On Monday, Fitch Ratings, the New York City-based credit rating agency, released a report predicting that the US not-for-profit hospital sector will see average operating margins reset in the one-to-two percent range, rather than returning to historical levels of above three percent.

Following disruptions from the pandemic that saw utilization drop and operating costs rise, hospitals have seen a slower-than-expected recovery.

But, according to Fitch, these rebased margins are unlikely to lead to widespread credit downgrades as most hospitals still carry robust balance sheets and have curtailed capital spending in response.

The Gist:As labor costs stabilize and volumes return, the median hospital has been able to maintain a positive operating margin for the past ten months.

But nonprofit hospitals are in a transitory period, one with both continued challenges—including labor costs that rebased at a higher rate and ongoing capital restraints—and opportunities—including the increase in outpatient demand, which has driven hospital outpatient revenue up over 40 percent from 2020 levels.

While the future margin outlook for individual hospitals will depend on factors that vary greatly across markets, organizations that thrive in this new era will be the ones willing to pivot, take risks, and invest heavily in outpatient services.

The physician-led healthcare network formed to save hospitals from financial distress. Now, hospitals in its own portfolio need bailing out after years of alleged mismanagement.

Steward Health Care formed over a decade ago when a private equity firm and a CEO looking to disrupt a regional healthcare environment teamed up to save six Boston-based hospitals from the brink of financial collapse. Since that time, Steward has expanded from a handful of facilities to become the largest physician-led for-profit healthcare network in the country, operating 33 community hospitals in eight states, according to its own corporate site.

However, Steward has also found itself once again on the precipice of failure.

Steward’s ongoing issues in Massachusetts have played out in regional media outlets in recent weeks. Massachusetts Gov. Maura Healey warned there would be no bailout for Steward in an interview on WBUR’s Radio Boston.

The Massachusetts Department of Public Health said it is investigating concerns raised about Steward facilities and began conducting daily site inspections at some Steward sites to ensure patient safety beginning Jan. 31.

However, the tide may have begun to change. Steward executives said on Feb. 2 they had secured a deal to stabilize operations and keep Massachusetts hospitals open — for now. Steward will receive bridge financing under the deal and consider transferring ownership of one or more hospitals to other companies, a Steward spokesperson confirmed to Healthcare Dive on Feb. 7.

While politicians welcomed the news, some say Steward’s long term outlook in the state is uncertain. Other politicians sought answers for how a prominent system could seemingly implode overnight.

“I am cautiously optimistic at this point that [Steward] will be able to remain open, because it’s really critical they do,” said Brockton City Councilor Phil Griffin. “But they owe a lot of people a lot of money, so we’ll see.”

However, the business model wasn’t immediately a financial success. Steward didn’t turn a profit between 2011 and 2014, according to a 2015 monitoring report from the Massachusetts attorney general. Instead, Steward’s debt increased from $326 million in 2011 to $413 million at the end of the 2014 fiscal year, while total liabilities ballooned to $1.4 billion in the same period as Steward engaged in real estate sale and leaseback plays.

Under the 2010 deal, Steward agreed to assume Caritas’ debt and carry out $400 million in capital expenditures over four years to upgrade the hospitals’ infrastructure. However, that capital expenditure could come in part from financial engineering, such as monetizing Steward’s own assets, according to Zirui Song, associate professor of health care policy and medicine at the Harvard Medical School who has studied private equity’s impact on healthcare since 2019.

Cerberus did not contribute equity into Steward after making its initial investment of $245.9 million, according to the December 2015 monitoring report. Meanwhile, according to reporting at the time, de la Torre wanted to expand Steward. Steward was on its own to raise funds.

Such deals are typically short-sighted, Song explained. When hospitals sell their property, they voluntarily forfeit their most valuable assets and tend to be saddled with high rent payments.

Healthcare Dive spoke with four workers across Steward’s portfolio who said Steward’s emphasis on the bottom line negatively impacted the company’s operations for years.

Terra Ciurro worked in the emergency department at Steward Health Care-owned Odessa Regional Medical Center in January 2022 as a travel nurse. She recalled researching Steward and being attracted to the fact the company was physician owned.

“I remember thinking, ‘That’s all I need to know. Surely, doctors will have their heart in the right place,’” Ciurro said. “But yeah — that’s not the experience I had at all.”

