Qualifying Payment Amount (QPA) and specific remittance codes indicating whether a claim falls under state or federal jurisdiction. This upfront transparency allows providers to accurately assess eligibility before committing resources to a dispute.

Reducing IDR Fees

Perhaps most notably, the final rule reduces the non-refundable administrative fee to just $15 per party, per dispute. This represents an 85% drop from the previous $115 rate.

While the final rule establishes that these fees will now be collected earlier in the workflow to maintain system capacity, the lower financial barrier to entry makes it far more viable for providers to pursue arbitration for lower-dollar claims. Ultimately, this allows revenue cycle teams to seek out-of-network reimbursements without the fear that the administrative cost of the dispute will eclipse the potential recovery.

Revamped Batching Rules

New batching rules will help providers to more efficiently manage IDR costs and consolidate efforts by relaxing previous constraints and offering clearer guidelines for grouping claims.

Providers can now batch items and services billed under the same or similar service codes. To qualify, these claims must involve the same provider and the same payer, and they must have occurred within a specified 30-day window.

Enforcing the Cooling-Off Period

The NSA originally established a 90-day cooling-off period following a final determination to help manage dispute volumes.

The final rule explicitly clarifies how this timeline is triggered and applied. Providers cannot continuously submit the same disputed item or service code for the same payer once a determination is made. Revenue cycle teams will need to refine their internal tracking processes to ensure compliance with the cooling-off window and avoid administrative dismissals.

Will Payers Play Nice?

While the final rule clarifies details of the IDR process, it neglected to address comments from providers calling for an enforcement mechanism. Health systems are increasingly winning their IDR cases, only to find that payers are simply refusing to remit the owed amounts, according to Kathy Stull, manager of revenue cycle and analytics for HFMA.

“Instead of even getting the incorrect payment, they’re not going to pay anything,” Stull noted during the recent HFMA Region 1 Annual Conference.

If payers fail to make post-decision payments, revenue cycle leaders and health system government relations teams should advocate for H.R. 4710, a proposed bill that would impose civil monetary penalties on insurers for every instance they fail to pay following an IDR loss.

