More Americans are dying at home than in hospitals for the first time in more than a half century, according to a new study in the New England Journal of Medicine.

Why it matters: “Americans have long said that they prefer to die at home, not in an institutional setting. Many are horrified by the prospect of expiring under florescent lights, hooked to ventilators, feeding tubes and other devices that only prolong the inevitable,” NYT writes.

By the numbers: In 2017, 29.8% of deaths by natural causes occurred in hospitals, and 30.7% were in people’s homes.

Centene, the nation’s largest Medicaid managed care provider, wants Congress to change the eligibility requirements around Medicaid, the government-sponsored safety net program that covers one in five low-income Americans.

Its proposal would ultimately push more people onto the Affordable Care Act exchanges by allowing states to adopt a partial Medicaid expansion, an idea typically embraced by red states.

CEO Michael Neidorff told Healthcare Dive the company has been quietly talking to lawmakers on both sides of the aisle on Capitol Hill about the plan, though he emphasized nothing of substance will happen until after the 2020 election.

Centene says its proposal is an attempt to strengthen the ACA markets by increasing the pool of people while enticing holdout states to partially expand their Medicaid programs.

“I think there’s a way to get it done,” Neidorff told Healthcare Dive. “We have a very powerful Washington office and they’ve been working with leadership and their staff.”

Centene filed lobbying forms totaling about $2 million in spending in the congressional lobbying database for 2019, as of Dec. 11. In 2018, the payer reported spending roughly $2.5 million.

However, policy experts caution that it would result in increased spending for the federal government and fewer protections for those enrolled in Medicaid who are then pushed into the exchanges.

It’s unclear how receptive Congress will be, but experts were skeptical of any consensus on the polarizing health law.

“It would be a very major change. I certainly don’t see that happening. It’s opening up the ACA and as we know from past history, it’s a battle royale when you go into the ACA,”Joan Alker, executive director and co-founder of the Center for Children and Families at Georgetown University, told Healthcare Dive.

Centene’s proposal

Under the ACA, states can expand their Medicaid programs to cover all adults whose annual incomes does not exceed 138% of the federal poverty level, or $17,236 for an individual.

Centene’s proposal calls for lowering that income ceiling from 138% to 100%, or $12,490 for an individual.

That would shrink the pool of who is eligible for Medicaid and push those people into the exchanges. Neidorff said the move would grow the exchange pool and ultimately drive down prices. High costs haveattracted criticism as they play a role in forcing those who are not subsidized to leave the market.

Credit: Samantha Liss/Healthcare Dive

For Centene, it would be a notable shift because its core business has long been in Medicaid. The insurance exchanges only became a viable business beginning in 2013 with the advent of the ACA. It’s a nod to how important the exchange business has become for the payer.

Centene arguably stands to benefit the most as the nation’s largest insurer on the exchanges in terms of enrollment, plus the exchanges generate higher profit margins than its Medicaid book of business.

“You move those lives into exchange and your profitability is higher,” David Windley, an analyst with Jefferies, told Healthcare Dive.

In the states that have not expanded Medicaid, there are about 2 million people with incomes between 100% and 138% of the federal poverty level, according to the Kaiser Family Foundation.

Hospitals and providers are likely to favor the proposal because Medicaid plans tend to pay less than commercial ones. The idea could garner support from states with tight budgets as some, even Massachusetts, have already expressed a desire to adopt a partial expansion. (Both the Trump and Obama’s administrations have denied providing the enhanced match rate for states seeking partial expansions).

Who benefits the most?

Still, there are potential drawbacks, according to analysts and policy experts. For example, the plan could potentially cost taxpayers more if there is a greater shift to the exchanges away from Medicaid coverage.

“Medicaid is broadly accepted as the cheapest coverage vehicle in the country,” Windley said, noting that the exchanges are typically a more expensive insurance product than Medicaid coverage.

Plus, because of the way the ACA was written, the federal government would be forced to pick up the entire tab of the subsidies for those between 100% and 138% of FPL.

