On Tuesday, CMS announced the States Advancing All-Payer Health Equity Approaches and Development (AHEAD) Model, a new payment model that will give up to eight states or sub-state regions the ability to test global hospital budgets across an 11-year period.

Participating states will assume responsibility for managing healthcare costs for traditional Medicare and Medicaid populations, while encouraging private payers to pay hospitals under a similar relationship.

Primary care practices will have the option to participate in a primary care component of the model, called Primary Care AHEAD, in which they will receive a Medicare care management fee and be required to engage in state-led Medicaid transformation initiatives.

CMS is hoping that the AHEAD model will reduce healthcare cost growth, improve population health, and reduce health outcome disparities. It builds upon existing Innovation Center state-based models, including the Maryland Total Cost of Care Model, the Vermont All-Payer Accountable Care Organization Model, and the Pennsylvania Rural Health Model, which have all shown promise in lowering Medicare spending while improving patient outcomes.

Program applications will open late this year, and the first states selected would begin a pre-implementation period in summer 2024.

The Gist:

Shifting to a total-cost-of-care model will be a difficult undertaking for even the most motivated states.

Though a stable annual budget may be a welcome prospect to struggling hospitals, large regional systems may balk at the idea, especially as the Maryland Hospital Association has claimed that their state’s regulated rates have lagged hospital cost inflation by 1.3 percent per year.

With the Medicare Shared Savings Program (MSSP)saving only one quarter of one percent of Medicare’s total spending in 2022, CMS has good reason to explore other ways to reduce Medicare cost growth

—but these Innovation Center models will only achieve their goals if they can first induce sufficient participation.

Last week, the Centers for Medicare and Medicaid Services (CMS) released the list of the first round of prescription drugs chosen for Medicare Part D price negotiations. The 2022 Inflation Reduction Act (IRA) granted CMS the authority to negotiate directly with pharmaceutical manufacturers, establishing a process that will ramp up to include 20 drugs per year and cover Part B medicines by 2029.

The majority of the initial 10 medications, including Eliquis, Jardiance, and Xarelto, are highly utilized across Medicare beneficiaries, treating mainly diabetes and cardiovascular disease. But three of the drugs (Enbrel, Imbruvica, and Stelara) are very high-cost drugs used by fewer than 50k beneficiaries to treat some cancers and autoimmune diseases.

Together the 10 drugs cost Medicare about $50B annually, comprising 20 percent of Part D spending. Drug manufacturers must now engage with CMS in a complex negotiation process, with negotiated prices scheduled to go into effect in 2026.

The Gist:

Most of the drugs on this list are not a surprise, with the Biden administration prioritizing more common chronic disease medications, with large total spend for the program, over the most expensive drugs, many of which are exempted by the IRA’s minimum seven-year grace period for new pharmaceuticals.

However, pharmaceutical companies are threatening to derail the process before it even begins. Several companies with drugs on the list have already filed lawsuits against the government on the grounds that the entire negotiation program is unconstitutional.

While President Biden is already touting lowering drug prices as a key plank of his reelection pitch, it will take years before these negotiations translate into lower costs for beneficiaries and reduced government spending. There also may be adverse unintended consequences, as drug companies may raise prices for commercial payers while increasing rebates to stabilize net prices, leading to higher costs for some consumers.

Still, it’s a step in the right direction for the US, given that we pay 2.4 times more than peer countries for prescription medications.

Last Tuesday, the Center for Medicare and Medicaid Services (CMS) announced the first 10 medicines that will be subject to price negotiations with Medicare starting in 2026 per authorization in the Inflation Reduction Act (2022). It’s a big deal but far from a done deal.