The emergency department was “shabby, rundown and ill-equipped,” and management didn’t fix broken equipment that could have been hazardous, she said. Nine weeks into her 13-week contract and three hours before Ciurro was scheduled to work, Ciurro said her staffing agency called to cut her contract unceremoniously short. Steward hadn’t paid its bills in six months, and the agency was pulling its nurses, she said she was told.

In Massachusetts, Katie Murphy, president of the Massachusetts Nurses Association, which represents more than 3,000 registered nurses and healthcare professionals who work in eight Steward hospitals, said there were “signals” that Steward facilities had been on the brink of collapse for “well over a year.”

Steward hospitals are often “significantly” short staffed and lack supplies from the basics, like dressings, to advanced operating room equipment, said Murphy. While most hospitals in the region got a handle on staffing and supply shortages in the aftermath of the COVID pandemic, at Steward hospitals shortages “continued to accelerate,” Murphy said.

A review of Steward’s finances by BDO USA, a tax and advisory firm contracted last summer by the health system itself to demonstrate it was solvent enough to construct a new hospital in Massachusetts, showed Steward had a liquidity problem. The health system had few reserves on hand last year to pay down its debts owed to vendors, possibly contributing to the shortages. The operator carried only 10.2 days of cash on hand in 2023. In comparison, most healthy nonprofit hospital systems carried 150 days of cash on hand or more in 2022, according to KFF.

One former finance employee, who worked for Steward beginning around 2018, said that the books were routinely left unbalanced during her tenure. Each month, she made a list of outstanding bills to determine who must be paid and who “we can get away with holding off” and paying later.

Food, pharmaceuticals and staff were always paid, while all other vendors were placed on an “escalation list,” she said. Her team prioritized paying vendors that had placed Steward on a credit hold.

The worker permanently soured on Steward when she said operating room staff had to “make do” without a piece of a crash cart — which is used in the event of a heart attack, stroke or trauma.

She stopped referring friends to Steward facilities, telling them “Don’t go — if you can go anywhere else, don’t go [to Steward], because there’s no telling if they’ll have the supplies needed to treat you.”

Away from regulatory review

Massachusetts officials maintain that it hasn’t been easy to see what was happening inside Steward.

Steward is legally required to submit financial data to the MA Center for Health Information and Analysis (CHIA) and to the Massachusetts Registration of Provider Organizations Program (MA-RPO Program), according to a spokesperson from the Health Policy Commission, which analyzes the reported data. Under the latter requirement, Steward is supposed to provide “a comprehensive financial statement, including information on parent entities and corporate affiliates as applicable.”

However, Steward fought the requirements. During Stuart Altman’s tenure as the chair of the Commission from 2012 to 2022, Altman told Healthcare Dive that the for-profit never submitted documents, despite CHIA levying fines against Steward for non-compliance. Steward even sued CHIA and HPC for relief against the reporting obligations.

Steward is currently appealing a superior court decision and order from June 2023 that required it to comply with the financial reporting requirements and produce audited financial reports that cover the full health system, Mickey O’Neill, communications director for the HPC told Healthcare Dive. As of Feb. 6, Steward’s non-compliance remained ongoing, O’Neill said.

Without direct insight into Steward’s finances, the state was operating at a disadvantage, said John McDonough, professor of the practice of public health at The Harvard T.H. Chan School of Public Health. He added that some regulators saw a crisis coming generally, “but the timing was hard to predict.”

Altman gives his team even more of a pass for not spotting the Steward problem.

“There was no indication while I was there that Steward was in deep trouble,” Altman said. Although Steward was the only hospital system that failed to report financial data to the HPC, that alone had not raised red flags for him. “[CEO] Ralph [de la Torre] was just a very contrarian guy. He didn’t do a lot of things.”

Song and his co-author, Sneha Kannan, a clinical research fellow at Harvard Medical School, are hopeful that in the future, regulatory agencies can make better use of the data they collect annually to track changes in healthcare performance over time. They can potentially identify problem operators before they become crises.

“State legislators, even national legislators, are not in the habit of comparing hospitals’ performances on [quality] measures to themselves over time — they compare to hospitals’ regional partners,” Kannan said. “Legislators, Medicare, [and] CMS has access to that information.”

