Cartoon- Leadership Struggle Looming

American Medical Association President Jack Resneck Jr., MD, detailed in a post on the medical group’s website the “Kafkaesque” prior authorization process that an unnamed insurance company allegedly put one of his patients through.

Dr. Resneck, a San Francisco-based dermatologist, was treating a patient with severe head-to-toe eczema, who was unable to sleep because of the condition, according to the post. Dr. Resneck found a medication that allowed the patient to sleep and return to work.

Several months later, however, the patient was unable to get the prescription refilled at the pharmacy, according to the report. Dr. Resneck completed the paperwork describing how well the patient had responded to the medication, as required by the insurance company, and faxed it over. The prior authorization request for the prescription refill was rejected.

Dr. Resneck said the insurance company rejected the refill on the grounds that the patient no longer met the severity criteria because not enough of his body was covered and he was not missing enough sleep.

The insurance company allegedly wanted to take the patient off the medication for several weeks to let his eczema flare up again, according to the post. It took more than 20 additional telephone calls until the patient’s prescription was refilled.

https://www.beckerspayer.com/payer/5-questions-medicare-advantage-data-doesnt-answer.html

A lack of data about Medicare Advantage plans means there are several unanswered questions about the program, according to an analysis from Kaiser Family Foundation.

The analysis, published April 25, breaks down the kinds of Medicare Advantage data not publicly available. Some missing data is not collected from insurers by CMS, and some data is collected by the agency but not available to the public.

Here are five questions researchers can’t answer without more data, according to Kaiser Family Foundation:

Twenty U.S. hospitals have received consecutive “A” safety grades from The Leapfrog Group since 2012, according to the group’s spring safety grades released May 3.

Since 2012, Leapfrog has assigned letter grades to nearly 3,000 acute-care general hospitals across the nation every fall and spring. The safety grades evaluate hospitals’ performance on up to 22 patient safety measures from CMS, the Leapfrog Hospital survey and other supplemental sources. The safety grades are the only hospital ratings program solely based on hospitals’ ability to protect patients from preventable errors, accidents, injuries and infections.

Twenty hospitals have received 23 consecutive “A” grades since the launch.

Last fall, 22 hospitals achieved consecutive “A” grades. For the spring grades, two hospitals lost their consecutive “A” streak: Sentara Williamsburg Regional Medical Center in Virginia and Sierra Vista Regional Medical Center in San Luis Obispo, Calif., both earned a “B.”

Read more about Leapfrog’s hospital safety grade methodology here.

Here are the 20 hospitals that have achieved 23 consecutive “A” grades:

Arizona

Mayo Clinic Hospital (Phoenix)

California

French Hospital Medical Center (San Luis Obispo)

Kaiser Permanente Orange County-Anaheim Medical Center

Colorado

Rose Medical Center (Denver)

Florida

AdventHealth Daytona Beach

Illinois

Elmhurst Memorial Hospital

University of Chicago Medical Center

Northwestern Medicine Central DuPage Hospital (Winfield)

Massachusetts

Beverly Hospital

Saint Anne’s Hospital (Fall River)

Michigan

University of Michigan Health (Ann Arbor)

Mississippi

Baptist Memorial Hospital Golden Triangle (Columbus)

North Carolina

Rex Hospital (Raleigh)

Ohio

OhioHealth Dublin Methodist Hospital

OhioHealth Grady Memorial Hospital (Delaware)

Texas

St. David’s Medical Center (Austin)

Virginia

Inova Loudoun Hospital (Leesburg)

Sentara CarePlex Hospital (Hampton)

Sentara Leigh Hospital (Norfolk)

Washington

Virginia Mason Medical Center (Seattle)

Franklin, Tenn.-based CHS, which reported a net loss of $20 million in the first quarter on revenues of $3.1 billion, is on the hunt for new acquisitions just as it is also in discussions to sell off more assets.

“We are considering further opportunities to expand our portfolio,” CEO Tim Hingtgen said in a webcast discussing first-quarter results.

