Cartoon – Preexisting Conditions

Republican efforts to alter the health law, left for dead in September, came roaring back to life this week as the Senate Finance Committee added a repeal of the “individual mandate” fines for not maintaining health insurance to their tax bill.

In this episode of “What the Health?” Julie Rovner of Kaiser Health News, Sarah Kliff of Vox.com, Joanne Kenen of Politico and Alice Ollstein of Talking Points Memo discuss the other health implications of the tax bill, as well as the current state of the Affordable Care Act.

Among the takeaways from this week’s podcast:

Plus, for “extra credit,” the panelists recommend their favorite health stories of the week they think you should read, too.

The Affordable Care Act has so far survived Republican attempts to replace it, but many people still face insurance concerns. Below, I answer three questions from readers.

Q: I have a rare disease, and there is literally only one specialist in my area with the expertise needed to treat me. I am self-employed and have to buy my own insurance. What do I do next year if there are zero insurance plans available that allow me to see my specialist? I cannot “break up” with my sub-specialty oncologist. I must be able to see the doctor that is literally saving my life and keeping me alive.

If the plan you pick covers out-of-network providers, you can continue to see your cancer specialist, although you’ll have to pay a higher percentage of the cost than if you were seeing someone in your plan’s network.

But many plans these days don’t provide any out-of-network coverage. This is certainly true of plans sold on the health insurance exchanges.

The situation you’re concerned about — that a specialist you consider crucial to your care isn’t in a plan’s provider network — isn’t uncommon, said Sabrina Corlette, a research professor at Georgetown University’s Center on Health Insurance Reforms.

If this happens, you can contact your plan and make the case that this particular provider is the only one who has the expertise to meet your needs. (Unfortunately, you probably can’t get this coverage assurance before you sign up.) Then ask your plan to make an exception and treat the out-of-network specialist as if she were in network for cost-sharing purposes. So, if in your plan an in-network specialist visit requires a $250 copayment, for example, the plan would agree that’s what you’d be charged to see your out-of-network specialist.

Or not. It’s up to the plan officials, and they may argue that someone in network has the expertise you need. If you disagree, you can appeal that decision.

But it may not come to that, said Corlette.

“Plans are prepared for this — the good ones are, anyway,” she said. “My understanding is that it’s pretty routine to grant exceptions for narrow subspecialties.”

Q: My company has asked employees to pay the Cadillac tax rather than putting the burden on the company. They are also telling us not to worry because it will never happen, but want us to agree that if it does we will take on the cost. Can they do that?

Let’s step back for a minute. The so-called Cadillac tax is a 40 percent surcharge on the value of health plans above the thresholds of $10,200 for single coverage and $27,500 for family plans.

A few months ago when it looked as if the ACA was going to be replaced, many employers believed, as yours apparently still does, that the Cadillac tax would never become effective. Both the House and Senate bills delayed the tax until 2026, and a lot can happen between now and then. With the collapse of efforts to repeal the ACA, however, the tax is on the front burner once again, said J.D. Piro, who leads the health and law group at benefits consultant Aon Hewitt. It’s set to take effect in 2020.

Under the law, insurers or employers would be responsible for paying the tax, but experts say the costs would likely be passed through to enrollees (whether or not you explicitly agree to absorb them). So it may not matter how you respond to your employer.

Also, employers who don’t want to pay the surcharge might sidestep the issue by reducing the value of the plans they offer, said Piro. For example, they could increase employee deductibles and other cost-sharing, make coverage less generous or shrink the provider network.

“That’s simplest way to avoid the tax,” he said.

Q: I need to purchase affordable health insurance for my two daughters who are 19 and 17. Is Trump insurance available yet? I need something I can afford and everything is so expensive.

President Donald Trump never put forward a proposal to replace the ACA. Instead, he backed the House and Senate replacement versions, which ultimately failed. But those versions might not have addressed your concerns, and you could have several options through the ACA.

“Coverage wouldn’t necessarily have been cheaper,” said Judith Solomon, vice president for health policy at the Center on Budget and Policy Priorities.

Under the Senate bill, for example, the nonpartisan Congressional Budget Office predicted that average 2018 premiums for single coverage would be 20 percent higher than this year’s. In 2020, however, premiums would be 30 percent lower than under current law, on average. But deductibles and other out-of-pocket costs would be higher for most people under the Senate bill, according to the CBO.

