The Supreme Court on Friday upheld a key Affordable Care Act requirement that insurance companies cover certain preventative measures recommended by an expert panel.

Justices upheld the constitutionality of the provision in a 6-3 decision and protected access to preventative care for about 150 million Americans.

The justices found that the secretary of the Department of Health and Human Services has the power to appoint and fire members of the U.S. Preventative Services Task Force (USPSTF).

The cases started when a small business in Texas and some individuals filed a lawsuit against the panel’s recommendation that pre-exposure prophylaxis (PreP) for HIV be included as a preventative care service.

They argued that covering PreP went against their religious beliefs and would “encourage homosexual behavior, intravenous drug use, and sexual activity outside of marriage between one man and one woman.”

The plaintiffs further argued that the USPSTF mandates are unconstitutional because panel members are “inferior officers” who are not appointed by the president or confirmed by the Senate.

While the panel is independent, they said that since their decisions impact millions of people members should be confirmed.

A U.S. district judge in 2023 ruled that all preventative-care coverage imposed since the ACA was signed into law areinvalid and a federal appeals court judge ruled in agreement last year.

The Biden administration appealed the rulings to the Supreme Court, and the Trump administration chose to defend the law despite its long history of disparaging Obamacare.

Though public health groups celebrated the ruling Friday, some noted another potential outcome.

“While this is a foundational victory for patients, patients have reason to be concerned that the decision reaffirms the ability of the HHS secretary, including our current one, to control the membership and recommendations of the US Preventive Services Task Force that determines which preventive services are covered,” Anthony Wright, executive director of Families USA, said in a statement.

“We must be vigilant to ensure Secretary Kennedy does not undo coverage of preventive services by taking actions such as his recent firing of qualified health experts from the CDC’s independent vaccine advisory committee and replacing them with his personal allies.”

The Trump administration is moving into its second 100 days facing conditions more problematic than its first 100. For healthcare, this period will define the industry’s near-term future as changes in three domains unfold:

The Economy: The economy is volatile and consumer confidence is waning. The impact of tariffs on U.S. prices remains an unknown and escalating tension between the Ukraine and Russia, Israel and Palestine, Pakistan and India are worrisome. Household debt is mounting as student loans, medical debt and housing costs imperil financial security for more than half of U.S. households. The 3 major stock indices remain in the red YTD, prospects for a recession are high and investors are increasingly cautious. Net impact on healthcare organizations and public programs: negative, especially those without strong balance sheets and access to affordable private capital.

The Courts: Recent opinions by the Supreme Court and District Courts suggest a willingness to challenge the administration’s Executive Orders on immigrant deportation and due process, threats and funding cuts aimed at law firms and universities considered “woke” and layoffs initiated by DOGE and more. Court challenges will slow the administration’s agenda and create uncertainty in workplaces. Net impact: negative. Uncertainty paralyses planning and operations in every public and private healthcare organization.

The Public Mood: The afterglow of the election has dissipated and the public’s mood has shifted from guarded optimism to anxiety and despair. The public’s uncertain about tariffs and worried about household expenses. Net impact: negative. Healthcare affordability and prices are major concerns to consumers: the majority (76%) think the system is more concerned about profitability than patient care (Jarrard).

Current events in these areas portend headwinds for most public and private healthcare organizations where attention in the next 100 days will be focused in these areas:

Oversight: New rules, programmatic priorities, key personnel appointments and re-organization in HHS, CMS, the FDA and VA: RFKJ’s MAHA plans and Commission appointees, Oz’ affinity for Medicare Advantage predisposition toward value-based care and Makary’s overhaul of the FDA’s drug oversight process will be “on the table” in the next 100 days.

Funding: Healthcare funding in the FY 2026 federal budget. The GOP-controlled House and Senate can pass a budget with minimal support from Dem’s that reflects a serious effort to reduce the federal debt ($37 trillion/123% of GDP– up from $20 trillion in 2017). Healthcare cuts expected to be significant though rumored massive cuts to Medicaid unlikely.

States: State healthcare referenda and executive actions: states are evaluating price controls on drugs and hospitals, reparations from insurers for delays and prior-authorizations, scope of practice restrictions and more. Topping the watchlist in most states is Medicaid funding and potential fallout from discontinued ACA marketplace subsidies factored into the FY 2026 budget being finalized by the GOP-led Congress in DC.

SCOTUS: Supreme Court decisions will be handed down or before June 30 when SCOTUS’ 2024 term ends including Braidwood Management v. Becerra which will determine whether the Affordable Care Act’s requirement that private insurers cover preventive services without cost-sharing will continue. The court will also opine to the authority of the HHS secretary to appoint members of the U.S. Preventive Services Task Force. The potential impact of these decisions on coverage, insurance premiums and access to preventive health services is pervasive.

Financial markets: Capital markets are in a watchful waiting mode as US trade policy unfolds, inflation fluctuates, the fed’s interest rate determination is disclosed and consumer spending reacts. Private investing in healthcare remains opportunistic though deal flow is shifting and risk thresholds tightening.

Polls: Polls draw the attention of media and elected officials. They influence how organizations prioritize advocacy strategies, address consumer complaints and concerns and manage reputations. As reflected in numerous national polls, trust in the system and its key players—insurers, hospitals, drug companies—is at a historic low.

Each sector in U.S. healthcare will be impacted differently: Three face the strongest headwinds:

Hospitals: Hospitals face enormous financial challenges, especially not-for-profits, safety net, rural and veteran’s hospitals. Last week’s unfavorable SCOTUS decision against hospitals alleging DSH under-payments will cost $1 billion per year. Congressional adoption of site neutral payment policy could cost $15 billion/year. Drug prices, labor costs, insurer payment cuts and red-tape will negate operating margins and lower investment income knee-capping growth and innovation plans. Complicating matters, employed physicians will demand higher pay and more control. And Congressional budget-creators believe the sector’s 31% share of total healthcare spending makes it ripe for cuts attributable to “waste, fraud and abuse”.

Insurers: Medicare Advantage (which enjoys support by key administrators including CMS’ Mehmet Oz) has become a lightening rod of insurer criticism alongside prior authorization policies that restrict care. Coverage remains key to household financial security but insurers are seen as barriers to rather than facilitators of evidence-based cost-effective care. And the concentration of power in corporate titans (United, Humana, Cigna, CVS, Centene and others) is viewed with skepticism.