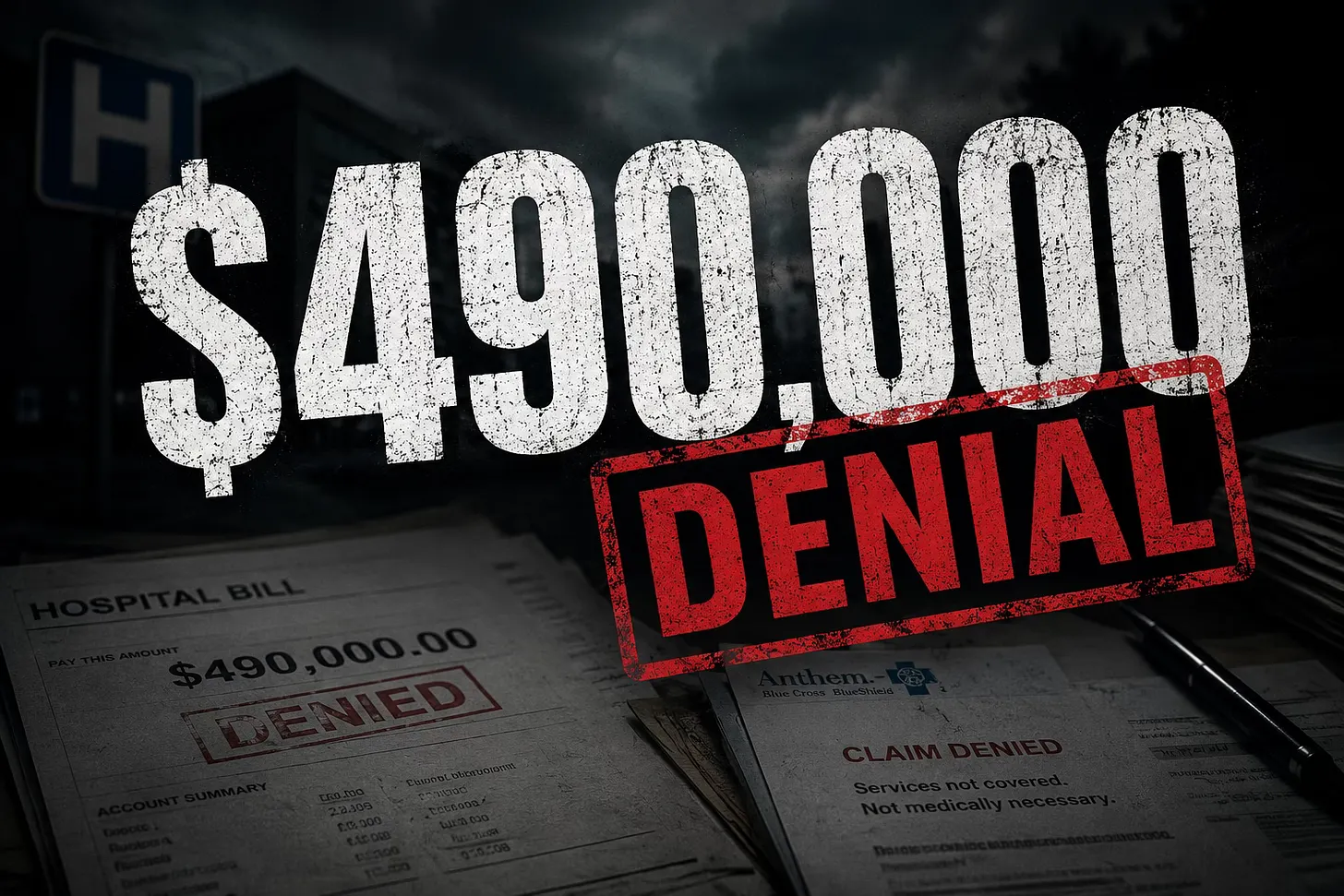

An emergency helicopter flight, life-saving surgeries and a health insurer that said it wasn’t medically necessary.

When Pamela Talley came home from an Arizona cycling vacation with a surgically repaired broken left wrist and elbow, she knew – as a retired family physician – that she’d be facing a tough recovery.

What the 62-year-old Colorado retiree wasn’t expecting was the letter she received not long after she got home last year from her health insurer, Anthem Blue Cross and Blue Shield. It informed Talley that her hospitalization in Tucson – where they’d helicoptered her after the nasty gravel spill which left part of her broken wrist protruding through her skin – was “medically unnecessary,” and the two emergency surgeries were not covered by her policy, either.

It said that she would be responsible for the medical costs that Anthem — which is part of the giant for-profit insurance conglomerate called Elevance Health — would not cover: $490,000.

“I’m still on narcotics,” Talley recalled of that moment. “I’m three days post-op. I’m in pain. I’m in a pretty vulnerable position. But my initial reaction – honestly, I think – as a physician was, ‘This is preposterous. I’m going to be able to resolve this with a telephone call.’”

Talley was not able to resolve this with a telephone call. Instead, the letter was just the beginning of an ordeal that lasted for 13 months and involved many two-hour phone calls, often waiting on hold, contradictory statements and explanations, and finally a plea for state regulators to help convince her insurer to pay.

The enormous dollar figure makes Talley’s battle somewhat unique, but receiving an insurance company denial letter is an experience that is painfully familiar to millions of Americans – and the problem is only getting worse. Exact numbers are hard to come by, but one 2023 study of patients covered in the Affordable Care Act (ACA) Marketplace found insurers initially denied 20% of claims.

Studies have also shown that it’s highly possible that patients who appeal these rejections can get them overturned, and yet very few – as few as 1%, it’s been reported – actually do fight back against rejections. Talley’s case arguably is a window into why, and why insurers count on this lack of appeals as they post record profits every year. Studies have shown that the cost of coverage denials falls hardest on lower-income Americans who lack the time and resources to fight back.

