Published last week in the Wall Street Journal, this piece predicts that the era of immense profitability for Medicare Advantage (MA) insurers may be drawing to a close.

MA has experienced rapid growth over the past decade, due both to the pace of Baby Boomers aging into Medicare, and the increasing numbers of beneficiaries choosing MA plans. In 2023, MA surpassed 50 percent of total Medicare enrollment.

Payers readily embraced the MA market because they found they could earn gross margins two to three times higher than from a commercial life.

However, as the rate of enrollment growth begins to slow (the last of the Boomers will turn 65 in 2030), competition between payers increases, and government payments become less generous, the MA business—while still profitable—is poised to become less of a jackpot.

The Gist:While MA has been an outsized driver of profits for insurance companies in recent years,the nation’s two largest MA payers, UnitedHealth Group (UHG) and Humana, have been signaling growing concerns to the market.

UHG announced late last month that its 2024 MA enrollment growth will be less than half of its 2023 rate, and Humana has been engaged in merger talks with Cigna.

As the “gold rush” period ends, MA payers will have to earn their keep by better integrating their various care and data assets, and more carefully managing spending for an aging cohort of seniors with increasingly complex needs, both much harder than riding a demographic wave to easy profits.

Following rumors of a potential merger reported last month by the Wall Street Journal, the paper shared this week that Bloomfield, CT-based Cigna is no longer pursuing an acquisition of Louisville, KY-based Humana.

According to insiders, the $140B merger was scuttled when the two health insurance giants couldn’t agree on price and other terms.

Instead, Cigna announced that it will be focusing on smaller, bolt-on acquisitions, and is reportedly still considering divesting its Medicare Advantage business.

Cigna also announced $10B of stock buybacks to assuage shareholders, who reacted negatively to the rumored deal, dropping the company’s stock price by nearly 10 percent since merger rumors surfaced.

The Gist: While there are several reasons why this deal may have been called off—Wall Street’s adverse reaction, antitrust concerns, leaking of the talks before the parties were ready—this likely isn’t the end of either payer’s pursuit of greater scale, as both stand in UnitedHealth Group’s giant shadow.

Given Cigna and Humana have each had potential mergers with other payers blocked by the courts, and federal antitrust scrutiny is only increasing, we’re wondering if each may be also looking at nontraditional partners (as Humana explored with Walmart in 2018), though the universe of companies with an interest in a vertically-integrated insurance and care business—and deep enough pockets—is small.

The nation’s largest for-profit hospital systems by revenue — HCA Healthcare, Community Health Systems, Tenet Healthcare and Universal Health Services —reported mixed results during the third quarter of 2023, despite announcing strong demand for patient services.

With the exception of HCA, each operator reported lower profits in the third quarter compared with the same period last year. Health systems CHS and HCA reported earnings that fell short of Wall Street expectations for revenue.

Major operators posted declining profits in the third quarter compared to the same period in 2022

Q3 net income in millions, by operator

Health System

Profit

Percent Change YOY

Community Health Systems

$−91

−117%

HCA Healthcare

$1,800

59%

Tenet Healthcare

$101

−23%

Universal Health Services

$167

−9%

Admissions rose across the board compared to the same period last year: Same facility equivalent admissions rose4.1% at HCA , 3.7% at CHS and 0.6% at Tenet,and adjusted admissions at acute hospitals rose 6.8% at UHS.

Although the for-profit operators began cost containment strategies earlier this year — recognizing that rising expenses, including costs of salary and wages, were pressuring hospital profitability post-pandemic — expenses also rose, with growth in salaries and benefit costs once again pressuring most operators’ revenue.

Hospital operators faced new challenges this quarter, executives said, including increased physician staffing fees and what hospital executives characterizedas aggressive behavior from payers.

Hospitals highlight rising physician fees

Rising physician fees were a topic of concern on earnings calls this quarter, with executives reporting fees that were 15% to 40% higher compared with the same period last year.