Public Health: Public health is not a priority in the U.S. health system despite recognition that social determinants account for 70% of the system’s $5 trillion spending. Most programs are funded by state and local governments with federal support limited. Public health is not seen as an investment and, in some settings treated with disdain as welfare or waste. As Mayors and Governors develop plans for the rest of 2025 and through 2026, public health cuts will be likely as federal co-funding becomes scarce.

The next 100 days will define the national agenda for the mid-term election in November 2026, reflect the solidarity of the MAGA movement and show the impact of tariffs on inflation, consumer prices and the public’s mood.

Healthcare leaders will be watching closely. All will be impacted.

In 126 days, U.S. voters will settle Campaign 2024 choosing the winners for 435 House seats, 34 Senate seats, 13 Governors and the White House. When final votes are counted, the last week of June, 2024 will be seen as the tipping point when much about politics and policy was re-set as the result of two events:

1-The ‘Great Debate’:

Thursday’s standoff between President Biden and former President Trump drew 51.3 million viewers across 17 networks that carried it. That’s well below previous head-to-head debate match-ups i.e. 84 million for Clinton-Trump in 2016, 73 million for Trump and Biden in 2020. Perhaps more telling, only 3.9 million of these were adults 18-34– 7.6% of debate viewers but 22.9% of U.S. population.

While pundits debated the fitness of the President to continue and speculated about alternative candidates over the weekend, the majority of Americans paid no attention—especially young adults. They think both candidates are old.

In 2020, 57% of 18–34-year-olds voted for a Presidential candidate vs. 69% of 35–64-year-olds and 74% of voters 65+.

Polls show young adults think the political system is fundamentally flawed and partisanship harmful to policies that advance the well-being of the population. They also show their declining trust and confidence in America’s institutions—the press, big business, Congress, organized religion and the medical system.

Young adults get their information from social media and friends and they’re tuning out spin in politics.

2-Supreme Court decisions impacting healthcare:

As is customary for the high court, many of its rulings are handed down in the last week of June before it adjourns for the summer. Only one case remains in limbo: Presidential immunity with a decision expected today. Of the 61 cases SCOTUS has heard in its 2023-2024 term, these four decisions are the most significant to the health industry:

Power of federal agencies (Loper Bright Enterprises v. Raimondo and Relentless, Inc. v. Dept. of Commerce): By a vote of 6-3, SCOTUS ruled that judges no longer have to defer to agency officials when interpreting ambiguous federal statutes about the environment, the workplace, public health and other aspects of American life overturning a 40-year-old legal precedent known as “Chevron deference.” The court’s decision will significantly curtail the power federal agencies have to regulatethousands of private companies, products, industries and the environment.

Emergency room abortions (Idaho v. U.S): SCOTUS ruled 6-3 that hospitals in Idaho that receive federal fundsmust allow emergency abortion care to stabilize patients — even though the state strictly bans the procedure.

Opioid lawsuit settlement (Harrington v. Purdue Pharma): By a vote of 5-4, the justices blocked a controversialPurdue Pharma bankruptcy plan that would have provided billions of dollars to address the nation’s opioid crisis in exchange for protecting the family that owns the company from future lawsuits. The majority found that the plan was invalid because all the affected parties had not been consulted on the deal

Abortion medication restrictions (FDA v. Alliance for Hippocratic Medicine): By a vote of 9-0, the justices maintained broad access to mifepristone, unanimously reversing a lower court decision that would have made the widely used abortion medication more difficult to obtain. The decision was not on the substance of the case, but a procedural ruling that the challengers did not have legal grounds to bring their lawsuit.

Based on these events last week, healthcare organizations and their trade groups making plans for 2025 and beyond should consider:

Young adults. Out of Sight, Out of Mind: Polling data shows young adults think the health system is broken and alternatives worth considering. Affordability, equitable access and price transparency matter to them. Their finances are stretched as inflation (housing, energy, food et al), their medical debt prevalent and mounting and their employers are cutting their health benefits and forcing them to assume more out-of-pocket responsibility. Hospitals, insurers, physicians and drug companies pay close attention to older working age consumers and seniors. They pay little attention to younger adults, and the reverse is true. But history teaches that social movements originate from disenchanted youth and young adults who feel taken for granted, abused by corporate greed and unheard. Might the healthcare status quo be a target?

The federal administrative state in flux: The ripple effect of the court’s Chevron decision is equivalent to its decision ending Roe v. Wade (June 2022). The latitude afforded key federal agencies i.e. CDC, CMS, OSHA, CMMI, FDA, HRSA et al will be revisited. States will be forced to step in where federal guidance is in jeopardy. Governors and the White House will face more frequent court challenges on their Executive Orders and agencies for their Administrative Actions as government oversight of healthcare evolves. For investors, safe bets will be targets. For hospitals, insurers and physicians, federal advocacy will require recalibration.

The administrative state flux means state legislatures and ballot referenda will play a bigger role in healthcare. States already have enormous responsibilities for healthcare:

Medicaid coverage determination

Retail Health i.e. services (efficacy), truth in advertising, consumer safety et al

Public health services i.e. STDs, disease surveillance, immunization policies et al.

Prescription Drug Affordability (in 11 states)

Health Insurance Marketplaces

Healthcare workforce scope of practice

Medical Malpractice and consumer protections

Abortion Rights: as a result of the 2022 Supreme Court ruling that Roe v. Wade

Behavioral health, substance abuse workforce adequacy, licensure, scope of practice et al.

Certificate of Need Programs

Use Medical Marijuana (Cannabis) for Therapeutics and/or Recreational Use.

Health Insurer Licensing, Network adequacy and Liquidity

Quality and patient safety inspection in post-acute & home-based settings.

Workers’ compensation eligibility, administration use and funding.

Formulary design and expense control.

School clinics

Prison health

And others

The court decisions last week open the door to additional actions by state agencies and elected officials in areas where federal policies are in limbo:

Tax exemptions for not-for-profit health systems

Hospital consolidation and price transparency,

Accessibility of hospital emergency services for abortion,

Insurer prior authorization and network adequacy

Minimum staffing requirements,

Telehealth use and payment

Restrictive drug formulary

And more.