Here are the 10:

Eliquis, for preventing strokes and blood clots, from Bristol Myers Squibb and Pfizer

Jardiance, for Type 2 diabetes and heart failure, from Boehringer Ingelheim and Eli Lilly

Xarelto, for preventing strokes and blood clots, from Johnson & Johnson

Januvia, for Type 2 diabetes, from Merck

Farxiga, for chronic kidney disease, from AstraZeneca

Entresto, for heart failure, from Novartis

Enbrel, for arthritis and other autoimmune conditions, from Amgen

Imbruvica, for blood cancers, from AbbVie and Johnson & Johnson

Stelara, for Crohn’s disease, from Johnson & Johnson

Fiasp and NovoLog insulin products, for diabetes, from Novo Nordisk

Notably, they include products from 10 of the biggest drug manufacturers that operate in the U.S. including 4 headquartered here (Johnson and Johnson, Merck, Lilly, Amgen) and the list covers a wide range of medical conditions that benefit from daily medications.

But only one cancer medicine was included (Johnson & Johnson and AbbVie’s Imbruvica for lymphoma) leaving cancer drugs alongside therapeutics for weight loss, Crohn’s and others to prepare for listing in 2027 or later.

And CMS included long-acting insulins in the inaugural list naming six products manufactured by the Danish pharmaceutical giant Novo Nordisk while leaving the competing products made by J&J and others off. So, there were surprises.

To date, 8 lawsuits have been filed against the U.S. Department of Health and Human Services by drug manufacturers and the likelihood litigation will end up in the Supreme Court is high.

These cases are being brought because drug manufacturers believe government-imposed price controls are illegal. The arguments will be closely watched because they hit at a more fundamental question:

what’s the role of the federal government in making healthcare in the U.S. more affordable to more people?

Every major sector in healthcare– hospitals, health insurers, medical device manufacturers, physician organizations, information technology companies, consultancies, advisors et al may be impacted as the $4.6 trillion industry is scrutinized more closely . All depend on its regulatory complexity to keep prices high, outsiders out and growth predictable. The pharmaceutical industry just happens to be its most visible.

The Pharmaceutical Industry

The facts are these:

66% of American’s take one or more prescriptions: There were 4.73 billion prescriptions dispensed in the U.S. in 2022

Americans spent $633.5 billion on their medicines in 2022 and will spend $605-$635 billion in 2025.

This year (2023), the U.S. pharmaceutical market will account for 43.7% of the global pharmaceutical market and more than 70% of the industry’s profits.

41% of Americans say they have a fair amount or a great deal of trust in pharmaceutical companies to look out for their best interests and 83% favor allowing Medicare to negotiate pricing directly with drug manufacturers (the same as Veteran’s Health does).

There were 1,106 COVID-19 vaccines and drugs in development as of March 18, 2023.

The U.S. industry employs 811,000 directly and 3.2 million indirectly including the 325,000 pharmacists who earn an average of $129,000/year and 447,000 pharm techs who earn $38,000.

And, in the U.S., drug companies spent $100 billion last year for R&D.

It’s a big, high-profile industry that claims 7 of the Top 10 highest paid CEOs in healthcare in its ranks, a persistent presence in social media and paid advertising for its brands and inexplicably strong influence in politics and physician treatment decisions.

The industry is not well liked by consumers, regulators and trading partners but uses every legal lever including patents, couponing, PBM distortion, pay-to-delay tactics, biosimilar roadblocks et al to protect its shareholders’ interests. And it has been effective for its members and advisors.

My take:

It’s easy to pile-on to criticism of the industry’s opaque pricing, lack of operational transparency, inadequate capture of drug efficacy and effectiveness data and impotent punishment against its bad actors and their enablers.

It’s clear U.S. pharma consumers fund the majority of the global industry’s profits while the rest of the world benefits.

And it’s obvious U.S. consumers think it appropriate for the federal government to step in. The tricky part is not just government-imposed price controls for a handful of drugs; it’s how far the federal government should play in other sectors prone to neglect of affordability and equitable access.

There will be lessons learned as this Inflation Reduction Act program is enacted alongside others in the bill– insulin price caps at $35/month per covered prescription, access to adult vaccines without cost-sharing, a yearly cap ($2,000 in 2025) on out-of-pocket prescription drug costs in Medicare and expansion of the low-income subsidy program under Medicare Part D to 150% of the federal poverty level starting in 2024. And since implementation of these price caps isn’t until 2026, plenty of time for all parties to negotiate, spin and adapt.