Premiums for young people would generally have declined. The bill would have allowed insurers to vary rates to a greater degree based on age, resulting in lower premiums for young people. In addition, premium tax credits generally would have increased for young people with incomes above 150 percent of the poverty level.

Your current coverage options under the ACA depend on your family situation. If you have coverage available to you through your employer, you can keep your daughters on your plan until they turn 26. For many parents, this is the most affordable, comprehensive option.

If that’s not a possibility, assuming the three of you live together and you claim them as dependents on your taxes, you may qualify for subsidized coverage on the health insurance marketplace next year. Your household income would need to be no more than 400 percent of the federal poverty level (about $82,000 for a family of three). You can apply for that coverage in the fall.

If you live in one of the 31 states plus the District of Columbia that have expanded Medicaid coverage to adults with incomes below 138 percent of the poverty level (about $28,000 for a family of three), you could qualify for that program. You don’t have to wait for open enrollment to sign up for Medicaid.

Don and Debra Clark of Springfield, Mo., are glad they have health insurance. Don is 56 and Debra is 58. The Clarks say they know the risk of an unexpected illness or medical event is rising as they age and they must have coverage.

Don is retired and Debra works part time a couple of days a week. As a result, along with about 20 million other Americans, they buy health insurance in the individual market — the one significantly altered by the Affordable Care Act (ACA).

But the Clarks are not happy at all with what they pay for their coverage — $1,400 a month for a plan with a $4,500 deductible. Nor are they looking forward to the ACA’s fifth open enrollment period, which runs from Wednesday through Dec. 15 in most states. Many insurers are raising premiums by double digits, in part because of the Trump administration’s decision to stop payments to insurers to cover the discounts they are required to give to some low-income customers to cover out-of-pocket costs.

“This has become a nightmare,” said Don Clark. “We are now spending about 30 percent of our income on health insurance and health care. We did not plan for that.”

Karen Steininger, 62, of Altoona, Iowa, said her ACA coverage not only gave her peace of mind but also helped her and her husband, who is now on Medicare, stay in business the past few years. But they too are concerned about rising costs and the effect of the president’s actions.

The Steiningers are self-employed owners of a pottery studio. Their income varies year to year. They now pay $245 a month for Karen’s subsidized coverage, which, like the Clarks’, has a $4,500 deductible. Without the government subsidy, the premium would be about $700 a month.

“What if we make more money and get less of a subsidy or just if the premiums increase a lot?” Karen Steininger asked. “That would be a burden. We’ll have to cut back on something or switch to cheaper coverage.”

The experiences of the Clarks and the Steiningers point to an emerging shortfall in the ACA’s promise of easier access to affordable health insurance for early retirees and the self-employed. Rising premiums and deductibles, recent actions by the Trump administration, and unceasing political fights over the law threaten those benefits for millions of older Americans.

“These folks are rightly the most worried and confused right now,” said Kevin Lucia, a health insurance specialist and research professor at Georgetown University’s Health Policy Institute in Washington, D.C. “Decisions about which health plan is best for them is more complicated for 2018, and many people feel more uncertain about the future of the law itself.”

At highest risk are couples like the Clarks who get no government subsidy (which comes in the form of an advanced tax credit) when they buy insurance. That subsidy is available to people earning up to 400 percent of the federal poverty level, or just under $65,000 for a couple. Their income is just above the amount that would have qualified them for a subsidy in 2017.

Premiums vary widely by state. Generally, a couple in their late 50s or early 60s with an annual income of $65,000 would pay from $1,200 to $3,000 a month for health insurance.

Premiums rose an average 22 percent nationwide in 2017 and are forecast to rise between 20 and 30 percent overall for 2018.

In an analysis released this week based on insurers’ rate submissions for 2018, the Kaiser Family Foundation found that individuals and families that don’t qualify for a subsidy but are choosing plans on the federal marketplace face premiums 17 to 35 percent higher next year, depending on the type of plan they choose. (Kaiser Health News is an editorially independent program of the foundation.)

A similar increase would be expected for people who also buy on the marketplaces run by some states or buy directly from a broker or insurance company.

The substantial premium increases two years in a row could lead fewer people to buy coverage.

“I’m really worried about this,” said Peter Lee, CEO of Covered California, the exchange entity in that state. “We could see a lot fewer people who don’t get subsidies enroll.” He said that California has taken steps to mitigate the impact for people who don’t get subsidies but that “consumers are very confused about what is happening and could just opt not to buy.”

