Cartoon – Finding an Executive Position

Yesterday aboard Air Force One, President Trump was asked by a reporter if he supported Senators Bill Cassidy (R-LA) and Mike Crapo’s (R-IN) new health care proposal, which would authorize $1,500 deposits in Health Saving Accounts (HSAs) for lower-income individuals to replace the expiring Affordable Care Act (ACA) subsidies. The president’s response to the question was telling. And it shows just how much Big Insurance has fallen from grace in recent months.

For decades, merely expressing disenchantment with private health insurers could get you labeled as a socialist. Now we are seeing daily criticism of health insurance companies from people across the political spectrum, leading one to not know if a quote like “Americans are getting crushed by health insurance with monthly payments” is coming from a progressive, like AOC, or a conservative like MTG. (Hint: that quote was from MTG). Trump’s response was in the same vein and could lead one to believe there is a chance of the left and right finding common ground in holding insurance companies accountable for their greed.

Below we will dissect the president’s response and explain where he’s right and wrong.

This is true. Big Insurance has been ripping us off for years. And almost all of insurers’ growth in recent years has come from us as taxpayers. Most big insurers now make far more money on the lucrative Medicare Advantage business and managing state Medicaid programs than from their commercial health insurance plans. And they’ve even figured out how to bilk the VA. UnitedHealthcare, the biggest insurer, now gets more than 75% of its revenues from taxpayer-funded programs. And yes, insurers are getting hundreds of billions of dollars every year from the ACA subsidies that are at the center of debate in Washington.

Here are a couple of examples. Private health insurers took in over $500 billion in tax dollars to administer Medicaid in 2023. And this year alone, they will be overpaid – yes overpaid – $85 billion as a consequence of how they’ve rigged the Medicare Advantage program.

Insurers also take in massive amounts of money in the form of premiums that people pay thinking that money goes to care. Much of that money ends up going toward things (and people) that do nothing to get us well or keep us well. Since 2014, the seven largest insurers have made over $500 billion in profits, and they used $146 billion to buy back their own stock. So yes, Trump is correct, health insurance companies have been ripping people off for years.

No, Mr. President, the ACA is not a scam and most Americans now know that it has done a lot of good for a lot of people. Among other things, it made it possible for millions of people who previously had been blackballed by insurers because of a preexisting condition to finally get coverage. It brought us many long-overdue consumer protections, outlawed junk insurance, enabled young people to stay on their parents policies until they turned 26, alleviated job-lock through the creation of the ACA (Obamacare) marketplaces, and it made millions more low-income families eligible for Medicaid.

But, the president is right to say that Big Insurance has gotten rich since the passage of the ACA. Between 2014 (the year the entirety of the ACA was implemented) and 2024, just seven for-profit health insurers amassed $543.4 billion in profits and took in a staggering $10.192 trillion in revenues.

The president is kind of right. As KFF reports, the cost of a family policy has increased 60% since 2014 – a rate of increase much higher than general inflation and also higher than medical inflation. And as we’ve published previously, not only has the total cost of an employer-sponsored plan skyrocketed, so has the share of premiums workers must pay. This year, employers deducted an average of $6,850 from their workers’ paychecks for family coverage, up from $4,823 in 2014. And keep in mind, all that money our employers are having to send to insurance companies is not money that’s available to give raises to workers or hire more people.

The president is right. Several Big Insurance companies have ballooned in size over the past decade to become some of the world’s biggest corporate conglomerates. UnitedHealth Group, CVS/Aetna and Cigna are now numbers 3, 5 and 13 on the Fortune 500 list. The only American companies that take in more revenue than UnitedHealth are Walmart and Amazon.

The president has his history wrong here. While there are plenty of Monday-morning-quarterbacking you can do for the ACA – the law was not passed to “take care of insurance companies.” While the ACA didn’t fix everything – not by a long shot – it did stop some of the insurance industry’s worst abuses, like refusing to sell policies to people with preexisting conditions – even acne – and “rescinding” policies to avoid paying for life-saving care. Some insurers were found to be paying employees bonuses to find policies to rescind, including the policies of women almost immediately after being diagnosed with breast cancer.

It prohibited health insurers from charging people more because of a preexisting condition and from dumping the sick so they could reward their shareholders more generously. Keep in mind that insurers consider every claim they pay as a loss, hence the term “medical loss ratio” (MLR), which the ACA addressed by requiring insurers to spend at least 80%-85% of our premiums on our health care.