Selling off certain assets would also help balance the system and further reduce some of its debt, President and CFO Kevin Hammons confirmed on the call.

“Moreover, we may give consideration to divesting certain additional hospitals and non-hospital businesses,” CHS said in an SEC filing. “Generally, these hospitals and non-hospital businesses are not in one of our strategically beneficial services areas, are less complementary to our business strategy and/or have lower operating margins. In addition, we continue to receive interest from potential acquirers for certain of our hospitals and non-hospital businesses.”

The health system, which operates 79 hospitals in 15 states, has agreed to sell four more hospitals effective Jan. 1, the filing stated.

CHS recently completed the $92 million sale of Oak Hill, W.Va.-base Plateau Medical Center to Charleston, W.Va.-based Vandalia Health. It also finalized on Jan. 3 an $85 million sale of its former 122-bed facility in Ronceverte, W.Va, also to Vandalia Health.

CHS shares were trading at $6.24 before its results were released. It is currently trading at approximately $3.70.

Here are 15 major hospital and healthcare merger and acquisition-related transactions from April:

Embattled insurtech Bright Health will fully ax its insurance business as a potential bankruptcy looms, the company announced Friday.

The company secured an extension to its credit facility through June 30, giving it a few extra months to avoid going belly-up. To ensure it qualifies for the extension, the company must find a buyer for its California-based Medicare Advantage (MA) business by the end of May, according to a filing with the Securities and Exchange Commission.

Bright Health revealed March 1 that it had overdrawn its credit and would need to secure $300 million by the end of April to stay afloat.

The MA business includes nearly 125,000 California seniors across its Brand New Day and Central Health Plan brands. In the announcement, Bright said the sale would “substantially bolster” its finances.

“Since our founding, Bright Health has worked to make healthcare simpler, more personal and affordable for consumers,” CEO Mike Mikan said in the announcement. “As our markets evolve, we are taking steps to adapt and ensure our businesses are best positioned for long-term success.”

In late 2022, the company announced that it would exit the Affordable Care Act’s (ACA’s) exchanges and slashed its reach in MA down to just California and Florida as its financial challenges mounted. It later cut the Florida plans as well.

Manny Kadre, lead independent director of Bright Health’s board of directors, said in the announcement that the company has “received inbound interest” about the California MA business as it explores its options.

With the full divestiture of its insurance business, that means Bright Health will be all-in on its NeueHealth care delivery services. Mikan said in the announcement that the segment performed well in the first quarter and has grown to serve about 375,000 value-based care customers.

As Bright shops for a buyer for its MA plans, it’s also continuing to unwind the ACA business, a process that hit a snag as it was hit with a lawsuit from Oklahoma-based health system SSM Health, which alleged that the insurer owed it more than $13 million in unpaid claims.

Bright Health is also under the gun to boost its stock price, as the New York Stock Exchange has threatened to delist its shares. Shares in the company were trading at 17 cents on Friday afternoon.