However, although there’s interest from regulators in scrutinizing healthcare quality more closely — particularly when private equity gets involved — a streamlined approach to analyzing such data is still a “ways off,” according to the pair. For now, all parties interviewed for this piece agreed that the best way to avoid being caught off guard by a failing system was to know how such implosions could occur.

“If there’s a lesson from [Steward],” McDonough ventured, “it is that the entire state health system and state government need to be much more wary of all for-profits.”

Creating a great rating agency presentation is imperative to telling your story. I’ve probably seen a thousand presentations across the past three decades and I can say without a doubt that a great presentation will find its way into the rating committee. Show me a crisp, detailed, well-organized presentation, and I’ll show you a ratings analyst who walks away with high confidence that the management team can navigate the industry challenges ahead.

During the pandemic, Kaufman Hall recommended that hospitals move financial performance to the top of the presentation agenda. Better presentations chronicled the immediate, “line item by line item” steps management was taking to stop the financial bleeding and access liquidity. We still recommend this level of detail in your presentations, but as many hospitals relocate their bottom line, management teams are now returning to discussing longer-term strategy and financial performance in their presentations.

Beyond the facts and figures, many hospitals ask me what the rating analysts REALLY want to know. Over those one thousand presentations I’ve seen, the presentations that stood out the most addressed the three themes below:

What makes your organization essential? Hospitals maintain limited price elasticity as Medicare and Medicaid typically comprise at least half of patient service revenue, leaving only a small commercial slice to subsidize operations. The ability to negotiate meaningful rate increases with payers will largely rest on the ability to prove why the hospital is a “must-have” in the network. In other words, a health plan that can’t sell a product without a hospital in its network is the definition of essential. This conversation now also includes Medicare Advantage plans as penetration rates increase rapidly across the country. Essentiality may be demonstrated by distinct services, strong clinical outcomes and robust medical staff, multiple access points across a certain geography, or data that show the hospital is a low-cost alternative compared to other providers. Volume trends, revenue growth, and market share show that essentiality. A discussion on essentiality is particularly needed for independent providers who operate in crowded markets.

What makes your financial performance durable? Many hospitals are showing a return to better performance in recent quarters. Showing how your organization will sustain better financial results is important. Analysts will want to know what the new “run rate” is and why it is durable. What are the undergirding factors that make the better margins sustainable? Drivers may include negotiated rate increases from commercial payers and revenue cycle improvements. On the expense side, a well-chronicled plan to achieve operating efficiencies should receive material airtime in the presentation, particularly regarding labor. It is universally understood that high labor costs are a permanent, structural challenge for hospitals, so any effort to bend the labor cost curve will be well received. Management should also isolate non-recurring revenue or expenses that may drive results, such as FEMA funds or 340B settlements. To that end, many states have established new direct-to-provider payment programs which may be meaningful for hospitals. Expect questions on whether these funds are subject to annual approval by the state or CMS. The analysts will take a sharpened pencil to a growing reliance on these funds.

The durability of financial performance should be represented with highly detailed multi-year projections complete with computed margin, debt, and liquidity ratios. Know that analysts will create their own conservative projections if these are not provided, which effectively limits your voice in the rating committee.

We also recommend that hospitals include a catalogue of MTI and bank covenants in the presentation. Complying with covenants are part of the agreement that hospitals make with their lenders, and it is the organization’s responsibility to report how it’s performing against these covenants. General philosophy on headroom to covenants also provides insight to management’s operating philosophy. For example, is it the organization’s goal to have narrow, adequate, or ample headroom to the covenants and why? As the rating agencies will tell you, ratings are not solely based on covenant performance, but all rating factors influence your ability to comply with the covenants.

What makes your capital plan affordable? Every rating committee will ask what the hospital’s future capital needs are and how those capital needs will be supported by cash flow, also known as “capital capacity.” To answer that question, a hospital must understand what it can afford, based on financial projections. Funding sources may require debt, which requires a debt capacity analysis with goals on debt burden, coverage, and liquidity targets. Over the years, better presentations explain the organization’s capital model, outline the funding sources, and discuss management’s tolerance for leverage.

There is always a lot to cover when meeting with the rating agencies and a near endless array of metrics and indicators to provide. As I’ve written before, how you tell the story is as important as the story itself. If you can weave these three themes throughout the presentation, then you will have a greater shot at having your best voice heard in rating committee.