“As a result, the states save money for every beneficiary whom they can move from Medicaid into their exchanges,” according to a previous paper in the New England Journal of Medicine.

However, policy experts warn the proposal may not be in the best interest of Medicaid members who would migrate to the exchanges.

These members are better off with Medicaid, Alker said.

“From a beneficiary perspective it’s problematic because there are no premiums in Medicaid for that group, 100-138 [FPL]. The cost sharing is very limited,” she said.

Plus, there are benefits in Medicaid members would no longer have access to if they move to the exchanges, Adrianna McIntyre, a health policy researcher at Harvard University, told Healthcare Dive, including non-emergency transportation and retroactive eligibility.

Centene argues many states have avoided expanding Medicaid because of cost concerns, which then leaves some residents without access to affordable care, particularly those in the coverage gap, or those with incomes below 100% of FPL.

If a partial option convinces some holdout states to expand “that’s a tradeoff some may be willing to make,” McIntyre said.

Some states that did expand are looking for ways to curb costs and have decided to implement work requirements, Neidorff noted. He believes the proposal is the answer to both these problems for states.

Centene’s plan comes as a slate of Democratic presidential contenders are calling for “Medicare for All,” a single-payer or public-option healthcare system.

Not surprisingly as such a plan would at a minimum sideline private plans and at the extreme eliminate private payers, Neidorff dismissed the idea.

He estimates his plan would cost $6 billion a year, which he characterized as “very affordable” when compared to a Medicare for All plan, which some studies estimate could cost as much as $32 trillion over 10 years.

Still, some policy experts say the change being proposed by Centene is a tall order.

Though the changes may seem small, the consequences of adopting a partial expansion are large, researchers wrote in a NEJM report: “The damage to Medicaid beneficiaries, the exchange population, and the federal budget could be serious.”

Legislative proposals could reduce bad debt, but would likely introduce additional complexity to billing processes.

Changes in insurance benefit design that shift greater financial responsibility to the patient, rising healthcare costs and confusing medical bills will continue to drive growth in bad debt — often faster than net patient revenue, according to a new report from Moody’s.

Legislative proposals to simplify billing have the potential to reduce bad debt, but the downside for hospitals is that they’ll likely introduce additional complexity to billing processes and complicate relationships with contracted physician groups. A recent accounting change will reduce transparency around reporting bad debt.

Higher cost sharing and rising deductibles are the main contributors to the trend of patients assuming greater financial responsibility, a trend that’s been occurring for more than a decade, and that will further increase the amount of uncollected payments. Hospitals and providers are responsible for collecting copays and deductibles from patients, which may not always be possible at the time of service; the longer the delay between providing service and collecting payment, the less likely a hospital is to collect payment.

On top of that, the higher an individual’s deductible is, the greater the share of reimbursement that a hospital has to collect. The prevalence of general deductibles increased to 85% of covered workers in 2018, up from 55% in 2006, and the amount of the annual deductible almost tripled in that time to an average of $1,573.

Multiple factors are driving the trend toward higher cost sharing, including a desire among employees and employers for stable premium growth despite steadily rising healthcare costs and the growing popularity of high deductible health plans.

WHAT’S THE IMPACT

Hospitals face an uphill battle when it comes to reducing bad debt. Strategies include point-of-service collections, enhanced technology to better estimate a patient’s responsibility for a medical bill, and offering low-cost financing or payment plans.

A common feature of these approaches is educating patients about what portion of a medical bill is their responsibility, after taking into account the specifics of their insurance plan. But hospitals often find it hard to provide reliable cost estimates for a given service, which can thwart efforts to provide patients with an accurate estimate of their financial responsibility.

One difficulty is that medical bills partly depend on the complexity of service and amount of resources consumed — which may not be known ahead of time. There’s also the need to incorporate specific benefits of the patient’s own insurance plan. A certain amount of bad debt is likely to arise from patients accessing emergency care given the insufficient time to determine insurance coverage.