If a doctor like Talley with a lifetime of health care experience had to fight for more than a year for a fair resolution, what chance do the rest of us have?

Talley retired early from her second career in public health to move back to Colorado, where she had planted some roots and could better indulge her passion for the great outdoors. It was that hobby that took her with her two adult sons on the bicycle tour on scenic gravel trails in Arizona, near the border with Mexico.

On the second day of that excursion, Talley was moving quickly downhill on what the guides called a difficult “technical stretch,” and was clipped into her bicycle, when she fell – hard. As she lay on the gravel, she looked at her left arm, which she’d used to break the fall. Her wrist was clearly broken – a part of the bone was protruding through the skin – and it appeared her elbow was broken as well.

Between the pain and the remote site of the accident, Talley’s insurance coverage wasn’t on the top of her mind as the tour van trailing the cyclers picked her up and began the arduous task of getting her the urgent medical care she needed. It took two hours just to get to an emergency clinic near the border, where she was sedated, X-rayed, had the wrist placed in a splint – and where it was decided she’d need to get to a Level 1 trauma center. The nearest one was in Tucson, which was five hours away by car or 45 minutes by medical helicopter.

Knowing the risks of delaying an operation, she chose the helicopter.

“It was clear I needed surgery,” she recalled. But getting to Tucson was only the first step. “They see me, then I sit on a gurney in the hall in the emergency department for about eight hours,” she recalled. And then, because they had no beds upstairs, I was ultimately put into the labor and delivery ward overnight because that’s where they had a bed.”

Finally, she underwent two separate surgeries with hand and elbow specialists over a period that lasted nearly a day, as well as a procedure to alleviate nerve pressure. Talley would spend a couple nights in the hospital, first to get intravenous antibiotics and for observation, and also until she could arrange a flight back to Denver.

“So the day after I got back to Denver, I got a notice from Anthem that my $490,000 hospitalization bill was denied as medically unnecessary,” Talley said.

Too young for Medicare when she retired, Talley had signed up for Anthem’s high-deductible health insurance plan in the Affordable Care Act Marketplace. She said she knew she’d be liable for the first $10,000 or so in annual medical expenses, and she was OK with that. But she said she never expected that the giant insurer would find a plethora of grounds for not covering her emergency – that out-of-state care wasn’t eligible, or that her surgeons were out-of-network, or that some of her treatment was excessive.

Talley waited a couple days until she felt better to call Anthem, and then waited two hours to speak with someone who contradicted himself on the call, first stating that the denied care wasn’t medically necessary and then saying that actually the issue was that it occurred in Arizona and not in Colorado.

“Preposterous,” she said. “Come on, this was an emergency. It’s not like I went to get a hip replacement at the Mayo Clinic, which is what my plan is trying to prevent.” The Anthem representative promised her case would be reviewed, but nothing happened for a couple of months.

As bills for Talley’s complicated care trickled in, she was befuddled to see which services were covered and which were not. For example, Anthem was paying the anesthesiologist for her operation, but not the surgeons.

By now, Talley was calling Anthem about every three weeks, typically spending a couple of hours on hold each time. “I would get to a person, this conversation would start and they would hang up on me. And it got to the point where I felt like, oh, there’s a pop-up that says, ‘Hang up on this person. She’s persistent.’”

Talley filed a formal appeal within the six-month time period, and – again, with significant delay – finally received the guidelines for this policy upon which she argued that all of her care should have been covered. When Anthem denied her appeals, she looked into hiring a lawyer when she learned from a family member that the Colorado Department of Insurance had helped resolve a disputed claim for a much smaller amount. Talley convinced the state agency to help intervene in her matter.

Her last-gasp plea for government intervention worked, as regulators reminded Anthem of relevant state and federal statutes – such as the 2022 No Surprises Bill – intended to ensure claims such as Talley’s are covered. Still, the bills were resolved in pieces, not one fell swoop. By this spring, Talley was down from the initial $490,000 to one final $135 radiology bill, yet she continued to contest it.