Third-party staffing firms charge hospitals physician fees, a percentage of physicians’ salaries, on top of the salaries themselves. Physician fees are separate but related to contract labor costs, which plagued hospitals during the COVID-19 pandemic as they attempted to stem staffing shortages.

Hospitals typically contract specialty hospitalist roles — like anesthesiologists, radiologists and emergency department physicians — and incur associated staffing costs.

Physician fees at HCA, the country’s largest hospital chain, grew 20% year over year in the third quarter, according to CFO Bill Rutherford.

Physician fees were up by as much as 40% at UHS — making up 7.6% of totaloperating expenses this quarter and surpassing the company’s initial projections for the year,CEOMarc Miller said during an earnings call. Historically, physician fees accounted for about 6% of UHS’ total expenses.

Likewise, Franklin, Tennessee-based CHS attributed some of its third-quarter losses to “increased rates for outsourced medical specialists,” according to a release on the operator’s earnings.

Tenet CEO Saum Sutaria noted that physician fee expenses were up 15% year over year, but said on an earnings call that the operator had spied rising physician fees during the pandemic, and had begun efforts to contain costs — including restructuring staffing contracts and in-sourcing critical physician services.

As a result, physician fee costs at Tenet had remained “relatively flat” from the second quarter to the third quarter this year, according to the Sutaria.

Physician fee increases may be a delayed consequence of the No Surprises Act, which went into effect in January of last year, experts say.

On an earnings call, UHS CFO Steve Filton said “the industry has largely had to reset itself” in wake of the law. Tenet and CHS executives echoed the sentiment, noting that the law had disrupted staffing firms’ business models and complicated payment processes.

The No Surprises Act prevents patients who unknowingly receive out-of-network care at an in-network facility from being stuck with unexpectedbills. However, the act has had unintended ripple effects, experts say.

Staffing firms and hospitals allege that the arbitration process created to resolve disputes between providers and insurers is unbalanced and incentivizes insurers to withhold reimbursement for care. In an August survey, over half of doctors reported insurers have either ignored decisions made by arbitrators or declined to pay claims in full.

In other cases, a backlog prevents claims from being adjudicated at all. Last year, the CMS found the federal arbitration process had only reached a payment determination in 15% of cases. Federal regulators have been forced to pause and restart the arbitration process multiple times in the wake of federal court decisions challenging arbitration methodology.

Although the act went into effect more than a year ago, many hospitals are just now feeling the strain, saidLoren Adler, associate director at the Brookings Institute’s Schaeffer Initiative on Health Policy.

That’s because most insurers, hospitals and medical groups operate on three-year contracts, according to Adler. Staffing firms, which have struggled since the No Surprises Act was enacted, have passed on costs to hospitals as contracts come up for negotiation and insurers charge firms higher rates.

In the face of rising costs, some hospitals may opt to follow Tenet and CHS and in-source physicians — either to retain contracts with physicians who worked with firms that have folded or because the passing of the No Surprises Act makes outsourcing less attractive.

CHS hired 500 physicians from staffing firm American Physician Partners after the company collapsed in July. CFO Kevin Hammons said on an earnings call that hiring the physicians had saved CHS “approximately $4 million sequentially compared to the subsidy payments previously paid” to the staffing firm.

However, in-sourcing may not be an effective cost containment strategy for all operators. HCA reported it was hemorrhaging money following its first-quarter majority stake purchase of staffing firm Valesco, which brought about 5,000 physicians onto its payroll. HCA CEO Sam Hazen said the system expects to lose $50 million per quarter on the venture through 2024, citing low payments as the primary issue.

Payer problems

Hospital executives also tied quarterly losses to aggressive behavior from insurers during third-quarter earnings calls.

