Cartoon – Market Development

President Donald Trump’s plan to make it easier for small businesses to band together and buy stripped-down health insurance plans could violate a federal law governing employee benefit plans and will almost certainly be challenged in court, legal experts said.

Trump signed an executive order on Thursday aimed at letting small businesses join nationwide associations for the purpose of buying large-group health plans that are not subject to coverage requirements of the Affordable Care Act, commonly known as Obamacare.

Industry experts said Trump’s order could ultimately enable such associations to purchase insurance from states with the fewest regulations. That would undermine Obamacare, former Democratic President Barack Obama’s signature healthcare law, which Republicans have failed to repeal.

Several healthcare and employment law experts said if Trump’s plan moves forward, states could argue the federal government had overstepped its authority in violation of the U.S. Employee Retirement Income Security Act (ERISA), a law that governs large-group plans.

In Thursday’s order, Trump asked the Department of Labor to propose rules that would allow more employers to participate in association health plans. Legal experts said lawsuits might not be brought until such regulations are issued.

Dania Palanker, an assistant research professor at Georgetown University’s Center on Health Insurance Reforms, said ERISA granted states the right to regulate association health plans.

Attorneys general could argue the federal government had overreached if the Trump administration winds up allowing associations to buy health coverage across borders that only complies with a single state’s regulations.

”Any attempt to allow the sale of association plans to small groups across state lines will be open to legal scrutiny as to whether it is violating ERISA and undermining state authority,” said Palanker.

‘PREPARED TO FIGHT’

A White House official said that “departments will be drafting rules in a way that minimizes litigation risk.”

The Department of Labor “will be reviewing ERISA in the course of following the President’s direction” in the order, the official said.

A number of state attorneys general from Democratic-leaning states said on Thursday they would fight any efforts to weaken Obamacare, which extended health insurance to 20 million Americans, but which Republicans call intrusive and ineffective.

“It should come as no surprise that California is prepared to fight in court to protect affordable healthcare for its people,” said Xavier Becerra, the state’s Democratic attorney general.

Legal experts said states may argue the associations formed for the purpose of buying insurance are not employers under ERISA.

Although ERISA allows associations to qualify as employers and manage large-group plans, federal regulators have generally required that members of such associations have a high degree of common interest beyond buying insurance, said Allison Hoffman, a professor at the University of Pennsylvania School of Law.

Trump’s order asks the secretary of labor, who enforces ERISA, to consider expanding the common-interest requirements to permit broader participation in association health plans.

The idea of expanding association health plans across state lines has long been championed by Republican U.S. Senator Rand Paul, who made it a key plank of his own proposal to repeal and replace Obamacare. The Kentucky Republican was at Trump’s side when the president signed the executive order.

Paul’s proposal said ERISA was too restrictive in its definition of associations and that the law needed to be amended.

Thursday’s order also asked the Labor, Treasury and Health and Human Services Departments to look into expanding participation in cheaper, bare-bones, short-term limited-duration insurance plans, which are not subject to the ACA.

Timothy Jost, a professor at the Washington and Lee University School of Law, said such a move would face fewer legal hurdles than the expansion of association health plans.

The current three-month limitation on the use of such plans was a rule adopted by the Obama administration last year, so the Trump administration could roll it back through the normal rulemaking process.

Such plans are typically marketed to individuals who are between jobs or have a gap in coverage. They are much cheaper than ACA plans, but cover less and can exclude those with pre-existing conditions.

With efforts to repeal the Affordable Care Act dead in Congress for now, a critical test for the law’s future is playing out in one small, conservative-leaning state.

Iowa is anxiously waiting for the Trump administration to rule on a request that is loaded with implications for the law’s survival. If approved by the federal Centers for Medicare and Medicaid Services, it would allow the state to jettison some of Obamacare’s main features next year — its federally run insurance marketplace, its system for providing subsidies, its focus on helping poorer people afford insurance and medical care — and could open the door for other states to do the same.

Iowa’s Republican leaders think their plan would save the state’s individual insurance market by making premiums cheaper for everyone. But critics say the lower prices come at the expense of much higher deductibles for many with modest incomes, and that approval of the plan would amount to another way of undermining the law. Already the administration has slashed funding for advertising and outreach to help people sign up for insurance, and President Trump is preparing to issue an executive order allowing more access to plans that don’t meet the law’s standards.

Adding to the uncertainty, the Washington Post reported last week that Mr. Trump in August asked Seema Verma, the federal official in charge of reviewing Iowa’s plan, to reject it. Some supporters of the law saw that as a deliberate effort to keep premiums high; Mr. Trump frequently cites sharply rising premiums as proof that the health law is failing.

