Cartoon – Working from Work

Health systems are recovering from the worst financial year in recent history. We surveyed strategic planners to find out their top priorities for 2024 and where they are focusing their energy to achieve growth and sustainability. Read on to explore the top six findings from this year’s survey.

With this survey, we sought the answers to five key questions:

Bigger is Better for Financial Recovery

Hospitals are beginning to recover from the lowest financial points of 2022, where they experienced persistently negative operating margins. In 2023, the majority of respondents to our survey expected positive changes in operating margins, total margins, and capital spending. However, less than half of the sample expected increases in full-time employee (FTE) count. Even as many organizations reported progress in 2023, challenges to workforce recovery persisted.

40%

Importantly, the sample was relatively split between those who are improving financial performance and those who aren’t. While 53% of respondents projected a positive change to operating margins in 2023, 40% expected negative changes to margin.

One exception to this split is large health systems. Large health systems projected above-average recovery of FTE counts, volume, and operating margins. This will give them a higher-than-average capital spending budget.

These findings echo an industry-wide consensus on improved financial performance in 2023. However, zooming in on the data revealed that the rising tide isn’t lifting all boats. Unequal financial recovery, especially between large and small health systems, can impact the balance of independent, community, and smaller providers in a market in a few ways. Big organizations can get bigger by leveraging their financial position to acquire less resourced health systems, hospitals, or provider groups. This can be a lifeline for some providers if the larger organization has the resources to keep services running. But it can be a critical threat to other providers that cannot keep up with the increasing scale of competitors.

Variation in financial performance can also exacerbate existing inequities by widening gaps in access. A key stakeholder here is rural providers. Rural providers are particularly vulnerable to financial pressures and have faced higher rates of closure than urban hospitals. Closures and consolidation among these providers will widen healthcare deserts. Closures also have the potential to alter payer and case mix (and pressure capacity) at nearby hospitals.

Volumes are decoupled from margins

Positive changes to FTE counts, reduced contract labor costs, and returning demand led the majority of respondents in our survey to project organizational-wide volume growth in 2023. However, a significant portion of the sample is not successfully translating volume growth to margin recovery.

44%

On one hand, 84% of our sample expected to achieve volume growth in 2023. And 38% of respondents expected 2023 volume to exceed 2022 volume by over 5%. But only 53% of respondents expected their 2023 operating margins to grow — and most of those expected that the growth would be under 5%. Over 40% of respondents that reported increases in volume simultaneously projected declining margins.

Health systems struggled to generate sufficient revenue during the pandemic because of reduced demand for profitable elective procedures. It is troubling that despite significant projected returns to inpatient and outpatient volumes, these volumes are failing to pull their weight in margin contribution. This is happening in the backdrop of continued outpatient migration that is placing downward pressure on profitable inpatient volumes.

There are a variety of factors contributing to this phenomenon. Significant inflationary pressures on supplies and drugs have driven up the cost of providing care. Delays in patient discharge to post-acute settings further exacerbate this issue, despite shrinking contract labor costs. Reimbursements have not yet caught up to these costs, and several systems report facing increased denials and delays in reimbursement for care. However, there are also internal factors to consider. Strategists from our study believe there are outsized opportunities to make improvements in clinical operational efficiency — especially in care variation reduction, operating room scheduling, and inpatient management for complex patients.

Strategists look to technology to stretch capital budgets

Capital budgets will improve in 2024, albeit modestly. Sixty-three percent of respondents expect to increase expenditures, but only a quarter anticipate an increase of 6% or more. With smaller budget increases, only some priorities will get funded, and strategists will have to pick and choose.

Respondents were consistent on their top priority. Investments in IT and digital health remained the number one priority in both 2022 and 2023. Other priorities shifted. Spending on areas core to operations, like facility maintenance and medical equipment, increased in importance. Interest in funding for new ambulatory facilities saw the biggest change, falling down two places.

Capital budgets for health systems may be increasing, but not enough. With the high cost of borrowing and continued uncertainty, health systems still face a constrained environment. Strategists are looking to get the biggest bang for their buck. Technology investments are a way to do that. Digital solutions promise high impact without the expense or risk of other moves, like building new facilities, which is why strategists continue to prioritize spending on technology.