Rating agencies have done a great job in increasing transparency around how ratings are determined. Detailed methodologies, scorecards, and medians are a big part of that effort.

Central to the rating process is the rating committee. All rating decisions are made by a rating committee, not an individual. The rating committee provides a robust discussion of various viewpoints as it deliberates, votes, and assigns ratings to the debt instrument.

Here are five things to know about what happens in a rating committee.

1. Rating committees are presided over by a Rating Committee Chair.

The Chair’s primary responsibility is to check that the committee follows numerous processes that meet company and SEC-mandated guidelines. For example, the Chair must verify that the correct methodology is being used to determine the rating, or if a rating requires additional methodologies (such as short-term rating methodologies on variable rate debt). The Chair must confirm that the rating decision will be based on verifiable facts or assessments (such as an audit) and that voting members are free of conflicts. Committees can be subject to internal and external reviews after the fact to ensure that decisions were made impartially and documented correctly.

The Chair ensures that the committee is populated with voting members who possess in-depth knowledge about the sector or related-credit knowledge (such as a higher education analyst in the case of an academic medical center) and are skilled in credit assessment. Each voting member has one vote and an equal vote. Serving as a voting member of a rating committee or as a Chair is a privilege and must be earned.

2. The rating committee discussion centers around the ability of a borrower to repay its obligations, or said another way, the likelihood of payment default.

As such, debt structure is integral to the rating committee. Detailed information provided in the committee package will include information on outstanding and proposed debt (if a bond financing is imminent), debt structure risks (fixed versus variable, for example), debt service schedule (level payments or with bullets), maturities and call dates, taxable and tax-exempt debt, bank lines and revolvers, counterparty risk and termination events, derivative products such as interest rate swaps and collateral thresholds, senior-subordinate debt structures, bond and bank covenants, obligated group, and security pledge, to name a few. Leases and pension obligations are also considered, particularly when liabilities outsize the direct debt.

Rating committees review hundreds of financial metrics to assess recent financial performance and an organization’s ability to pay debt in the future. Audited financial statements, year-to-date results, and annual budgets and projections are the basis for computing the financial ratios. Non-quantitative factors include success with past strategies and capital projects, market position and essentiality, management, governance and corporate structure, workforce needs, and local economic data. Confidential information provided by the organization is also shared. The job of the lead analyst is to distill all the information and present an organized credit story to the rating committee.

3. Rating consistency is paramount.

An “A” should be an “A” should be an “A.” Comparables (or “comps”) are an important part of the rating committee. Comps may include the other hospitals and health systems operating in the same state given shared Medicaid and state regulations (such as Certificate of Need or state-mandated minimum wage), workforce environment (such as the presence of active unions), and similar economic factors. Like-sized peers in the same rating category also populate comps. The type of hospital being evaluated is also important. For example, health systems that own health plans would be compared to other integrated delivery systems; likewise for children’s hospitals, academic medical centers, or subacute care providers. Medians are also a part of the comps and provide relativity to like-rated borrowers by highlighting outliers.

4. Rating committee spends time reviewing the draft report to make sure the committee’s views are accurately expressed and check that confidential information was not inadvertently revealed. If you want to know what was discussed in the rating committee, read the last rating report.

Over the years, many executives have asked to speak directly to the rating committee. While that is not possible, you can bring your voice to the discussion with an informative, well-crafted rating presentation. That brings me to my final “inside rating committee” point.

5. Rating presentations matter.

Effective, informative presentations that encapsulate your organization’s strengths will be shared with the rating committee. Every slide in your presentation should send a clear message that the organization’s ability to repay the debt and exceed covenants is strong. Emphasize the positives, acknowledge the challenges, and share what your action plan is to address them. Do your homework and review what you shared with the analysts last year; they will be doing the same to prepare. Provide updates on how the strategic plans are going. If you exceeded your financial goals, explain how. If you fell short, explain why.

How you tell the story is as important as the story itself. That’s how you can inform the discussion and ensure your voice is heard around the rating committee table.

