Republican cuts to federal health programs, AI automation and rising costs are making health systems and other employers level off hiring — including for jobs requiring a professional license like nurses or physical therapists.

The results could widen gaps in care and exacerbate health disparities.

By the numbers:

Health care employment drove most of the month-by-month job growth last year, increasing by an average of 34,000 jobs per month, according to the Bureau of Labor Statistics.

But that’s less than health care’s monthly average increase of 56,000 roles in 2024.

Health care hiring hasessentially returned to a pre-pandemic pattern of slower growth after a post-COVID surge driven by returning patients and hospitals replacing burned-out workers, said Neale Mahoney, an economics professor at Stanford.

“It was only a question of when … and we’re starting to see it now,” Mahoney said.

Federal policychanges could further chill hiring.

Hospitals face financial pressure from the nearly $1 trillion cut to federal Medicaid spending in the GOP budget law. That’s combined with rising costs from treating more uninsured patients and other factors.

New caps on federal student loan borrowing could also push students away from clinical careers, many of which require pricey advanced degrees.

It wouldn’t be a surprise if a rise in deportations — combined with fewer foreign-born health workers opting to come to the U.S. on visas — dried up the pipeline of available help, especially in segments like home care.

Case in point:

Alameda Health System, a safety-net provider based in Oakland, California, announced last month that it’s laying off 247 employees, including clinicians.

Administrators cited the system’s precarious finances: It expects to lose $100 million annually by 2030 as a result of the Medicaid cuts, per CBS San Fransisco.

AI automation is also pushing some providers to cut administrative staff.

Revere Health, the largest physician-owned health system in Utah, announced in September that it will lay off 177 employees, citing a partnership with a company that automates claims processing.

Clinical jobs in health care are more insulated from automation, and AI may actually help extend the clinical workforce where shortages exist.

Still, some clinicians are concerned. Almost 15,000 nurses in New York City went on strike this month, demanding new safeguards around AI use in hospitals, among other things.

What they’re saying:

This past year represented “a repositioning of the labor market,” said Rick Gundling, chief mission impact officer at the Healthcare Financial Management Association.

Health systems are doing more targeted hiring, he said. They might look to downsize in revenue management but increase their clinical staff.

The intrigue:

Demand for care is still high. The “silver tsunami” of aging Baby Boomers may keep jobs plentiful, said Laura Ullrich, director of economic research in North America at the Indeed Hiring Lab.

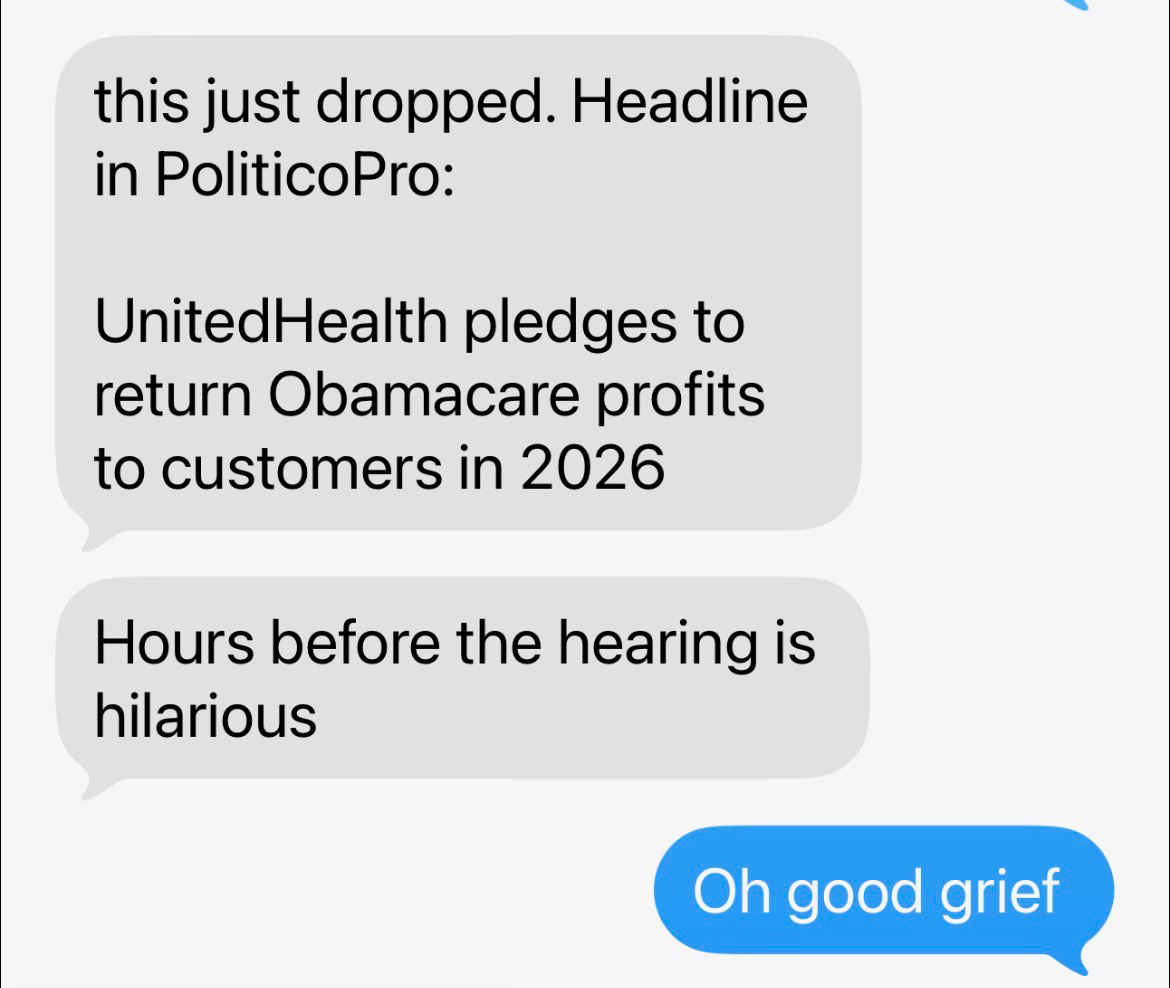

And the questions I’d ask UnitedHealth Group’s CEO about his company’s ACA pledge.