“I’m stubborn,” she said with a laugh, and ultimately Anthem paid that bill as well. It took 13 months, but Talley ultimately only paid the $10,000 under her deductible.

But the big picture, unfortunately, is that there are too many other cases like Talley’s out there, and the number is likely to rise. For one thing, artificial intelligence, or AI, is increasingly used by Big Insurance to review claims, and often deny them, in the most coldly calculating fashion.

But also, the refusal late last year by the Republican-led Congress to extend subsidies that allowed millions of Americans to afford their monthly ACA premiums has forced many families to seek inferior alternatives – including high-deductible plans such as Talley’s. These policies typically have more loopholes that insurers can invoke to deny claims – exactly what happened to Talley.

However, as Talley herself pointed out, the tiny minority of patients who appeal these denials are often successful, especially when they are persistent, or make use of every available resource. For example, one KFF survey of 2022 data found that appeals of insurance companies’ prior authorization rejections successfully overturned them more than 82% of the time.

She also advised patients to study their insurers’ guidelines ahead of time. “I had never read my contract in detail,” Talley said. “What’s covered, what’s not covered. I’d never had the reason to do that, but now I know.”

Today, recovered from her Arizona accident, Talley is looking forward to her next outdoorsy travel adventure, in Europe. This time, she said she won’t clip into her bicycle – and she’s also getting trip insurance. She said: “I don’t want to not do things that have some risk, you know?”

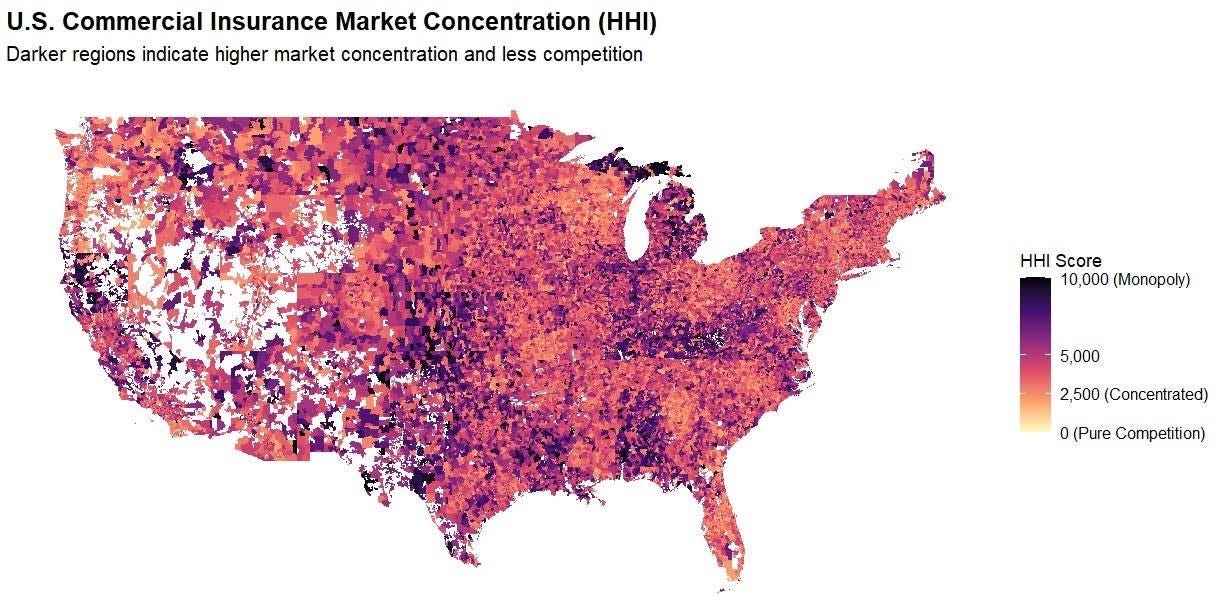

Hospital monopolies get the headlines – but new research shows health insurance markets are highly concentrated in every state, giving insurers more pricing power than most policymakers realize.