Neither C.M.S. nor the White House would comment on whether Mr. Trump had pushed for the application to be denied. A spokeswoman for C.M.S. said only that the plan remains under review.

In Des Moines on Tuesday, Gov. Kim Reynolds told reporters that her team was in constant contact with the White House and C.M.S. about the plan, including a call with Ms. Verma this week, trying “to get to yes.” She said the administration has been “very receptive” to the plan as a solution to the “unaffordable,” “unworkable” health law until it can be repealed.

Iowa calls its request a stopgap plan that would allow the state to opt out of the federal health insurance marketplace, HealthCare.gov, for 2018 and create a state-run system that its insurance commissioner says would lower premiums for the 72,000 Iowans who currently have Obamacare health plans, including 28,000 who earn too much to get subsidies to help with the cost.

But the cheaper premiums would come with a big trade-off: higher out-of-pocket costs. The only option for customers would be a plan with deductibles of $7,350 for a single person and $14,700 for a family. The proposal would also reallocate millions of federal dollars that the health law dedicates to lowering costs for people with modest incomes and use the money for premium assistance to those with higher incomes, no matter how much money they make.

The individual insurance market is particularly fragile in Iowa, partly because the state has allowed tens of thousands of people to keep old plans that do not meet the health law’s standards. Aetna and Wellmark Blue Cross & Blue Shield, the state’s most popular insurer, are both withdrawing at the end of the year. The only insurer planning to remain, Medica, is seeking premium increases that average 56 percent, blaming Mr. Trump’s ongoing threats to stop paying subsidies known as cost-sharing reductions that lower many people’s deductibles and other out-of-pocket costs. Wellmark has said it will stay if the stopgap plan is approved.

“What we are trying to address is a really large number of people being priced out,” said Doug Ommen, the state’s Republican insurance commissioner.

Two other states, Alaska and Minnesota, have already won permission to shore up their Obamacare markets with waivers allowed under the law; they will use federal money to help insurers cover the claims of their most expensive customers next year. But Oklahoma abruptly withdrew a similar request in late September — one that state officials said would have reduced premiums by an average of 30 percent — saying that the Trump administration had reneged on a promise to approve it by Sept. 25 and they were out of time. (A C.M.S. spokeswoman said, “At no time was an approval package or an approval date ever agreed upon.”)

Iowa’s waiver request is more far-reaching, providing what Timothy S. Jost, an emeritus professor of health law at Washington and Lee University, has called a “watershed moment” for Obamacare.

“It’s a decision to abandon a number of key principles of the Affordable Care Act,” he said.

Under the law, people who don’t get insurance through work can buy it through the online marketplace. They get federal subsidies to help with the cost if their income is below 400 percent of the poverty level, or about $65,000 a year for a couple. Those whose incomes are below 250 percent of the poverty level — $40,600 a year for a couple — also get cost-sharing reductions.

Iowa’s plan would reallocate much of that federal assistance, using it to provide premium subsidies based on age and income for even the wealthiest individual market customers. It would also be used to create a “reinsurance” program, like Alaska’s and Minnesota’s, to help insurers cover their sickest customers. The law’s essential health benefits and protections for people with pre-existing conditions would remain in place, but every individual market customer would get the same standardized high-deductible plan.

Mr. Jost and other supporters of the law say Iowa’s proposal does not meet the requirements for so-called innovation waivers, including that the coverage they provide must be at least as comprehensive and affordable as Obamacare plans, because poorer people would face higher deductibles and other out-of-pocket costs. That, they say, leaves the plan open to almost-certain legal challenges.

Seemingly acknowledging that problem, Mr. Ommen has tweaked Iowa’s proposal — including with a supplemental filing to the Trump administration on Thursday — to preserve subsidies that reduce out-of-pocket costs for roughly 21,000 low-income Iowans.

But those at slightly higher income levels would lose cost-sharing assistance completely, facing the $7,350 deductible and other out-of-pocket expenses.

“You still have some real problems from the perspective of making sure low-income people can afford coverage,” said Joel Ario, a managing director at Manatt Health who worked on the Affordable Care Act at the Department of Health and Human Services during the Obama administration.

But for the roughly 28,000 Iowans who have Obamacare coverage but earn too much to get subsidies, the need for a shake-up is urgent. And with open enrollment starting in about three weeks, time is of the essence.

Dozens of them, including many farmers, submitted comments to Mr. Ommen or testified at public hearings in favor of the stopgap plan, with many saying they would be forced to drop their insurance next year if it were not approved.