UHS executives said payers were improperly denying high volumes of claims and disrupting payments to its hospitals, with UHS’ Miller characterizing insurers as “increasingly aggressive” during the third quarter. Though insurers had reduced their number of claims audits, denials and patient status changes during the early stages of the pandemic, payers were increasing denials and reviews, according to UHS’ Filton.

Tenet’s Sutaria said that claims denials were “excessive and inappropriate” during a third-quarter earnings call, adding that the hospital system was working to push back on the volume of claims denials.

Their number one strategy is to provide “excellent documentation” to refute denials quickly, Sutaria said.

Still, excessive claims denials can drive up administrative costs for hospitals, according to Matthew Bates, managing director at Kaufman Hall.

“That denial creates a lot more work, because now I have to deal with that bill two, three, four times to get through the denial process,” Bates said. “It starts to rapidly eat into the operating margins… [becoming] both a cashflow problem and an administrative costs burden.”

Executives across the four for-profit operators said they planned to negotiate with insurers to receive more favorable rates and limit the number of denials in subsequent quarters.

HCA’s Hazen said that it was important for HCA to maintain its in-network status with insurers “to avoid the surprise billing and that [independent dispute resolution] process,” but that it would work with its payers to get “reasonable rates” going forward.

Claim denials are increasing, especially in Medicare Advantage, and it’s affecting hospital’s revenue cycles and patient care.

“We definitely are seeing an increase in denials,” said Sherri Liebl, executive director of Revenue Cycle, CentraCare Health, a large multispecialty system in Minnesota. CareCare has two acute care hospitals, seven Critical Access Hospitals and 30 standalone clinics, many of them in rural areas.

CentraCare reported a positive margin this year, but in no way realizes the profits of insurers, especially the national insurers where Liebl is having the most difficulty with claims.

CentraCare’s goal in its cost to collect – not all-around denials – is to be at 2%. The health system is closer to 7% on its cost to collect.

“The cost for our organization is exorbitant,” Lieble said.

Much of the blame for denials is falling to artificial intelligence being used in algorithms to deny claims.

UnitedHealthcare has been sued in a class action lawsuit that alleges the insurer unlawfully used an artificial intelligence algorithm to deny rehabilitative care to sick Medicare Advantage patients.

Cigna has also been suedfor allegedly using algorithms to deny claims. The lawsuit claims the Cigna PXDX algorithm enables automatic denials for treatments that do not match preset criteria, evading the legally required individual physician review process.

A Cigna Healthcare spokesperson said the vast majority of claims reviewed through PXDX are automatically paid, and that the PXDX process does not involve algorithms, AI or machine learning, but a simple sorting technology that has been used for more than a decade to match up codes. Claims declined for payment via PXDX represent less than 1% of the total volume of claims, the spokesperson said.

Industry consultant Adam Hjerpe, who formerly worked for UnitedHealth Group, said there’s nothing new about payers using artificial intelligence. AI has been used for 20 years in robotic processes, statements in Excel and algorithms, he said.

Everybody is working with good intent, Hjerpe said. There are reasonable controls in place to avoid fraud and abuse.

Claims are being denied for missing information, or for the information being out of sequence, or for the claim giving an incomplete picture of the care.

“We don’t want care delayed,” he said.

Nobody wins in claims denials, said Susan Taylor, Pega’s vice president of Healthcare and Life Sciences.

While payers save money in the short-term, in the long-term, the best arrangement is to have payers and providers work together to prevent denials, said Taylor, who has worked in healthcare for more than 25 years, starting on the health system side before moving into IT.

“There are more claims of note being denied,” Taylor said. “If you look at the ecosystem, there are a lot of opportunities for error.”

The solution is building an agility layer to streamline workflows throughout the revenue cycle, from initial claim submission to the complex denials processing stage.

WHY THIS MATTERS

Liebl said that denials have increased over the past two years and that there’s also been an uptick in payer audits months after payment has been made.

Insurers want justification for why CentraCare should keep its payments, and this is especially true for Medicare Advantage claims, she said.