The value proposition of investing in technology has changed with recent advances in artificial intelligence (AI), and our respondents expressed a high level of interest in AI solutions. New applications of AI in healthcare offer greater efficiencies across workforce, clinical and administrative operations, and patient engagement — all areas of key concern for any health system today.

Building is reserved for those with the largest budgets

Another way to stretch capital budgets is investing in facility improvements rather than new buildings. This allows health systems to minimize investment size and risk. Our survey found that, in general, strategists are prioritizing capital spending on repairs and renovation while deprioritizing building new ambulatory facilities.

When the responses to our survey are broken out by organization type, a different story emerges. The largest health systems are spending in ways other systems are not. Systems with six or more hospitals are increasing their overall capital expenditures and are planning to invest in new facilities. In contrast, other systems are not increasing their overall budgets and decreasing investments in new facilities.

AMCs are the only exception. While they are decreasing their overall budget, they are increasing their spending on new inpatient facilities.

Health systems seek to attract patients with new facilities — but only the biggest systems can invest in building outpatient and inpatient facilities. The high ranking of repairs in overall capital expenditure priorities suggests that all systems are trying to compete by maintaining or improving their current facilities. Will renovations be enough in the face of expanded building from better financed systems? The urgency to respond to the pandemic-accelerated outpatient shift means that building decisions made today, especially in outpatient facilities, could affect competition for years to come. And our survey responses suggest that only the largest health system will get the important first-mover advantage in this space.

AMCs are taking a different tack in the face of tight budgets and increased competition. Instead of trying to compete across the board, AMCs are marshaling resources for redeployment toward inpatient facilities. This aligns with their core identity as a higher acuity and specialty care providers.

Partnerships and affiliations offer potential solutions for health systems that lack the resources for building new facilities. Health systems use partnerships to trade volumes based on complexity. Partnerships can help some health systems to protect local volumes while still offering appropriate acute care at their partner organization. In addition, partnerships help health systems capture more of the patient journey through shared referrals. In both of these cases, partnerships or affiliations mitigate the need to build new inpatient or outpatient facilities to keep patients.

Revenue diversification tactics decline despite disruption

Eighty percent of respondents to our survey continued to lose patient volumes in 2023. Despite this threat to traditional revenue, health systems are turning from revenue diversification practices. Respondents were less likely to operate an innovation center or invest in early-stage companies in 2023. Strategists also reported notably less participation in downside risk arrangements, with a 27% decline from 2022 to 2023.

The retreat from revenue diversification and risk arrangements suggests that health systems have little appetite for financial uncertainty. Health systems are focusing on financial stabilization in the short term and forgoing practices that could benefit them, and their patients, in the long term.

Strategists should be cautious of this approach. Retrenchment on innovation and value-based care will hold health systems back as they confront ongoing disruption. New models of care, patient engagement, and payment will be necessary to stabilize operations and finances. Turning from these programs to save money now risks costing health systems in the future.

Market intelligence and strategic planning are essential for health systems as they navigate these decisions. Holding back on initiatives or pursuing them in resource-constrained environments is easier when you have a clear course for the future and can limit reactionary cuts.

Advisory Board’s long-standing research on developing strategy suggests five principles for focused strategy development:

Strategists align on a strategic vision to go back to basics

Despite uneven recovery, health systems widely agree on which strategic initiatives they will focus more on, and which they will focus less on. Health system leaders are focusing their attention on core operations — margins, quality, and workforce — the basics of system success. They aim to achieve this mandate in three ways. First, through improving efficiency in care delivery and supply chain. Second, by transforming key elements of the care delivery system. And lastly, through leveraging technology and the virtual environment to expand job flexibility and reduce administrative burden.

Health systems in our survey are least likely to take drastic steps like cutting pay or expensive steps like making acquisitions. But they’re also not looking to downsize; divesting and merging is off the table for most organizations going into 2024.

The strategic priorities healthcare leaders are working toward are necessary but certainly not easy. These priorities reflect the key challenges for a health system — margins, quality, and workforce. Luckily, most of strategists’ top priorities hold promise for addressing all three areas.