And it’s not like Big Insurance wanted the ACA to pass. Back in 2010, America’s Health Insurance Plans (AHIP), the PR and lobbying group for health insurers, quietly funneled $100 million to the U.S. Chamber of Commerce to orchestrate a PR, advertising and lobbying blitz to keep the ACA from being passed.

While big health insurance companies have only grown since the passage of the ACA, it has been Big Insurance’s corporate maneuvers and work on Capitol Hill (not the law itself) that has allowed these companies to flout some of the ACA’s regulations and bend the law to do their will.

While that is a compelling sound bite, it’s disingenuous. The money proposed by Cassidy and Crapo to go to HSAs would then be used by enrollees to buy insurance, thus still giving money to the insurance companies. Even worse, the proposed amount of money to go to people’s HSAs to help them pay for health insurance and care is $1,000-$1,500. This is money that would be used to purchase a bronze or copper plan with a high deductible (with many of those plans having deductibles north of $5,000). That means under this plan people would still need to come up with thousands to meet their deductible on top of paying their premiums every month. $1,000 wouldn’t come close to even covering the premiums for a decent policy, much less the out-of-pocket costs.

Replacing ACA subsidies with HSAs would still keep Americans tied to the same private health insurers that Trump calls “big, bad” and “money-sucking.” Most families would still be exposed to crippling medical bills, and even more tax dollars would flow to insurance conglomerates that own HSA custodian businesses (like UnitedHealth’s Optum Bank).

That’s wishful thinking far removed from reality. The health insurance plans available to people who get money for their HSAs under the Cassidy-Crapo proposal – rather than getting subsidies – are the same as those currently available. Worse, without the subsidies, people will not be able to afford the gold or silver plans that have lower out-of-pocket costs. In reality the plans that people buy under the proposed Cassidy-Crapo plan would have less value than the plans they previously bought with subsidies.

Trump’s comments are coming ahead of tomorrow’s scheduled vote in the Senate on dueling Democratic and Republican proposals to deal with the enhanced subsidies for ACA plans that will expire in three weeks. Without those subsidies, premiums will spike for many of the 24 million American enrolled in “Obamacare” plans. Democrats want to extend the subsidies for three years. Republicans, led by Senate Majority Leader John Thune, will push a plan replacing those subsidies with direct payments into individuals’ Health Savings Accounts (HSAs), as the president is suggesting. Neither plan is expected to get the 60 votes required for passage. What happens next is anybody’s guess.

Hospitals are closing unprofitable pediatric units and eliminating some surgical services for kids as they grapple with lower Medicaid reimbursements, staffing issues and more complicated cases, a 20-year review in the journal Pediatrics found.

Why it matters:

The cuts can erect additional hurdles to getting care in already underserved communities and require families to travel longer distances to regional or urban health centers.

What they found:

The review of nearly 4,000 facilities from 2003 to 2022 found the proportion of hospitals that researchers identified as having the lowest capabilities for pediatric care more than doubled.

The intrigue:

Hospitalizations for children fell 26% from 2000 to 2019, prompting more hospital operators to take pediatric inpatient units offline, with little incentive to bring them back.

Yes, but: The lack of pediatric inpatient beds doesn’t mean that a hospital will not admit a child on an adult ward.

The Senate will vote tomorrow on dueling health care plans: Democrats’ proposal to extend enhanced Affordable Care Act subsidies for three years, and a plan from two Republican chairmen that would instead give enrollees funds in health savings accounts.

Why it matters:

The move gives the GOP an alternative to point to if the ACA subsidies expire at the end of the year and health care costs spike for millions of people.

Driving the news:

The plan from Finance Committee chair Mike Crapo (R-Idaho) and health committee Chair Bill Cassidy (R-La.) wouldn’t extend the tax credits past their year-end expiration, instead providing $1,000 to $1,500 in health savings accounts to help certain marketplace enrollees with out-of-pocket costs.

Senate Majority Leader John Thune (S.D.) left open the possibility of talks after both votes fail on Thursday, though there is deep skepticism about the chances of reaching a bipartisan agreement.

Between the lines:

On the House side, GOP leadership, committee chairs and leaders of House GOP factions met yesterday to discuss health proposals, with an eye toward a possible House vote this year.