Inflation, labor pressures, and general economic uncertainty have created significant financial strain for hospitals in the wake of the COVID pandemic. Compressed operating margins and weakened liquidity have left many hospitals in a precarious economic situation, with some entities deciding to delay or even cancel planned capital expenditures or capital raising. Given these tumultuous times, hospital entities could look to the realm of the higher education sector for a playbook on how to leverage non-core assets to unlock significant unrealized value and strengthen financial positions, in the form of public-private partnerships.

These structures, also known as P3s, involve collaborative agreements between public entities, like hospitals, and private sector partners who possess the expertise to unlock the value of non-core assets. A special purpose vehicle (SPV) is created, with the sole purpose of delivering the responsibilities outlined under the project agreement. The SPV is typically owned by equity members. The private sector would be responsible for raising debt to finance the project, which is secured by the obligations of the project agreement (and would be non-recourse to the hospital). Of note, the SPV undergoes the rating process, not the hospital entity. Even more importantly, the hospital retains ownership of the asset while benefiting from the expertise and resources of the private sector.

Hospitals can utilize P3s to capitalize on already-built assets, in what is known as a “brownfield” structure. A brownfield structure would typically result in an upfront payment to the hospital in exchange for the right of a private entity to operate the asset for an agreed-upon term. These upfront payments can range from tens of millions to hundreds of millions of dollars.

Alternatively, hospitals can engage in “greenfield” structures where the underlying asset is either not yet built or needs significant capital investment. Greenfield structures typically do not result in an upfront payment to the hospital entity. Instead, (in the example of a new build) private partners would typically design, build, finance, operate and maintain the asset. The hospital still retains ownership of the underlying asset at the completion of the agreed upon term.

P3 structures can be individually tailored to suit the unique needs of the hospital entity, and the resulting benefits are multifaceted. Financially, hospitals can increase liquidity, lower operating expenses, increase debt capacity, and create headroom for financial covenants. These partnerships provide a means to raise funds without directly accessing the capital markets or undergoing the rating process. Upfront payments represent unrestricted funds and can be used as the hospital entity sees fit to further its core mission. Operationally, infrastructure P3s offer hospitals the opportunity to address deferred maintenance needs, which may have accumulated over time. Immediate capital expenditure on infrastructure facilities can enhance reliability and efficiency and contribute to meeting carbon reduction or sustainability goals. Furthermore, these structures provide a means for the hospital to transfer a meaningful amount of risk to private partners via operation and maintenance agreements.

For years, various colleges and universities have adopted the P3 model, which is emerging as a viable solution for hospitals as well. Examples of recent structures in the higher education sector include:

Fresno State University, which partnered with Meridiam (an infrastructure private equity fund) and Noresco (a design builder) to deliver a new central utility plant. The 30-year agreement involved long-term routine and major maintenance obligations from the operator, with provisions for key performance indicators and performance deductions inserted to protect the university. Fresno State is not required to begin making availability payments until construction is completed.

The Ohio State University, which secured a $483 million upfront payment in exchange for the right of a private party to operate and maintain its parking infrastructure. The university used the influx of capital to hire key faculty members and to invest in their endowment.

The University of Toledo, which received an approximately $60 million upfront payment in exchange for a 35-year lease and concession agreement to a private operator. The private team will be responsible for operating and maintaining the university’s parking facilities throughout the term of the agreement.

Ultimately, healthcare entities can learn from the successful implementation of infrastructure P3 structures in the higher education sector. The experiences of Fresno State, The Ohio State University, and the University of Toledo (among others) serve as compelling examples of the transformative potential of P3s in the healthcare sector. By unlocking the true value of non-core assets through partnerships with the private sector, hospitals can reinforce their financial stability, meet sustainability goals, reduce risk, and shift valuable focus back to the core mission of providing high-quality healthcare services.

Author’s note: Implementing P3 structures requires careful consideration and expert guidance. Given the complex nature of these partnerships, hospitals can greatly benefit from the support of experienced advisors to navigate the intricacies of the process. KeyBank and Cain Brothers specialize in guiding entities through P3 initiatives, providing valuable expertise and insight. For additional information, please refer to a recording of our recent webinar and associated summary, which can be accessed here: https://www.key.com/businesses-institutions/business-expertise/articles/public-private-partnerships-can-unlock-hospitals-hiddenvalue.html