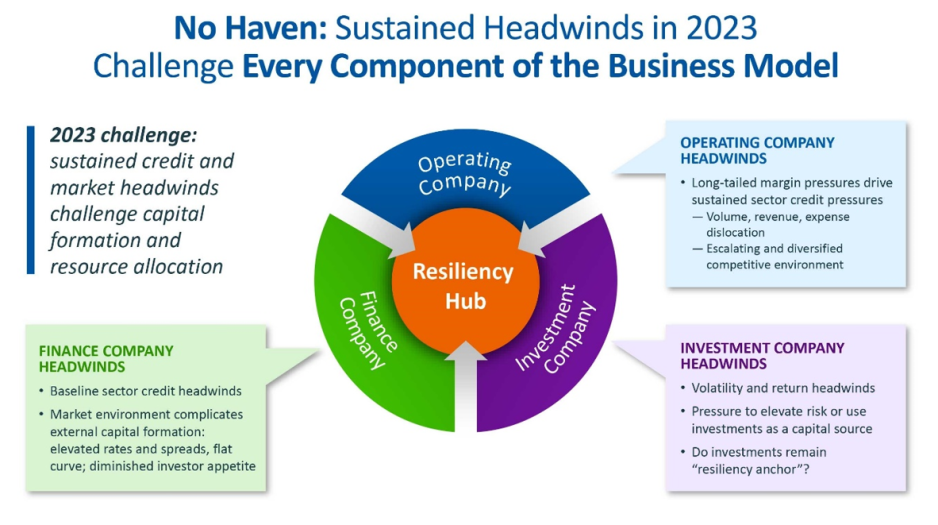

For the first time in recent history, we saw all three

functions of the not-for-profit healthcare system’s

financial structure suffer significant and sustained

dislocation over the course of the year 2022

(Figure above).

The headwinds disrupting these functions

are carrying over into 2023, and it is uncertain how

long they will continue to erode the operating and

financial performance of not-for-profit hospitals

and health systems.

The Operating Function is challenged by elevated

expenses, uncertain recovery of service volumes, and

an escalating and diversified competitive environment.

The Finance Function is challenged by a more

difficult credit environment (all three rating agencies

now have a negative perspective on the not-forprofit healthcare sector), rising rates for debt, and

a diminished investor appetite for new healthcare

debt issuance. Total healthcare debt issuance in

2022 was $28 billion, down sharply from a trailing

two-year average of $46 billion.

The Investment Function is challenged by volatility and

heightened risk in markets concerned with the Federal

Reserve’s tightening of monetary policy and the

prospect of a recession. The S&P 500—a major stock

index—was down almost 20% in 2022. Investments

had served as a “resiliency anchor” during the first

two years of the pandemic; their ability to continue

to serve that function is now in question.

A significant factor in Operating Function challenges is

labor: both increases in the cost of labor and staffing

shortages that are forcing many organizations to

run at less than full capacity. In Kaufman Hall’s 2022

State of Healthcare Performance Improvement Survey, for

example, 67% of respondents had seen year-over-year

increases of more than 10% for clinical staff wages,

and 66% reported that they had run their facilities at

less-than-full capacity because of staffing shortages.

These are long-term challenges,

dependent in part on

increasing the pipeline of new talent entering healthcare

professions, and they will not be quickly resolved.

Recovery of returns from the Investment Function

is similarly uncertain. Ideally, not-for-profit health

systems can maintain a one-way flow of funds into

the Investment Function, continuing to build the

basis that generates returns. Organizations must now

contemplate flows in the other direction to access

funds needed to cover operating losses, which in

many cases would involve selling invested assets at a

loss in a down market and reducing the basis available

to generate returns when markets recover.

The current situation demonstrates why financial

reserves are so important:

many not-for-profit

hospitals and health systems will have to rely on

them to cover losses until they can reach a point

where operations and markets have stabilized, or

they have been able to adjust their business to a

new, lower margin environment. As noted above,

relief funding and the MAAP program helped bolster

financial reserves after the initial shock of the

pandemic. As the impact of relief funding wanes

and organizations repay remaining balances under

the MAAP program, Days Cash on Hand has begun

to shrink, and the need to cover operating losses is

hastening this decline. From its highest

point in 2021, Days Cash on Hand had decreased, as

of September 2022, by:

29% at the 75th percentile, declining from 302 to 216

DCOH (a drop of 86 days)

28% at the 50th percentile, declining from 202 to 147

DCOH (a drop of 55 days)

49% at the 25th percentile, declining from 67 to 34

DCOH (a drop of 33 days)

Financial reserves are playing the role

for which they were intended; the only

question is whether enough not-for-profit

hospitals and health systems have built

sufficient reserves to carry them through

what is likely to be a protracted period of

recovery from the pandemic.