But the bigger impact of this program will be in other sectors where pricing is opaque, the public’s suspicious and valid and reliable data is readily available to challenge widely-accepted but flawed assertions about quality, value, access and outcomes. It’s highly likely hospitals will be next.

Studies show healthcare affordability is an issue to voters as medical debt soars (KFF) and public disaffection for the “medical system” (per Gallup, Pew) plummets. But does it really matter to the hospitals, insurers, physicians, drug and device manufacturers and army of advisors and trade groups that control the health system?

Each sector talks about affordability blaming inflation, growing demand, oppressive regulation and each other for higher costs and unwanted attention to the issue.

Each play their victim cards in well-orchestrated ad campaigns targeted to state and federal lawmakers whose votes they hope to buy.

Each considers aggregate health spending—projected to increase at 5.4%/year through 2031 vs. 4.6% GDP growth—a value relative to the health and wellbeing of the population. And each thinks its strategies to address affordability are adequate and the public’s concern understandable but ill-informed.

As the House reconvenes this week joining the Senate in negotiating a resolution to the potential federal budget default October 1, the question facing national and state lawmakers is simple: is the juice worth the squeeze?

Is the US health system deserving of its significance as the fastest-growing component of the total US economy (18.3% of total GDP today projected to be 19.6% in 2031), its largest private sector employer and mainstay for private investors?

Does it deserve the legal concessions made to its incumbents vis a vis patent approvals, tax exemptions for hospitals and employers, authorized monopolies and oligopolies that enable its strongest to survive and weaker to disappear?

Does it merit its oversized role, given competing priorities emerging in our society—AI and technology, climate changes, income, public health erosion, education system failure, racial inequity, crime and global tension with China, Russia and others.

In the last 2 weeks, influential Republicans leaders (Burgess, Cassidy) announced plans to tackle health costs and the role AI will play in the future of the system. Last Tuesday, CMS announced its latest pilot program to tackle spending: the States Advancing All-Payer Health Equity Approaches and Development Model (AHEAD Model) is a total cost of care budgeting program to roll out in 8 states starting in 2026. The Presidential campaigns are voicing frustration with the system and the spotlight on its business practices intensifying.

So, is affordability to the federal government likely to get more attention?

Yes. Is affordability on state radars as legislatures juggle funding for Medicaid, public health and other programs?

Yes, but on a program by program, non-system basis.

Is affordability front and center in CMS value agenda including the new models like its AHEAD model announced last week? Not really.

CMS has focused more on pushing hospitals and physicians to participate than engaging consumers. Is affordability for those most threatened—low and middle income households with high deductible insurance, the uninsured and under-insured, those with an expensive medical condition—front of mind? Every minute of every day.

Per CMS, out-of-pocket spending increased 4.3% in 2022 (down from 10.4% in 2021) and “is expected to accelerate to 5.2%, in part related to faster health care price growth. During 2025–31, average out-of-pocket spending growth is projected to be 4.1% per year.” But these data are misleading. It’s dramatically higher for certain populations and even those with attractive employer-sponsored health benefits worry about unexpected household medical bills.

So, affordability is a tricky issue that’s front of mind to 40% of the population today and more tomorrow.

Legislation that limits surprise medical bills, requires drug, hospital and insurer price transparency, expands scope of practice opportunities for mid-level professionals, avails consumers of telehealth services, restricts aggressive patient debt collection policies and others has done little to assuage affordability issues for consumers.

Ditto CMS’ value agenda which is more about reducing Medicare spending through shared savings programs with hospitals and physicians than improving affordability for consumers. That’s why outsiders like Walmart, Best Buy and others see opportunity: they think patients (aka members, enrollees, end users) deserve affordability solutions more than lip service.

Affordability to consumers is the most formidable challenge facing the US healthcare industry–more than burnout, operating margins, reimbursement or alternative payment models. Today, it is not taken seriously by insiders. If it was, evidence would be readily available and compelling. But it’s not.