One insurer said the claim didn’t meet inpatient criteria and downgraded the claim to an observation patient.

“We have a pretty good success rate as far as being able to justify we did the right care,” Liebl said.

Asked what’s driving the higher denial rates Lieble said, “Everybody wants to keep margins and expand their business. I think it comes down to profit margins, trying to keep profit margins high; we’re just trying to stay afloat.”

To combat denials and work with payers, CentraCare founded a joint operating committee to have successful partnerships. They’ve been more successful with the local Minnesota plans than the national plans, but Liebl is optimistic, she said.

“I am hopeful we can create partnerships …” she said. “Some of the denials we receive are against their payer policy. We need to be able to hold payers accountable.”

Larger health systems have a little more clout, and CentraCare is able to partner with other health systems through the Minnesota Hospital Association.

What’s being lost in all this is the patient, Liebl said. Sometimes a patient is getting a bill up to a year after a procedure.

“Sometimes the patient focus is lost when we work through some of this,” she said.

“They keep our money longer,” Liebl said. “They hold our money hostage. We have denials sitting out there for 300 days. It’s a lot of administrative burden on our part. We’ve spent a lot of money just to get the money in the door. Finally when that claim has been resolved, it’s a year later. No one wins? I think there is some winning going on one side.”

Published this week in Stat, this article explores the confusing payment landscape patients must navigate when receiving colonoscopies. While the Affordable Care Act requires that preventative care services be covered without cost-sharing, this only applies to the “screening” colonoscopies that low-risk patients are recommended to get every ten years.

But when procedures are performed at more frequent intervals for higher-risk patients, they are called “surveillance” or “diagnostic” colonoscopies, for which patients have no guarantees of cost-sharing protections, despite being essentially the same procedure, done for the same purpose.

If a gastroenterologist finds and excises one or more precancerous polyps during a screening colonoscopy, the procedure can leave the patient—especially one with a high deductible health plan—with a large, unexpected bill.

The Gist: Against the backdrop of a sharp rise in colorectal cancer rates among US adults under 65, articles like this are a frustrating demonstration of how insurance incentive structures can work against optimal care delivery.

Incentives should be carefully designed such that proven, preventative screenings—at the discretion of their doctor—are widely available to patients with minimal financial barriers. Surely, no one is “choosing” to have an “unnecessary” colonoscopy—as the procedure is notoriously disliked by patients.

At UnitedHealth Group’s (UHG’s) 2023 investor conference, Optum Health CEO Amar Desai, MD, revealed that Optum has added nearly 20K physicians in 2023, bringing its total physician count to nearly 90K.

None of these acquisitions were formally disclosed, including this year’s largest known pickup, Crystal Run Healthcare—a Middletown, NY-based group with over 400 doctors—which only became public after an internal email was shared with the press. Optum was already the nation’s largest employer of physicians by far, and its nearly 30 percent growth in 2023 only extends its lead.

The next two largest physician employers, Ascension and HCA Healthcare, manage a combined total of around 100K. Optum also employs or affiliates with an additional 40K advanced practice clinicians.

The Gist: Optum’s physician acquisition binge continues at a stunning pace: it has tripledits physician ranks since 2017, and now controls nearly 10 percent of all physicians in the US. But now that it has amassed a veritable physician army, there are emerging signs that it’s turning attention to right-sizing and rationalizing this massive portfolio.

Recent layoffs at the Everett Clinic and the Polyclinic in greater Seattle suggest an end to Optum’s more hands-off initial approach to integration. While each of Optum’s myriad medical group acquisitions has been too small, relative to total company revenue, to trigger regulatory review, the proposed updates to federal merger reporting requirements could put a damper on its unfettered provider buying spree.

According to a Wall Street Journal exclusive published this Wednesday, Bloomfield, CT-based Cigna and Louisville, KY-based Humana, two of the nation’s largest health insurers, are exploring a merger that could close as soon as the end of this year.