KEY TAKEAWAYS

All three functions of the not-for-profit healthcare

system’s financial structure—operations, finance,

and investments—suffered significant and

sustained dislocation over the course of 2022.

These headwinds will continue to challenge not-forprofit

hospitals and health systems well into 2023.

Days Cash on Hand is showing a steady decline, as

the impact of relief funding recedes and the need

to cover operating losses persists.

Financial reserves are playing a critical role in

covering operating losses as hospitals and health

systems struggle to stabilize their operational and

financial performance.

Conclusion

Not-for-profit hospitals and health systems serve

many community needs. They provide patients

access to healthcare when and where they need it.

They invest in new technologies and treatments that

offer patients and their families lifesaving advances

in care. They offer career opportunities to a broad

range of highly skilled professionals, supporting the

economic health of the communities they serve.

These services and investments are expensive and

cannot be covered solely by the revenue received

from providing care to patients.

Strong financial reserves are the foundation of good

financial stewardship for not-for-profit hospitals and

health systems.

Financial reserves help fund needed

investments in facilities and technology, improve an

organization’s debt capacity, enable better access to

capital at more affordable interest rates, and provide a

critical resource to meet expenses when organizations

need to bridge periods of operational disruption or

financial distress.

Many hospitals and health systems today are relying

on the strength of their reserves to navigate a difficult

environment; without these reserves, they would

not be able to meet their expenses and would be at

risk of closure.

Financial reserves, in other words,

are serving the very purpose for which they are

intended—ensuring that hospitals and health systems

can continue to serve their communities in the face of

challenging operational and financial headwinds.

When these headwinds have subsided, rebuilding these

reserves should be a top priority to ensure that our

not-for-profit hospitals and health systems can remain

a vital resource for the communities they serve.

For large capital projects—construction of a new cancer

treatment center, for example, or replacement of an

aging facility—issuance of municipal debt is one of the

most affordable ways for not-for-profit hospitals and

health system to finance the project.

The affordability of that debt is, however, partly contingent on the

organization’s ability to maintain a strong credit rating,

and financial reserves—again measured as Days Cash on

Hand—are a significant component of that credit rating.

There are two basic forms of municipal debt:

General obligation bonds are backed by the full

taxing power of the issuing municipal authority and

are considered relatively low risk. Hospitals that are

owned by a city or county can be funded by general

obligation bonds, although there are practical

limitations on their ability to issue these bonds,

including in many instances the need to obtain voter

or county commissioner approval. Organizations

without municipal ownership—including most

not-for-profit hospitals and health systems—

cannot issue general obligation bonds.

Revenue-backed municipal bonds are backed by

the ability of the organization borrowing the debt

to meet its obligation to make principal and interest

payments through the revenue it generates over the

life of the bond. Because revenues can be disrupted

by any range of factors, revenue-backed bonds are

higher risk for investors. Most healthcare bonds

are revenue-backed municipal bonds.

When determining whether to invest in revenue-backed

municipal healthcare bonds, investors will look to the

credit rating of the hospital or health system that is

borrowing the debt. Credit ratings—issued by one or

more of the three major credit rating agencies (Fitch

Ratings, Moody’s Investors Service, and S&P Global

Ratings)—provide an assessment of the probability

that the hospital or health system will be able to meet

the terms of the debt obligation. These ratings are

tiered. A credit rating in the AA tier is better than a credit

rating in the A tier, which is better than a rating in the

BBB tier. Ratings below the BBB tier are considered sub-investment grade.

Organizations with a sub-investment

grade rating can still access various forms of debt,

but the amount of debt they can access generally will

be lower, the cost of the debt will be higher, and the

covenants that lenders require will be more stringent

than for investment-grade rated organizations.

Financial reserves and credit ratings

Days Cash on Hand is one of the most important factors

credit rating agencies use because it is an indicator

of how long the rated organization could withstand

serious disruption to its operations and cashflow.