For every healthcare organization and trade group, vigilance about pending legislation/action at the state level will take on added importance.

The U.S. health system’s future is not a repeat of its past: The week’s events lend to the health industry’s uncertain future. Today, strategic planning in most U.S. healthcare organizations i.e. insurers, hospitals, physician organization, device and drug manufacturers, et al is based on incremental changes forecast 3-5 years out. While consideration is given “transformational” changes 10-15 years out, it is under-studied by planners and rarely included on board agenda dockets. Yet, signal detection of disruptive shifts in financial services, higher education and other industries predict winners and losers. The U.S. system is change-averse because it benefits its self-interests. Outsiders do not share this view. No trade group or organization in healthcare can afford to bet its future on incrementalism in healthcare. These court decisions and the pending election results suggest that healthcare’s future is not a repeat of its past: new rules, new players and new critical success factors are inevitable.

It was a big week for U.S. politics and perhaps a bigger week for healthcare. Stay tuned.

In February, the American Hospital Association and five other hospital organizations had urged the court to review the case. The current formula costs DHS hospitals more than a billion dollars each year, according to the AHA.

“The AHA is pleased that the Supreme Court agreed to consider this case,” said Chad Golder, AHA general counsel and secretary, by statement. “As we explained in our amicus brief urging the Court to grant certiorari, it is critical to hospitals and health systems that HHS interpret the DSH fraction consistently across the statute. The agency’s longstanding failure to do so has cost hospitals more than a billion dollars each year, directly harming the hospitals that serve America’s most vulnerable patients. We look forward to the Supreme Court rectifying this legal error next term.”

WHY THIS MATTERS

This case, and one heard by SCOTUS in 2002 called Becerra v. Empire Health Foundation, can be viewed as being two sides of the same coin. Both deal with a different portion of the DSH fraction that determines payment. The Empire Health case dealt with the Medicare portion. This latest case is about the Supplemental Security Income portion.

The AHA and other organizations have argued that HHS incorrectly adopted the view that a patient is entitled to Supplemental Security Income benefits only if the patient actually received cash SSI payments during a hospital stay. This interpretation is inconsistent with the court’s reasoning in Becerra v. Empire Health Foundation, the AHA said.

That 2022 decision said that patients are entitled to Medicare Part A benefits for purposes of the DSH formula if they qualify for the program, even if Medicare is not paying for their hospital stay.

“This case concerns a question that is critical to calculating the Medicare DSH fraction: When are patients ‘entitled to’ SSI benefits and so counted in the numerator? Is it when they are eligible for SSI benefits, or when they are actually receiving cash SSI benefits,” the AHA and other organizations wrote in their brief to the court.

THE LARGER TREND

In February, the American Hospital Association and five other national hospital associations representing hospitals urged the Court to review the case challenging how HHS applies Congress’ formula for calculating Disproportionate Share Hospital payments..

“The correct interpretation of the DSH formula is vitally important to America’s hospitals,” the brief said. “Although HHS has refused to share the data that would allow hospitals to accurately count the SSI-eligible patients whom the agency’s approach excludes, the available estimates suggest that hospitals will lose more than a billion dollars each year in DSH funds. What’s more, a hospital’s eligibility for DSH payments affects its entitlement to other federal benefits designed to help hospitals ‘provide a wide range of medical services’ to vulnerable populations. HHS’s error thus has far-reaching implications for hospitals, patients, and the American healthcare system.”

Becerra v. Empire Health Foundation was a United States Supreme Court case that in 2022 clarified calculations for the Medicare fraction — one of two fractions the Medicare program uses to adjust the rates paid to hospitals that serve a higher-than-usual percentage of low-income patients, according to SCOTUSblog. Those individuals “entitled to [Medicare Part A] benefits” are all those qualifying for the program, regardless of whether they receive Medicare payments for part or all of a hospital stay, the court ruled.

In Becerra v. Empire Health Foundation, the court ruled 5-4 that HHS had properly interpreted the underlying statute and reversed and remanded the decision of the United States Court of Appeals for the Ninth Circuit.

Three critical healthcare struggles will define the year to come with cutthroat competition and intense disputes being played out in public:

1. A Nation Divided Over Abortion Rights

2. The Generative AI Revolution In Medicine

3. The Tug-Of-War Over Healthcare Pricing American healthcare, much like any battlefield, is fraught with conflict and turmoil. As we navigate 2024, the wars ahead seem destined to intensify before any semblance of peace can be attained. Let me know your thoughts once you read mine.

Modern medicine, for most of its history, has operated within a collegial environment—an industry of civility where physicians, hospitals, pharmaceutical companies and others stayed in their lanes and out of each other’s business.

It used to be that clinicians made patient-centric decisions, drugmakers and hospitals calculated care/treatment costs and added a modest profit, while insurers set rates based on those figures. Businesses and the government, hoping to save a little money, negotiated coverage rates but not at the expense of a favored doctor or hospital. Disputes, if any, were resolved quietly and behind the scenes.

Times have changed as healthcare has taken a 180-degree turn. This year will be characterized by cutthroat competition and intense disputes played out in public. And as the once harmonious world of healthcare braces for battle, three critical struggles take centerstage. Each one promises controversy and profound implications for the future of medicine:

1. A Nation Divided Over Abortion Rights

For nearly 50 years, from the landmark Roe v. Wade decision in 1973 to its overruling by the 2022 Dobbs case, abortion decisions were the province of women and their doctors. This dynamic has changed in nearly half the states.

This spring, the Supreme Court is set to hear another pivotal case, this one on mifepristone, an important drug for medical abortions. The ruling, expected in June, will significantly impact women’s rights and federal regulatory bodies like the FDA.

Traditionally, abortions were surgical procedures. Today, over half of all terminations aremedically induced, primarily using a two-drug combination, including mifepristone. Since its approval in 2000, mifepristone has been prescribed to over 5 million women, and it boasts an excellent safety record. But anti-abortion groups, now challenging this method, have proposed stringent legal restrictions: reducing the administration window from 10 to seven weeks post-conception, banning distribution of the drug by mail, and mandating three in-person doctor visits, a burdensome requirement for many. While physicians could still prescribe misoprostol, the second drug in the regimen, its effectiveness alone pales in comparison to the two-drug combo.