Another difficulty in billing is surprise medical bills, received by insured patients who inadvertently receive care from providers outside their insurance networks, usually in emergency situations. While the term “surprise medical bills” refers to a specific, narrow slice of healthcare costs, they have become part of the broader debate about the affordability and accessibility of U.S. healthcare.

THE LARGER TREND

To minimize surprise bills, Congress is considering proposals to essentially “bundle” all of the services a patient receives in an emergency room into a single bill. Under a bundled billing approach, the hospital would negotiate a set charges for a single or “bundled” episode of care in the emergency room. The hospital would then allocate payments to the providers involved.

This approach, which major hospital and physician trade groups oppose, has the potential to significantly affect hospitals and disrupt the business models of physician staffing companies, according to Moody’s. Many hospitals outsource the operations and billing of their emergency rooms or other departments to staffing companies. Bundling services would require a change in the contractual relationship between hospitals and staffing companies.

Another recent proposal in Congress would require in-network hospitals to guarantee that all providers operating at their facilities are also in network. This approach adds significant complexity because many physicians and ancillary service providers are not employed or controlled by the hospitals where they work. Some hospitals would likely seek to employ more physicians, leading to increases in salaries, benefits and wages expense.

Americans are putting off medical treatment in record numbers because of cost, Gallup data shows

One quarter of American adults say they or a family member has put off treatment for a serious medical condition because of cost, according to data released this week by Gallup. That number is the highest it’s been in nearly three decades of Gallup polling.

An additional 8 percent have made the same choice for less serious ailments, the survey showed. That means a collective 33 percent of those polled have prioritized financial considerations over their health, tying the high set in 2014.

The report also shows a growing income gap in cost-related delays. In 2016, for instance, one-fourth of U.S. households earning less than $40,000 a year reported cost-related delays, vs. 13 percent for households making more than $100,000. In 2019, the rate of cost-related delays among poorer households shot up to 36 percent, while the rate for the richer group remained at 13 percent.

Gallup cautions that the Trump presidency may be influencing these numbers on a partisan level: From 2018 to 2019, the share of Democrats reporting cost-related delays for serious conditions jumped from 22 percent to 34 percent. Among Republicans, the year-over-year increase was more subdued, from 12 percent to 15 percent.

Gallup data also show Democrats (31 percent) self-report higher rates of preexisting conditions than Republicans (22 percent).

“Whether these gaps are indicative of real differences in the severity of medical and financial problems faced by Democrats compared with Republicans or Democrats’ greater propensity to perceive problems in these areas isn’t entirely clear,” according to Gallup’s Lydia Saad. “But it’s notable that the partisan gap on putting off care for serious medical treatment is currently the widest it’s been in two decades.”

Data from the Kaiser Family Foundation’s Employer Health Survey underscores the severity of the health-care spending problem. In 2019, 82 percent of covered workers must meet a deductible before health-care coverage kicks in, up from 63 percent a decade ago. “The average single deductible now stands at $1,655 for workers who have one,” according to KFF, “similar to last year’s $1,573 average but up sharply from the $826 average of a decade ago.”

Deductibles have surged 162 percent since 2009, data show — more than six times the 26 percent climb in earnings over the same period.

Physician pay is another significant expense. The Commonwealth Fund, a health-care research group, estimates American doctors earn “nearly double the average salary” of doctors in other wealthy nations. The American Medical Association, a trade group representing doctors, has a long history of opposing efforts to implement European-style single-payer health-care systems in the United States.

The American health-care system, in other words, works pretty well for the powerful players in the health-care industry. Hospitals and insurance companies are reaping significant profits. Doctors are earning high salaries. But what are the rest of us getting in return for our ever-growing co-pays and deductibles?

The disparities domestically are perhaps even more shocking: In the nation’s wealthiest places, where the high cost of modern health care remains within relatively easy reach, life expectancies are literally decades longer than in America’s poorest places.