This triple mandate of improving margins, quality, and workforce seems simple in theory but is hard to get right in practice. Integrating all three core dimensions into the rollout of a strategic initiative will amplify that initiative’s success. But, neglecting one dimension can diminish returns. For example, focusing on operational efficiency to increase margins is important, but it’ll be even more effective if efforts also seek to improve quality. It may be less effective if you fail to consider clinicians’ workflow.

Health systems that can return to the basics, and master them, are setting a strong foundation for future growth. This growth will be much more difficult to attain without getting your house in order first.

Vendors and other health system partners should understand that systems are looking to ace the basics, not reinvent the wheel. Vendors should ensure their products have a clear and provable return on investment and can map to health systems’ strategic priorities. Some key solutions health systems will be looking for to meet these priorities are enhanced, easy-to-follow data tools for clinical operations, supply chain and logistics, and quality. Health systems will also be interested in tools that easily integrate into provider workflow, like SDOH screening and resources or ambient listening scribes.

Going back to basics

Craft your strategy

1. Rebuild your workforce.

One important link to recovery of volume is FTE count. Systems that expect positive changes in FTEs overwhelmingly project positive changes in volume. But, on average, less than half of systems expected FTE growth in 2023. Meanwhile, high turnover, churn, and early retirement has contributed to poor care team communication and a growing experience-complexity gap. Prioritize rebuilding your workforce with these steps:

2. Become the provider of choice with patient-centric care.

Becoming the provider of choice is crucial not only for returning to financial stability, but also for sustained growth. To become the provider of choice in 2024, systems must address faltering consumer perspectives with a patient-centric approach. Keep in mind that our first set of recommendations around workforce recovery are precursors to improving patient-centered care. Here are two key areas to focus on:

3. Recouple volume and margins.

The increasingly decoupled relationship between volume and margins should be a concern for all strategists. There are three parts to improving volume related margins: increasing volume for high-revenue procedures, managing costs, and improving clinical operational efficiency.

On January 1st, 2024 #AB1076 and #SB699, two draconian noncompete laws go into effect. It could put many #employedphysicians in a new position to walk away from #employeeremorse.

AB1076 voids non-compete contracts and require the employer to give written notice by February 14th, 2024 that their contract is void.

Is this a good or bad thing? It depends.

If the contract offers more protections and less risk to the employed physician, and the contract is void – does that mean the whole contract is void? Or is the non-compete voidable?

But for the hospital administrator or practice administrator, we’re about to witness the golden handcuffs come off and administrators will have to compete to retain talent that could be lured away more easily than in the past. But the effect of the non-compete is far more worrisome for an administrator because of the following:

The physicians many freely and fairly compete against the former employer by calling upon, soliciting, accepting, engaging in, servicing or performing business with former patients, business connections, and prospective patients of their former employer.

It could also give rise to tumult in executive positions and management and high value employees like managed care and revenue cycle experts who may have signed noncompete contracts.

If the employer does not follow through with the written notice by February 14th, the action or failure to notify will be “deemed by the statute to be an act of unfair competition that could give rise to other private litigation that is provided for in SB699.

The second law, SB699, provides a right of private action, permitting the former employees subject to SB699 the right to sue for injunctive relief, recovery of actual damages, and attorneys fees. It also makes it a civil violation to enter into or enforce a noncompete agreement. It further applies to employees who were hired outside California but now work in or through a California office.

What else goes away?

Employed physicians can immediately go to work for a competitor and any notice requirement or waiting period (time and distance provisions) are eliminated by the laws. So an administrator could be receiving “adios” messages on January 2nd, and watch market share slip through their fingers like a sieve starting January 3rd.

And what about the appointment book? Typically, appointments are set months in advance, especially for surgeons – along with surgery bookings, surgery block times, and follow up visits.

Hospitals may be forced to reckon with ASCs where the surgeons could not book cases under their non-compete terms and conditions. They could up and move their cases as quickly as they can be credentialed and privileged and their PECOS and NPPES files updated and a new 855R acknowledged as received.