Favorable selection of healthier beneficiaries led to overpayments in counties with high Medicare Advantage penetration, but benchmark changes could mitigate the impact.

Dive Brief:

Favorable selection of beneficiaries in Medicare Advantage is throwing off benchmarks used to set payments to those plans, resulting in billions of overpayments to the privatized insurance program for seniors, according to a study published this week in Health Affairs.

Healthier people are more likely to enroll in MA compared to traditional Medicare, leading to overpayment in counties with high levels of MA participation and underpayment in counties with less MA market penetration, the study found.

Overall, MA plans were overpaid by an average of $9.3 billion per year between 2017 and 2020. As seniors increasingly turn to MA plans, setting payment benchmarks based on traditional Medicare spending has become “less tenable” and requires reform, researchers argued.

Dive Insight:

Overpayments to MA plans are a growing concern for regulators and researchers as more seniors choose the increasingly popular coverage option. More than half of the eligible Medicare population is now enrolled in MA, a stark increase from 19% of the eligible population enrolled in 2007.

One analysis from the USC Schaeffer Center for Health Policy and Economics found overpayments could reach more than $75 billion this year due to the favorable selection of healthier beneficiaries, aggressive coding and quality bonuses.

MA plans are administered by private insurers and paid a set amount each month regardless of beneficiaries’ use of healthcare services. Those payment rates are set by benchmarks in each county every year alongside quality payments and risk scores based on beneficiaries’ health needs.

But those benchmarks, which are tied to risk-adjusted spending in traditional Medicare, may be contributing to overpayments to MA plans, as healthier people are more likely to choose MA and sicker seniors switch to traditional Medicare plans.

The distribution of MA beneficiaries has also shifted toward counties that were overpaid, according to the study.

In benchmark year 2020, 31.4% of MA beneficiaries lived in underpaid counties, while 68.6% lived in counties that were overpaid, the study found. There were more than 2,700 underpaid counties compared with just over 330 overpaid counties, highlighting the concentration of beneficiaries in counties with high MA market penetration.

In underpaid counties, underpayments totaled a loss of $407 per beneficiary, while overpayments reached an extra $762 per beneficiary in overpaid areas.

Overall, the Health Affairs study estimated that overpayments to MA plans reached $37.3 billion between 2017 and 2020.

The CMS could take action to improve its risk adjustment methodology, which doesn’t take into account favorable selection dynamics for MA, according to the study.

“The simplest strategy would be to allow risk adjustment to vary according to MA penetration, thereby flattening the relationship between traditional Medicare risk and spending across levels of MA penetration,” the authors wrote.

Federal regulators have moved to audit MA plans and are attempting to claw back billions in overpayments.

Insurers have pushed back on the rule. Humana, one of the largest providers of MA plans in the country, sued the HHS last week, arguing the regulation is unfair and should be vacated.

An investigative piece published this month by ProPublica documents how it came to be that nearly 60 percent of healthcare providers report being charged fees to receive electronic payments from insurers.

The fees, which can be as high as five percent of total reimbursement, were briefly forbidden by the Centers for Medicare and Medicaid Services (CMS), before the agency reversed its policy in 2018. The article follows one dogged physician’s efforts to uncover why CMS allows these fees. His voluminous stream of public records requests revealed a highly coordinated pressure campaign, mounted by the insurance industry through one particularly influential regulator-turned-lobbyist.

While the American Medical Association has urged the Biden administration to protect physicians from these fees, and the Veterans Health Administration is refusing to pay them, CMS is so far maintaining the position that electronic-payment claims-processing fees are permissible.

The Gist: Through partnerships with payment companies, who charge double the average fees of electronic bank transfers and share the spoils of their “virtual credit cards”, insurers are essentially using the same business model as credit card companies, skimming revenue from physician payments just as Visa and MasterCard do to merchants.

With the increasing consolidation of both insurers and claims processors, physicians are left with little recourse but to pay these fees, as nonelectronic payments come with infrastructure costs and payment delays.