There are already signs of that, according to an analysis for this article by the Commonwealth Fund. The percentage of 50- to 64-year-olds who were uninsured ticked up from 8 percent in 2015 to 10 percent in the first half of 2017. In 2013, the figure was 14 percent.

Indeed, the ACA has been a boon to people in this age group whether they get a subsidy or not. It barred insurers from excluding people with preexisting conditions — which occur more commonly in older people. And the law restricted insurers from charging 55- to 64-year-olds more than three times that of younger people, instead of five times more, as was common.

The law also provided much better access to health insurance for early retirees and the self-employed — reducing so-called “job lock” and offering coverage amid a precipitous decline in employer-sponsored retiree coverage that began in the late 1990s.

Only 1 in 4 companies with 200 or more workers offered any kind of coverage to early (pre-65) retirees in 2017 compared with 66 percent of firms in 1988, reported the Kaiser Family Foundation. And the vast majority of small firms never did offer such coverage.

Overall, before the ACA became law, 1 in 4 55- to 64-year-olds buying coverage on their own either couldn’t get it at all because of a preexisting condition or couldn’t afford it, according to AARP.

“The aging but pre-Medicare population was our major reason to support the ACA then and it still is now,” said David Certner, director of legislative policy at AARP. “This group benefited enormously from the law, and we think society and the economy benefited, too.”

Just how many 55- to 64-years-olds have been liberated from job lock by the ACA has yet to be fully assessed. But recent data show that 18 percent of people ages 55 to 64 who were still working in 2015 got coverage through the ACA marketplaces, up from 11.6 percent in 2013, according to an analysis for this article by the Employee Benefit Research Institute.

Also, a report released in January 2017 by the outgoing Obama administration found that 1 in 5 ACA marketplace enrollees of any age was a small-business owner or self-employed person.

A bipartisan effort is underway in Congress to provide dedicated funds to woo enrollees to healthcare.gov and help state agencies explain changes in the law for 2018 triggered by the Trump administration. But the fate of the proposed legislation is uncertain.

The Clarks said they’ll look carefully at options to keep their premiums affordable in 2018.

Said Don Clark, “If we get to a point where we have a $10,000 deductible and pay 40 percent or more of our income for health insurance, I’m not sure what we’ll do. We can’t afford that.”

This week, Senate Republicans announced that they plan to pay for their tax cuts for large corporations and millionaires not only by imposing tax increases on the middle-class but also by undermining people’s access to health care. Specifically, they have proposed eliminating the Affordable Care Act’s (ACA) individual mandate, which helps keep premium costs affordable by ensuring that both healthy and sick people have health insurance.

Repealing the mandate would drive up premiums by 10 percent in 2019 and lead to 13 million fewer people having health insurance by 2025. A Congressional Budget Office (CBO) report also revealed that the similar House version of the tax bill would result in $25 billion in cuts to Medicare in fiscal year 2018 and hundreds of billions of dollars of cuts to the program overall. Taken as a whole, the tax bill would not only increase taxes for millions of middle-class families but would also have disastrous effects on people’s health care.

The Senate tax bill would substantially increase premiums in the individual market for health insurance, and middle-class families would bear the brunt of the price hike. The bill would eliminate the individual mandate—the requirement that people maintain health coverage or pay a penalty. Without the mandate, people would only purchase coverage when they needed it, resulting in adverse selection that would drive up premiums. The CBO estimates that premiums would increase about 10 percent as a result of this adverse selection.

The Center for American Progress estimates that this premium increase translates to an extra $1,990 for benchmark plan coverage for an unsubsidized middle-class family of four. Families with incomes above 400 percent of the federal poverty level (FPL)—more than $98,400 for a family of four in the lower 48 states—are not eligible for premium tax creditsto reduce the cost of marketplace coverage. The 10 percent increase would be an even greater financial burden for families in states with higher premium levels, increasing costs by $2,900 in Alaska, $2,350 in Maine, and $2,060 in Arizona.

The CBO estimates that repeal of the mandate would result in 4 million fewer people having coverage in 2019 and 13 million fewer with coverage by 2025. As a result, about 16 percent of the nonelderly population would not have health insurance by 2025, compared with about 10 percent currently.

The individual mandate is necessary because of the consumer protections put in place by the ACA. The ACA banned discrimination by insurance companies against people with pre-existing conditions, required that people be charged the same amount regardless of health status, and eliminated annual and lifetime limits on coverage. But these protections would also make it easy for people to game the system by only buying health insurance once they needed it. To address this concern, the ACA coupled these reforms with an individual shared responsibility provision, also known as the individual mandate, which requires that everyone maintain health insurance coverage so that the overall insurance risk pool is healthy and premium rates are kept in check.