Should the Supreme Court overrule and overturn the FDA’s clinical expertise on these matters, abortion activists fear the floodgates will open, inviting new challenges against other established medications like birth control.

In response, several states have fortified abortion rights through ballot initiatives, a trend expected to gain momentum in the November elections. This legislative action underscores a significant public-opinion divide from the Supreme Court’s stance. In fact, a survey published in Nature Human Behavior reveals that 60% of Americans support legal abortion.

Path to resolution: Uncertain. Traditionally, SCOTUS rulings have mirrored public opinion on key social issues, but its deviation on abortion rights has failed to shift public sentiment, setting the stage for an even fiercer clash in years to come. A Supreme Court ruling that renders abortion unconstitutional would contradict the principles outlined in the Dobbs decision, but not all states will enact protective measures. As a result, America’s divide on abortion rights is poised to deepen.

2. The Generative AI Revolution In Medicine

A year after ChatGPT’s release, an arms race in generative AI is reshaping industries from finance to healthcare. Organizations are investing billions to get a technological leg up on the competition, but this budding revolution has sparked widespread concern.

In Hollywood, screenwriters recently emerged victorious from a 150-day strike, partially focused on the threat of AI as a replacement for human workers. In the media realm, prominent organizations like The New York Times, along with a bevy of celebs and influencers, have initiated copyright infringement lawsuits against OpenAI, the developer of ChatGPT.

The healthcare sector faces its own unique battles. Insurers are leveraging AI to speed up and intensify claim denials, prompting providers to counter with AI-assisted appeals.

But beyond corporate skirmishes, the most profound conflict involves the doctor-patient relationship. Physicians, already vexed by patients who self-diagnose with “Dr. Google,” find themselves unsure whether generative AI will be friend or foe. Unlike traditional search engines, GenAI doesn’t just spit out information. It provides nuanced medical insights based on extensive, up-to-date research. Studies suggest that AI can already diagnose and recommend treatments with remarkable accuracy and empathy, surpassing human doctors in ever-more ways.

Path to resolution: Unfolding. While doctors are already taking advantage of AI’s administrative benefits (billing, notetaking and data entry), they’re apprehensive that ChatGPT will lead to errors if used for patient care. In this case, time will heal most concerns and eliminate most fears. Five years from now, with ChatGPT predicted to be 30 times more powerful, generative AI systems will become integral to medical care. Advanced tools, interfacing with wearables and electronic health records, will aid in disease management, diagnosis and chronic-condition monitoring, enhancing clinical outcomes and overall health.

3. The Tug-Of-War Over Healthcare Pricing

From routine doctor visits to complex hospital stays and drug prescriptions, every aspect of U.S. healthcare is getting more expensive. That’s not news to most Americans, half of whom say it is very or somewhat difficult to afford healthcare costs.

But people may be surprised to learn how the pricing wars will play out this year—and how the winners will affect the overall cost of healthcare.

Throughout U.S. healthcare, nurses are striking as doctors are unionizing. After a year of soaring inflation, healthcare supply-chain costs and wage expectations are through the roof. A notable example emerged in California, where a proposed $25 hourly minimum wage for healthcare workers was later retracted by Governor Newsom amid budget constraints.

Financial pressures are increasing. In response, thousands of doctors have sold their medical practices to private equity firms. This trend will continue in 2024 and likely drive up prices, as much as 30% higher for many specialties.

Meanwhile, drug spending will soar in 2024 as weight-loss drugs (costing roughly $12,000 a year) become increasingly available. A groundbreaking sickle cell disease treatment, which uses the controversial CRISPR technology, is projected to cost nearly $3 million upon release.

To help tame runaway prices, the Centers for Medicare & Medicaid Services will reduce out-of-pocket costs for dozens of Part B medications “by $1 to as much as $2,786 per average dose,” according to White House officials. However, the move, one of many price-busting measures under the Inflation Reduction Act, has ignited a series of legal challenges from the pharmaceutical industry.

Big Pharma seeks to delay or overturn legislation that would allow CMS to negotiate prices for 10 of the most expensive outpatient drugs starting in 2026.

Path to resolution: Up to voters. With national healthcare spending expected to leap from $4 trillion to $7 trillion by 2031, the pricing debate will only intensify. The upcoming election will be pivotal in steering the financial strategy for healthcare. A Republican surge could mean tighter controls on Medicare and Medicaid and relaxed insurance regulations, whereas a Democratic sweep could lead to increased taxes, especially on the wealthy. A divided government, however, would stall significant reforms, exacerbating the crisis of unaffordability into 2025.

Is Peace Possible?

American healthcare, much like any battlefield, is fraught with conflict and turmoil. As we navigate 2024, the wars ahead seem destined to intensify before any semblance of peace can be attained.

Yet, amidst the strife, hope glimmers: The rise of ChatGPT and other generative AI technologies holds promise for revolutionizing patient empowerment and systemic efficiency, making healthcare more accessible while mitigating the burden of chronic diseases. The debate over abortion rights, while deeply polarizing, might eventually find resolution in a legislative middle ground that echoes Roe’s protections with some restrictions on how late in pregnancy procedures can be performed.

Unfortunately, some problems need to get worse before they can get better. I predict the affordability of healthcare will be one of them this year. My New Year’s request is not to shoot the messenger.

In the last 2 weeks, the Affordable Care Act (ACA) has been inserted itself in Campaign 2024 by Republican aspirants for the White House:

On Truth Social November 28, former President Trump promised to replace it with something better:“Getting much better Healthcare than Obamacare for the American people will be a priority of the Trump Administration. It is not a matter of cost; it is a matter of HEALTH. America will have one of the best Healthcare Plans anywhere in the world. Right now, it has one of the WORST! I don’t want to terminate Obamacare, I want to REPLACE IT with MUCH BETTER HEALTHCARE. Obamacare Sucks!!!!”

Then, on NBC’s Meet the Press December 3, Florida Governor Ron DeSantis offered “We need to have a healthcare plan that works,” Obamacare hasn’t worked. We are going to replace and supersede with a better plan….a totally different healthcare plan… big institutions that are causing prices to be high: big pharma, big insurance and big government.”