When I first saw the headline that UnitedHealth Group would “return Obamacare profits to customers in 2026,” my immediate reaction was: Oh good grief.

The timing is just too perfect.

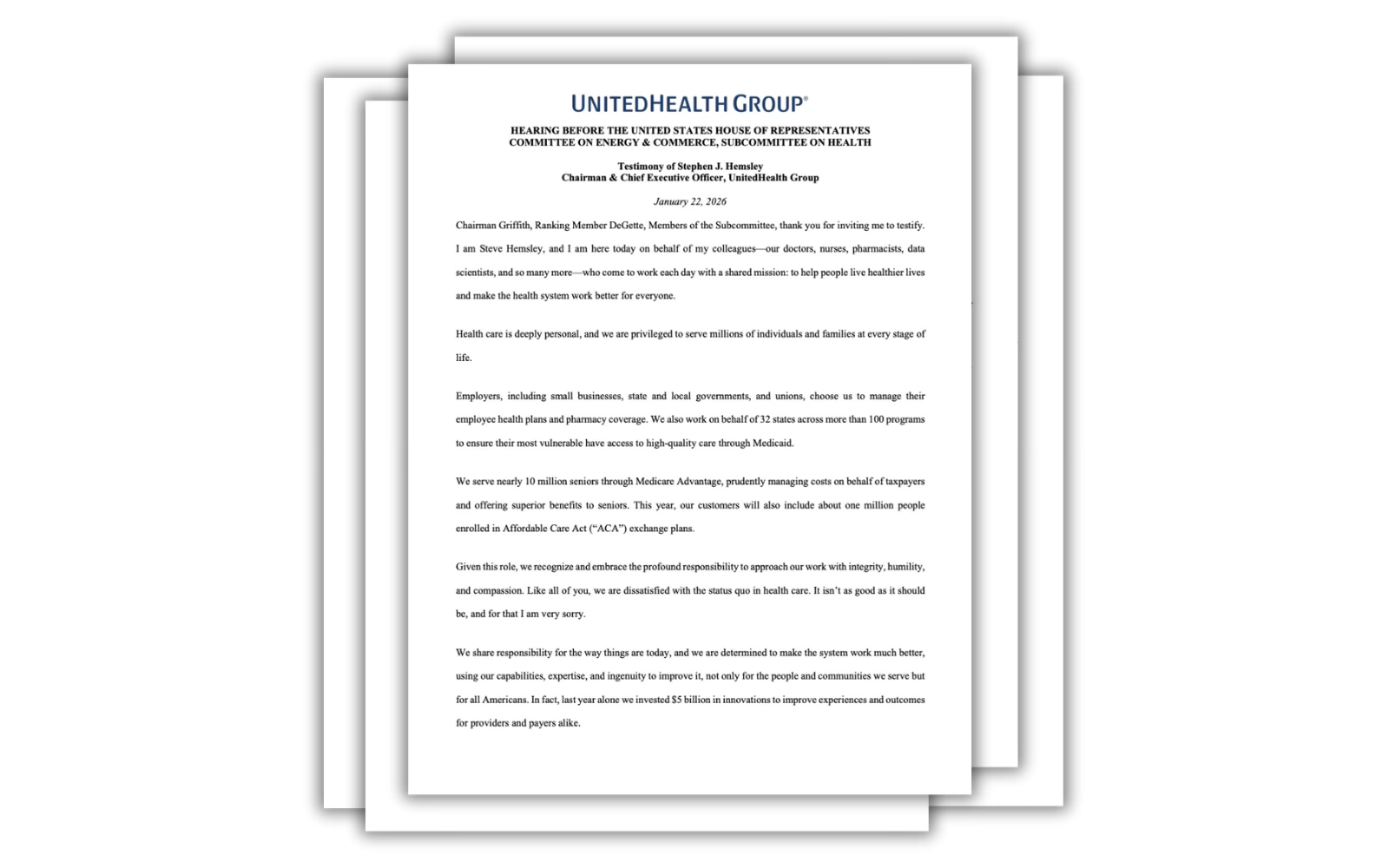

UnitedHealth’s pledge was tucked neatly into prepared testimony from CEO Stephen Hemsley, just hours before he (and four other Big Insurance CEOs) are to be hauled into Congress to testify before two House hearings on health care affordability.

“A text message conversation between my colleague, Joey Rettino, and me.

Today, the CEOs will be asked to explain why Americans are paying through the nose for coverage and still getting denied care, trapped in narrow networks and buried under medical debt. As of late, Republican lawmakers — and President Trump himself — have discovered religion on the issue, publicly fuming about high premiums and insurer abuses.

If you’re feeling a little misty-eyed about this sudden burst of corporate altruism, let me save you the trouble. This isn’t a moral awakening. It’s a PR maneuver and narrative control being implemented in real time.

Hail Mary

It’s the corporate version of a quarterback, down by four points, seconds left on the clock, closing his eyes and launching the ball fifty yards downfield, hoping something — anything — miraculous happens before the time runs out. UnitedHealth’s pledge is just a long, desperate PR pass into the end zone, praying lawmakers and reporters will focus on the gesture instead of the business model that allows them to gobble up those dollars in the first place.

It’s worth noting that UnitedHealthcare, while the largest insurer in the country with 50 million health plan enrollees, is actually a relatively small player in the ACA marketplace — about 1 million customers in 2026, compared with roughly 6 million for Centene, according to Politico. This is not UnitedHealth sacrificing a part of its core profit engine. (It doesn’t even disclose how much it makes on its ACA business, but I can assure you it’s a very small part of the more than $30 billion in annual profits it’s been making in recent years.) This is a carefully calibrated concession of a slice of this conglomerate’s business that won’t jeopardize its Wall Street standing, which is what Hemsley cares about most.

As I wrote yesterday, I spent years inside the insurance industry, helping executives shape their public image and get ahead of bad headlines. I know this playbook by heart. When scrutiny spikes, you roll out a “good guy” story. You announce a consumer-friendly initiative and you flood the zone with talking points. You give lawmakers anything they can point to as evidence of “progress,” so the temperature in the room drops just a few degrees. It’s all an optics game, and if I was in my old job I’d probably get a bonus for thinking of a stunt like this.