With Cigna valued at around $83B and Humana at roughly $62B, their potential combination would be the largest domestic merger of the year, not just in healthcare, but across all industries.

According to anonymous insiders, the companies are discussing a cash-and-stock deal, but nothing has been finalized. Should an agreement be reached, the merger is expected to receive close attention from antitrust authorities. Both Humana and Cigna have attempted to merge with rival insurers over the past decade, only to see the deals blocked on antitrust grounds.

The Gist: This would be a blockbuster deal, putting the combined entity on par with CVS Health and UnitedHealth Group.

Though Cigna and Humana have relatively little direct overlap in their health insurance businesses—Humana recently announced it will exit the commercial group business to focus on its more successful Medicare Advantage (MA) offerings and Cigna, mostly a commercial insurer, is reportedly shopping its much smaller MA business—their respective pharmacy benefit managers (PBMs) may be an antitrust sticking point. (By market share, Cigna’s Express Scripts is the second-largest PBM, while Humana’s CenterWell Pharmacy is fourth.)

Given the Biden administration’s focus on targeting potentially anticompetitive healthcare mergers, as well as rising Congressional scrutiny around PBMs, this potential merger is sure to face many hurdles prior to closing.

This week, Statpublished a scathing investigation into the way UnitedHealth Group subsidiary NaviHealth uses an algorithm, nH Predict, to deny Medicare Advantage (MA) patients access to rehabilitation services and long-term care. United set a target to keep rehab stays within one percent of nH Predict’s projection for the year.

Interviews with former case managers and access to internal documents reveal that NaviHealth employees faced disciplinary action and even termination if they approved care that strayed from these algorithmic recommendations.

UnitedHealthcare, the nation’s largest insurer, is now subject to a class-action lawsuit filed this week over these practices. But NaviHealth’s impact extends beyond just United beneficiaries, as other insurers, covering around 15M MA enrollees, also use its services.

The Gist:This article provides a stark example of what can happen when an artificial intelligence (AI) algorithm is used not to complement, but to replace, clinical judgment.

While profit incentives in US healthcare are nothing new, what’s pernicious about an algorithm like nH Predict is how it replaces individual patients, whose needs vary, with a theoretical “average patient”, whose health and life needs can be easily predicted by the handful of data points available to the insurer.

When patients fail to recover along expected timelines—that are imperfectly calculated by incomplete datasets—they’re the ones who suffer.