Repeal of the mandate would have two effects on the individual market. First, people who expect to be healthy would avoid purchasing coverage until they need it. As a result, the remaining enrollees in the individual market would be sicker on average, and insurance companies would need to raise rates to cover the increased average cost. Second, the resulting higher premiums would discourage additional people from purchasing coverage through the individual market. Those who become uninsured would no longer have financial protection against catastrophic medical costs, and hospitals and other providers would be forced to provide more uncompensated care.

In addition to its frontal assault on health care for the middle class, the Senate bill would also secretly cut Medicare. Because the tax cuts for the wealthy in the proposed bill are not fully paid for, they would increase the deficit by more than $1.4 trillion over 10 years. But the little-known Statutory Pay-As-You-Go Act of 2010 requires that any deficit-increasing legislation be offset with cuts to other mandatory programs, including Medicare. The CBO has estimated that the offsetting spending reductions for the similar House version of the tax bill would cut Medicare by about $25 billion in fiscal year 2018. Given that similar cuts would be required in subsequent years, the total cost imposed on the Medicare program would be hundreds of billions of dollars over the next decade. This would have a particularly harmful effect on rural hospitals with thin margins, which could be at risk of closure as a result.

Asking millions of middle-class families to pay more in taxes so that corporations and the wealthy few can pay less in bad enough. But to use those cuts to also undermine health care for middle-class families is unconscionable. Once again, the congressional majority seems to be doing everything in its power to make life harder for everyday Americans, just so it can provide giveaways to the wealthy few.

Our estimated reduction in coverage in 2025 due to repeal of the mandate is based on national projections by the CBO. The CBO estimates that 13 million fewer people will have coverage in 2025, including 5 million fewer people with Medicaid, 5 million fewer people with individual market coverage, and 3 million fewer people with employer-sponsored insurance. We used data from the 2016 American Community Survey Public Use Microdata Sample (ACS PUMS), available from the IPUMS-USA to tabulate the number of nonelderly people in each state by primary coverage type using a coverage hierarchy. We then assumed that each state’s reduction in coverage was proportional to its share of the national total for each of those three coverage types. For more on the IPUMS-USA data set, see Steven Ruggles and others, “Integrated Public Use Microdata Series: Version 5.0” (Minneapolis: Minnesota Population Center, 2010).

We made two adjustments to our ACS PUMS tabulations to account for potential effects of Medicaid expansion in Maine, given voters’ recent approval of expansion. We increased the number of Medicaid enrollees in Maine by 51,000 based on projections by the Urban Institute. We also decreased the number of people with coverage through Maine’s individual market by 20 percent to account for the fact that some enrollees will lose access to marketplace premium subsidies when they become Medicaid eligible under expansion. Enrollment data from the Centers for Medicare and Medicaid Services (CMS) show that 27 percent of 2017 marketplace plan selections were by people with family incomes between 100 and 150 percent of the federal poverty level.

Our estimates of 2019 premium increases are based on the CBO projection that mandate repeal will increase individual market premiums 10 percent. We used the HealthCare.govplan information to calculate the 2018 average marketplace benchmark—second-lowest cost silver—plan in each state, weighting by the geographic distribution of current marketplace enrollment. We then inflated that premium to 2019 levels according to National Health Expenditure projections for per-enrollee cost growth. To calculate the 2019 average benchmark premium specific to a typical family of four, we borrowed the example family composition that the U.S. Department of Health and Human Services uses in its reports: 40-year-old and 38-year-old parents and two children. We estimated that the family would pay an additional 10 percent of that 2019 benchmark due to mandate repeal. Premium data were not available for all states.

Finally, our estimates of state-level cuts to Medicare in fiscal year 2018 divided the $25 billion total Medicare funding reduction projected by the CBO proportional to each state’s share of national Medicare spending as of 2014, the most recent year for which CMS National Health Expenditure data is available, using data published by the Kaiser Family Foundation.

As the House prepares to vote Thursday on its tax reform bill, a new Kaiser Family Foundation poll finds almost three in 10 Americans (28%) view tax reform as a top priority for President Trump and Congress.