It’s no surprise. Health costs and affordability rank behind the economy as top issues for Republican voters per the latest Kaiser Tracking Poll. And distaste with the status quo is widespread and bipartisan: per the Keckley Poll (October 2023), 70% of Americans including majorities in both parties and age-cohorts under 65 think “the system is fundamentally flawed and needs major change.” To GOP voters, the ACA is to blame.

Background:

The Affordable Care Act (aka Obamacare aka the Patient Protection and Affordable Care Act) was passed into law March 23, 2013. It is the most sweeping and controversial health industry legislation passed by Congress since Lyndon Johnson’s Medicare and Medicaid Act (1965). Opinions about the law haven’t changed much in almost 14 years: when passed in 2010, 46% were favorable toward the law vs. 40% who were opposed. Today, those favorable has increased to 59% while opposition has stayed at 40% (Kaiser Tracking Poll).

Few elected officials and even fewer voters have actually read the law. It’s understandable: 955 pages, 10 major sections (Titles) and a plethora of administrative actions, executive orders, amendments and legal challenges that have followed. It continues to be under-reported in media and misrepresented in campaign rhetoric by both sides. Campaign 2024 seems likely to be more of the same.

In 2009, I facilitated discussions about health reform between the White House Office of Health Reform and the leading private sector players in the system (the American Medical Association, the American Hospital Association, America’s Health Insurance Plans, AdvaMed, PhRMA, and BIO). The impetus for these deliberations was the Obama administration’s directive that systemic reform was necessary with three-aims: reduce cost, increase access via insurance coverage and improve the quality of care provided by a private system. In parallel, key Committees in the House and Senate held hearings ultimately resulting in passage of separate House and Senate versions with the Senate’s becoming the substance of the final legislation. Think tanks on the left (I.e. the Center for American Progress et al.) and on the right (i.e. the Heritage Foundation) weighed in with members of Congress and DC influencers as the legislation morphed. And new ‘coalitions, centers and institutes’ formed to advocate for and against certain ACA provisions on behalf of their members while maintaining a degree of anonymity.

So, as the ACA resurfaces in political discourse in coming months, it’s important it be framed objectively. To that end, 3 major considerations are necessary to have a ‘fair and balanced’ view of the ACA:

1-The ACA was intended as a comprehensive health reform legislative platform. It was designed to be implemented between 2010 and 2019 in a private system prompted by new federal and state policies to address cost, access and quality. It allowed states latitude in implementing certain elements (like Medicaid expansion, healthcare marketplaces) but few exceptions in other areas (i.e.individual and employer mandates to purchase insurance, minimum requirements for qualified health plans, et al). The CBO estimated it would add $1.1 trillion to overall healthcare spending over the decade but pay for itself by reducing demand, administrative red-tape and leveraging better data for decision-making. The law included provisions to…

To improve quality by modernizing of the workforce, creating an Annual Quality Report obligation by HHS, creating the Patient Centered Outcome Research Institute and expanding the the National Quality Forum, adding requirements that approved preventive care be accessible at no cost, expanding community health centers, increasing residency programs in primary care and general surgery, implementing comparative effectiveness assessments to enable clinical transparency and more.

To increase access to health insurance by subsidizing coverage for small businesses and low income individuals (up to 400% of the Federal poverty level), funding 90% of the added costs in states choosing to expand their Medicaid enrollments for households earning up to 138% of the poverty level, extending household coverage so ‘young invincibles’ under 26 years of age could stay on their parent’s insurance plan, requiring insurers to provide “essential benefits” in their offerings, imposing medical loss ratio (MLR) mandates (80% individual, 85% group) and more.

To lower costs by creating the CMS Center for Medicare and Medicaid Innovation to construct 5-year demonstration pilots and value-based purchasing programs that shift provider incentives from volume to value, imposing price and quality reporting and transparency requirements and more.

The ACA was ambitious: it was modeled after Romneycare in MA and premised on the presumption that meaningful results could be achieved in a decade. But Romneycare (2006) was about near-universal insurance coverage for all in the Commonwealth, not the triple aim, and the resistance calcified quickly among special interests threatened by its potential.

2-The ACA passed at a time of economic insecurity and hyper-partisan rancor and before many of the industry’s most significant innovations had taken hold. The ACA was the second major legislation passed in the first term of the Obama administration (2009-2012); the first was the $831 billion American Recovery and Reconstruction Act (ARRA) stimulus package that targeted “shovel ready jobs” as a means of economic recovery from the 2008-2010 Great Recession. But notably, it included $138 billion for healthcare including requirements for hospitals and physicians to computerize their medical records, extension of medical insurance to laid off workers and additional funding for states to offset their Medicaid program expenses. The Obama-Biden team came to power with populist momentum behind their promises to lower health costs while keeping the doctors and insurance plans they had. Its rollout was plagued by miscues and the administration’s most popular assurances (‘keep your doctor and hospitals’) were not kept. The Republican Majority in the 111th Congress’ (247-193)) seized on the administration’s miss fueling anti-ACA rhetoric among critics and misinformation.

3-Support for the ACA has grown but its results are mixed. It has survived 7 Supreme Court challenges and more than 70 failed repeal votes in Congress. It enjoys vigorous support in the Biden administration and among the industry’s major trade groups but remains problematic to outsiders who believe it harmful to their interests. For example, under the framework of the ACA, the administration is pushing for larger provider networks in the 18 states and DC that run their own marketplaces, expanded dental and mental health coverage, extended open enrollment for Marketplace coverage and restoration of restrictions on “junk insurance’ but its results to date are mixed: access to insurance coverage has increased. Improvements in quality have been significant as a result of innovations in care coordination and technology-enabled diagnostic accuracy. But costs have soared: between 2010 and 2021, total health spending increased 64% while the U.S. population increased only 7%.

So, as the ACA takes center stage in Campaign 2024, here are 4 things to watch:

1-Media attention to elements of the ACA other than health insurance coverage. My bet: attention from critics will be its unanticipated costs in addition to its federal abortion protections now in the hands of states. The ACA’s embrace of price and quality transparency is of particular interest to media and speculation that industry consolidation was an unintended negative result of the law will energize calls for its replacement. Thus, the law will get more attention. Misinformation and disinformation by special interests about its original intent as a “government takeover of the health system” will be low hanging fruit for antagonists.