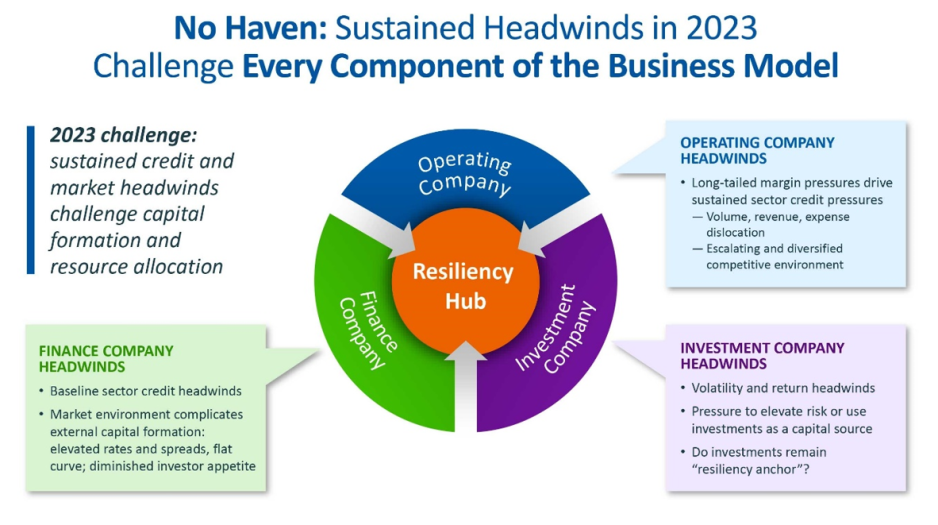

For the first time in recent history, we saw all three functions of the not-for-profit healthcare system’s financial structure suffer significant and sustained dislocation over the course of the year 2022 (Figure above).

The headwinds disrupting these functions are carrying over into 2023, and it is uncertain how long they will continue to erode the operating and financial performance of not-for-profit hospitals and health systems.

The Operating Function is challenged by elevated expenses, uncertain recovery of service volumes, and an escalating and diversified competitive environment.

The Finance Function is challenged by a more difficult credit environment (all three rating agencies

now have a negative perspective on the not-forprofit healthcare sector), rising rates for debt, and a diminished investor appetite for new healthcare debt issuance. Total healthcare debt issuance in 2022 was $28 billion, down sharply from a trailing two-year average of $46 billion.

The Investment Function is challenged by volatility and heightened risk in markets concerned with the Federal Reserve’s tightening of monetary policy and the prospect of a recession. The S&P 500—a major stock index—was down almost 20% in 2022. Investments had served as a “resiliency anchor” during the first two years of the pandemic; their ability to continue to serve that function is now in question.

A significant factor in Operating Function challenges is labor: both increases in the cost of labor and staffing shortages that are forcing many organizations to run at less than full capacity. In Kaufman Hall’s 2022 State of Healthcare Performance Improvement Survey, for example, 67% of respondents had seen year-over-year increases of more than 10% for clinical staff wages, and 66% reported that they had run their facilities at less-than-full capacity because of staffing shortages.

These are long-term challenges,

dependent in part on increasing the pipeline of new talent entering healthcare professions, and they will not be quickly resolved. Recovery of returns from the Investment Function is similarly uncertain. Ideally, not-for-profit health systems can maintain a one-way flow of funds into the Investment Function, continuing to build the basis that generates returns. Organizations must now contemplate flows in the other direction to access

funds needed to cover operating losses, which in many cases would involve selling invested assets at a loss in a down market and reducing the basis available to generate returns when markets recover.

The current situation demonstrates why financial reserves are so important:

many not-for-profit hospitals and health systems will have to rely on them to cover losses until they can reach a point where operations and markets have stabilized, or they have been able to adjust their business to a new, lower margin environment. As noted above, relief funding and the MAAP program helped bolster financial reserves after the initial shock of the pandemic. As the impact of relief funding wanes and organizations repay remaining balances under the MAAP program, Days Cash on Hand has begun to shrink, and the need to cover operating losses is hastening this decline. From its highest

point in 2021, Days Cash on Hand had decreased, as of September 2022, by:

29% at the 75th percentile, declining from 302 to 216 DCOH (a drop of 86 days)

28% at the 50th percentile, declining from 202 to 147 DCOH (a drop of 55 days)

49% at the 25th percentile, declining from 67 to 34 DCOH (a drop of 33 days)

Financial reserves are playing the role for which they were intended; the only question is whether enough not-for-profit hospitals and health systems have built sufficient reserves to carry them through what is likely to be a protracted period of recovery from the pandemic.