As health care becomes more expensive and economywide inequalities more pronounced, these disparities in life span are likely to get worse — and the share of Americans skipping out on much-needed medical care only likely to grow.

Bad debt, a proxy for unpaid bills, rose in 2018 for nonprofit hospitals after falling for several years since 2014, when some states decided to expand Medicaid, Moody’s Investors Services said in a recent report.

Rising deductibles are fueling the trend, as patients are on the hook for an increasing share of care costs. The growth of bad debt may at times outpace net patient revenue, the ratings agency said.

At the same time, deductibles and premiums are increasing faster than wage growth, another ominous signal for hospitals.

Dive Insight:

More Americans have high deductible plans than ever before, according to the Kaiser Family Foundation.

“More than a quarter (28%) of all covered workers, including nearly half (45%) of those at small employers with fewer than 200 employees, are now in plans with a deductible of at least $2,000, almost four times the share who faced such deductibles in 2009,” KFF said in a recent report.

But when patients with high deductibles seek care, hospitals typically have to collect from the patient first. And as more Americans struggle to afford treatment, it’s harder to collect from patients right away.

“The longer the delay between providing service and collecting payment, the less likely a hospital is to collect payment,” Moody’s said.

Many patients don’t have enough saved to cover the cost of their deductible, according to a survey from accounting firm PwC. At least a third of those with employer-based coverage and HDHPs don’t have enough on hand to pay for their deductible, the company reported.

It will be difficult for hospitals to reduce bad debt, according to Moody’s, which characterized it as an “uphill battle.” Collecting on unpaid bills requires “constant vigilance,” the ratings agency said.

In 2014, bad debt clocked in at roughly 5.6% of net patient revenue for nonprofit health systems, and then fell below 4.5% in 2016 and 2017. But in 2018, bad debt climbed again above 4.5%, Moody’s said.

The Trump administration has encouraged consumers to use private brokers, who often make more money if they sell the less robust plans.

The Trump administration is encouraging consumers on the Obamacare individual market to seek help from private brokers, who are permitted to sell short-term health plans that critics deride as “junk” because they don’t protect people with preexisting conditions, or cover costly services such as hospital care, in many cases.

Consumers looking at their health insurance options on the website for the federal marketplace, called healthcare.gov, may be redirected to other enrollment sites, some of which allow consumers to click a tab entitled “short-term plans” and see a list of those plans, often with significantly cheaper premiums. Short-term plans were once barred from the exchanges because they were considered inadequate coverage and do not meet the insurance requirements laid out under the Affordable Care Act. If consumers select a short-term plan, they are directed to call a phone number to finish signing up, according to screenshots provided to The Post.

Critics say that both the sale of short-term plans through private brokers and consumers’ ability to select such plans are the latest examples of Trump administration efforts to weaken the ACA after failing to repeal and replace the law in Congress.The president has repeatedly contended that short-term plans provide “relief” from expensive individual market insurance plans that are unaffordable to many consumers. The rule allowing the sale of such plans was finalized late last year, just weeks before open enrollment, so this is the first year they are widely available.

In addition to these efforts, the administration is also seeking to void the law in court, siding with a group of Republican state attorneys general who argue it is unconstitutional since Congress zeroed out the penalty for not having insurance in its 2017 tax overhaul legislation. A trial court in Texas ruled the entire law invalid late last year, and an opinion is expected at any time from the U.S. Court of Appeals for the 5th Circuit. The law is likely to end up in front of the Supreme Court for a third time, possibly amid the 2020 presidential election.

Under the ACA, all health insurance plans have to cover 10 essential health benefits, including maternity and newborn care, prescription drugs, emergency room services and mental health. Short-term health plans do not have to cover those services, can discriminate against those with preexisting conditions and set caps on how much they are willing to pay, which is prohibited for Obamacare plans.

Brokers often make higher commissions on short-term plans, health policy experts said, which gives them an incentive to sell them. They are supposed to present ACA-compliant plans to consumers, but are allowed to provide other options, including short-term plans. Some brokers make clear that such plans are not as comprehensive as ACA plans, but experiences differ.