“Fortunately both my husband and I have already prepaid our funeral expenses,” write a woman identified as Nancy K., of Bellevue, who said she could no longer afford her coverage. “Every single item, even our cemetery marker, is paid for or covered for my death in the event that we cannot afford insurance to pay for any so-called catastrophic health care.”

Landi Livingston, whose family raises beef cattle in rural southern Iowa, said she was paying almost $500 a month for a Wellmark plan and dreaded having to switch to Medica next year, with what she assumed would be significantly higher prices.

If the Trump administration approves the state’s request, Ms. Livingston’s premium would likely drop to around $350 a month, according to estimates from the state, saving her $1,800 next year. But her $3,000 deductible would more than double, meaning that if she had high medical expenses she could end up paying more toward those bills.

“I still think it’s the best thing on the table right now,” she said of the stopgap plan. “It’s high time the people in power get this figured out.”

For Tony Ross, a retired paralegal in Des Moines who has a subsidized marketplace plan from Aetna, the stopgap plan would lower his premiums to about $85 a month, from $220, according to the state estimates. But his deductible – currently $750 because his low income qualifies him for cost-sharing reductions – would balloon by almost tenfold. That would mean paying thousands more each year for his expensive blood pressure medication, he said.

“Obviously I need a way lower deductible than $7,350,” said Mr. Ross, 63. “This doesn’t seem like a fair way of fixing things.”

https://www.vox.com/policy-and-politics/2017/10/11/16447504/obamacare-open-enrollment-trump-sabotage

/cdn.vox-cdn.com/uploads/chorus_asset/file/9426285/Screen_Shot_2017_10_09_at_5.14.59_PM.png)

President Trump hasn’t succeeded in repealing Obamacare yet. But his administration is doing its best to force the law to fail.

The most critical time of the year for the health care law is almost here: open enrollment, when millions of people log on to online marketplaces, check whether they qualify for federal subsidies to help them pay their premiums, and shop for plans. For the past three years, at least 10 million people have gotten insurance that way each year.

But this year, open enrollment is in the hands of a White House that’s openly hostile to the Affordable Care Act — and the Trump administration is taking advantage of the best opportunity it has to undercut the law.

President Trump has said that he wants Obamacare to implode, which he hopes would reignite the stalled congressional effort to repeal it. He isn’t just sitting around waiting for that to happen. His administration halved the length of open enrollment. They slashed spending on advertising and assistance programs. They pulled out of outreach events at the last minute.

The entire health care law could be at stake. Advertising and outreach are primarily targeted to younger and healthier people, who are essential to the law’s goal of affordable insurance coverage for all Americans. If their enrollment drops while older, sicker people keep signing up, premiums are going to increase even more next year.

It’s the start of a death spiral, a self-perpetuating cycle of price hikes and falling enrollment — which is exactly what Trump has said he wants.

“I think what this cumulative activity can do is start that death spiral,” Kathleen Sebelius, President Obama’s health and human services secretary during the ACA’s first open enrollment, told me.

Obamacare supporters are already conceding that as a result of these cuts, they likely won’t be able to match last year’s 12 million sign-ups. “I don’t actually think that’s possible anymore,” Lori Lodes, who worked on Obamacare enrollment in the Obama administration, told me.

We will know by December 15, the end of this year’s open enrollment period, how much the White House has succeeded in gutting Obamacare. By embracing this strategy, the Trump administration has put its political goals ahead of the millions of people who depend on the ACA for insurance.

“I really do think what they want to be able to do is come out on December 16 and say, ‘See, we told you Obamacare is imploding; it’s failing,’” Lodes said. “When the reality is they are going to be responsible because of the decisions they’ve made to undermine open enrollment.”

Every fall, the Obamacare insurance marketplaces open for business. People have a few weeks to log on, check out their options, and sign up for coverage. This year, sign-ups start on November 1 and close on December 15.

An entire apparatus exists to support open enrollment. Most states use the federal Healthcare.gov, while a few run their own marketplaces. The feds and some states run call centers, where people can talk to a real person to walk through enrollment. The federal government funds navigator and in-person assistance programs, which set up places where people can get help navigating the sign-up process.

Open enrollment hasn’t technically changed much this year, except it’s been shortened from 12 weeks to six. Otherwise, it’s pretty much the same. Healthcare.gov will still be open. People can still get tax subsidies and shop for coverage. All of the ACA’s regulations, such as protections for people with preexisting conditions and the requirement that insurers cover essential health benefits, remain in place.