APPs such as PAs and NPs could also walk off and bottleneck appointment schedules, surgical assists, and many office-based procedures that were assigned to them. They could also walk to a new practice or a different hospitals and also freely and fairly compete against the former employer by calling upon, soliciting, accepting, engaging in, servicing or performing business with former patients, business connections, and prospective patients of their former employer.

Next, let’s talk about nurses and CRNAs. If they walk off and are lured away to a nearby ASC or hospital, or home health agency, that will disrupt many touchpoints of the current employer.

Consultants’ contracts are another matter to be reckoned with. In all my California (and other) contracts, contained within them are anti-poaching provisions that state that I may not offer employment to one of their managed care, revenue cycle, credentialing, or business development superstars. Poof! Gone!

The time to conduct a risk assessment is right now! But many of the people who would be assigned this assessment are on holiday vacation and won’t be back until after January 1st. But then again, they too could be lured away or poached.

What else will be affected?

Credentialing and privileging experts should be ready for an onslaught of applications that have to be processed right away. They will not only be hit with new applications, but also verification of past employment for the departing medical staff.

Billing and Collections staff will need to mount appeals and defenses of denied claims without easy access they formerly had with departing employed physicians.

Medical Records staff will need to get all signature and missing documentation cleared up without easy access they formerly had with departing employed physicians.

Managed Care Network Development experts at health plans and PPOs and TPAs will be recredentialing and amending Tax IDs on profiles of former employed physicians who stand up their own practice or become employed or affiliated with another hospital or group practice. This comes at an already hectic time where federal regulations require accurate network provider directories.

The health plans will need to act swiftly on these modifications because NCQA-accredited health plans must offer network adequacy and formerly employed physicians who depart one group but cannot bill for patient visits and surgeries until the contracting mess is cleared up does not fall under “force majeure” exceptions. If patients can’t get appointments within the stated NCQA time frames, the health plan is liable for network inadequacy. I see that as “leverage” because the physician leaving and going “someplace else” (on their own, to a new group or hospital) can push negotiations on a “who needs whom the most?” basis. Raising a fee schedule a few notches is a paltry concern when weight against loss of NCQA accreditation (the Holy Grail of employer requirements when purchasing health plan benefits from a HMO) and state regulator-imposed fines. All it takes to attract the attention of regulators and NCQA are a few plan member complaints that they could not get appointments timely.

Health plans who operate staff model and network model plans that employ physicians, PAs and NPs (e.g., Kaiser and others who employ the participating practitioners and own the brick and mortar clinics where they work) are in for risk of losing the medical staff to “other opportunities.” These employment arrangements are at a huge risk of disruption across the state.

Workers Compensation Clinics that dot the state of California and already have wait times measured in hours as well as Freestanding ERs and Freestanding Urgent Care Clinics could witness a mass exodus of practitioners that disrupt operations and make their walk in model inoperative and unsustainable in a matter of a week.

FQHCs that employ physicians, psychotherapists, nurse practitioners and physician assistants could find themselves inadequately staffed to continue their mission and operations. Could this lead to claims of patient abandonment? Failed Duty of Care? Who would be liable? The departing physician or their employer?

And then, there are people like me – consultants who help stand up new independent and group practices, build new brands, rebrand the physicians under their own professional brands, launch new service lines like regenerative medicine and robotics, cardiac and vascular service lines, analyze managed care agreements, physician, CRNA, psychotherapist, and APP employment agreements. There aren’t many consultants with expertise in these niches. There are even fewer who are trained as paralegals, and have practical experience as advisors or former hospital and group practice administrators (I’ve done both) who are freelancers. I expect I will become very much in demand because of the scarcity and the experience. I am one of very few experts who are internationally-published and peer-reviewed on employment contracts for physicians.

The post-pandemic labor force has 1.5 million fewer individuals with some post-secondary education short of a bachelor’s degree. This shortfall is hitting healthcare hardest, affecting wages and qualification levels among jobholders.

Job vacancies requiring a post-secondary certificate or associate degree, particularly in healthcare, remain high. The mismatch between the supply of workers with this education level and the ongoing demand for them is leading to increased wages and greater reliance on more educated workers, according to a December 2023 bulletin from the Federal Reserve Bank of Kansas City.