Hospital consolidation dominates the discussion on health care costs – with good reason. There is overwhelming evidence that it raises prices. But every hospital must ultimately negotiate rates with insurers, yet the consolidation story in the health insurer market has only gotten a tiny fraction of the attention. This is a mistake. While the insurer market is not as highly consolidated as the hospital market, it is still highly concentrated by any reasonable antitrust standard, and a major (and under-estimated) driver of cost growth.

The Department of Justice (DOJ) and Federal Trade Commission (FTC) use the Herfindahl Hirschman Index (HHI) to measure market concentration, where >1,800 is highly concentrated, 5,000-7,500 is where a few firms hold substantial market power, and >7,500 is a near monopoly, where a single firm holds absolute (or near absolute) price-setting autonomy. The hospital market is heavily concentrated and has an average HHI score of 5,273, with 97% of markets being at least heavily concentrated and 64% being near or complete monopolies.

By comparison, our recent work similarly shows a high degree of consolidation among insurers. (Figure 1) We found that the state-level average HHI score in the commercial insurance market was 4,458, with 50 of 50 states (100%) at least heavily concentrated, comparable to hospital markets. This means that in almost every state, health insurers hold pronounced power in price-setting, a key component of the health care cost crisis roiling the country. The most competitive states (although still very highly concentrated) were Oregon (2,870), New York (3,203), and Georgia (3,222), whereas Kentucky (6,752) and Alabama (6,988) are near monopolies.

We find that insurers are even more consolidated than previously reported by the American Medical Association (AMA). Yet the market power of insurers, in combination with hospitals, is a vastly under-appreciated and under-studied driver of costs.

There are several reasons why it is important.

1. Vertical integration

Vertical integration is rapidly accelerating the ability of insurers to consolidate power and redefining what an insurer even is (UnitedHealth/Optum, CVS/Aetna, Cigna/Express Scripts, Elevance/Carelon, BCBSA/Ascendiun). This means that traditional plan-level data (such as that used by researchers and the DOJ/FTC) underestimates the true market power of insurers, and the shadowy network of MSOs, banks, and vendors makes it very difficult to quantify, absent new reporting or regulatory requirements

2. Geography

Where you live is important since it determines where you receive care and buy insurance. In some states, the average competition tells the story, e.g. Louisiana, Kentucky, Alabama, since certain insurers dominate the metro areas and everything in between. In others, the reassuring state averages (CA, NY) mask the variance, and hide the pockets of very uncompetitive markets, particularly in rural areas. Understanding this issue at a market level is important for creating transparency and accountability, to ensure that everyone has options and access to affordable health insurance.

3. Competition

Competition among insurers and hospitals matters, as power asymmetry and/or collusion create dysfunctional markets where costs are “optimized” for the purposes of power and profits, not to make health care more affordable for consumers. It is also important to look at competition among insurers. Market dominance confers advantages that have little to do with delivering better care, such as leverage over providers, captive employer relationships, and pricing power insulated from competition.

While insurer markets aren’t as concentrated as hospital markets, they’re concentrated enough to matter, and the structure of that concentration makes it a distinct and important part of the cost problem. In our next piece, we will show which carriers hold dominant positions and where, and why the answer surprised us.

This research was made possible by the support of Arnold Ventures.

Data from Clarivate Managed Market Surveyor dataset. Includes FI/SI/HMO/PPO/POS/ACA plans.

HHI scores weighted according to zip-level and policy volume. Concentration levels: Red – Extreme; Orange – Severe; and Yellow – Very High.