But the mere need to clarify that, yes, Obamacare is still around is a big problem for open enrollment. After eight months of Republicans fighting to repeal it while claiming it’s failing, people like Lodes worry that many Americans think the law either is already gone or won’t be around for much longer.

Which is why outreach is so important.

The Obama administration went all out every year to promote open enrollment. President Obama appeared on late-night TV and viral online shows. The administration recruited celebrities to star in ads or highlight open enrollment on social media. Senior officials scrounged for as much money for the navigator program as they could find.

While things didn’t always go smoothly — the launch of Healthcare.gov was a disaster — the efforts helped 12 million people sign up for coverage in 2016. The uninsured rate has dropped to historic lows, and insurers have started to see improved business on the law’s marketplaces.

The key, Lodes said, was blanketing people with information — from television ads and email and text message reminders to working with community-based groups and churches. The biggest barrier was convincing people they could actually afford insurance, once the law’s financial assistance was accounted for.

Outreach works: The Huffington Post reportedrecently that an internal Health and Human Services Department report concluded that 37 percent of sign-ups in the last few months of 2016 could be attributed to outreach.

Trump administration officials have defended their outreach cuts in part by arguing that people are already familiar with Obamacare after three years. “I don’t think we can force people to sign up for a program,” a senior administration official told reporters in August.

But that runs counter to the available evidence. Nearly 40 percent of the US uninsured were still unaware of the marketplaces last year, and almost half did not know they might be eligible for financial assistance, according to surveys by the Commonwealth Fund.

“There is a difference knowing Obamacare is the law and knowing what you should do with that information,” Lodes said, “between knowing you need to sign up in this finite period of time or you do not get health coverage.”

The Obama administration had assumed that older people or people with preexisting conditions who struggled to get insurance before the ACA would be eager to sign up. So they focused their efforts on reaching younger people or people who hadn’t had insurance before. Every year, people turn 26 and roll off their parents’ health insurance, or maybe they get a new job with a higher salary and need to move from Medicaid to private insurance.

Every year, in other words, there are brand new customers for the ACA marketplaces.

“They’re either the least familiar or they are the healthiest. Either way, they either don’t know or don’t believe they need or want health insurance,” Sebelius said. “For somebody to suggest that there is no persuasion needed is just nuts.”

Because open enrollment is such a sprawling undertaking, the Trump administration has many tools at its disposal to undermine it and, by extension, the ACA. It seems to be using all of them.

The White House has some minimal requirements under federal law. It must perform outreach and education, it must run a call center, it must have a website where people can enroll, and it must operate a navigator program.

On paper, the Trump administration will do each of those things. But each is facing significant cuts. Together, they add up to a clear picture of an administration using every means available to drop support for ACA enrollment:

In other words, the Trump administration is cutting funding for outreach, cutting funding for enrollment assistance, and dropping out of partnerships to support enrollment, while shrinking the window for people to sign up for coverage, sowing doubts about whether people will be required to have insurance, and making threats that drive up premiums.

So as Trump claims Obamacare is failing, his administration is setting up a self-fulfilling prophecy.

Obamacare supporters are trying to fill the gaps with grassroots programs like the Get Covered campaign, run by former Obama administration officials. But they do not have the same resources as the federal government.

The ideal TV advertising campaign, for example, would cost about $15 million, said Lodes, who is helping to oversee Get Covered. They already know, with mere weeks left until open enrollment starts, that they will not be able to raise that kind of money, which means the hole left by the Trump administration cutting $90 million from the ACA’s advertising budget will go largely unfilled.

“There is no way that anything we do or anyone else does can fill the footprint of what the admin should be doing,” she said. “They were unable to get repeal passed through the Congress, so they really seem intent to do everything they can do to make sure open enrollment is not successful.”

The inevitable result of the Trump administration’s actions will be fewer Americans with health insurance. Last year, 12 million people signed up for coverage through the Obamacare marketplaces. Nobody expects to match that number this year, after open enrollment has been so severely undermined.

“There is no doubt that the actions by the administration will mean that fewer people get covered,” Lodes said.

The number of uninsured Americans will likely tick up from its current historic lows. Hundreds of thousands or even millions will not be financially protected against a medical emergency, and it will be harder for them to afford the routine health care that prevents bigger problems later on. That will have a real effort on people’s lives and financial security.

But falling enrollment also threatens Obamacare’s future.

The law works when younger, healthier people and older, sicker people all sign up for coverage. Insurers need the low-cost patients to help cover the costs of the sicker ones, who are more likely to rack up big medical bills. The ACA has both sticks (the individual mandate) and carrots (cheaper premiums for young people and generous subsidies) to get everybody into the market.