Reputational damage control

When Hemsley and his Big Insurance buddies sit before Congress, don’t be surprised if he pivots quickly from this show of supposed humility to pointing fingers at everyone else for driving up costs – including hospitals, doctors, drug companies and whoever else. How do I know this? Hemsley said as much in his prepared testimony. His fellow CEOs sang from the exact same hymnbook, written by the best flacks money can buy.

So no, I’m not impressed by UnitedHealth Group’s gesture. And neither should lawmakers.

If UnitedHealth and its peers were serious about affordability, they wouldn’t be waiting until the night before a congressional grilling to dangle a symbolic rebate. They would be opening their books and explaining their pricing algorithms. They’d come clean about how much of our premium dollar goes to care and how much goes to executive compensation, stock buybacks and acquisitions that tighten their grip on the health care system.

This isn’t a gift. It’s a distraction.

And like most Hail Marys, it doesn’t work if you’re already down a whole lot of points. I hope the lawmakers at today’s hearing remember the score.

In light of UnitedHealth Group’s latest move, see below for some questions that I would ask Hemsley if I were in Congress:

ACA plan and pledge specifics

How many people are enrolled in your ACA marketplace plans, and how much total profit are you committing to rebate to them?

What were your profits from ACA marketplace plans in recent years?

Will you commit to disclosing ACA-specific enrollment and profit figures when you announce 2025 earnings next Tuesday? And how many people dropped coverage after the enhanced ACA subsidies were not renewed?

By how much, on average, did you raise ACA premiums because Congress did not renew those subsidies?

Public money vs. private plans

Between 2020–2024, your filings show about $140 billion in operating profits and roughly $894 billion in revenue from Medicare and Medicaid versus $321 billion from commercial plans. Do you agree that about 74% of your revenue now comes from taxpayers and seniors?

Given that you have about twice as many people in commercial plans as in Medicare/Medicaid, do you agree the government is paying you far more per enrollee than private customers are?

Accountability going forward

Will you commit to disclosing ACA-specific enrollment and profit figures when you announce 2025 earnings next Tuesday?

Will you commit not to raise premiums or fees in your other lines of business to offset the ACA rebates?

Will you commit to providing the transparency and granularity needed for the public to verify that this rebate pledge is real and not a PR maneuver?

Rising health care costs are quietly reshaping family life and pushing homeownership, parenthood and financial stability further out of reach for millions of Americans.

The youngest of Millennials will hit 30 years old this year. For them and their older Millennial-counterparts, this is supposed to be the stage of life where people buy homes, have kids and settle into the textbook version of stability. But the reality for far too many Americans is something entirely different. It means delaying marriage, delaying children, delaying homeownership — and adopting pets to save them from college tuitions and pediatric specialists.

It’s not because an entire generation is collectively bucking the way “adulthood” used to be. It’s because the math doesn’t work anymore – and health insurance costs are a huge part of why.

Health care is eating the family budget

According to a new analysis from the Center for Economic and Policy Research (CEPR), the typical working family spent $3,960 on health care in 2024, including premiums and out-of-pocket costs. That’s the median… meaning half of families paid more.

Another striking finding from CEPR is that one in ten working families paid more than $14,800 in a single year on health care expenses. And for many low-income and rural households, health care consumed more than 10% of their entire income.

When the average Millennial earns about $47,034 a year, even the “average” health insurance spending now represents a meaningful slice of take-home pay before rent, student loans or the price of simply existing are even deducted. That threshold forces real tradeoffs: rent or deductible? Daycare or co-pays? Savings or prescriptions?

For young families trying to get started, that tradeoff answers itself.

Families with children spend significantly more on both health insurance and health care than those without. Working families with at least one child spent a median $5,150 per year.

Add that to childcare costs and it becomes clearer why many Millennials are putting off parenthood — or skipping it altogether. Hence the cat that doesn’t need braces or an albuterol prescription.

Health costs and home ownership

Diapers aside, medical bills also directly collide with the ability to own a home.

A recent study published in JAMA Network Open found that adults carrying medical debt were significantly more likely to experience housing instability such as trouble paying rent and mortgage, or evictions and foreclosures. As KFF researchers found, more than 100 million Americans have medical debt, and the vast majority of them have health insurance. It just isn’t adequate coverage because of ever-growing cost-sharing requirements.

That matters enormously for young families and would-be homeowners. Medical debt lowers credit scores, drains savings needed for down payments and makes lenders more hesitant. It’s hard to compete in today’s housing market when your emergency fund got wiped out by an MRI. Or your credit score took a hit because you found a lump.

This is not about lifestyle choices

In part because of these costs, the traditional milestones that once built financial security now often increase financial risk. Health insurance and health care costs are rising faster than inflation and faster than they did for previous generations. That’s why more and more insured families are delaying prescriptions and skipping care because of cost.

These uniquely American costs bleed into career moves, relationships, everything.

Millennials aren’t afraid of commitment. They’re afraid of math that doesn’t add up in large part because of a health care system that continues to be an ever-growing weight that is capable of wiping out savings and reshaping family decisions.

It’s easy to frame these trends as cultural shifts or personal preferences, but the data helps fill in the blanks. It’s not just Millannials facing these issues. Gen Xers and even Baby Boomers (some of whom still have a few years until they cross the Medicare and Social Security finish line) are dealing with budget-eating health care costs and medical debt, too.

When nearly half of adults say they couldn’t afford an unexpected $500 medical bill, it’s not surprising that people hesitate before taking on a 30-year mortgage or the lifelong responsibility of raising a child (or taking that trip to celebrate their retirement for that matter.)

For now, all that can be said is that Millennials’ cats are doing fine. They are benefiting heavily from the status quo. Maybe they have something to do with all of this.

Health insurers are feeling political heat as Republicans try to shape the affordability narrative and counter Democratic messaging on health care costs.

Why it matters:

President Trump and his allies have been increasingly assailing health plans over costs while seeking to deflect blame for blocking enhanced Affordable Care Act subsidies that help people afford premiums.

But the administration and Congress have less leverage than they have with drugmakers, and would have to address underlying drivers of health costs to really do something about premiums.

Driving the news:

House Republicans have called CEOs of five of the largest health insurance companies in back-to-back hearings on Thursday, where they will be pressed on costs of coverage.