Over 17 million nonelderly Californians (55%) received health benefits through an employer in 2023. The California Health Benefits Survey (CHBS) tracks trends in these workers’ coverage, including premiums, employee premium contributions, cost sharing, offer rates, and employer benefit strategies. In 2025, the survey also included questions about provider networks, coverage for GLP-1 agonists, premium cost drivers, and employee concerns about utilization management. The CHBS is jointly sponsored by the California Health Care Foundation and KFF.

KEY FINDINGS INCLUDE:

Read the full report on the KFF website or download it below.

Key Takeaways:

Last week…

This week, Thanksgiving will likely slow down things on the U.S. domestic front but not for healthcare. Unlike just about every other industry in the economy, we operate 24/7/365. And like some industries, demand for our services is hard to predict– acts of God, accidents, court decisions, regulatory policy changes, social media “experts” et al. make predictions educated guesses at best. New technologies, clinical innovations, A.I. and private capital keep planners off-balance. Short-terms plans are more defensible; longer-term plans more challenging.

Thus, the industry is understandably focused on 2026. Here are assumptions:

And, reflecting on the current state of affairs in U.S. healthcare, here are 10 healthcare headlines you MIGHT see next year:

And, I’m confident, many others.

2026 is a mid-term election year. In 2016 (Trump 45 Year One), Republicans controlled 31 governorships and 68 legislative chambers. This January, the GOP will control 26 governorships and 57 legislative chambers– a 15% reduction on both. Politics is divided, affordability matters most to voters and healthcare is a high-profile target for campaigns so humility, thoughtful messaging backed by demonstrable actions will be an imperative for every healthcare organization.

2026 is a HUGE year for U.S. healthcare. The outcome is unknown.

As lawmakers debate ACA subsidy extensions and HSAs tied to banks and insurers, the public’s appetite for a health care overhaul is stronger than at any time since the 2020 Democratic primaries.

Washington is running out of hours to address the health care crisis of their own making. There are just 23 days before the Affordable Care Act’s (ACA) enhanced subsidies expire and congressional leaders are still trading barbs and floating half-baked ideas as millions of Americans brace for punishing premium spikes.

Meanwhile, the public has grown frustrated with both congressional dysfunction, and private health insurance companies that continue to raise premiums and out-of-pocket costs at a dizzying pace. According to new KFF data, 6 in 10 ACA enrollees already struggle to afford deductibles and co-pays, and most say they couldn’t absorb even a $300 annual increase without financial pain.

And even as Congress flails, Americans are coalescing around a solution party leaders rarely mention: Medicare for All.

After Senator Bernie Sanders bowed out of the presidential race in April 2020, Medicare for All faded to the background following political infighting, industry fearmongering and the lack of a national champion. But nearly six years later, the proposed policy solution has re-emerged as a top choice among frustrated voters.