Five takeaways from the bank’s report:

1. Before the pandemic, job openings across educational groups moved together and subsequently peaked together in mid-2022. Since then, while vacancies for most groups have fallen, the number of job vacancies requiring some college education remains 60% above its pre-pandemic level.

2. Vacancies for jobs requiring some college education are concentrated in healthcare. As of August 2023, about 50% of all open jobs posted in 2023 that required an associate degree or non-degree certificate were in healthcare.

3. As a result of the high demand, healthcare employers are turning to more educated workers to fill positions with requirements for some college education. Healthcare employment among workers with some college education has dropped by about 400,000 since 2019; healthcare employment among workers with a bachelor’s degree or more has increased by 600,000.

4. Combined, these factors can place upward pressure on healthcare wages. The supply-demand mismatch can lead employers to offer higher wages to competitively attract qualified workers. Employers turning to workers with more education, who are generally more expensive, will increase the average wage in these occupations.

5. From 2019 to 2023, overall wages for healthcare workers rose by nearly 25%, an increase the bank partially attributes to both increased wages within educational groups and composition effects. The shift in employment toward higher-educated workers accounts for an additional 2.7 percentage points of the total wage increase, for instance.

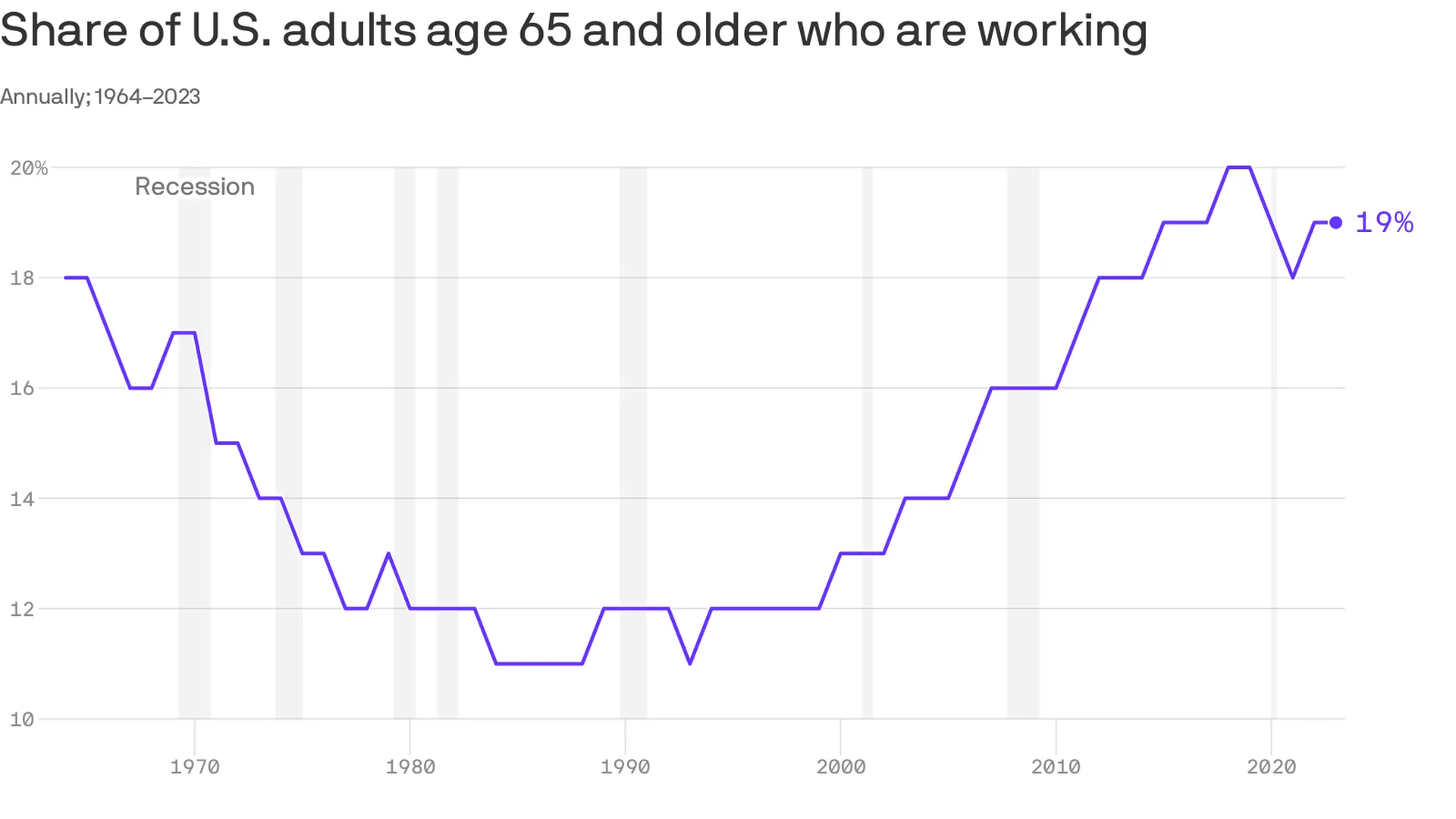

https://www.axios.com/2023/12/14/older-american-adults-working-wages-economy

An increasing number of Americans age 65 and older are working — and earning higher wages, per a study from the Pew Research Center out Thursday.

Why it matters:

This is good for the economy, especially as the U.S. population ages — but whether or not it’s good for older Americans is a bit more subjective.

Zoom in:

The share of older adults working has been steadily increasing since the late 1980s, with a detour during the pandemic as older folks retired in greater numbers. Several forces are driving the shift:

By the numbers:

Last year, the typical 65+ worker earned $22 an hour, up from $13 (in 2022 dollars) in 1987. That’s about $3 less than the average for those age 25-64, and the number includes wages of full- and part-time workers.

Be smart:

Before Social Security existed, older people worked — a lot. In the 1880s, about three-fourths of older men were employed, said Richard Fry, senior researcher at Pew. They also didn’t live as long.

The big picture:

“If people are working longer because they find purpose in their jobs and want to stay engaged, that’s good for them individually,” said Nick Bunker, head of economic research at Indeed Hiring Lab.

What to watch:

The share of older adults working peaked before the pandemic — will it surpass those levels?

The layoff process used to be abrupt: a worker learns their job has been cut and they leave the same day (sometimes with a security escort). Now, some companies are alerting employees that their roles will be eliminated months in advance, The Wall Street Journal reported Dec. 10.

The longer runways — adopted by the likes of Wells Fargo and Disney — benefit both employer and employee, according to the Journal.

Many companies overhired during the pandemic, causing the white-collar job market to tighten. Employers, now sporting the upper hand, are adding additional steps to their hiring processes to ensure they choose the right candidate. A longer goodbye gives them time to be more selective when bringing on replacements.

Advance layoff notice also benefits employees by giving them more time to find a new opportunity and figure out their finances while still collecting a paycheck. This reflects positively on employers, who have faced increased social media backlash for mass layoffs this year. It also shows existing and prospective employees that the company aims to treat them fairly — a practice that could improve retention rates in the future, Wade Rogers, senior vice president of global human resources and chief compliance officer at the chemical company Huntsman, told the Journal.

“How we handle ourselves and how we handle our relationships with our associates matters,” Mr. Rogers said.

A long layoff period is more dangerous at some companies, such as those where a begrudged employee can access confidential patents or business plans, according to the Journal. Others worry that workers who receive advance notice of their impending layoff will lose motivation while continuing to collect their pay.

Jennifer Bender, who most recently served as senior vice president of human resources at the technology company Change Healthcare, recommended letting these employees know they could still be terminated sooner if they give the company due cause. At her company, which informed people of their layoff date two to four weeks in advance, this reduced security concerns.

“It’s really a best practice at this point,” Ms. Bender told the Journal.

These days I have been reading From Strength to Strength: Finding Success, Happiness, and Deep Purpose in the Second Half of Life by Arthur C. Brooks. Brooks is the former President of the American Enterprise Institute and is currently a professor at both the Harvard Kennedy School and the Harvard Business School.