Executives from UnitedHealth, CVS, Elevance, Cigna and Ascendiun will appear before the House Energy and Commerce and Ways and Means committees.

Energy and Commerce Chair Brett Guthrie (R-Ky.) said on Wednesday the companies cover over half of the insured lives in the U.S., “so everybody’s being affected by the high cost of health insurance.”

Between the lines:

It’s one thing to bash insurers, but quite another to match the talk with substantive health system changes.

“I think it’s interesting that they’re adopting some of the anti-insurer, populist rhetoric, but it needs to be backed up with actual policies that hold the health industry to account,” said Anthony Wright, executive director of consumer group Families USA.

He added that the hearing also should not be used to “distract” from the need to extend the ACA subsidies.

The other side:

Insurers agree that health care costs are too high, but say they’re the part of health care that’s working to bring costs down. Executives blame high premiums on the prices charged by hospitals and drug companies.

“Congress is doing its job,” Mike Tuffin, CEO of the insurer trade group AHIP, told Axios when asked about the pressure from Republicans.

But he added that “a thorough evaluation of the causes of higher premiums clearly demonstrates that it’s the underlying cost of medical care that is the reason that premiums continue to go up.”

What they’re saying:

Stephen Hemsley, CEO of UnitedHealth Group, will strike a note of contrition in his testimony, saying “like all of you, we are dissatisfied with the status quo in health care,” according to prepared remarks.

“The cost of health insurance is driven by the cost of health care,” he adds. “It is a symptom, not a cause.”

Still, Hemsley will say his company will rebate its profits this year from ACA coverage back to consumers, though he notes the company is a “relatively small participant” in that market. It’s unclear how much money will be rebated.

UnitedHealth became the object of widespread consumer anger just over a year ago, when the killing of CEO Brian Thompson unleashed a wave of social media-fueled rage over coverage denials and other business practices.

The big picture:

Insurers say they support a range of policies aimed at lowering health care costs by targeting hospitals and drug companies.

Those include “site-neutral” payment policies to address hospital outpatient billing, efforts to curb hospital consolidation and a crackdown on tactics drug companies use to delay cheaper generic competition.

But lawmakers have broached other changes that would directly strike health plans, like targeting what many experts say are overpayments in Medicare Advantage, or restricting pretreatment reviews that can lead to denials of care.

What’s next:

Trump earlier this month said he wanted a meeting with health insurance executives to press them on costs, but nothing is on the schedule and it’s unclear if that will happen.

Tuffin said he also expects future House hearings on health care costs with other parts of the health care industry besides insurers.

An Energy and Commerce Committee spokesperson confirmed there’s more to come but declined to provide details.

The bond market isn’t as responsive to Federal Reserve interest-rate policy as President Trump’s rhetoric might suggest. That makes the market a powerful check on the president.

We explore the tension — and what it means for this volatile week in geopolitics — below. 🏔

Plus, a dark horse to be the next Fed chair looks to be gaining ground. 🐎

Situational awareness:

The Commerce Department released shutdown-delayed data that showed solid growth in incomes and spending for October and November.

Consumption expenditures were up 0.5% both months (0.3% inflation-adjusted), pointing to steady underlying demand.

The Fed’s preferred inflation measure rose 0.2% both months, and in November was up 2.8% over the previous year.

Q3 GDP was revised slightly higher, to a 4.4% annual growth rate (from 4.3% previously), reflecting an upward adjustment to exports.

Trump really, really wantslower interest rates, and the Federal Reserve and other tools of state power have tried to deliver them. The bond market isn’t cooperating.

Why it matters:

Longer-term borrowing rates are set on global markets, as savvy players who together deploy trillions of dollars make bets on the future of growth and inflation.

In an era of vast power concentrated in the Oval Office, that makes it one of the few forces even Trump can’t control. It is a constraint on his actions that will not respond to insults or threats.

That, in turn, shows why the TACO trade — the bet that Trump Always Chickens Out when his rhetoric or actions start to ripple across global markets — has been in full force this week.

Driving the news:

Trump sees the Fed as the main mechanism to bring rates down. That was evident in his latest plea for lower rates, which he brought to the global stage yesterday in Davos, Switzerland.

“I’ll be announcing a new Fed chairman in the not-too-distant future. I think he’ll do a very good job,” Trump told a room of global CEOs and government leaders at the World Economic Forum.

“Problem is, they change once they get the job. You know they’re saying everything I want to hear and then they get the job … and all of a sudden, it’s ‘let’s raise rates a little.'”

Trump said he hopes his pick “does the right thing” with lowering rates. He later added that the U.S. should be paying “the lowest interest rate of any country in the world” on its debt “because without the United States, you don’t have a country.”

Reality check:

The Fed cut interest rates by a full percentage point in 2024 and another three-quarters of a percentage point in 2025. Yet longer-term borrowing costs are up in that time.

The day that rate-cutting began, Sept. 18, 2024, the 10-year U.S. Treasury yielded 3.7%. When the second wave of cutting began this past September, it was 4.06%.

This morning, the 10-year yield was 4.27%.

The rise in longer-term borrowing costs has happened for a mix of good reasons (higher growth prospects) and bad (higher inflation being priced in). But regardless, the swing shows the limit of the Fed’s ability to cater to the president’s wishes.

What they’re saying:

“The Fed doesn’t really set interest rates,” JPMorgan Chase CEO Jamie Dimon said in Davos.

“What happens if inflation goes up? They raise interest rates. What happens if inflation goes down? They reduce interest rates. They are a follower.”

Yes, but:

That doesn’t mean the president has no power over long-term interest rates. Tax and spending policy determines government deficits and, in turn, bond issuance and supply.

And this administration in particular has been creative in using the tools of government to try to encourage demand for longer-term securities, including directing Fannie Mae and Freddie Mac to buy hundreds of billions of dollars in mortgage bonds and tweaking regulations to encourage banks to hold more Treasuries.

Fed appointments also matter — though not necessarily in the way Trump emphasizes. A key to longer-term rates remaining low is investor confidence that the Fed will do what it takes to prevent inflation from taking off — even if that means rate increases in the near term.

Between the lines:

Last April, a bond market sell-off was a big factor in Trump backing away from “Liberation Day” tariffs.