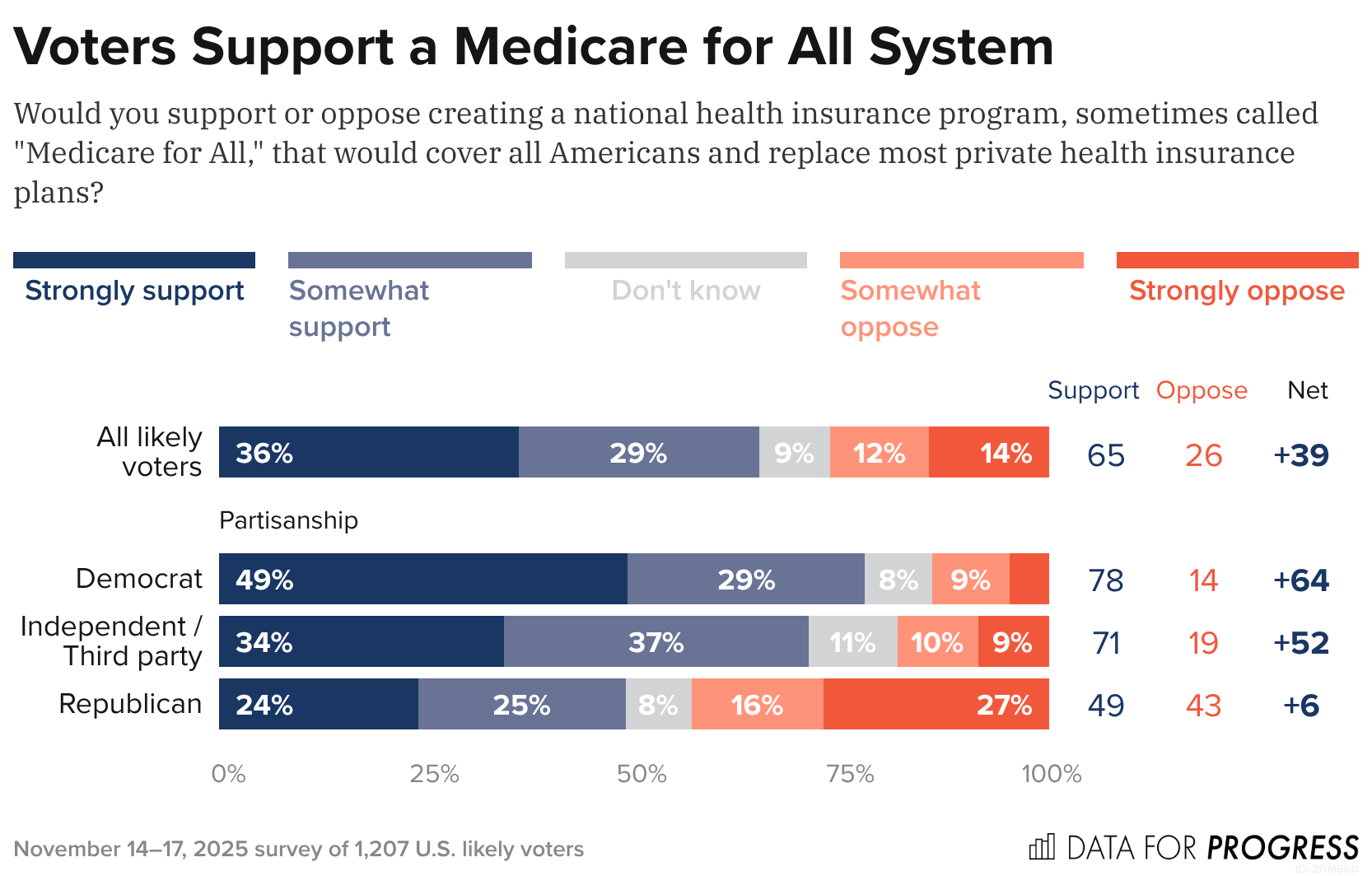

A new Data for Progress poll found that 65% of likely voters (including 71% of independents and nearly half of Republicans) support creating a national health insurance program that would replace most private plans. What’s notable is that the poll shows that support barely budges – holding at 63% – even when voters are told Medicare for All would eliminate private insurance and replace premiums with taxes, a dramatic shift from years past when just 13% supported such a plan under those conditions.

These new polls show that Americans are not simply dissatisfied with the looming subsidy crisis. But instead, as I wrote last month, they’re losing faith in the current system that allows Big Insurance to collect record profits at the expense of Americans’ health and bank accounts.

The KFF poll shows that ACA enrollees lack confidence that President Trump or congressional Republicans will handle the crisis, with almost half of ACA enrollees saying a $1,000 cost spike would “majorly impact” their vote in 2026. More than half of ACA enrollees are in Republican congressional districts, which explains why Republicans representing swing districts are desperately trying to persuade their Republican colleagues — so far without success — to extend the subsidies.

Of course, Medicare for All still faces steep odds in Congress. Industry opposition remains powerful, Democrats are divided and Republicans are openly hostile. But the polling shift is significant and suggests the political terrain is changing faster than Washington is acknowledging — and that voters, squeezed by soaring premiums and dwindling subsidies, are being nudged toward policies previously attacked as too ambitious to pass.

And against this backdrop, Medicare for All’s revival feels less like a left-wing wet dream and more like a window into the public’s thinning patience. Americans are looking past the Affordable Care Act’s limits and past Big Insurance’s promises – and towards a solution that decouples Americans health from profit-hungry, Wall Street-driven corporate monsters. While Washington has met this moment with inaction, Americans seem ready to act.

As we approach the end of 2025, it’s a good time to take stock of the US economy. There’s justifiable concern that this year has entrenched a K-shaped economy, where the have-mores leave the haves and have-nots behind. But there are more than two stories going on right now.