2- Changes to the law necessary intended to correct/mitigate its unintended consequences, modernize it to industry best practice standards and responses to court challenges will lend to the law’s complex compliance challenges for each player in the system. New ways of prompting Medicaid expansion, integration of mental health and social determinants with traditional care, the impact of tools like ChatGPT, quantum computing, generative AI not imagined as the law was built, the consequences of private equity investments on prices and spending, and much more.

3-Public confusion. The ACA is a massive law in a massive industry. Cliff’s Notes are accessible but opinions about it are rarely based on a studied view of its intent and structure. It lends itself to soundbites intended to obscure, generalize or misdirect the public’s attention.

4-The ACA price tag. In 2010, the CBO estimated its added cost to health spending at $1.1 trillion (2010-2019) but its latest estimate is at least $3 trillion for its added insurance subsidies alone. The fact is no one knows for sure what its costs are nor the value of the changes it has induced into the health system. The ranks of those with insurance coverage has been cut in half. Hospitals, physicians, post-acute providers, drug manufacturers and insurers are implementing value-based care strategies and price transparency (though reluctantly) but annual health cost increases have consistently exceeded 4% annually as the cumulative impact of medical inflation, utilization, consolidation and price increases are felt.

Final thought:

I have studied the ACA, and the enabling laws, executive orders, administrative and regulatory actions, court rulings and state referenda that have followed its passage. Despite promises to ‘repeal and replace’ by some, it is more likely foundational to bipartisan “fix and repair’ regulatory reforms that focus more attention to systemness, technology-enabled self-care, health and wellbeing and more.

It will be interesting to see how the ACA plays in Campaign 2024 and how moderators for the CNN-hosted debates January 10 in Des Moines and January 21 in New Hampshire address it. In the 2-hour Tuscaloosa debate last Wednesday, it was referenced in response to a question directed to Gov. DeSantis about ‘reforming the system’ 101 minutes into the News Nation broadcast. It’s certain to get more attention going forward and it’s certain to play a more prominent role in the future of the system.

The ACA is back on the radar in U.S. healthcare. Stay tuned.

PS The resignations under pressure of Penn President Elizabeth Magill and Board Chair Scott Bok over inappropriate characterization of Hamas’ genocidal actions toward Jews are not surprising. Her response to Congressional questioning was unfortunate. The eventuality turned in 4 days, sparked by student outrage and adverse media attention that tarnished the reputations of otherwise venerable institutions like Penn, MIT and Harvard.

The lessons for every organization, including the big names in healthcare, are not to be dismissed: Beyond the issues of genocide, our industry is home to a widening number of incendiary issues like Hamas.

They’re increasingly exposed to public smell tests that often lead to more: Workforce strikes. CEO compensation. Fraud and abuse. Tax exemptions and community benefits. Prior authorization and coverage denial. Corporate profit. Patient collection and benevolent use policies. Board independence and competence and many more are ripe for detractors and activist seeking attention.

Public opinion matters. Reputations matter. Boards of Directors are directly accountable for both.

Six individuals and the owners of two small businesses sued the federal government, arguing that the ACA provision “makes it impossible” for them to purchase health insurance for themselves or their employees that excludes free preventive care. The plaintiffs argue that they do not want or need such care. They specifically name the medication PrEP (used to prevent the spread of HIV), contraception, the HPV vaccine, and screening and behavioral counseling for sexually transmitted diseases and substance use; however, they seek to invalidate the entire ACA preventive benefit package.

A federal trial court judge agreed with some of their claims and invalidated free coverage of more than 50 services, including lung, breast, and colon cancer screenings and statins to prevent heart disease.

This ruling, which is currently being appealed, strips free preventive services coverage from more than 150 million privately insured people and approximately 20 million Medicaid beneficiaries who are covered under the ACA’s Medicaid expansion.

This suit was first filed in 2020. The plaintiffs in the case, Braidwood Management v. Becerra, continue to oppose the entire preventive benefit package, which consists of four service bundles: services rated “A” or “B” by the United States Preventive Services Task Force (USPSTF); routine immunizations recommended by the Advisory Committee on Immunization Practices (ACIP); evidence-informed services for children recommended by the Health Resources and Services Administration (HRSA); and evidence-informed women’s health care recommended by HRSA. The trial judge invalidated all benefits recommended by the USPSTF after March 23, 2010, the date the ACA became law. (The court also exempted the plaintiffs on religious grounds from their obligation to cover PrEP.) The Fifth Circuit put the trial court’s decision on temporary hold while the case is on appeal.

The Fifth Circuit, one of the nation’s most conservative appeals courts, will hear the Biden administration’s appeal of the trial court’s USPSTF ruling and the entirety of the plaintiffs’ original challenge, thereby putting all four coverage guarantees in play. The court also will hear whether the ruling should apply only to the plaintiffs or to all Americans.

The trial court held that the USPSTF lacks the legal status necessary under the Constitution to make binding coverage decisions, and that the Secretary of the U.S. Department of Health and Human Services (HHS) — who can make such binding decisions — lacks the power to rectify matters by formally adopting USPSTF recommendations. The judge concluded that federal law fails to require that members be presidential nominees confirmed by the Senate under the Appointments Clause; in the judge’s view, this means that members are not politically accountable for their decisions, which is constitutionally problematic. The judge also ruled that federal law makes the USPSTF the final coverage arbiter, which means that the HHS Secretary, who is nominated and confirmed under the Appointments Clause and thus politically accountable, cannot cure the constitutional problem by ratifying USPSTF recommendations.

On appeal, the Biden administration argues that the USPSTF passes constitutional muster because the HHS Secretary, who oversees the Task Force, is a nominated and confirmed constitutional officer. Alternatively, the administration argues the appeals court should interpret the statute as allowing the HHS Secretary to ratify USPSTF recommendations, since the law specifies that USPSTF members are independent of political pressure only “to the extent practicable.” The administration makes similar arguments on behalf of ACIP and HRSA.

The plaintiffs argue that secretarial ratification cannot cure the constitutional problems with all three advisory bodies. According to the plaintiffs, none of the advisory bodies has the status of constitutional officers demanded by the Appointments Clause, and so their recommendations must remain recommendations only, unenforceable by HHS on insurers, health plans, and state Medicaid programs.