This week’s threats of military force against Greenland and new tariffs on Europe — followed by backtracking — seemingly had echoes of that episode.

Treasury Secretary Scott Bessent, however, said on a podcast that “the bond market didn’t change the calculus” and that “President Trump always knew where he was going.”

Last week, J.P. Morgan hosted its 44th annual healthcare conference, with over 500 companies and 8,000 people in attendance to discuss health system performance, pharmaceutical trends, and new AI offerings.

Health systems outline current performance, future plans

According to STAT, many health systems took a measured tone at this year’s conference, focusing largely on stability and consistency, especially in the face of significant Medicaid funding cuts from the One Big Beautiful Bill Act.

“For me, it’s been about stabilizing,” said Kevin Smith, CFO of SSM Health. “Taking a look at the operations, doing a lot of blocking and tackling. Getting back to the basics.”

Separately, Paul Rathbun, outgoing CFO at AdventHealth, said that “[i]t all begins and ends with consistent financial performance.” He also emphasized sustainability and the importance of a solid foundation to handle future uncertainty.

As hospitals and health systems face financial challenges, many are focusing on boosting efficiency and reducing expenses. For example, Intermountain Health is focusing on optimizing its supply chain and simplifying healthcare with value-based arrangements.

Some health systems, like CommonSpirit Health, are planning to sell some facilities to help boost finances and expand ambulatory networks. Providence is also considering selling some of its assets, potentially including some hospitals.

“We have 51 hospitals, most of which have No. 1 market share in their communities, but we do have a handful that we may have to find a different purpose or different sponsors for,” said Providence CFO Greg Hoffman.

Other health systems, like Mass General Brigham and Hackensack Meridian, are aiming to expand their partnerships with other providers or outside organizations. Currently, Mass General Brigham has a new ambulatory care venture with Tampa General Hospital, and Hackensack Meridian is planning to add 20 new primary care clinics in New Jersey with Amazon One Medical.

Top CMS officials meet with hospital, insurance leaders

At the conference, CMS Administrator Mehmet Oz, along with four top members of his staff, hosted an event with hundreds of top hospital and health insurance leaders to discuss the Trump administration’s healthcare policies.

During the event, Oz downplayed the potential impact of upcoming Medicaid cuts, saying that they won’t be felt for at least a year and a half. “The catastrophizing over the idea that it’s going to rip the guts out of the system, I don’t think that’s fair,” he said.

CMS leaders also discussed efforts to combat fraud, the Trump administration’s focus on deregulation, recent vaccine changes, and more.

“The catastrophizing over the idea that it’s going to rip the guts out of the system, I don’t think that’s fair.”

According to David Joyner, CEO of Hill Physicians Medical Group, the general mood among attendees was skeptical and pessimistic, particularly about cuts to Medicaid and the impact of declining Affordable Care Act membership. At the same time, people were curious and optimistic about CMS’ potential to promote new innovation and technology that could address some of the healthcare industry’s most persistent challenges.

AI offerings continue to expand

AI was a large focus of the conference, with many organizations announcing new tools or collaborations.

At the conference, Anthropic announced Claude for Healthcare, a new AI model that includes HIPAA-ready infrastructure for enterprise customers, native integration to commonly used medical and scientific databases, and a model specifically trained for healthcare and life sciences tasks.

The new model follows Claude for Life Sciences, which was launched last October. Anthropic also announced new capabilities for life sciences, which ranged from preclinical research and development and regulatory affairs.

According to Eric Kauderer-Abrams, head of biology and life sciences at Anthropic, healthcare and life sciences are one of the company’s largest bets.

“Anthropic is a very natural fit for the healthcare and life sciences world because our identity as an AI company is built around safety and responsibility and rigor and reproducibility, and these are all the central tenants of the healthcare and life sciences industries,” Kauderer-Abrams said.

Currently, several healthcare organizations already use Anthropic’s Claude model, including Banner Health, Novo Nordisk, and AbbVie. At the conference, Elation Health announced that it integrated Claude into its EHR to create chart summaries and clinical insights.

Other AI companies at the conference also announced new expansion efforts. For example, Hippocratic AI, which develops patient-facing generative AI healthcare agent, said it acquired Grove AI, a startup that provides agentic AI for pharma research and development and clinical trial operations. According to Hippocratic, the acquisition will help it build its life sciences division and accelerate the use of generative and agentic AI in the biopharma and med tech sectors.

Separately, Open Evidence said it plans to move toward “medical super-intelligence” by building its AI platform on top of a group of specialist medical AI models (oncology, neurology, radiology, etc.) instead of a single centralized model.

Pharma companies discuss new products, drug pricing deals

According to Johnson & Johnson (J&J) CEO Joaquin Duato, 2026 should be a better financial year for the company as it focuses on three high-growth areas for its med tech business: cardiovascular, surgery, and vision. Currently, J&J has around a dozen upcoming product launches across its med tech and innovative medicine businesses, including its new Ottava Robotic Surgical System.

Separately, BioNTech, which is most known for developing a COVID-19 vaccine with Pfizer, is turning its attention to cancer treatment. The company has an $11 billion partnership with Bristol Myers Squibb for its bispecific PDL1-VEGF antibody.

Pharmaceutical leaders also discussed the “most favored nation” (MFN) deals they signed with the Trump administration to reduce the prices of certain prescription drugs.

Paul Hudson, CEO of Sanofi, said that while it may sound like everyone won with these deals, there were compromises from both sides.

“I would say the government got what it needed, and we worked very hard to make sure that we could still deliver what we think is an attractive investment thesis for the company without breaking stride,” Hudson said. “So it was a very difficult needle to thread. I don’t want to give the impression that there’s no impact from MFN, because the question for us is: Can we manage that and deliver an attractive long-range plan?”

Christopher Boerner, CEO of Bristol Myers Squibb, had a similar view. “I think what we did with the agreement we signed at the end of last year is find a way to balance the interest of the administration in ‘most-favored nation’ with, obviously, what’s best for the company, but importantly, how can we find ways to provide real value to patients?”

The digital health market ramps up

In 2025, digital health investments reached $14.2 billion in funding, a 35% increase from 2024 and the highest total since 2022. Last year, there were 26 megadeals, or those that raised over $100 million, and 15 new “unicorn” companies, or those valued at over $1 billion, up from just six in 2024.