“The whole business model is signing people up for coverage and getting a cut of what they sell, and the place they’re going to make their money is selling these short-term plans,” said Nicholas Bagley, a professor of law at the University of Michigan and proponent of the ACA. Consumers “don’t fully understand the lack of protections if they go over some annual or lifetime [insurance] limit. These plans don’t cover preexisting conditions.”

The administration’s use of outside brokers has prompted nearly two dozen Senate Democrats, including Democratic presidential candidates Elizabeth Warren, Kamala D. Harris and Amy Klobuchar, to send a letter to CMS on Wednesday expressing their concern over the promotion of short-term health plans.

“We are concerned that [CMS] is not only failing to conduct sufficient oversight to protect customers, but is actively emailing consumers to encourage them to obtain coverage through third-party agents and brokers instead of the HealthCare.gov website,” the senators wrote in a letter. Democratic New Hampshire Senator Jeanne Shaheen orchestrated the effort.

Such plans were previously available for periods of three months or less and could not be renewed, but the administration late last year finalized a rule that allowed for the plans’ availability for up to 12 months, with the option to renew them for up to three years. A federal judge sided with the administration in a court challenge to their expanded availability and upheld the rule in July. Consumers still cannot use government subsidies to purchase short-term plans, however.

“For most of the people buying on the exchanges, this would be worse than what they’ve been buying, especially because the majority of people who buy on exchanges get help with their premiums,” said Allison Hoffman, a law professor at the University of Pennsylvania Law School.

The Centers for Medicare and Medicaid Services has sent at least five emails so far to individual market consumers encouraging them to use outside brokers, including through a service called Help on Demand, to sign up for health insurance, according to emails obtained by The Post from a recipient of ACA market emails. The agents and brokers must be registered with the federal exchanges, CMS said in a statement, and they help consumers sign up for individual market plans.

“While agents and brokers are required to provide assistance with Exchange, Medicaid and CHIP coverage and are directed to enroll consumers in such coverage options whenever possible, they are not prohibited from sharing information on other coverage options, such as those offered off-Exchange,” a CMS spokeswoman said.

Some critics of the policy say the expanded sale of short-term plans may be one of the factors depressing enrollment in Obamacare plans, which dropped 13 percent in the first three weeks of the sign-up period, compared to the same period last year, according to federal data released Wednesday. During the 2019 open enrollment, 1,924,476 people signed up for individual market plans in the first two weeks of enrollment, compared to 1,669,401 for 2020. Open enrollment ends on Dec. 15.

CMS said it has used Help on Demand for three years, but the agency has increasingly encouraged consumers to seek their advice through emails directing them to the service’s website.

The Trump administration has drastically cut federal funding for “navigators” — grass roots organizations that help people sign up for ACA plans, including those who may not otherwise know they are eligible for coverage. .

Premiums for the most common type of Obamacare plan dropped by 4 percent for 2020, CMS said last month, and the vast majority of consumers on the individual market qualify for government tax subsidies that help cover the cost of their insurance. However, consumers complain about high deductibles and premiums in individual market plans.

Retirement in America is growing less secure, physically and financially, given the omnipresent threat and cost of serious illness or disease, Bob reports.

Why it matters: Qualifying for Medicare does not guarantee that older adults will skirt potentially ruinous medical bills. Millions of seniors have also come to rely on the taxpayer-funded program for lower income people — Medicaid — and there’s no indication that will slow down.