The second issue is the scope of the remedy if the law is found unconstitutional. The trial court did not limit its holding to the four individual plaintiffs and two companies who sued, but instead applied its order nationwide. The Biden administration argues that, if the coverage guarantee is unconstitutional, the court only should prohibit HHS from enforcing the preventive services provision against the plaintiffs who brought the lawsuit and should allow the coverage guarantee to remain in force for the rest of the country. Citing an amicus brief filed by the American Public Health Association and public health deans and scholars, the administration argues that barring HHS from enforcing the preventive services requirement nationwide “pose[s] a grave threat to the public health” by decreasing Americans’ access to lifesaving preventive services. The plaintiffs argue that a nationwide prohibition is necessary, the broader public interest in free preventive coverage is irrelevant, and insurers will voluntarily continue to offer free preventive coverage if people want it.

The administration’s arguments on appeal have attracted amicus briefs by bipartisan economic scholars, organizations concerned with health equity and preventive health, health care organizations, and 23 states.

Crucially, the economists point out that, prior to the ACA, comprehensive free preventive coverage was extremely limited because it is not in insurers’ interest to make a long-term economic investment in members’ health. Indeed, prior to the ACA, insurers did not even uniformly cover the basic screenings for newborns to detect treatable illnesses and conditions.

Amicus briefs supporting the plaintiffs have been filed by Texas and an organization dedicated to “protecting individual liberties . . . against government overreach.” All briefing will be complete by November 3, 2023, with oral argument thereafter. A decision is likely in early to mid-2024. Whatever the outcome, expect a Supreme Court appeal given the size of the stakes in the case.

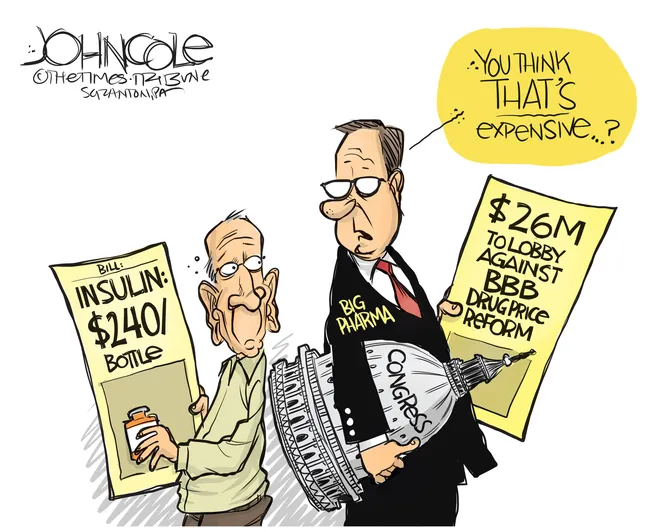

Last Tuesday, the Center for Medicare and Medicaid Services (CMS) announced the first 10 medicines that will be subject to price negotiations with Medicare starting in 2026 per authorization in the Inflation Reduction Act (2022). It’s a big deal but far from a done deal.

Here are the 10:

Eliquis, for preventing strokes and blood clots, from Bristol Myers Squibb and Pfizer

Jardiance, for Type 2 diabetes and heart failure, from Boehringer Ingelheim and Eli Lilly

Xarelto, for preventing strokes and blood clots, from Johnson & Johnson

Januvia, for Type 2 diabetes, from Merck

Farxiga, for chronic kidney disease, from AstraZeneca

Entresto, for heart failure, from Novartis

Enbrel, for arthritis and other autoimmune conditions, from Amgen

Imbruvica, for blood cancers, from AbbVie and Johnson & Johnson

Stelara, for Crohn’s disease, from Johnson & Johnson

Fiasp and NovoLog insulin products, for diabetes, from Novo Nordisk

Notably, they include products from 10 of the biggest drug manufacturers that operate in the U.S. including 4 headquartered here (Johnson and Johnson, Merck, Lilly, Amgen) and the list covers a wide range of medical conditions that benefit from daily medications.

But only one cancer medicine was included (Johnson & Johnson and AbbVie’s Imbruvica for lymphoma) leaving cancer drugs alongside therapeutics for weight loss, Crohn’s and others to prepare for listing in 2027 or later.

And CMS included long-acting insulins in the inaugural list naming six products manufactured by the Danish pharmaceutical giant Novo Nordisk while leaving the competing products made by J&J and others off. So, there were surprises.

To date, 8 lawsuits have been filed against the U.S. Department of Health and Human Services by drug manufacturers and the likelihood litigation will end up in the Supreme Court is high.

These cases are being brought because drug manufacturers believe government-imposed price controls are illegal. The arguments will be closely watched because they hit at a more fundamental question:

what’s the role of the federal government in making healthcare in the U.S. more affordable to more people?

Every major sector in healthcare– hospitals, health insurers, medical device manufacturers, physician organizations, information technology companies, consultancies, advisors et al may be impacted as the $4.6 trillion industry is scrutinized more closely . All depend on its regulatory complexity to keep prices high, outsiders out and growth predictable. The pharmaceutical industry just happens to be its most visible.

The Pharmaceutical Industry

The facts are these:

66% of American’s take one or more prescriptions: There were 4.73 billion prescriptions dispensed in the U.S. in 2022

Americans spent $633.5 billion on their medicines in 2022 and will spend $605-$635 billion in 2025.

This year (2023), the U.S. pharmaceutical market will account for 43.7% of the global pharmaceutical market and more than 70% of the industry’s profits.

41% of Americans say they have a fair amount or a great deal of trust in pharmaceutical companies to look out for their best interests and 83% favor allowing Medicare to negotiate pricing directly with drug manufacturers (the same as Veteran’s Health does).

There were 1,106 COVID-19 vaccines and drugs in development as of March 18, 2023.

The U.S. industry employs 811,000 directly and 3.2 million indirectly including the 325,000 pharmacists who earn an average of $129,000/year and 447,000 pharm techs who earn $38,000.

And, in the U.S., drug companies spent $100 billion last year for R&D.

It’s a big, high-profile industry that claims 7 of the Top 10 highest paid CEOs in healthcare in its ranks, a persistent presence in social media and paid advertising for its brands and inexplicably strong influence in politics and physician treatment decisions.