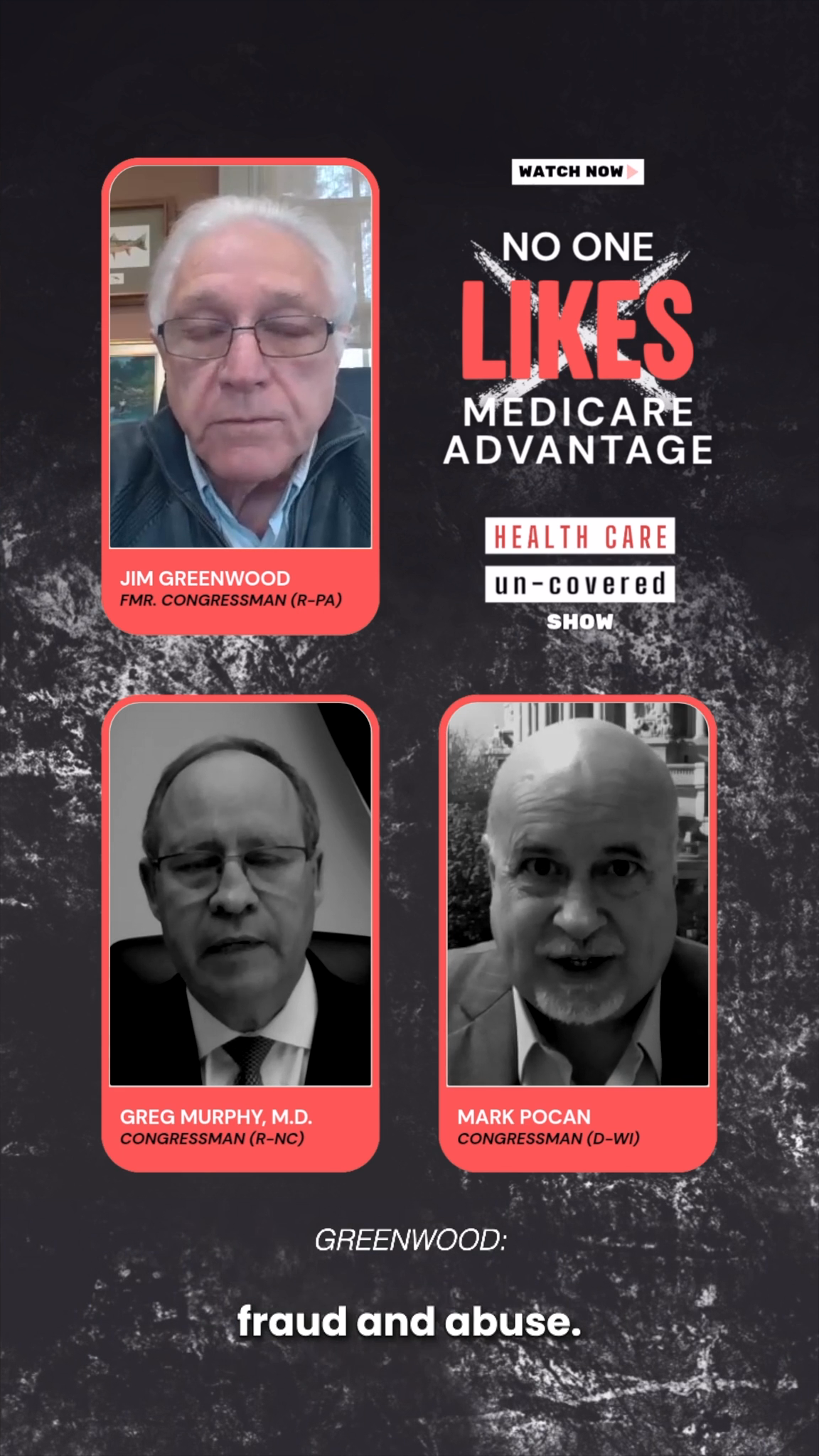

We’re joined by former Republican Congressman Jim Greenwood (R-PA) and Reps. Greg Murphy (R-NC) and Mark Pocan (D-WI) to discuss the costly and flawed Medicare Advantage program.

Concern about Medicare Advantage is no longer limited to patient advocates and health care reformers. Increasingly, lawmakers from across the political spectrum are questioning whether the program is serving seniors and taxpayers as intended.

Below are three clips from our latest episode of the HEALTH CARE un-covered Show featuring former Congressman Jim Greenwood (R-PA), Rep. Greg Murphy (R-NC) and Rep. Mark Pocan (D-WI).