KEY TAKEAWAYS

All three functions of the not-for-profit healthcare system’s financial structure—operations, finance, and investments—suffered significant and sustained dislocation over the course of 2022.

These headwinds will continue to challenge not-forprofit

hospitals and health systems well into 2023.

Days Cash on Hand is showing a steady decline, as the impact of relief funding recedes and the need to cover operating losses persists.

Financial reserves are playing a critical role in covering operating losses as hospitals and health systems struggle to stabilize their operational and financial performance.

Conclusion

Not-for-profit hospitals and health systems serve many community needs. They provide patients access to healthcare when and where they need it. They invest in new technologies and treatments that offer patients and their families lifesaving advances in care. They offer career opportunities to a broad range of highly skilled professionals, supporting the economic health of the communities they serve.

These services and investments are expensive and cannot be covered solely by the revenue received from providing care to patients.

Strong financial reserves are the foundation of good financial stewardship for not-for-profit hospitals and health systems.

Financial reserves help fund needed investments in facilities and technology, improve an organization’s debt capacity, enable better access to capital at more affordable interest rates, and provide a critical resource to meet expenses when organizations need to bridge periods of operational disruption or financial distress. Many hospitals and health systems today are relying on the strength of their reserves to navigate a difficult

environment; without these reserves, they would not be able to meet their expenses and would be at risk of closure.

Financial reserves, in other words, are serving the very purpose for which they are intended—ensuring that hospitals and health systems can continue to serve their communities in the face of challenging operational and financial headwinds.

When these headwinds have subsided, rebuilding these reserves should be a top priority to ensure that our not-for-profit hospitals and health systems can remain a vital resource for the communities they serve.

For large capital projects—construction of a new cancer treatment center, for example, or replacement of an aging facility—issuance of municipal debt is one of the most affordable ways for not-for-profit hospitals and health system to finance the project.

The affordability of that debt is, however, partly contingent on the organization’s ability to maintain a strong credit rating, and financial reserves—again measured as Days Cash on Hand—are a significant component of that credit rating.

There are two basic forms of municipal debt:

General obligation bonds are backed by the full taxing power of the issuing municipal authority and are considered relatively low risk. Hospitals that are owned by a city or county can be funded by general obligation bonds, although there are practical limitations on their ability to issue these bonds, including in many instances the need to obtain voter or county commissioner approval. Organizations

without municipal ownership—including most not-for-profit hospitals and health systems— cannot issue general obligation bonds.

Revenue-backed municipal bonds are backed by the ability of the organization borrowing the debt to meet its obligation to make principal and interest payments through the revenue it generates over the life of the bond. Because revenues can be disrupted by any range of factors, revenue-backed bonds are higher risk for investors. Most healthcare bonds are revenue-backed municipal bonds.

When determining whether to invest in revenue-backed municipal healthcare bonds, investors will look to the credit rating of the hospital or health system that is borrowing the debt. Credit ratings—issued by one or more of the three major credit rating agencies (Fitch Ratings, Moody’s Investors Service, and S&P Global Ratings)—provide an assessment of the probability

that the hospital or health system will be able to meet the terms of the debt obligation. These ratings are tiered. A credit rating in the AA tier is better than a credit rating in the A tier, which is better than a rating in the BBB tier. Ratings below the BBB tier are considered sub-investment grade.

Organizations with a sub-investment grade rating can still access various forms of debt, but the amount of debt they can access generally will be lower, the cost of the debt will be higher, and the covenants that lenders require will be more stringent than for investment-grade rated organizations.

Financial reserves and credit ratings

Days Cash on Hand is one of the most important factors credit rating agencies use because it is an indicator of how long the rated organization could withstand serious disruption to its operations and cashflow. The rating agencies issue median values for the various metrics they use to determine credit ratings. Median

values for Days Cash on Hand increased significantly across most rating categories for all three agencies in 2020 and 2021; this reflects the temporary inflow of pandemic relief funding through, for example, the Coronavirus Aid, Relief, and Economic Security (CARES) Act.