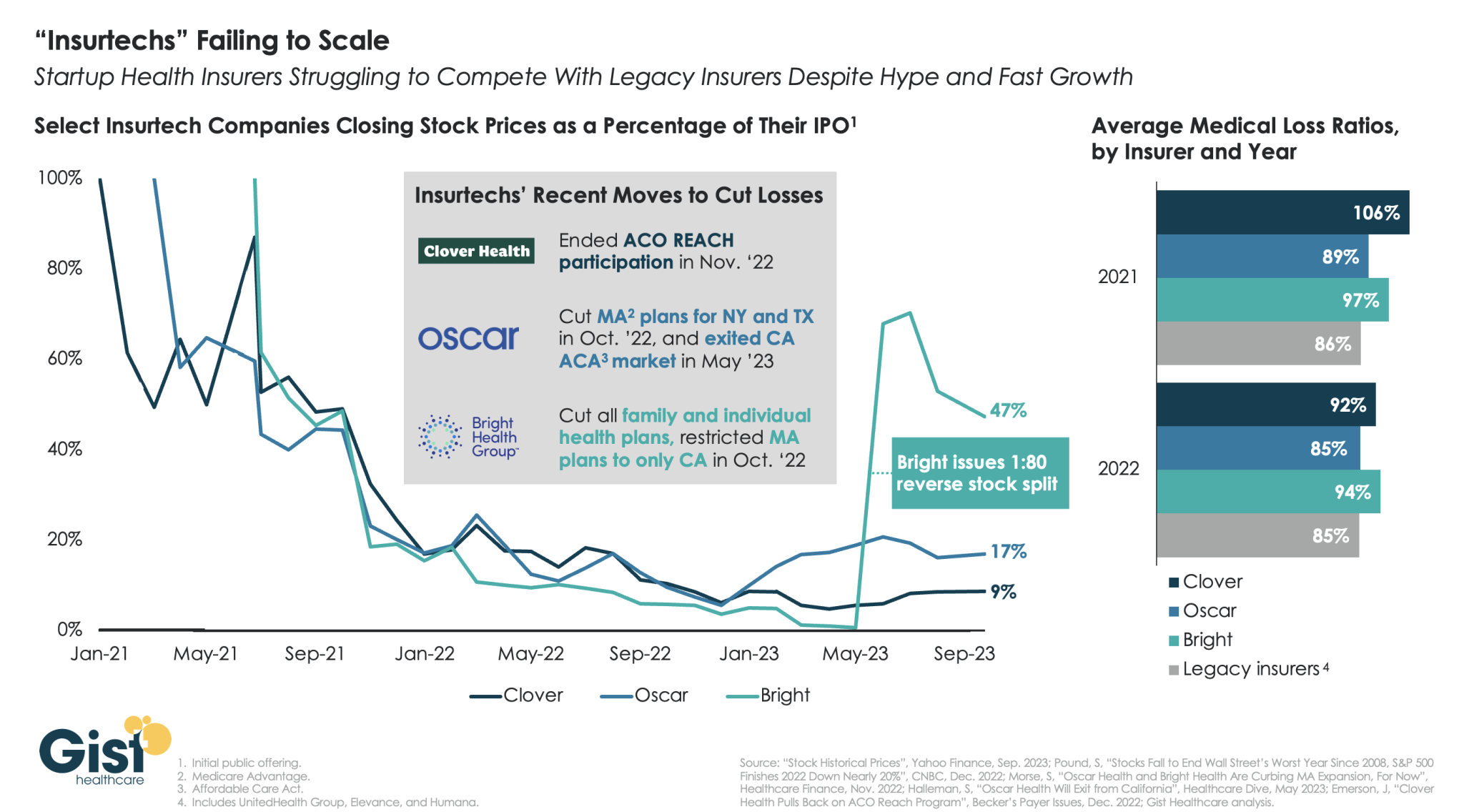

“Insurtechs” Clover Health, Oscar Health, and Bright Health all went public in the midst of the hot equity market of 2021. Investors were excited by the fast growth of these health insurer startups, and their potential to revolutionize an industry dominated by a few large players.

However, the hype has dissipated as financial performance has deteriorated. After growing at all costs during a period of low interest rates, changing market conditions directed investors to demand a pivot to profitability,which the companies have struggled to deliver—twoyears later,none of the three has turned a profit.

Oscar and Bright have cut back their market presence significantly, while Clover has mostly carried on while sustaining high losses. In the last two years, only Oscar has posted a medical loss ratio in line with other major payers, who meanwhile are reporting expectation-beating profits. While Oscar has shown signs of righting the ship since the appointment of former Aetna CEO Mark Bertolini,

the future of these small insurers remains uncertain. As their losses mount and they exit markets, they may become less desirable as acquisition targets for large payers.

Medicare Advantage provides health coverage to more than half of the nation’s seniors, but a growing number of hospitals and health systems nationwide are pushing back and dropping the private plans altogether.

Among the most commonly cited reasons are excessive prior authorization denial rates and slow payments from insurers. Some systems have noted that most MA carriers have faced allegations of billing fraud from the federal government and are being probed by lawmakers over their high denial rates.

“It’s become a game of delay, deny and not pay,” Chris Van Gorder, president and CEO of San Diego-based Scripps Health, told Becker’s.

“Providers are going to have to get out of full-risk capitation because it just doesn’t work — we’re the bottom of the food chain, and the food chain is not being fed.”