While the shift to electronic payments spurred on by the Affordable Care Act was supposed to improve efficiency, this article offers yet another example of how efficiency gains can be captured by industry middlemen before they can be translated into provider and consumer benefits.

This week, the Centers for Medicare and Medicaid Services (CMS) for the second time suspended the arbitration process, outlined in the No Surprises Act, for new out-of-network payment disputes between providers and payers.

Federal judge Jeremy Kernodle in the Eastern District of Texas once again sided with the Texas Medical Association (TMA) in the lawsuit, which challenged CMS’s 2023 increase in administrative fees for arbitration (from $50 to $350), as well as restrictions on batching claims, which require providers to go through a separate IDR process for each claim related to an individual’s care episode. While CMS said that it made these changes to increase arbitration efficiency, TMA argued that the changes made the IDR process cost-prohibitive for providers, particularly smaller practices.

The Gist: Implementing the No Surprises Act has been a huge headache for CMS. Since it went into effect last spring, the IDR has seen a case load nearly 14 times greater than initially estimated, and has been hampered with delays. Insurers have blamed providers for overloading the system with frivolous claims, while providers have accused insurers of ignoring payment decisions determined by third-party arbiters or declining to pay in full.

The silver lining amid all this infighting is that the No Surprises Act is successfully preventing surprise bills for many consumers, despite the intra-industry turf war over its implementation.