First, the vibes are bad (just ask anyone coming out of a grocery store). Second, the real economy—prices, jobs, and consumer and business spending, among other factors—is worse than it was a year ago, but holding up OK (4.4 percent unemployment, GDP growth over 2 percent, and inflation around 3 percent is hardly the stuff of recession). Third, a small number of people and companies are doing extremely well.

Depending on where you stand, you’re hearing very different things about the economy, but a pretty consistent theme is an administration that has not delivered on promises made to voters—while delivering to the president’s family and friends.

It’s been a predictably rough year for the US economy. Tariffs have raised goods prices and hit manufacturing jobs, immigration crackdowns have crippled the labor force, and reversing energy policies dramatically has unwound an energy investment boom. As a result, the job market is softer, prices are still high, and inflation is up and apparently rising based on the data flow that has (finally) started to trickle back in.

That said, if the data are weaker, the economic mood of the country is, in a word, awful. Consumer sentiment in October was only exceeded by lows from the worst of the early 1980s recession, the peak of the 2022 inflation, and the months following the “Liberation Day” tariff announcement this year. Since January, consumer sentiment has plunged, giving up essentially all gains from a steady rise after the inflation peak of 2022.

That pessimism isn’t purely emotional—it reflects months of higher grocery and utility bills. In fact, across both the major household expectations surveys, families expect inflation to keep going up next year—which most economists expect as well. And roughly twice as many consumers surveyed by the Conference Board expect the jobs picture to be weaker rather than stronger in the next six months.

This view is both pessimistic and realistic given the data we’ve seen so far this year. It’s unmistakably true that the labor market and the inflation picture are weaker than last fall. What’s worrying to the wonkier economy watchers, however, is that the pressures on both inflation and unemployment are in the wrong direction. There are real risks that both inflation and the jobs picture could get worse, but (short of policy reversals) few predictable shocks are likely to make either improve in the near term.

Job growth has stayed positive but slowed dramatically, from an average 167,000 jobs a month in January to just 109,000 in September (and will likely be revised down further with annual revisions early next year). Over 87 percent of all jobs added this year are in health care and social assistance (a given in an aging country), while the rest of the economy has added just 71,000 jobs all year. And there’s little sign that tariffs are about to bring down prices, nor are there signs that the demand side of the economy is about to pick up.

The closer you are to the data, the less pessimistic you probably are right now. But, as we can see in recent Fed meeting minutes, the debate is largely between two camps: The first is those who think the labor market is middling and the risks of rising inflation are serious. The second is those who think the risks of rising inflation are less worrisome than the chances the labor market deteriorates further.

It’s clearly too soon to panic about a recession, and the best labor market data we have say things are holding up well by historical standards—September’s 4.4 percent unemployment is better than about 80 percent of months since 2000—it’s just that there’s little to suggest things are about to improve significantly.

That said, the economy continues to chug along on the strength of spending by resilient, yet quite frustrated, consumers. The final reading on second quarter GDP shows US consumer spending keeping the economy going, even as savings deplete.

Early holiday spending numbers look strong, so it seems like US consumers are going to muddle through tariffs. The distribution of consumer spending remains pretty narrow—high earners are doing much more of the broad-based spending in the economy

However, if you get your news from stock markets, or even from retirement statements, the world is different entirely, and much more optimistic—at least from a high level. After a massive swoon in April, the US stock market has had a great year, powered by tax cuts for corporations and the wealthy and an AI investment boom that looks bubble-like to some inside it.

Yet, like in the real economy, the more you dig into the data the farther from the extremes your views can go. Job and corporate earnings growth are concentrated in increasingly narrow slices of the economy. Corporate earnings are notoriously concentrated at this point, with the top 1.4 percent of S&P 500 companies accounting for almost all of stock market gains this year—just seven companies are now one-third of the value of S&P 500.

Overall, the data are on a more even keel than either the awful vibes most Americans are feeling from an affordability crisis or the anxiously warm vibes of investors. We’re not living through the economic boom tech investors see everywhere, nor the near-term dystopia consumers are feeling. The economy is weaker than last year and likely to continue to soften a bit more over the first part of next year, but the good news is at least for now things are not as bad in the data as in the headlines. The bad news is . . . that’s the good news.