That’s significantly fewer than the share that say the same about reauthorizing funding for the Children’s Health Insurance Program (62%), hurricane recovery funding (61%), stabilizing the Affordable Care Act’s insurance marketplaces (48%) and addressing the prescription painkiller epidemic (43%). Two immigration-related issues – strengthening controls to limit who enters the country (35%) and passing legislation to allow the Dreamers to legally stay (34%) – also rank higher, while a similar share (29%) say repealing the Affordable Care Act is a top priority.

Among Republicans, half (51%) say reforming the tax code is a top Washington priority, behind strengthening immigration controls (69%) but similar to the share who consider hurricane recovery funding (52%), repealing the Affordable Care Act (50%), stabilizing the insurance marketplaces (46%) and reauthorizing CHIP funding (46%) to be top priorities.

In a tweet Monday, President Trump called on Congress to end the Affordable Care Act’s individual mandate, which requires most Americans to have health insurance or pay a tax penalty and has long been the least popular provision in the law. While the House tax reform bill does not currently address the mandate, key Republican senators said Tuesday that they will include such a provision in their version of the bill.

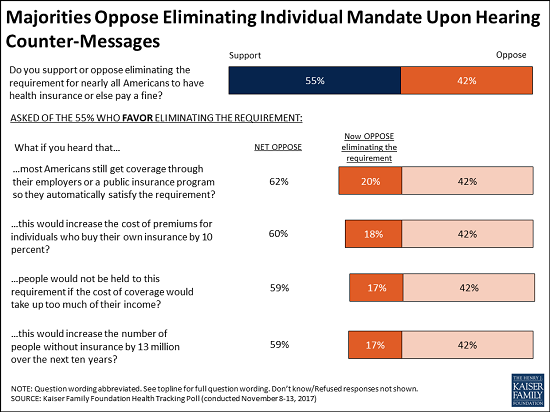

The new poll finds that most Americans (55%) initially support eliminating the mandate as part of tax reform, while four in 10 (42%) oppose it. Most Republicans (73%) and independents (58%) support ending the mandate, while most Democrats (59%) oppose it.

These views are malleable, with about a third of supporters (representing a fifth of the public overall) switching to oppose the mandate’s repeal when presented with facts and arguments about who is impacted and potential consequences of its repeal.

For example, the share who oppose eliminating the mandate can rise as high as 62 percent when initial supporters hear that most Americans get coverage through their employers or government programs that meets the mandate’s requirements. Similar majorities ultimately oppose eliminating the mandate when presented with other arguments against it, including that premiums for people who buy their own health insurance would go up, that people are exempted from the mandate if the cost of coverage takes up too much of their income and that getting rid of the mandate would result in 13 million more people being uninsured over the next 10 years, as the Congressional Budget Office has estimated.

One provision in the House bill would eliminate a tax deduction that allows people with high medical costs to deduct any medical and dental expenses that exceed 10 percent of their income. A majority (68%) of the public – including majorities of Democrats (77%), independents (66%), and Republicans (61%) oppose eliminating the tax deduction for individuals who have high health care costs.

More than four in 10 (44%) of the public think eliminating the deduction for high medical costs will affect them and their families, though in reality a much smaller share of the public uses that deduction in any given tax year. According to the Internal Revenue Service, about 17 percent of taxpayers who file itemized deductions use this deduction (approximately 6% of all taxpayers and 3% of the public).

Looking ahead to the 2018 midterm elections, the public is divided over whether not passing a tax reform plan or not repealing the ACA would be a bigger deal for President Trump and Republicans. Nearly half of the public say it will be a bigger problem if the president and Republicans are unable to pass their tax reform plan (47%), similar to the share who say it will be a bigger problem if they are unable to revive a repeal of the ACA (44%). Republicans are also divided, with similar shares saying it would be a bigger deal if President Trump and Republicans are unable to repeal the ACA (50%) and if they are unable to pass tax reform (45%).

Designed and analyzed by public opinion researchers at the Kaiser Family Foundation, the poll was conducted from November 8 – 13, 2017 among a nationally representative random digit dial telephone sample of 1,201 adults. Interviews were conducted in English and Spanish by landline (415) and cell phone (786). The margin of sampling error is plus or minus 3 percentage points for the full sample. For results based on subgroups, the margin of sampling error may be higher.