From Strength to Strength is a book about intelligence and aging and the relationship of those aspects to personal happiness. The book is part sociology, part psychology, and part self-help. But if you read carefully, the book also offers important lessons in contemporary management.

The central theme of From Strength to Strength is how our intelligence changes over time and how individuals must change to make the best use of this changing intelligence. To make this point, Brooks cites Raymond Cattell, a British-American psychologist, who in 1971 suggested that there are two types of intelligence: “fluid intelligence” and “crystallized intelligence.”

Cattell and Brooks define fluid intelligence as the ability to “reason, think flexibly, and solve novel problems.” This is the kind of smarts and intelligence that is associated with young Nobel Prize winners and the tech titans of Silicon Valley. Crystallized intelligence is different. Brooks defines crystallized intelligence as the ability to use a stock of knowledge accumulated and learned in the past. Fluid intelligence is a characteristic of the young while crystallized intelligence is more closely associated with our aging process.

At its best, fluid intelligence is “raw smarts” or what I might term “mental athleticism.” Crystallized intelligence at its best is what we recognize as “wisdom.”

Extrapolating from Brooks’ observations and analysis, one can conclude that complex organizations, both not-for-profit and for-profit, require both kinds of executive intelligence. Fluid intelligence generates new ideas, top-shelf innovation, and executive solutions to the most difficult business problems. But crystallized intelligence provides organizations with “the wisdom and experience of people who have seen a lot.”

To further paraphrase Brooks, crystallized intelligence can teach the organization how not to make flagrant, self-defeating, and avoidable errors.

Reading Brooks and thinking about Cattell’s research led me to two observations. First, in our general corporate environment, including hospitals, we very much de-emphasize the value of crystallized intelligence. Just at the moment when many “older” executives are at the highest point of institutional wisdom, our modern corporate structure tends to react in two ways:

Turning this discussion more specifically to hospital management leads to my second observation. Since Covid, the number of hospital CEO resignations has significantly increased when compared to previous years. Additionally, not only has CEO turnover increased but a number of important, influential, and highly capable CEOs—who previously might have been expected to work into their mid-sixties or, perhaps, even into their early seventies—have also decided to leave hospital leadership.

If we come back then to the central observations of Brooks and Cattell, we can see that hospital leadership and management, which is already challenged by so many external and difficult factors, is now losing critically required crystallized intelligence and wisdom.

Having said all this, it is still patently obvious that your organization requires the fluid intelligence of the next generation and the generation after that. That kind of intelligence is necessary and essential to solve today’s and tomorrow’s hardest healthcare problems. And, of course, to innovate and then to innovate some more.

But at the same time, your hospital or health system must also preserve a prominent place for older executives who possess the crystallized intelligence that assures your hospital will prioritize caring, thoughtfulness, and an essential level of managerial balance—all things that come along with executive wisdom.

From Strength to Strength signals a new way of looking at your executive team. This includes understanding that executives of differing tenures bring very different types of intelligence to the organization. And, it requires finding the proper balance between fluid and crystallized intelligence to give your hospital the very best opportunity to re-find its way to a much-needed new vision of hospital success.

https://mailchi.mp/f12ce6f07b28/the-weekly-gist-november-10-2023?e=d1e747d2d8

One welcome side effect of the current economic challenges health systems face has been the return to prominence of the chief nursing officer (CNO) as a pivotal driver of system strategy.

So many of a hospital’s important operating and margin pressures intersect with the CNO’s domain: staffing shortages, nurse recruiting and retention, workplace violence, rising union activity, care model redesign, adoption of new care technologies (including AI), the shift of the clinical workforce into non-hospital settings, and on and on.

Never has the role of the CNO been more important to ensuring systems’ continued ability to deliver high-quality, cost-effective care in a sustainable way.

Even more heartening, we’ve been part of a number of system board retreats and strategy discussions over the past several months at which the CNO has been an important voice in the room.

We’d argue that, given how important these issues will be over the coming years, it may be time to give CNOs a permanent role in health system governance, just as boards often include physician members.

One additional agenda item that will be critical for systems to address, given the demographics of nursing executives:

what’s being done to cultivate the next generation of strong nursing leadership to fill the CNO role? A topic worth keeping an eye on.