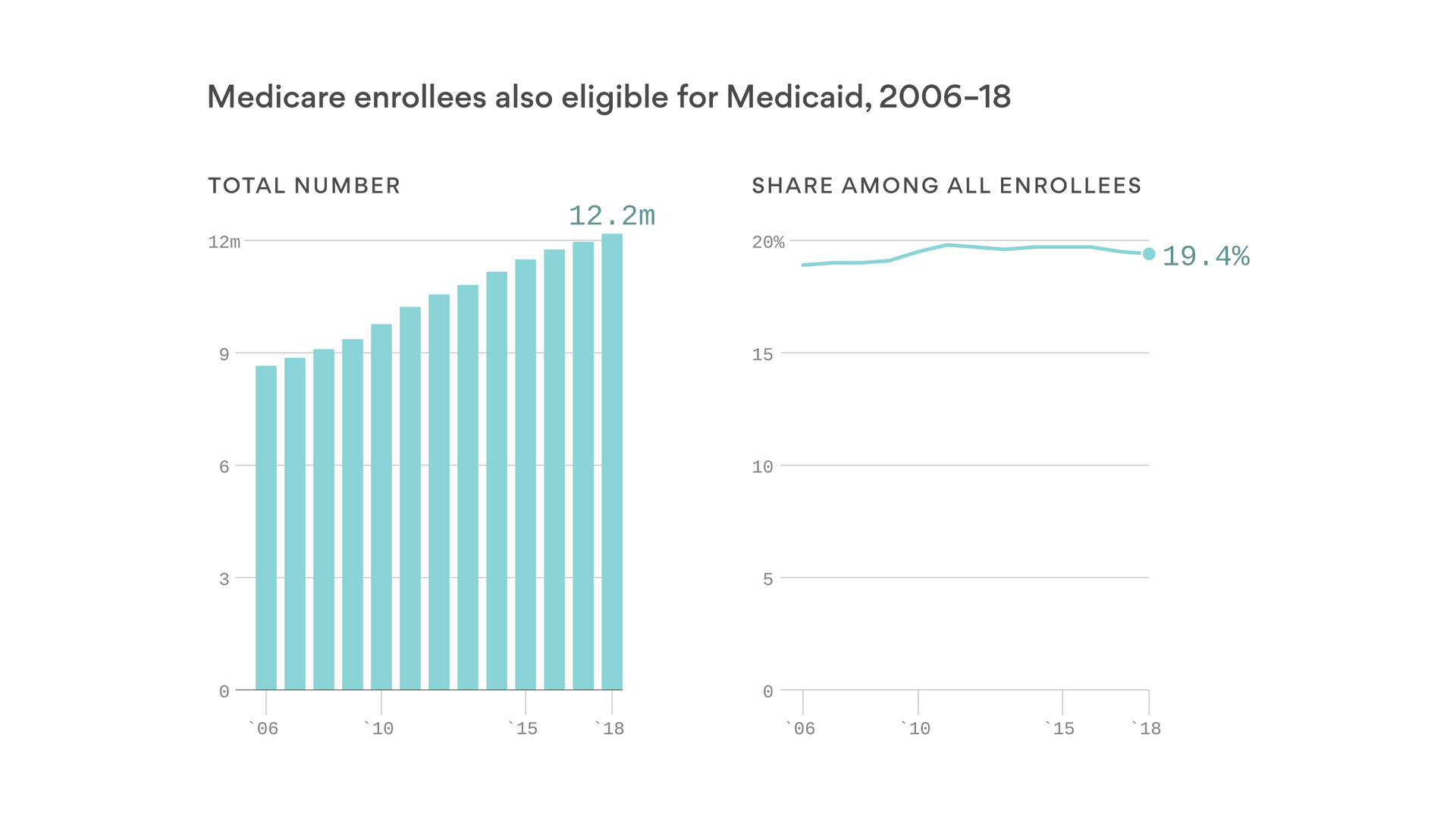

By the numbers: More than 12 million Americans — most of them over 65 — have both Medicare and Medicaid coverage.

That represents about one-fifth of all Medicare enrollees, a percentage that has stayed stable over time even as more baby boomers enter the program.

This low-income population has some of the most expensive health care conditions and disabilities — averaging roughly $30,000 in annual spending per person, or double the average Medicare enrollee.

Between the lines: Some people who age into Medicare have very few assets and income, and therefore automatically qualify for Medicaid.