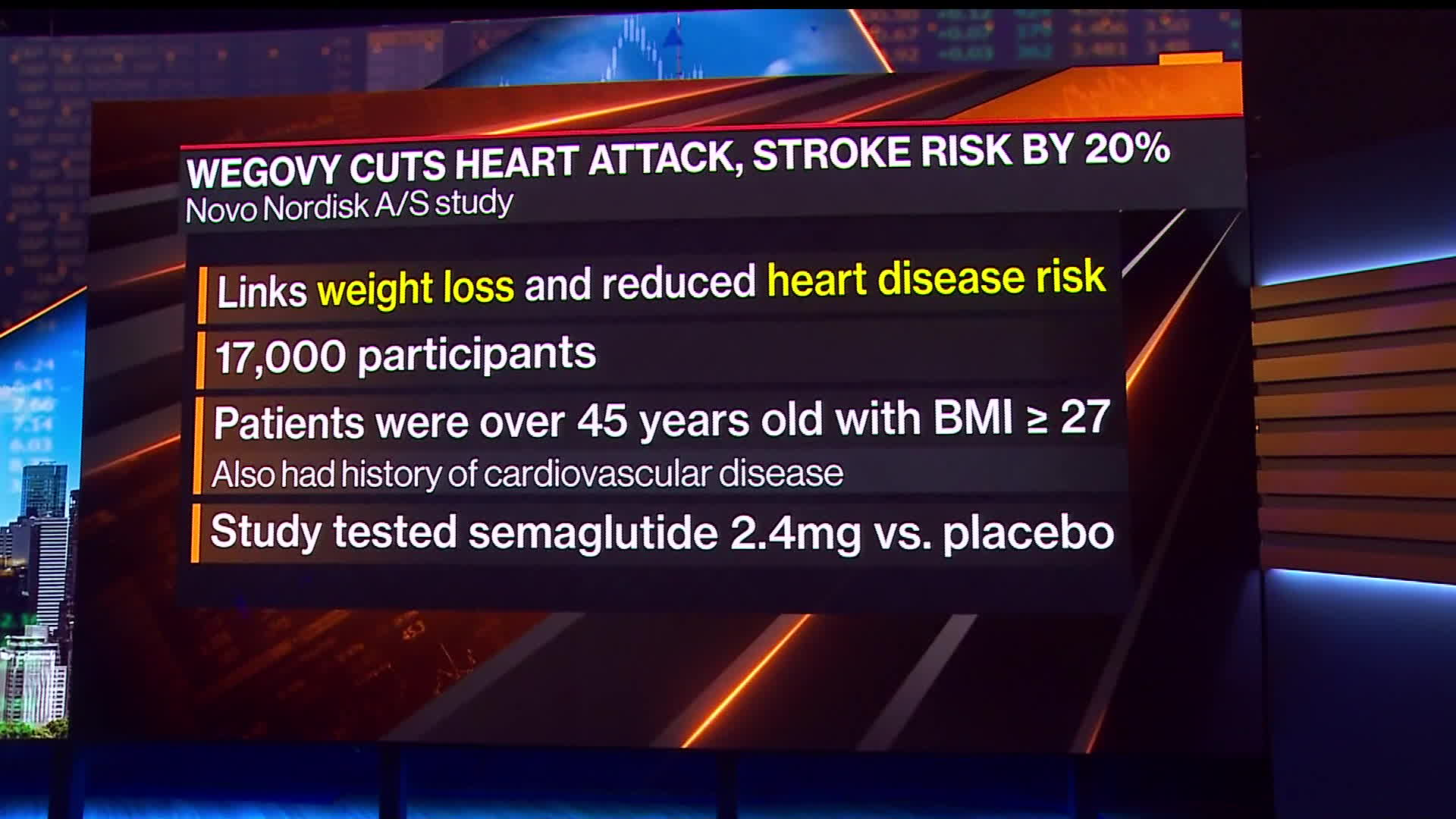

On Tuesday, Novo Nordisk released the headline results of a large clinical trial demonstrating that its popular GLP-1 inhibitor Wegovy reduced the risk of heart attacks, strokes, and cardiovascular deaths by 20 percent. The SELECT trial enrolled roughly 17,600 non-diabetic adults aged 45 and older who were overweight or obese with established cardiovascular disease. It compared people in this population treated with the drug to those given a placebo, and tracked them for up to five years. The drugmaker said it plans to release the full trial results at a conference later this year. These results are similar to a previous study that found Wegovy sister drug Ozempic, also made by Novo Nordisk, reduced the risk of adverse cardiac events by 26 percent in adults with type 2 diabetes.

The Gist: The cardioprotective effects demonstrated in this study far exceeded researchers’ expectations. Though concerns still abound about the high costs of Wegovy (nearly $1,350 per month) and similar drugs, these results will certainly put pressure on Medicare and other insurers to provide coverage.

Questions remain around how the drug actually improves cardiovascular outcomes, and whether patients with cardiac disease who are not overweight or obese might also benefit from taking it.

Despite the fact that the data are still preliminary, the argument that obesity medications are solely “lifestyle” or “vanity drugs”—which some insurers and employers have been using to deny coverage—will now be much harder to defend.

Starting next month, UnitedHealthcare says it will move forward with plans to drop prior authorization requirements for a range of procedures, including dozens of radiology services and genetic tests, among others.

Why it matters:

UnitedHealth is among the health insurance giants who have announced plans to cut back on prior authorization as federal regulators consider tougher curbs on the practice.

Catch up quick:

Prior authorization is often criticized by patients and doctors, who complain they are an administrative burden or impede necessary care. Insurers, meanwhile, say prior authorization provides important guardrails against improper health care utilization, helping to keep costs down.

UnitedHealth, the largest commercial U.S. insurer, previously said its prior authorization removals will represent roughly 20% of its overall prior authorization volume.

Cigna and Aetna also announced plans to roll back some prior authorization requirements.

The Centers for Medicare and Medicaid Services proposed a rule to limit the amount of time insurers have to review requests on services for which they require prior approval, BenefitsPro previously reported.

Congress is also eyeing a plan to streamline and add transparency to the process by which Medicare Advantage plans can deny coverage for services via prior authorization.

Zoom in:

UnitedHealth says the removals will take effect Sept. 1 and Nov. 1 across the vast majority of its plans.

The company also spelled out which procedures would see prior authorization requirements removed. For instance, hundreds of codes for genetic testing — accounting for tens of thousands of prior authorization requests a year from commercial and Medicaid members — are among those that will be removed, officials said.