Former Congressman Jim Greenwood (R-PA) helped author the Medicare Modernization Act of 2003, which created Medicare Advantage’s modern framework. More than two decades later, he argues the program has drifted far from what lawmakers originally envisioned.

Rep. Greg Murphy, MD (R-NC), a practicing physician and co-chair of the GOP Doctors Caucus, discusses Medicare Advantage’s high costs and upcoding schemes — and why he believes reforms are needed.

Rep. Mark Pocan (D-WI) has been one of Medicare Advantage’s most persistent critics in Congress. In this clip, he explains why he believes lawmakers must do more to curb insurer abuses and strengthen Traditional Medicare.

These clips offer just a glimpse of a much broader conversation about prior authorization, denied care, narrow provider networks, insurer overpayments and what Washington is doing about Medicare Advantage.

You can watch the full episode of the HEALTH CARE un-covered Show here:

A Trump administration plan to overhaul wage levels for visa holders is jolting hospitals and long-term care facilities that are heavily reliant on foreign-born workers.

Why it matters:

It’s the latest immigration-related policy change to loom over the health care workforce, coming after President Trump’s $100,000 H-1B visa fee and the suspension of certain immigrants’ work authorization renewals.

The latest move could further drive up costs for providers already struggling with staffing shortages, thin margins and growing patient demand, because many health jobs can’t be outsourced or automated.

Driving the news:

The Department of Labor wants to change the formula for calculating what it considers “fair minimum pay” for workers on certain visas, like H-1Bs, and green card sponsorship jobs.

The administration says the change would make it harder for companies to use visa programs to obtain cheaper labor and undercut American workers.

But the rule could have an outsized effect on health systems, testing labs, nursing homes and research institutions that sponsor foreign-trained workers.

There’s special concern about rural health providers that rely heavily on foreign-born clinicians to fill gaps in care in underserved areas.

Critics say the changewon’t adequately account for regional wage differences or experience levels.

They also warn a higher wage requirement will force employers to raise pay for U.S. workers to comply with labor laws — and make it unsustainable to hire foreign-born talent.

The big picture:

The U.S. health care system is heavily dependent on a foreign-born workforce. Immigrants make up about 16% of registered nurses nationwide, per a KFF analysis.

They make up 28% of the U.S. long-term care workforce, KFF found.

“This has the potential to significantly limit the sector’s ability to provide timely and quality health care services to those in need, both now and in the future,” Dana Ritchie, associate vice president of the American Health Care Association and National Center for Assisted Living, wrote in public comments on the proposal.

Zoom in:

Lynn Bruder, the CEO of staffing firm Nucleus Healthcare, said wage rates for visa-holding nurses on the lower end of the pay scale could jump 25% to 35% in certain markets, or from about $40 an hour to more than $50 an hour.

“The likely outcome is continued reliance on significantly more expensive agency staffing solutions and reduced ability for hospitals to build stable, long term workforce pipelines,” Bruder wrote in comments about the rule.

The other side:

The Department of Labor declined to comment. But visa programs have long been criticized for suppressing wages across many industries.

The changes would force employers to pay an estimated $6.5 billion in additional wages and increase the average certified wage by approximately $14,000 per year, according to the proposed rule.

“These proposed revisions aim to better align prevailing wage levels with the wages paid to U.S. workers,” the Labor Department wrote.

The window for public comments on the proposal closed this week.

The bottom line:

Health care providers say the administration is treating hospitals and nursing homes like any other employer, even though the workforce is being squeezed by an aging population and rising demand for care.

“Larger hospital systems may be able to absorb this increase, but you’ll see employers who are much smaller or mid-sized won’t,” Ann-Rose Johnson-Lewis, director of legal services at WorldWide HealthStaff Solutions, told Axios.

“You’ll see rural heath care systems not be able to absorb that. We’ll see a reduction in the workforce, fewer new hires and, ultimately, the broader economy will see the consequence of that.”