But retirees who consider themselves middle-class increasingly have to resort to Medicaid because high costs, like dementia or nursing home care, consume their entire nest egg.

What to watch: The federal government has been experimenting with ways to coordinate care better for this population, but that’s a reaction to seniors falling into poverty due to health care costs.

Unless policymakers address the high and rising costs of care, more retirees and their families will have to depend on both Medicare and Medicaid.

Almost all of the major health insurance companies are spending more on medical care this year than they have in the past, Axios’ Bob Herman reports.

The big picture: Rising prices and more services for some sicker patients are among the many reasons why this is happening. That uptick in spending has freaked out Wall Street, even though insurers are still quite profitable.

Driving the news: Almost all of the eight major publicly traded insurers have shown theirmedical loss ratio — the percentage of premium revenues they’re spending on medical claims — is rising this year.

UnitedHealth Group, the largest insurer in the country, said its loss ratio was 82.4% in the third quarter this year compared with 81% in the same period a year ago.

But these companies are handling billions of premium dollars, so any increase in medical claims equates to hundreds of millions of dollars in additional spending, which they don’t want.

Between the lines: Medical loss ratios are often higher for health plans that cover more older adults, the disabled and the poor, because those groups typically need more care or are in the hospital more frequently.

But costs have been climbing in some commercial markets, too.

Anthem executives admitted on their earnings call that the company is dumping some employers with workers who had medical needs and costs that were too high.

CVS Health, which now owns Aetna, previously said some middle-market clients had employees that it thought were getting too many services and drugs.

CVS “intensified our medical management in those geographies,” an executive said on the earnings call.

The bottom line: Health insurance companies closely track their medical loss ratios and aim to hit those targets most often by charging higher premiums, denying care, forcing people to use lower-priced providers or declining to cover people they deem to be too expensive.

Elizabeth Warren on Friday detailed how she intends to pay for Medicare for All without raising costs for middle-class households. The senator from Massachusetts said her plan will cover everyone in the country without raising overall spending, “while putting $11 trillion back in the pockets of the American people by eliminating premiums and virtually eliminating out-of-pocket costs.”

Warren’s plan relies in large part on redirecting existing spending toward a universal, federal health care system, while adding new revenues from taxes on the wealthy, the financial sector and large corporations. “We can generate almost half of what we need to cover Medicare for All just by asking employers to pay slightly less than what they are projected to pay today, and through existing taxes,” Warren said.

Some key details from the Warren plan:

Much lower cost estimate: Warren starts with the Urban Institute’s estimate that the federal government would need $34 trillion more over 10 years to pay for Medicare for All, but she slices that number dramatically — down to $20.5 trillion — by using existing federal and state spending on programs including Medicaid to fund a portion of her proposal, along with larger assumed savings produced by a streamlined system paying lower rates to hospitals, doctors and other health care providers.

Total health care spending stays about the same: Warren projects about $52 trillion in national health care spending over 10 years, close to estimates for the existing system, despite covering more people and offering more generous benefits, including long-term care, audio, vision and dental benefits. Applying Medicare payment levels across the health care system is projected to produce substantial savings that would be used to finance the expanded size and scope of the plan.

Heavy reliance on employer funding: The employer contribution to Medicare for All is pegged at $8.8 trillion, with employers required to contribute to the federal government 98% of what they would pay in employee premiums. Businesses with fewer than 50 employees would be exempt.

Public spending continues: State and local governments would be still on the hook for the $6 trillion they currently spend on Medicaid, the Children’s Health Insurance Program and public employee premiums.

New taxes on the wealthy: Warren proposes a new 3% tax on household wealth over $1 billion — and that’s on top of her proposed wealth tax, which calls for a separate 3% tax on wealth over $1 billion (and a 2% tax on wealth between $50 million and $1 billion). Combined with an annual capital gains tax on the top 1% of households, her proposal projects that the new health-care-focused wealth taxes would produce $3 trillion.