Although the digital health market is still below its pandemic-era peak, there was significant growth in the market in 2025, largely driven by excitement around AI, according to analysts from Rock Health. The analysts also noted that there is a growing concentration of power in the digital health space, with certain companies having outsized influence.

“On one side, AI-native upstarts attracted huge rounds at unprecedented speed, a handful of companies broke the IPO drought, and private equity made major moves, signaling real bets on an emerging ‘winner’ class,” wrote Rock Health analysts Megan Zweig, Jacqueline Kimmell, and Maddie Knowles. However, on the other side, “… many companies are still grappling with valuation overhangs from prior cycles while operating in a more competitive market.”

Yesterday, the Centers for Medicare and Medicaid Services released the latest data on national health expenditures (NHE). The headline number, 7.2 percent growth in 2024, is concerning but hardly a surprise. It follows 7.4 percent growth in 2023. This rate of NHE growth is not sustainable. It exceeds general inflation and growth in the gross domestic product (GDP), pushing the share if GDP devoted to health care spending to 18 percent in 2024; the share of GDP devoted to health care is projected to rise to 20.3 percent by 2033. In fact, these figures may be an underestimate of the fiscal burden of the health care system because spending on some things, such as employer administrative costs, are not captured.

Government policies that shield employers, their workers, those seeking individual coverage and participants in public insurance programs from the financial burden of the health care system can mitigate access and affordability problems from the perspective of those groups. But shifting the financing burden from employers and individuals to taxpayers broadly does not solve the affordability problem and will exacerbate already challenging federal and state fiscal situations. Long term fiscal stability of the system requires addressing the underlying growth in spending, not simply who pays.

What Is Not Driving Spending Growth

Given all the attention to prices and insurer profits, it is important to note that those factors are not the main drivers of spending growth—this time, it’s not the prices, stupid. There was virtually no excess medical inflation (medical inflation above general inflation) for 2023 or 2024. In fact, prices for retail drugs (net of rebates) rose at a rate below inflation. There will certainly be cases of rising prices driving spending, but on average, price growth is not the problem. This does not mean high-priced products and services are not an important component of spending growth, but instead it implies that their contribution to spending growth on average stems from their greater use, not rising prices.

Similarly, non-medical spending by private health insurers, which includes profits, grew at 4.4 percent rate, which is below overall spending growth. As the study notes, the increased medical spending was unanticipated by many insurers, which led to reductions in nonmedical insurance expenditures, the subcategory that includes underwriting gains or losses and thus where profits (or surpluses in the case of non-profit insurers) are recorded.

What Is Driving Spending Growth

The main driver of spending growth is greater volume and intensity of care. Volume refers to the number of encounters (admissions, visits, etc.) and intensity refers to the mix of services (high-cost versus low-cost admissions, shifts from an inpatient to an outpatient setting or from an office to a hospital outpatient department, or the use of expensive vs less-expensive drugs). Most decompositions of health spending growth follow the national health accounts framework, focusing on the sector getting paid (hospital, physicians, retail drugs). This may mask some underlying dynamics related to mix that are important.

Coding Intensity

Payment for health care services is based on service codes and the coding system is dependent on coding patterns. Spending may rise if the care delivered is coded differently, even if the underlying delivery of care is unchanged. There is some evidence from recent years of an uptick in coding for sepsis, greater use of higher acuity evaluation and management codes and use of new Evaluation & Management codes.

The drivers of greater coding intensity are unclear. Coding concerns are not new, but new technologies enabled by artificial intelligence (AI) and ambient scribe technology may be accelerating the trend. Some of the coding may be accurate. But if payment rates are based on earlier coding patterns, the payment rates may not be appropriate. As a result, greater coding intensity increases spending and may add very little clinical value.

AI-Enabled Medical Services

Apart from the role of AI technology in supporting administrative activities such as coding, AI offers great potential to improve the value and efficiency of care. New AI-enabled services, particularly diagnostic services, can better direct care, eliminating unnecessary, potentially harmful, and costly services.

It stands to reason that such tools will lower spending, but realization of that promise depends on how AI services are priced and how providers respond. If the new services are paid for by fee for service, price will likely exceed marginal cost and use may grow beyond what would be optimal. (Because of the potential for quality improvement, the optimal level of use would be above the money-saving level.) Moreover, such tools may require use of other, potentially expensive diagnostic services. For example, AI tools that help diagnose heart disease may require CT-scans that would otherwise not occur. Finally, the productivity gains from AI may free up resources to deliver services that would otherwise not be used.

We are very early in the adoption of AI-based services into the health care system, and it is unlikely that such services contributed significantly to the 2024 spending trend. But going forward, monitoring and evaluating the impact of these services will be a first order concern.

Changes In Health Care Infrastructure, Provider Consolidation And Shifts In Patient Flows

The infrastructure of health care is constantly changing. New outpatient facilities (independent and system-affiliated) are opening and providers are consolidating. Private equity firms have a growing presence in the market. These developments may have important consequences for spending. The shift to lower price settings may lower spending, but integration of physician practices with health systems may raise it because, in general, systems are paid more. Expanding infrastructure may also lead to greater utilization of care. Shifts in patients towards higher-priced providers within sectors (e.g., from low-priced to high-priced hospitals) may also increase spending.

Much of the related policy attention has been focused on antitrust issues and private equity, both of which are important, but the impact of the evolving infrastructure and changing patient flows extends well beyond these issues and remains poorly understood. The key issue is the balance between, on the one hand, efficiency-generating shifts toward lower-priced or better-quality care and, on the other hand, inefficient shifts towards high-priced settings, higher-priced providers within settings, or potentially inappropriate use of services.

