https://finance.yahoo.com/news/weekly-unemployment-claims-week-ended-dec-4-2021-192034644.html

New initial jobless claims improved much more than expected last week to reach the lowest level in more than five decades, further pointing to the tightness of the present labor market as many employers seek to retain workers.

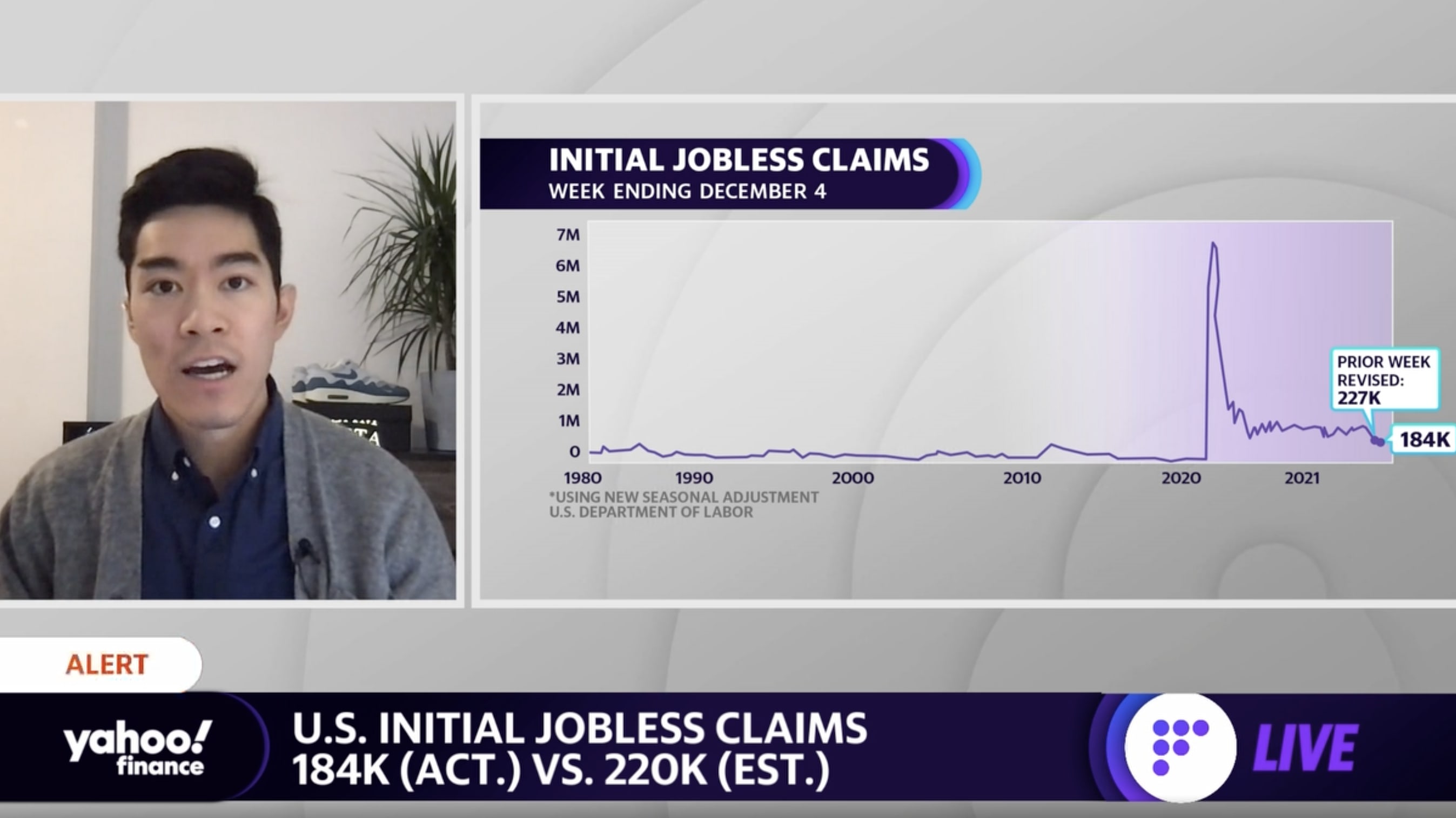

The Labor Department released its weekly jobless claims report on Thursday. Here were the main metrics from the print, compared to consensus estimates compiled by Bloomberg:

- Initial unemployment claims, week ended Dec. 4: 184,000 vs. 220,000 expected and an upwardly revised 227,000 during prior week

- Continuing claims, week ended Nov. 27: 1.992 million vs. 1.910 million expected and a downwardly revised 1.954 million during prior week

Jobless claims decreased once more after a brief tick higher in late November. At 184,000, initial jobless claims were at their lowest level since Sept. 1969.

“The consensus always looked a bit timid, in light of the behavior of unadjusted claims in the week after Thanksgiving in previous years when the holiday fell on the 25th, but the drop this time was much bigger than in those years, and bigger than implied by the recent trend,” Ian Shepherdson, chief economist for Pantheon Macroeconomics, wrote in an email Thursday morning. “A correction next week seems likely, but the trend in claims clearly is falling rapidly, reflecting the extreme tightness of the labor market and the rebound in GDP growth now underway.”

After more than a year-and-a-half of the COVID-19 pandemic in the U.S., jobless claims have begun to hover below even their pre-pandemic levels. New claims were averaging about 220,000 per week throughout 2019. At the height of the pandemic and stay-in-place restrictions, new claims had come in at more than 6.1 million during the week ended April 3, 2020.

Continuing claims, which track the number of those still receiving unemployment benefits via regular state programs, have also come down sharply from pandemic-era highs, and held below 2 million last week.

“Beyond weekly moves, the overall trend in filings remains downward and confirms that businesses facing labor shortages are holding onto workers,” wrote Rubeela Farooqi, chief U.S. economist for High Frequency Economics, in a note on Wednesday.

Farooqi added, however, that “the decline in layoffs is not translating into faster job growth on a consistent basis, which was evident in a modest gain in non-farm payrolls in November.”

“For now, labor supply remains constrained and will likely continue to see pandemic effects as the health backdrop and a lack of safe and affordable child care keeps people out of the workforce,” she added.

Other recent data on the labor market have also affirmed these lingering pressures. The November jobs report released from the Labor Department last Friday reflected a smaller number of jobs returned than expected last month, with payrolls growing by the least since December 2020 at just 210,000. And the labor force participation rate came in at 61.8%, still coming in markedly below its pre-pandemic February 2020 level of 63.3%.

And meanwhile, the Labor Department on Wednesday reported that job openings rose more than expected in October to top 11 million, coming in just marginally below July’s all-time high of nearly 11.1 million. The quits rate eased slightly to 2.8% from September’s record 3.0% rate.

“There is a massive shortage of labor out there in the country that couldn’t come at a worst time now that employers need workers like they have never needed them before. This is a permanent upward demand shift in the economy that won’t be alleviated by companies offering greater incentives to their new hires,” Chris Rupkey, FWDBONDS chief economist, wrote in a note Wednesday. “Wage inflation will continue to keep inflation running hot as businesses fall all over themselves in a bidding war for talent.”