Taxes on business and finance: Warren says she can raise $3.8 trillion through “targeted” taxes on big business and financial transactions, including a financial transaction tax of .01% on the sale of stocks, bonds and derivatives.

Reduced tax evasion: Cracking down on tax evasion is projected to bring in $2.3 trillion. “The federal government has a nearly 15% ‘tax gap’ between what it collects in taxes what is actually owed because of systematic under-enforcement of our tax laws, tax evasion, and fraud,” Warren said. “By investing in stronger enforcement and adopting best practices on tax reporting, withholding, and filing, experts predict that we can close the tax gap by a third.”

Revenue increase from higher take-home pay: Employees would no longer pay premiums for health insurance, providing a pay hike and higher tax revenues, estimated to total $1.4 trillion.

Abolishing the Overseas Contingency Operations fund: Warren is calling for reduced military spending, with a focus on what some call the “slush fund” that covers the cost of overseas military operations. Eliminating this off-budget spending is projected to save $800 billion.

Immigration reform: Expanded legal immigration would bring in $400 billion in revenue as more incomes are subject to taxes, Warren says.

A record tax cut? Once the new revenues and cost savings are added up, Warren says her plan will deliver what amounts to an historic tax cut. “No middle class tax increases. $11 trillion in household expenses back in the pockets of American families. That’s substantially larger than the largest tax cut in American history.”

Warren won plaudits from some analysts and policy wonks for releasing a plan, but the details she laid out are also being picked apart by critics and rivals, with some experts already expressing doubts about her assumptions and numbers. Here’s some of the reaction:

Congratulations from a conservative: “Kudos to Senator Warren for actually releasing a plan,” said Scott Greenberg, formerly an analyst with the right-leaning Tax Foundation. “There are a lot of things in here that will draw attacks from the left and from the right, and it might have been politically easier not to release it at all. But Warren has stuck by her commitment to explain her proposals.”

Criticism from a key rival: “The mathematical gymnastics in this plan are all geared towards hiding a simple truth from voters: it’s impossible to pay for Medicare for All without middle class tax increases,” said Kate Bedingfield, deputy campaign manager for Joe Biden. Bedingfield argued that employees would end up paying the tax on employers.

Dire warnings from the White House: “It is the middle class who would have to pay the extra $100 billion or more to finance this kind of socialist government takeover of health care,” said Larry Kudlow, President Trump’s top economic adviser. “It would have a catastrophic effect on the economy and all these numbers that we’re seeing, all these numbers, on incomes per household, on wage increases, on jobs, all these numbers would literally evaporate and by the by, so would the stock market.”

Tax vs. premium: Warren’s plan will likely kick off a debate about the difference between taxes and health care premiums, and whether that difference matters, says William Gale of the Brookings Institution. “Does [the Warren plan] raise ‘taxes’ on the middle class?,” Gale asked Friday. “Short answer — it does not raise ‘burdens’ on the middle class.”

Cost reduction is crucial: “The key to Warren’s plan for financing Medicare for all is aggressively constraining prices paid to hospitals, physicians, and drug companies. We’d still have the most expensive health system in the world, but it would be less expensive than it is now,” said LarryLevitt of the Kaiser Family Foundation. “Warren’s plan to aggressively constrain health care prices under Medicare for all would be quite disruptive. On the other hand, every other developed country has managed to figure it out, so we know it’s possible.”

And the battle is ultimately political: “In laying out the specifics of her Medicare for all plan, Warren’s challenge is more about politics than arithmetic,” Levitt continued. “She is taking on the wealthy, corporations, and pretty much every part of the health care and insurance industries. Those are some powerful enemies.”

So don’t expect major legislation soon: “Experts will argue for months whether [Warren is] being too optimistic — whether her cost estimates are too low and her revenue estimates too high, whether we can really do this without middle-class tax hikes,” said economist Paul Krugman. “You might say that time will tell, but it probably won’t: Even if Warren becomes president, and Dems take the Senate too, it’s very unlikely that Medicare for all will happen any time soon.”