In late September, Scripps began notifying patients that it is terminating Medicare Advantage contracts for its integrated medical groups, a move that will affect more than 30,000 seniors in the region. The medical groups, Scripps Clinic and Scripps Coastal, employ more than 1,000 physicians, including advanced practitioners.

Mr. Van Gorder said the health system is facing a loss of $75 million this year on the MA contracts, which will end Dec. 31 for patients covered by UnitedHealthcare, Anthem Blue Cross, Blue Shield of California, Centene’s Health Net and a few more smaller carriers. The system will remain in network for about 13,000 MA enrollees who receive care through Scripps’ individual physician associations.

“If other organizations are experiencing what we are, it’s going to be a short period of time before they start floundering or they get out of Medicare Advantage,” he said. “I think we will see this trend continue and accelerate unless something changes.”

Bend, Ore.-based St. Charles Health System has taken it a step further and is not only considering dropping all Medicare Advantage plans, but is also encouraging its older patients not to enroll in the private Medicare plans during the upcoming enrollment period in October.

The health system’s president and CEO, CFO and chief clinical officer cited high rates of denials, longer hospital stays and overall administrative burden for clinicians.

“We recognize changing insurance options may create a temporary burden for Central Oregonians who are currently on a Medicare Advantage plan, but we ultimately believe it is the right move for patients and for our health system to be sustainable into the future to encourage patients to move away from Medicare Advantage plans as they currently exist,” St. Charles Health CFO Matt Swafford said.

“I feel terrible for the patients in this situation; it’s the last thing we wanted to do, but it’s just not sustainable with these kinds of losses,” Mr. Van Gorder added. “Patients need to be aware of how this system works. Traditional Medicare is not an issue. With these other models, seniors need to be wary and savvy buyers.”

Here are six more recent examples of hospitals dropping Medicare Advantage contracts:

1. Adena Regional Medical Center is terminating its contract with Anthem BCBS’ Medicare Advantage and managed Medicaid plans in Ohio, effective Nov. 2. The flagship facility of Chillicothe, Ohio-based Adena Health System said rate negotiations between the organizations “have not been productive,” leading it to terminate its agreement with Anthem, whose parent company is Elevance Health.

2. Corvallis, Ore.-based Samaritan Health Servicesended its commercial and Medicare Advantage contracts with UnitedHealthcare. The five-hospital, nonprofit health system cited slow “processing of requests and claims” that have made it difficult to provide appropriate care to UnitedHealth’s members, which will be out of network with Samaritan’s hospitals on Jan. 9. Samaritan’s physicians and provider services will be out of network on Nov. 1, 2024.

3. Cameron (Mo.) Regional Medical Center stopped accepting Cigna’s MA plans in 2023 and plans to drop Aetna and Humana in 2024. It plans to continue Medicare Advantage contracts with UnitedHealthcare and BCBS, the St. Joseph News-Press reported in May. Cameron Regional CEO Joe Abrutz previously told the newspaper the decision stemmed from delayed reimbursements.

4. Stillwater (Okla.) Medical Centerended all in-network contracts with Medicare Advantage plans amid financial challenges at the 117-bed hospital. Humana and BCBS of Oklahoma were notified that their MA members would no longer receive in-network coverage after Jan. 1, 2023. The hospital said it made the decision after facing rising operating costs and a 22 percent prior authorization denial rate for Medicare Advantage plans, compared to a 1 percent denial rate for traditional Medicare.

5. Brookings (S.D.) Health System will no longer be in network with any Medicare Advantage plans in 2024, the Brookings Register reported. The 49-bed, municipally owned hospital said the decision was made to protect the financial sustainability of the organization.

6. Louisville, Ky.-based Baptist Health Medical Group went out of network with Humana’s Medicare Advantage and commercial plans on Sept. 22, Fox affiliate WDRB reported.