The industry is not well liked by consumers, regulators and trading partners but uses every legal lever including patents, couponing, PBM distortion, pay-to-delay tactics, biosimilar roadblocks et al to protect its shareholders’ interests. And it has been effective for its members and advisors.

My take:

It’s easy to pile-on to criticism of the industry’s opaque pricing, lack of operational transparency, inadequate capture of drug efficacy and effectiveness data and impotent punishment against its bad actors and their enablers.

It’s clear U.S. pharma consumers fund the majority of the global industry’s profits while the rest of the world benefits.

And it’s obvious U.S. consumers think it appropriate for the federal government to step in. The tricky part is not just government-imposed price controls for a handful of drugs; it’s how far the federal government should play in other sectors prone to neglect of affordability and equitable access.

There will be lessons learned as this Inflation Reduction Act program is enacted alongside others in the bill– insulin price caps at $35/month per covered prescription, access to adult vaccines without cost-sharing, a yearly cap ($2,000 in 2025) on out-of-pocket prescription drug costs in Medicare and expansion of the low-income subsidy program under Medicare Part D to 150% of the federal poverty level starting in 2024. And since implementation of these price caps isn’t until 2026, plenty of time for all parties to negotiate, spin and adapt.

But the bigger impact of this program will be in other sectors where pricing is opaque, the public’s suspicious and valid and reliable data is readily available to challenge widely-accepted but flawed assertions about quality, value, access and outcomes. It’s highly likely hospitals will be next.

A federal drug discount program for safety-net providers that’s been a perennial source of fierce disputes among health care industry powerhouses is back in the spotlight, with billions of dollars at stake.

The big picture:

Separate but coinciding issues are generating renewed focus on the decades-old 340B program, which requires that drugmakers give large discounts on outpatient drugs to health care providers serving low-income patients.

A Biden administration proposal to issue hefty back payments due to 340B providers, drugmakers’ efforts to limit discounts, and rebooted congressional interest in broader reforms are again igniting debate about the program’s scope.

Context:

The Supreme Court last year unanimously sided with hospitals who challenged a nearly 30% reduction to their 340B payments by the Centers for Medicare and Medicaid Services that began under the Trump administration.

In response to the court decision, CMS last month announced a $9 billion plan to repay 340B providers that’s generated some controversy. While 340Bhospitals are happy they’re getting paid back, industry groups are upset that the payments are funded by clawing back money to other hospitals.

Meanwhile, the Biden administration is battling drugmakers in court over restrictions they’ve placed on where hospitals can use their 340B discounts.

A bipartisan group of senators this summer also released a request for information on how to improve stability and oversight within the program.

Hospitals could face further cutbacks if Congress or the courts place new limits on 340B.

Flashback:

The 340B program began in 1992 to help providers serving patient populations who struggled to afford their prescription drugs. It allowshospitals and other safety-net providers like community health clinics to save an average of 25% to 50% on drug purchases, according to the federal government.

When hospitals partner with off-site pharmacies to dispense drugs, the pharmacies also benefit financially from 340B savings.

The program has grown significantly since its inception, increasing from 8,100 participating safety-net providers in 2000 to 50,000 in 2020.

Between the lines:

The expansive program growth has drawn lawmakers’ scrutiny and complaints from pharmaceutical companies, who accuse providers of using the program to pad their profits rather than help vulnerable patients. Providers dispute those accusationsand say the program helps them stretch limited federal resources.

More than 20 drug companies have placed restrictions on when providers can use 340B discounts at off-site pharmacies. Drug companies say the limits help prevent them from having to give duplicate discounts, which occurswhen both the provider and state Medicaid agency receive a discount on the same drug.

The Biden administration asked several drugmakers to lift their 340B restrictions and threatened fines if they don’t comply.

Several drugmakers have sued the administration, arguing federal officials didn’t have the right to stop them from limiting discounts. One appellate judge ruled in favor of drugmakers earlier this year, and two other cases are pending in federal appellate courts.Experts say the cases could go all the way to the Supreme Court.

As the legal fight plays out, 340B providers are urging Congress to approve new measures to prevent drugmakers from restricting access to discounts.

The other side: Drugmakers, meanwhile, want lawmakers to tightenhospital eligibility standards and place stronger limits on how 340B pharmacies can profit from the program.

Of note: Rural hospitals, some of which were spared from the 340B cuts made years ago, are especially concerned about the hit they would takefrom CMS’ proposed funding clawbacks.

Rural facilities today rely heavilyon 340B to offset other financial losses, Brock Slabach, chief operations officer at the National Rural Health Association, told Axios.

“You can’t get out of this problem without harming those who were helped,” Slabach said.

What we’re watching: Expect to keep hearing about 340B in the coming months.

CMS still needs to finalize the 340B repayment planafter the public comment ends Sept. 5.

The D.C. Circuit Court of Appeals and the 7th Circuit Court of Appeals will issue rulings on whether the Biden administration can reverse drugmakers’340B restrictions.

Congress could take up a serious reform effort following the Senate’s information request, though that would take time.

Last week Johnson & Johnson followed Merck, Bristol Myers Squibb, and Astellas Pharma by filing a lawsuit against the Biden administration in federal court over the Medicare Drug Price Negotiation Program, established through the 2022 Inflation Reduction Act. PhRMA, the industry trade group, and the US Chamber of Commerce have also filed suits.

The lawsuits claim that the program violates the First and Fifth Amendments by compelling speech, and taking private property for public use without just compensation. The US Chamber of Commerce also filed a motion earlier this month requesting a preliminary injunction.

This flurry of legal activity comes just a month before the Centers for Medicare & Medicaid Services is due to publish its list of the first ten drugs selected for negotiations. The makers of those drugs will then have a month to decide if they will participate in negotiations, risking significant financial penalties if they do not. Any negotiated prices would take effect in 2026.

The Gist:Theability for Medicare to negotiate drug prices is a key pillar of the Biden administration’s healthcare agenda, one the President plans to tout in his upcoming reelection campaign. But the pharmaceutical industry’s legal challenges—multiple, separate suits in different federal courts nationwide—are destined for the Supreme Court if these cases generate conflicting rulings, which is likely. A protracted legal fight will delay or potentially alter the program before it is fully implemented.