The Obamacare repeal debate is on again. Senate Republicans decided on Tuesday to include the elimination of the Affordable Care Act’s individual mandate in their tax plan, a risky move that would raise hundreds of billions of dollars to help pay for their desired tax cuts but is also sure to reignite intense clashes over health care coverage. Here’s a quick look at this latest twist in the tax reform effort:

Why They’re Doing It: Repealing the mandate, which requires individuals to buy health insurance or pay a penalty, helps solve the difficult math problems Senate tax-writers faced. The Senate tax bill can add up to $1.5 trillion to the debt over 10 years, and it can’t add to the deficit after that period. President Trump and some Senate Republicans had urged that the mandate repeal be included in the tax plan since it saves a projected $338 billion over 10 years, according to the Congressional Budget Office.

“Repealing the mandate pays for more tax cuts for working families and protects them from being fined by the IRS for not being able to afford insurance that Obamacare made unaffordable in the first place,” Sen. Tom Cotton (R-AR), who had proposed the move, said after the decision was announced. And if the repeal passes as part of a tax cut package, Trump and congressional Republicans would deliver on two promises to voters in one bill.

What It Means: Repealing the mandate may help Republicans chalk up a big win on taxes, but it also comes at a cost. The move raises revenue because it would lead to 13 million fewer people having health insurance, according to the CBO, and thus reduces the amount the government must shell out for insurance subsidies and care. Analysts also warn that, without the mandate, premiums will rise and some insurers might not participate in Obamacare markets that require them to cover pre-existing conditions. “Eliminating the individual mandate by itself likely will result in a significant increase in premiums, which would in turn substantially increase the number of uninsured Americans,” a coalition of insurers, hospitals and doctors wrote in a letter to congressional leaders on Tuesday.

Those expected effects carry significant political risk. For one thing, it could reawaken the liberal base that mobilized so effectively against Obamacare repeal and turn their focus to the tax bill. Michael Linden, a liberal policy expert, tweeted that “Reducing the corporate tax rate to 23% instead of 20% generates the SAME savings as repealing the ACA mandate. They could cut taxes for corporates just a little less, but instead they’re cutting health care.” Democratic leaders are already slamming the decision. “Republicans just can’t help themselves,” Sen. Chuck Schumer said. “They’re so determined to provide tax giveaways to the rich that they’re willing to raise premiums on millions of middle-class Americans and kick 13 million people off their health care.”

Will It Pass? A “skinny” Obamacare repeal bill that would have eliminated the individual mandate failed in the Senate in July when Republican Sens. John McCain, Lisa Murkowski and Susan Collins voted against it. But Senate Majority Leader Mitch McConnell told reporters that including the repeal provision would make it easier for the tax bill to pass. As part of the deal, the Senate would also reportedly vote on another bill to restore federal payments to insurers that the president had halted last month. Sen. John Thune (R-SD) said that a whip count had been done and expressed confidence that Republicans had the 50 votes they need.

On Friday, HHS released a proposed rule that would make a number of adjustments to the rules governing insurance exchanges for 2019. The rule is long and detailed; there’s a lot to digest. Among the most noteworthy changes, however, are those relating to the essential health benefits. They’re significant, and I’m not convinced they’re legal.

By way of background, the ACA requires all health plans in the individual and small-group markets to cover a baseline roster of services, including services falling into ten broad categories (e.g., maternity care, prescription drugs, mental health services). Taken as a whole, the essential health benefits must be “equal to the scope of benefits provided under a typical employer plan, as determined by the Secretary.”

The ACA’s drafters anticipated that HHS would establish a national, uniform slate of essential health benefits. Instead, the Obama administration opted to allow the states to select a “benchmark plan” from among existing plans in the small group market (or from plans for state employees). The benefits covered under the benchmark were then considered “essential” within the state.

At the time, Helen Levy and I concluded that HHS’s approach brushed up against the limits of what the law allowed. We noted, among other things, that the ACA tells HHS to establish the essential health benefits—not the states. And it’s black-letter administrative law that an agency can’t subdelegate its powers to outside entities, states included.

At the end of the day, however, Helen and I concluded that the Obama-era regulation passed muster. Our rationale bears repeating:

Although a federal agency cannot delegate its powers to the states, it “may turn to an outside entity for advice and policy recommendations, provided the agency makes the final decisions itself.” Here, the secretary gave the states a constrained set of options (e.g., choose a benchmark plan from among the three largest small-group plans in the state) and retained the authority to select a benchmark for any state that either does not pick a benchmark or chooses an inappropriate one. As such, the secretary remains firmly in control. Nothing in the ACA prevents her from deferring to states that select benchmark plans from among the few options she has provided. That choice to defer is itself an exercise of her delegated powers.