We anticipate these medians will move closer to pre-pandemic levels as relief funds are exhausted and hospitals repay remaining balances on Medicare’s COVID-19 Accelerated and Advanced Payment (MAAP) program funds. But even before the pandemic, organizations in 2019 had a median Days Cash on Hand of 276 to 289 days at the AA level, 173 to 219 days at the A level, and 140 to 163 days at the BBB level.

In other words, the Days Cash on Hand benchmark for organizations seeking to maintain an investment-grade rating would be well over 100 Days Cash on Hand, and well over 200 Days Cash on Hand for organizations seeking to achieve a higher rating level. Again, these reserves are proportionate to the operating expenses of the individual hospital or health system.

Impact of credit ratings on access to capital

Organizations that can achieve a higher rating can also borrow money at more affordable interest rates. Figure 3 shows average interest rates for municipal bonds across a range of maturities as of mid-December 2022 (maturity is the term in years for repayment of the bond at the time the bond is issued). Lower-risk general obligation municipal bonds are shown as the baseline, with lines for AA, A, and BBB rated healthcare revenue-backed bonds above it. As a reminder, most hospitals and health systems cannot borrow money using general obligation bonds; instead, they use higher-risk revenue-backed bonds. Because revenue-backed bonds are a higher risk for investors than tax-based general obligation bonds,

even hospitals and health systems with a strong AA credit rating will pay a higher interest rate than would a city or county that could back repayment of the bond with tax revenues (see the line for AA rated Healthcare Revenue Bonds compared to the line for AAA rated General Obligation bonds). But there is also a significant gap between the interest rate a hospital with an AA credit rating would pay compared to the interest rate available to a hospital with a lower BBB rating. Here, the difference is approximately three-fourths of a full percentage point. When the amount borrowed for a major new hospital project can run into the hundreds of millions of dollars, that difference represents significant savings for organizations with a higher credit rating.

Financial reserves and debt capacity

Financial reserves and the funds they generate— including investment income—also help define an organization’s debt capacity: essentially, the amount of debt an organization can assume without jeopardizing its current credit rating. There are two key ratios here:

The first is total unrestricted cash and investments to debt. In general, the more favorable that ratio is, the more latitude a hospital or health system has to take on additional debt, especially if the organization is toward the middle to top end of its rating tier.

The second is the debt service coverage ratio, which measures the organization’s ability to make principal and interest payments with funds derived from both operating and non-operating (e.g., investment income) activity. A higher ratio here means the organization has more funds available to service debt.

The ability to assume additional debt is an important safety valve if, for example, an organization needs to mitigate poor financial performance to fund ongoing capital needs or strategic initiatives.

KEY TAKEAWAYS

Not-for-profit hospitals and health systems often borrow debt through revenue-backed municipal bonds, meaning that the debt obligations will be met by the revenue the organization generates over the life of the bond.

Because revenue-backed bonds are higher risk than general obligation bonds backed by a municipality’s taxing authority (revenues can be disrupted), investors seek assurance that an organization will be able to meet its obligations.

Credit ratings offer investors an assessment of an organization’s current and near-term ability to meet these obligations.

Days Cash on Hand is an important metric in assessing the organization’s credit rating, and a higher rating generally requires a higher number of Days Cash on Hand.

A higher credit rating allows organizations to borrow money at more affordable interest rates.

A higher level of financial reserves and investment income in relation to existing debt obligations also increases an organization’s debt capacity, creating an important safety valve if an organization has to borrow money to mitigate poor operating or investment performance.

Moody’s Investors Service has downgraded the ratings on Providence’s revenue bond debt to “A1” from “Aa3.”

“The downgrade to ‘A1’ is driven by the disaffiliation with Hoag Hospital, and the expectation that weaker operating, balance sheet, and debt measures will continue for the time being,” Moody’s said in an April 5 release.

Renton, Wash.-based Providence and Newport Beach, Calif.-based Hoag ended their affiliation Jan. 31. The two organizations cut ties at a time when Providence is facing several challenges, including operating pressures, variable utilization and reliance on temporary labor, Moody’s said.

The “A1” rating and stable outlook also reflect Providence’s strengths, including a large service area, a large revenue base of more than $25 billion and a leading market share in all of its markets.

Moody’s said it expects Providence to continue to grow its operating platform and generate additional revenue growth.