Use Of Expensive Products

A non-trivial, though likely not the dominant, driver of spending growth is the increased use of expensive products. Prescription drugs, both in the retail setting and those covered by the medical benefit, garner the most attention. GLP-1s, used to treat diabetes and obesity, are the sentinel example. Despite declines in prices, increased utilization drove up spending on these medications. Yet other products matter as well, including skin substitutes, whose use has skyrocketed. As with all products and services, though more saliently for expensive ones, the core policy questions involve limiting use to situations where the clinical benefit is sufficient to justify the cost (net of any offsets elsewhere) and restraining prices without unduly hampering innovation. Policies such as greater bundling of similar medications, reforming the Average Sales Price+ 6 percent payment policy for drugs under Medicare Part B. and ensuring value is a cap on price should be explored. CMS has been very active in this area, launching several new financing models, including the GLOBE model, the GUARD model and the Generous model, on top of very active implementation of Inflation Reduction Act policies related to drug pricing. Monitoring the impact of these demonstrations on prices, spending, access and innovation will be important.

Looking Forward

Health care spending growth continued at an unsustainable pace in 2024. Early reports suggest spending growth in 2025 will remain elevated. Such growth challenges policy makers and private payers alike.

Reactions often involve efforts to shift the financial burden to other stakeholders. For example, reductions in the federal share of Medicaid spending (the federal Medicare assistance percentage, or FMPAP) shift funding from the federal to state governments; decreases in marketplace subsidies shift some of the burden to individuals, as do employer increases in employee premium contributions. In some cases, shifting who pays may induce reductions in aggregate spending, but such decreases—for example in the case of reductions from higher out-of-pocket cost sharing—may result in lower use of high value services. Our ultimate goal should be to reduce spending in the least deleterious manner possible.

In that spirit, several options include:

Focusing on strategies to reduce low-value care and inappropriate coding in fee-for-service settings. The WISeR model and private utilization management programs seek to accomplish this goal. The devil is always in the details.

Improving designs of alternative payment models (APM) that create incentives for providers to practice efficiently. Benchmark-setting rules and risk adjustment are likely the greatest leverage points, but it is also important to consider APM programs holistically; Maintaining too many constantly evolving APM experiments will likely be counter-productive.

Regulating areas where markets fail. This may include price regulation (including Medicare fee schedule improvement), standardization to support choice, and simplification of administratively burdensome regulations (including broad revision of programs to improve quality). System simplification should be a guiding principle

Improving market mechanisms to induce more efficient care-seeking behavior and pricing, which may involve antitrust enforcement, providing better consumer information, improving choice support tools, and creating benefit packages based on the principles of value-based insurance design. But market mechanisms have limits and past efforts have not proven very successful. Thus, pursuit of more efficient markets should not forestall necessary regulation.

The specifics of these strategies will be central to establishing a fiscally sustainable health care system. But the spending growth we have experienced, and will experience in the future, reflect system design choices. Our ability to support access to high-quality care at a cost that is affordable in aggregate will require redoubled efforts to reform both health care financing and delivery.

As media attention focused on Minneapolis, Greenland and Venezuela last week, the Center for Medicaid and Medicare Services (CMS) released its 2024 Health Expenditures report Thursday: the headline was “Health care spending in the US reached $5.3 trillion and increased 7.2% in 2024, similar to growth of 7.4% in 2023, as increased demand for health care influenced this two-year trend. “

Less media attention was given two Labor Department reports released the Tuesday before:

Prices: The consumer-price index (CPI) for December came in somewhat higher than expected with an increase of 0.3% and 2.7% over the past 12 months. Overall inflation isn’t rising, but it also isn’t coming down.

Wages: The Labor Department reported average hourly earnings after inflation in the last year rose 0.7% during the first five months of this year, but real hourly earnings have declined 0.2% since May. They’re stuck.

Prices are increasing but wages for most hourly workers aren’t keeping pace. That’s why affordability is the top concern for voters.

Meanwhile, the health economy continues to grow—no surprise. It’s a concern to voters only to the extent it’s impacting their ability to pay their household bills. They don’t care or comprehend a health economy that’s complex and global; they care about their out-of-pocket obligations and surprise bills that could wipe them out.

As Michael Chernow, MedPAC chair and respected Harvard Health Policy professor wrote:

“The headline number, 7.2% growth in 2024, is concerning but hardly a surprise. It follows 7.4% growth in 2023. This rate of NHE growth is not sustainable. It exceeds general inflation and growth in the gross domestic product (GDP), pushing the share if GDP devoted to health care spending to 18% in 2024; the share of GDP devoted to health care is projected to rise to 20.3% by 2033. In fact, these figures may be an underestimate of the fiscal burden of the health care system because spending on some things, such as employer administrative costs, are not captured… Given all the attention to prices and insurer profits, it is important to note that those factors are not the main drivers of spending growth—this time, it’s not the prices, stupid. There was virtually no excess medical inflation (medical inflation above general inflation) for 2023 or 2024. In fact, prices for retail drugs (net of rebates) rose at a rate below inflation. There will certainly be cases of rising prices driving spending, but on average, price growth is not the problem. This does not mean high-priced products and services are not an important component of spending growth, but instead it implies that their contribution to spending growth on average stems from their greater use, not rising prices. The main driver of spending growth is greater volume and intensity of care…”

My take:

Since 2000 to 2024, total healthcare spending in the U.S. has been volatile:

2000–2007: High growth, typically 6–8% per year (driven by rising utilization and prices).

2008–2013: Growth slowed to 3–4% during and after the Great Recession.

2014–2016: Growth ticked up to 4.5–5.8% with ACA coverage expansion.

2017–2019: Moderation around 4.5%.

2020: COVID‑19 shock—growth slowed to ~2% due to deferred care.

2021: Rebound to ~4%.

2022: 4.8%, close to pre‑pandemic norms.

2023: 7.4%, fastest since 1991–92.

2024: 7.2%, reaching $5.3 trillion (18% of GDP)

Between 2000 and 2024, total health spending in the U.S. increased $3.9 trillion (279%) while the U.S. population grew by 58 million (20.4%). 2025 spending is expected to follow suit. The underlying reason for the disconnect between health spending and population growth is more complicated than placing blame on any one sector or trend: it’s true in the U.S. and every other developed system in the world. Healthcare is expensive and it’s costing more.

This is good news if you’ve made smart bets as an investor in the health industry but it’s problematic for just about everyone else including many in the industry who’ve benefited from its aversion to spending controls and cost cutting.

The current environment for the healthcare economy is increasingly hostile to the status quo. Voters think the system is wasteful, needlessly complicated and profitable. Lawmakers think it’s no man’s land for substantive change, defaulting to price transparency, increased competition and state regulation in response. Private employers, who’ve bear the brunt of the system’s ineffectiveness, are timid and reformers are impractical about the role of private capital in the health economy’s financing.