The rating agencies issue median values for the various

metrics they use to determine credit ratings. Median

values for Days Cash on Hand increased significantly

across most rating categories for all three agencies

in 2020 and 2021; this reflects the temporary inflow

of pandemic relief funding through, for example,

the Coronavirus Aid, Relief, and Economic Security

(CARES) Act.

We anticipate these medians will move

closer to pre-pandemic levels as relief funds are

exhausted and hospitals repay remaining balances

on Medicare’s COVID-19 Accelerated and Advanced

Payment (MAAP) program funds. But even before

the pandemic, organizations in 2019 had a median

Days Cash on Hand of 276 to 289 days at the AA level,

173 to 219 days at the A level, and 140 to 163 days at

the BBB level.

In other words, the Days Cash on Hand

benchmark for organizations seeking to maintain an

investment-grade rating would be well over 100 Days

Cash on Hand, and well over 200 Days Cash on Hand for

organizations seeking to achieve a higher rating level.

Again, these reserves are proportionate to the operating

expenses of the individual hospital or health system.

Impact of credit ratings on access to capital

Organizations that can achieve a higher rating can

also borrow money at more affordable interest

rates. Figure 3 shows average interest rates for

municipal bonds across a range of maturities as of

mid-December 2022 (maturity is the term in years

for repayment of the bond at the time the bond is

issued). Lower-risk general obligation municipal bonds

are shown as the baseline, with lines for AA, A, and

BBB rated healthcare revenue-backed bonds above

it. As a reminder, most hospitals and health systems

cannot borrow money using general obligation bonds;

instead, they use higher-risk revenue-backed bonds.

Because revenue-backed bonds are a higher risk for

investors than tax-based general obligation bonds,

even hospitals and health systems with a strong

AA credit rating will pay a higher interest rate than

would a city or county that could back repayment of

the bond with tax revenues (see the line for AA rated

Healthcare Revenue Bonds compared to the line

for AAA rated General Obligation bonds). But there

is also a significant gap between the interest rate a

hospital with an AA credit rating would pay compared

to the interest rate available to a hospital with a lower

BBB rating. Here, the difference is approximately

three-fourths of a full percentage point. When the

amount borrowed for a major new hospital project

can run into the hundreds of millions of dollars,

that difference represents significant savings for

organizations with a higher credit rating.

Financial reserves and debt capacity

Financial reserves and the funds they generate—

including investment income—also help define an

organization’s debt capacity: essentially, the amount of

debt an organization can assume without jeopardizing

its current credit rating. There are two key ratios here:

The first is total unrestricted cash and investments

to debt. In general, the more favorable that ratio is,

the more latitude a hospital or health system has to

take on additional debt, especially if the organization

is toward the middle to top end of its rating tier.

The second is the debt service coverage ratio,

which measures the organization’s ability to

make principal and interest payments with funds

derived from both operating and non-operating

(e.g., investment income) activity. A higher ratio

here means the organization has more funds

available to service debt.

The ability to assume additional debt is an important

safety valve if, for example, an organization needs to

mitigate poor financial performance to fund ongoing

capital needs or strategic initiatives.

KEY TAKEAWAYS

Not-for-profit hospitals and health systems often

borrow debt through revenue-backed municipal

bonds, meaning that the debt obligations will be

met by the revenue the organization generates

over the life of the bond.

Because revenue-backed bonds are higher

risk than general obligation bonds backed by a

municipality’s taxing authority (revenues can

be disrupted), investors seek assurance that an

organization will be able to meet its obligations.

Credit ratings offer investors an assessment of

an organization’s current and near-term ability to

meet these obligations.

Days Cash on Hand is an important metric in

assessing the organization’s credit rating, and a

higher rating generally requires a higher number of

Days Cash on Hand.

A higher credit rating allows organizations to

borrow money at more affordable interest rates.

A higher level of financial reserves and investment

income in relation to existing debt obligations also

increases an organization’s debt capacity, creating

an important safety valve if an organization has

to borrow money to mitigate poor operating or

investment performance.