The Trump administration’s proposed rule would vastly enlarge this Obama-era subdelegation. For starters, the rule would allow a state to adopt another state’s benchmark, or part of a state’s benchmark, as its own. Michigan, for example, could borrow Alabama’s benchmark plan wholesale, or it could incorporate Alabama’s benchmark for mental health and substance use disorder treatment. More significantly, the rule would allow a state to “selec[t] a set of benefits that would become the State’s EHB-benchmark plan.”

You read that right: if the rule is adopted, each state can pick whatever essential health benefits it likes. No longer will it be choosing from a preselected menu; it’ll be picking the essential benefits out of a hat. In so doing, the proposed rule looks like it would unlawfully cede to the states the power to establish the essential benefits.

This extraordinary subdelegation of regulatory authority is subject only to the loosest of constraints: benefits can’t be “unduly weighted” toward any one benefit category or another, and the benchmark must “[p]rovide benefits for diverse segments of the population, including women, children, persons with disabilities, and other groups.” The selected benefits also can’t be more generous than the state’s 2017 benchmark (or any of the plans the state could have selected as its benchmark), but that’s a ceiling, not a floor, so states have lots of room to pare back.

The only meaningful constraint is that the benefits covered by the state’s benchmark must be “equal to the scope of benefits provided under a typical employer plan.” But another portion of the proposed rule would hollow out that requirement:

[W]e propose to define a typical employer plan as an employer plan within a product (as these terms are defined in §144.103 of this subchapter) with substantial enrollment in the product of at least 5,000 enrollees sold in the small group or large group market, in one or more States, or a self-insured group health plan with substantial enrollment of at least 5,000 enrollees in one or more States.

In other words, HHS is saying it will treat as “typical” any employer plan, in any state, that covers more than 5,000 people.

This looks like an innocuous change. It’s not. If the rule is adopted, it means that a single outlier plan can now count as typical, even if it’s way stingier than any other plan in the market. It also makes me wonder if HHS already has in mind some large employer with an unusually narrow health plan—maybe some hospital-based “administrative services only” plan, as Dave Anderson speculates. If so, voilá, the states can all ratchet down their essential benefits to that plan’s level.

I don’t think that’s legal. To know if a slate of health benefits is typical, you have to know something about how many health plans cover those benefits and how many don’t. The proposed rule eschews that comparative inquiry, and instead defines typicality with reference to the number of people who are covered by a single plan. Some random self-insured plan that excludes appendectomies could be treated as typical, even if it’s the only plan in the nation that does so.

In other words, HHS wants to define a “typical employer plan” to include atypical plans—which the agency emphatically cannot do. Yes, plans that enroll 5,000+ people are less likely to be outliers than smaller ones. But in a country as big and complicated as ours, there are bound to be some idiosyncratic quirks even in large plans. Those quirks would all be considered typical under HHS’s rule.

This definitional change, combined with the choose-your-own-adventure option to devise a benchmark, means that states will have wide authority to water down the essential health benefits requirement. Whether that’s good or bad is hard to say. Requiring plans to cover lots of services assures comprehensive coverage, but it also raises the cost of insurance. Because there’s no single “best” way to strike the balance, I think there’s a lot to be said for giving states the freedom to choose for themselves.

Wise or not, however, I’m skeptical that the Trump administration’s effort to hollow out the rule governing essential health benefits is legal. If HHS presses ahead with the rule, it could face tough sledding in the courts.

President Trump on Wednesday suggested using the GOP tax bill to repeal ObamaCare’s individual mandate.

“Wouldn’t it be great to Repeal the very unfair and unpopular Individual Mandate in ObamaCare and use those savings for further Tax Cuts,” Trump tweeted.

The idea is being pushed by Sen. Tom Cotton (R-Ark.) and also has the backing of House Freedom Caucus Chairman Mark Meadows (R-N.C.).

Meadows said Wednesday he supports repealing the mandate in tax reform and thinks “ultimately” it will be included because he is going to push for it. He said he has been talking to Cotton about it.

A Cotton spokeswoman told The Hill that Cotton and Trump spoke by phone about the idea over the weekend and “the President indicated his strong support.”

Senate Finance Committee Chairman Orrin Hatch (R-Utah) this week said that he wouldn’t rule out including repeal of the mandate in the tax legislation.

But other top Republicans have rejected the idea, including House Ways and Means Committee Chairman Kevin Brady (R-Texas), Senate Majority Whip John Cornyn (R-Texas) and Sen. John Thune (R-S.D.). They fear adding the ObamaCare change would jeopardize tax reform.