A code for cardiology stress test prior authorization for Medicare Advantage members will also be eliminated, reducing roughly 316,000 prior authorization requests a year.

The company next year also will roll out a “gold card” program eliminating most prior authorization requirements for doctors who have high approval rates.

Flashback: Earlier this summer, UnitedHealth walked back a controversial plan to require prior authorizations for colonoscopies and other endoscopic procedures.

A federal drug discount program for safety-net providers that’s been a perennial source of fierce disputes among health care industry powerhouses is back in the spotlight, with billions of dollars at stake.

The big picture:

Separate but coinciding issues are generating renewed focus on the decades-old 340B program, which requires that drugmakers give large discounts on outpatient drugs to health care providers serving low-income patients.

A Biden administration proposal to issue hefty back payments due to 340B providers, drugmakers’ efforts to limit discounts, and rebooted congressional interest in broader reforms are again igniting debate about the program’s scope.

Context:

The Supreme Court last year unanimously sided with hospitals who challenged a nearly 30% reduction to their 340B payments by the Centers for Medicare and Medicaid Services that began under the Trump administration.

In response to the court decision, CMS last month announced a $9 billion plan to repay 340B providers that’s generated some controversy. While 340Bhospitals are happy they’re getting paid back, industry groups are upset that the payments are funded by clawing back money to other hospitals.

Meanwhile, the Biden administration is battling drugmakers in court over restrictions they’ve placed on where hospitals can use their 340B discounts.

A bipartisan group of senators this summer also released a request for information on how to improve stability and oversight within the program.

Hospitals could face further cutbacks if Congress or the courts place new limits on 340B.

Flashback:

The 340B program began in 1992 to help providers serving patient populations who struggled to afford their prescription drugs. It allowshospitals and other safety-net providers like community health clinics to save an average of 25% to 50% on drug purchases, according to the federal government.

When hospitals partner with off-site pharmacies to dispense drugs, the pharmacies also benefit financially from 340B savings.

The program has grown significantly since its inception, increasing from 8,100 participating safety-net providers in 2000 to 50,000 in 2020.

Between the lines:

The expansive program growth has drawn lawmakers’ scrutiny and complaints from pharmaceutical companies, who accuse providers of using the program to pad their profits rather than help vulnerable patients. Providers dispute those accusationsand say the program helps them stretch limited federal resources.

More than 20 drug companies have placed restrictions on when providers can use 340B discounts at off-site pharmacies. Drug companies say the limits help prevent them from having to give duplicate discounts, which occurswhen both the provider and state Medicaid agency receive a discount on the same drug.

The Biden administration asked several drugmakers to lift their 340B restrictions and threatened fines if they don’t comply.

Several drugmakers have sued the administration, arguing federal officials didn’t have the right to stop them from limiting discounts. One appellate judge ruled in favor of drugmakers earlier this year, and two other cases are pending in federal appellate courts.Experts say the cases could go all the way to the Supreme Court.

As the legal fight plays out, 340B providers are urging Congress to approve new measures to prevent drugmakers from restricting access to discounts.

The other side: Drugmakers, meanwhile, want lawmakers to tightenhospital eligibility standards and place stronger limits on how 340B pharmacies can profit from the program.

Of note: Rural hospitals, some of which were spared from the 340B cuts made years ago, are especially concerned about the hit they would takefrom CMS’ proposed funding clawbacks.

Rural facilities today rely heavilyon 340B to offset other financial losses, Brock Slabach, chief operations officer at the National Rural Health Association, told Axios.

“You can’t get out of this problem without harming those who were helped,” Slabach said.

What we’re watching: Expect to keep hearing about 340B in the coming months.

CMS still needs to finalize the 340B repayment planafter the public comment ends Sept. 5.

The D.C. Circuit Court of Appeals and the 7th Circuit Court of Appeals will issue rulings on whether the Biden administration can reverse drugmakers’340B restrictions.

Congress could take up a serious reform effort following the Senate’s information request, though that would take time.