But getting younger and healthier people takes a little more effort. They have been the focus of the outreach that Trump is now cutting.

People who have medical conditions already or who are older and know they may soon need insurance are going to find a way to enroll regardless. But young and healthy people are less likely to think they need insurance. They need some persuading that the ACA’s coverage will help them in an unlikely medical event and that they will be able to afford it, Sebelius and Lodes said.

“The last person to sign up is probably the healthiest person to sign up,” David Anderson, a former insurance industry official who now researches at Duke University, told me.

With a sicker pool left behind, health insurers are likely to either increase premiums even more next year or leave the market altogether. Plans have already cited the marketing cuts as one reason for increased premiums in 2018. And the higher premiums get, the more difficult it is to persuade young and healthy people to pay the price.

If sign-ups plummet — which even Obamacare supporters expect after the Trump administration has done so much to undermine open enrollment — the law’s future will be in serious peril.

“What that means over the long term is the health of the marketplace is at risk,” Lodes said.

No matter what the president says, Obamacare isn’t failing yet. But his administration is trying as hard as it can to make those words a reality.

https://www.axios.com/vitals-2497054515.html

Good morning … Last week gave us an executive order and an end to cost-sharing payments. Can’t wait to find out what the health policy universe has in store for us this week.

Data: Kaiser Family Foundation; Daily Kos Elections; Census Bureau; Chart: Chris Canipe / Axios

Data: Kaiser Family Foundation; Daily Kos Elections; Census Bureau; Chart: Chris Canipe / Axios

The Trump administration’s decision to stop paying the Affordable Care Act’s cost-sharing reduction subsidies will affect ACA customers in Republican-leaning congressional districts as well as Democratic ones. Here’s a look at how many people could feel the impact in districts that voted for President Trump, compared with those in districts that voted for Hillary Clinton.

The details: This year, 11.1 million people were enrolled in ACA marketplace plans or in a Basic Health Plan created by the law. Of those, 5.9 million live in Republican-held congressional districts and 5.2 million live in districts held by Democrats, per the Kaiser Family Foundation.

The impact: The CSR subsidies are going to 58% of the people who are enrolled in ACA marketplace plans. In all, about 7 million people don’t receive any financial assistance with their premiums, so they’d pay the full cost when health insurance companies raise their rates. But others could be affected if health insurers decided to pull out of the markets rather than deal with the instability.

There are broader implications of the Trump administration’s decision to lean so heavily on a legal rationale for cutting off the CSR subsidies: institutional divisions between the executive and legislative branches.

Between the lines: The White House said it was ending the payments in part because of a ruling last spring that said it was unconstitutional to make the payments without an explicit appropriation from Congress. As part of that process, Attorney General Jeff Sessions wrote a memo saying, in effect, there was no point appealing that ruling.

Real talk: Former White House strategist Steve Bannon, speaking at the Values Voters Summit over the weekend, cut to the heart of Trump’s decision: “Not going to make the CSR payments, going to blow that thing up; going to blow those exchanges up, right?”

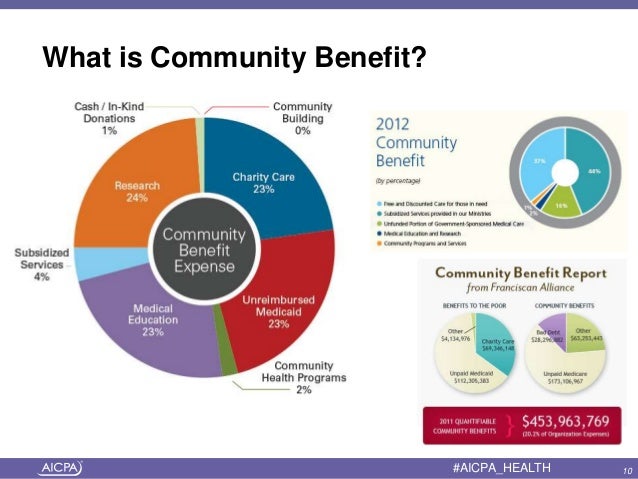

The American Hospital Association released a report last week that said the benefits that not-for-profit hospitals provide to their local communities far outweigh foregone federal tax revenue. But Axios’ Bob Herman talked to some experts who said the AHA’s report has flaws and omissions that exaggerate hospitals’ community roles and understate the power of their tax exemptions.

AHA’s response: Mindy Hatton, the AHA’s top lawyer, responded with a statement to Axios. The report did not include property tax values, she said, because the analysis only covered federal exemptions, which “Congress has jurisdiction over.”