“Look, I want to see that individual mandate repealed,” Brady said during an interview with radio host Hugh Hewitt on Tuesday. “I just haven’t seen, no one has seen, 50 votes in the Senate to do it.”

Brady added that he would be open to adding a repeal of the mandate to the House bill if the Senate passed it first.

Asked Wednesday about the president’s tweet, Senate Majority Whip John Cornyn (R-Texas) threw cold water on the idea.

“I think tax reform is complicated enough without adding another layer of complexity,” Cornyn told The Hill.

Thune, meanwhile, said mandate repeal is “not currently a part of our deliberations.”

But Thune added that some members have expressed interest in the idea and said he was “somewhat” interested in it because of the revenue implications.

Sen. Mike Rounds (R-S.D.) on Tuesday also dismissed adding a repeal of the mandate to tax reform.

“If there was a way to do it, I’d be open to it, but I’m not going to pitch it because I want to focus on taxes in the tax reduction plan,” Rounds told reporters.

The Congressional Budget Office has estimated that repealing the mandate would save the government $416 billion over a decade.

The mandate requires people, with some exceptions, to pay a fine to the IRS if they do not have health insurance.

Experts have said repealing the mandate would result in massive premium spikes and a major increase in the number of uninsured people.

It could also send ObamaCare exchanges into a “death spiral” because it would discourage healthy younger individuals to sign up for insurance.

The CMS proposed a rule late Friday aimed at giving states more flexibility in stabilizing the Affordable Care Act exchanges and in interpreting the law’s essential health benefits as a way to lower the cost of individual and small group health plans.

In the 365-page proposed rule issued late Friday, the agency said the purpose is to give states more flexibility and reduce burdens on stakeholders in order to stabilize the individual and small-group insurance markets and improve healthcare affordability.

The CMS said the rule would give states greater flexibility in defining the ACA’s minimum essential benefits to increase affordability of coverage. States would play a larger role in the certification of qualified health plans offered on the federal insurance exchange. And they would have more leeway in setting medical loss ratios for individual-market plans.

“Consumers who have specific health needs may be impacted by the proposed policy,” the agency said. “In the individual and small group markets, depending on the selection made by the state in which the consumer lives, consumers with less comprehensive plans may no longer have coverage for certain services. In other states, again depending on state choices, consumers may gain coverage for some services.”

However, the CMS acknowledged it’s unclear how much money the new state flexibility will save. States are not required to make any changes under the policy.

The CMS urged states to consider the so-called spillover effects if they choose to pick their own benefits. These include increased use of other services, such as increased used of emergency services or increased use of public services provided by the state or other government entities.

The agency in 2017 proposed standardized health plan options as a way to simplify shopping for consumers on the federally run marketplaces. The CMS said it would eliminate standardized options for 2019 to maximize innovation. “We believe that encouraging innovation is especially important now, given the stresses faced by the individual market,” the proposed rule states.

The CMS proposes to let states relax the ACA requirement that at least 80% of premium revenue received by individual-market plans be spent on members’ medical care. It said states would be allowed to lower the 80% medical loss ratio standard if they demonstrate that a lower MLR could help stabilize their individual insurance market.

The CMS also said it intended to consider proposals in future rulemaking that would help cut prescription drug costs and promote drug price transparency.

The Trump administration hopes to relax the ACA’s requirements and provide as much state flexibility as possible through administrative action, following the collapse of congressional Republican efforts this year to make those changes legislatively.

The proposed rule comes after months of calls from health insurers and provider groups for the federal administration to help stabilize the struggling individual insurance market. The fifth ACA open enrollment is slated to begin Nov. 1, and experts have predicted fewer sign-ups in the wake of a series of actions by the Trump administration to undercut the exchanges.

In the proposed rule, the CMS also proposes to exempt student health insurance from rate reviews for policies beginning on or after Jan. 1, 2019. The CMS said student health insurance coverage is written and sold more like group coverage, which is already exempt from rate review, and said the change would reduce regulatory burden on states and insurance companies.

The ACA requires that insurers planning to increase premiums by 10% or more submit their rates to regulators for review. The CMS proposed to increase the rate review threshold to 15% “in recognition of significant rate increases in the past number of years.”

The rule also tweaks a requirement that enrollees need to have prior coverage before attempting to get coverage via special enrollment after moving to a new area. Under the proposal, a person who lived in an area with no exchange qualified health plans will be able to obtain coverage.