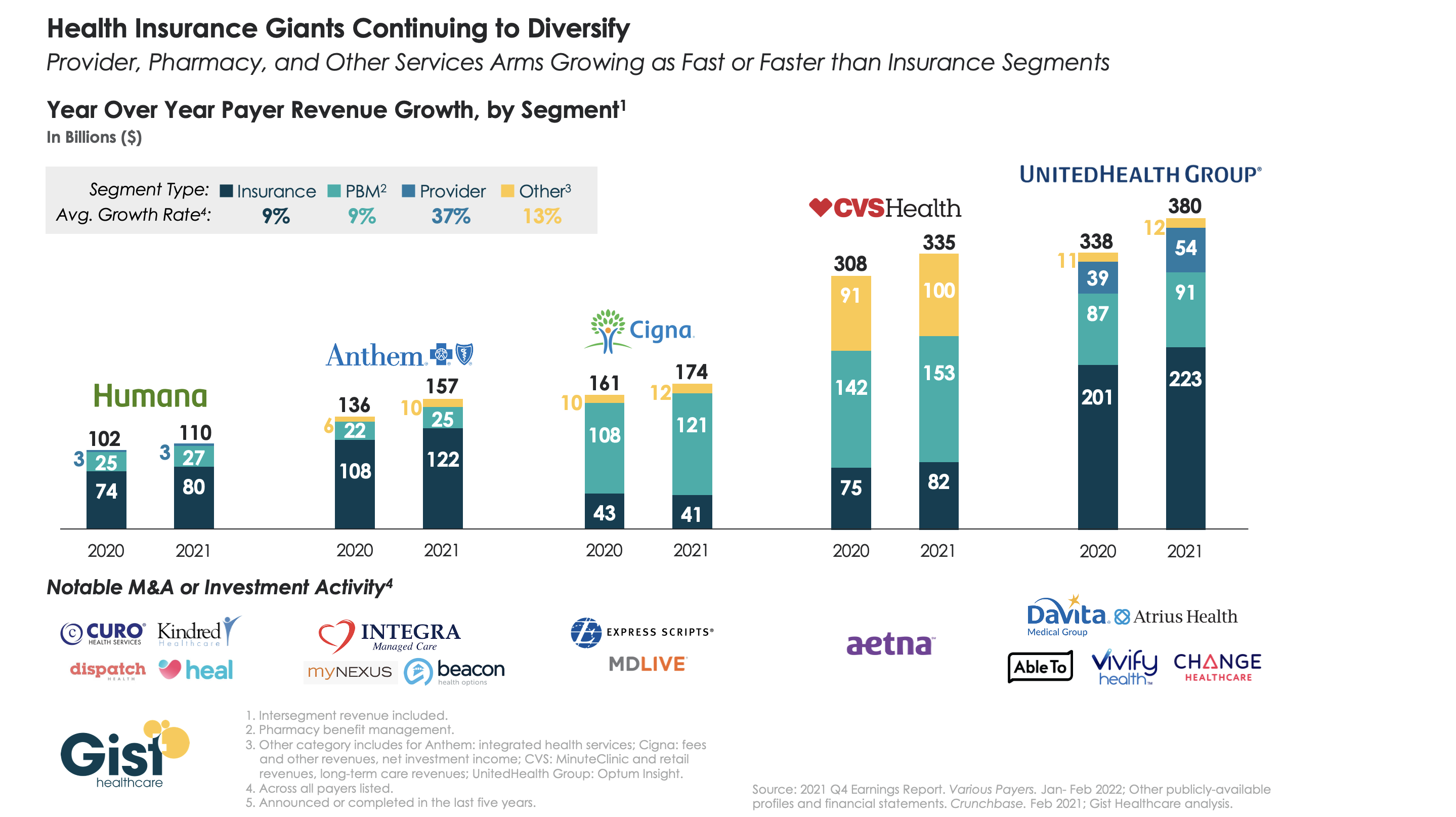

https://mailchi.mp/tradeoffs/research-corner-5222129?e=ad91541e82

High health care prices in the U.S. make it hard for people to access care, difficult for employers to provide insurance, and challenging for policymakers to balance health care spending with other budgetary priorities. That’s why it’s important to understand what drives prices higher and identify policies to keep prices from getting so high.

In a new paper in Health Affairs, Vilsa Curto, Anna Sinaiko and Meredith Rosenthal examined whether hospital and health systems’ acquisition of and contracting with physician practices – two forms of what is often called vertical integration – has led to higher prices for physician services. The researchers combined four sets of data from Massachusetts from 2013-2017 for their analysis.

They found that:

- The percent of physicians who joined health systems grew meaningfully: The percent of primary care physicians who remained independent dropped from 42% in 2013 to 31.5% in 2017, and the percent of independent specialists fell from 26% to 17%.

- Over this same period, prices for physician services rose. Price increases were especially large – 12% for primary care physicians and 6% for specialists – when physicians joined health systems that had a high share of admissions in their area.

This study stands out for several reasons. First, it shows vertical integration drives up health care prices. Second, the authors highlight actions states can and are considering taking to monitor and curb vertical integration, including antitrust enforcement and enacting laws to promote competition.

Finally, the Massachusetts data allow the public to better appreciate what’s happening across the state. Many earlier studies on health care consolidation have been limited to a subset of insurers, physicians or patients. Massachusetts is a leader when it comes to creating and sharing its data thanks to its all-payer claims database, which pulls together all the health care bills from private insurers and public programs like Medicare and Medicaid in the state. This critical information helps to illuminate patterns of care and prices and connect them to issues like consolidation and competition. Neither the federal government nor most states track how vertical integration mergers influence health care prices.

As these findings demonstrate, acquisitions and other forms of vertical integration impact what people pay for health care services. Given that prices in this sector continue to climb, this paper underscores the need for more state and national data to understand the downstream effects on all of us who use and participate in the U.S. health care system.