The healthcare economy will be an issue in Campaign 2026 not because aggregate spending increased 7-8% in 2025 per CMS, but because it’s no longer justifiable to a majority of Americans for whom it’s simply not affordable. Regrettably, as noted in Corporate Board Member’s director surveys, only one in five healthcare Boards is doing scenario planning with this possibility in mind.

Paul

P.S. The President released his Great Healthcare Plan last Thursday featuring his familiar themes—price transparency for hospitals and insurers, most favored pricing and elimination of PBMs to reduce prescription drug costs—along with health savings accounts for consumers in lieu of insurance subsidies. The 2-page White House release provided no additional details.

This week, 8000 healthcare operators and investors will head west to the 44th Annual JP Morgan Health Conference in San Francisco. Per JPM: “The (invitation-only) conference serves as a vital platform for networking, deal-making, and discussing the latest innovations in healthcare, attracting global industry leaders, emerging companies, and members of the investment community.” Daily media coverage will be provided by Modern Healthcare and STAT and most of the agenda will be at the St. Francis Hotel at Union Square.

General sessions about drug discovery, AI in healthcare obesity and more are scheduled, but that’s not why most make the trip.Representatives of the 500 presenting companies are there to engage with health investors in the tightly orchestrated speed-dating format JPM has fine-tuned through the years.

JPM circa 44 will be no different this year. It’s scheduled as company financials and market indicators for 2025 are coming in. Healthcare deal-flow was robust and bell-weather companies had a good year overall. The S&P, Dow and Nasdaq ended the year at all-time highs and investors appear poised to do more healthcare deals in 2026. Despite growing voter concern about affordability and their costs of living, there’s nothing on the immediate horizon that will dampen healthcare investor appetite for deals. That includes policy changes from the Trump administration that advantage healthcare companies that adapt to the administration’s playbook. It’s built on 3 fundamental assumptions:

The healthcare system is fundamentally flawed. Waste, fraud and abuse are deep-seeded in its SOP. It protects its own and resists accountability. The public wants change.

Fixing the health system requires policy changes that are attractive to the private companies that currently operate in the system. A federally-mandated regulatory framework (aka “the Affordable Care Act”) will cost more and be harmful. Companies, not Congress, are keys to system transformation.

Voters will support changes that make healthcare services more affordable and accessible. The means toward that end are less important.

What’s evolved from the administration’s first year in office is a mode of operating that’s predictable and uncomfortable to industries like healthcare:

It’s transactional, not ideologic. The administration believes its control of Congress, SCOTUS, the FTC and DOJ and legislatures in red states give it license to disrupt norms with impunity. Price transparency, limits on consolidation, mandated participation in ACOs, supply-chain disruption and AI-enabled workforce modernization are ripe for administrative action. A long-term vision for the system is not required to make needed short-term changes supported by its MAHA base.

It’s populism vs. corporatization. Healthcare’s proclivity for self-praise, addiction to “Best of…” recognition, celebrity CEOs and handsome executive compensation have postured it as “Big Business” in the eyes of most. Business practices associated with corporatization are fair game to the administration’s corrective agenda: hearings in the House Ways and Means and Energy and Commerce and Senate Health, Education, Labor and Pensions (HELP) committees will showcase the administration’s populist grievances. The administration will lavish advantages on private organizations that demonstrate support for its policies.

This week, the Senate will probably green-light a two-year extension of Tax Credits to temporarily avoid premium hikes. Barring a major escalation of tension abroad, attention will turn back to affordability where the K-economy is exacting its toll on lower-and-middle income households and widening despair among the young.

The health system’s role in making matters better or worse for consumers will be front and center alongside housing and costs of living. That context will be key to discussions between health investors and companies seeking their funds, though subordinate to term sheets.

In 2026, the Trump effect on dealmaking in healthcare will be significant.

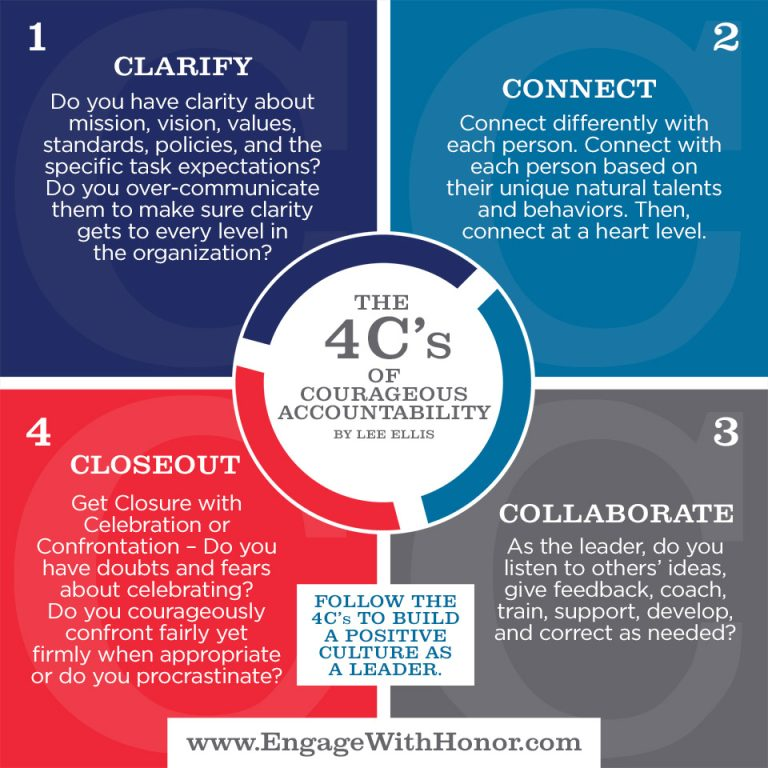

If you want a team that’s aligned and empowered, accountability is key. But not just any accountability—Courageous Accountability. We break it down into four simple steps:

Clarify expectations.

Connect with your people.

Collaborate through coaching.

Closeout with celebration or confrontation.

Great leadership takes courage. Which “C” are you focusing on this week?