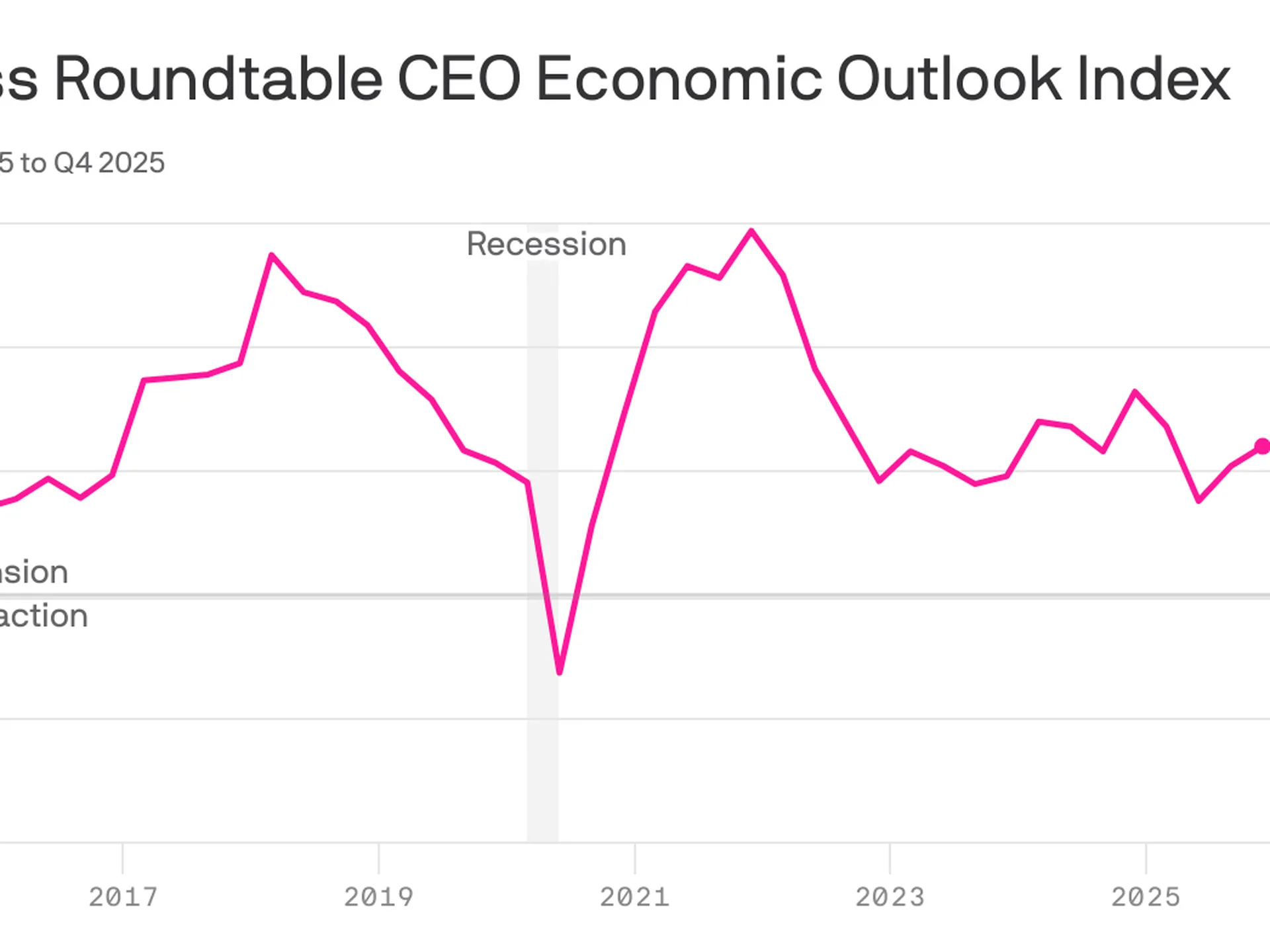

CEO sentiment increasedfor the third consecutive quarter, even as America’s most prominent executives expect underlying job market conditions to remain weak.

Why it matters:

The economic outlook among CEOs has steadily improved since plunging in the aftermath of President Trump’s initiation of the global trade war.

Under the hood, however, there is evidence that structural economic changes — including the proliferation of AI — are weighing on hiring intentions, a warning sign for the labor market.

By the numbers:

The Business Roundtable’s CEO Economic Outlook Index rose by 4 points in its fourth-quarter survey, which was fielded from the final weeks of November through earlier this month.

The index is still shy of the highest level of the Trump 2.0 era and slightly below the historical average of 83.

Zoom in:

The increase reflects a more upbeat view of company revenue in the next six months: Expectations for sales rose 6 points, though the survey does not ask respondents to adjust for the prospect of higher prices.

Plans for capital expenditures — investments in equipment, buildings or software — ticked up 2 points, following a 10-point surge in the previous quarter.

Hiring plans also improved relative to last quarter — up 4 points — though it is the survey’s lone indicator below the level that signals growth.

What they’re saying:

“Notably this quarter, more CEOs plan to reduce employment than increase it for the third quarter in a row – the lowest three-quarter average since the Great Recession,” Business Roundtable CEO Joshua Bolten said in a statement.

About one-quarter of CEOs say they will increase hiring, while 35% say employment will shrink at their respective firms. The remaining 40% plan to keep hiring steady.

A smaller share of CEOs plan to slash workers relative to last quarter, but the figures still show a notable shift among top executives.

Consider the results from this time last year: A similar share of CEOs expected no change in employment levels, but just 21% said they anticipated cutting jobs, while 38% planned to increase hiring.

“CEOs’ softening hiring plans reflect an uncertain economic environment in which AI is driving sizeable [capital expenditures] growth and productivity gains while tariff volatility is increasing costs, particularly for tariff-exposed companies, including small businesses,” Bolten said today.

The big picture:

The in-the-dumps hiring plans signaled by big firm CEOs — alongside a string of layoff announcements in recent months — signal a possible shift for the steady-state labor market that has persisted in recent years.

Powell raised the possibility that the labor market might be even weaker than government data suggests.

The economy has added a monthly average of 40,000 payroll jobs since April. But “we think there’s an overstatement in these numbers, by about 60,000, so that would be negative 20,000 per month,” Powell said at yesterday’s press conference.

“The labor market has continued to cool gradually, maybe just a touch more gradually than we thought,” he added.

The bottom line:

CEOs feel more optimistic, though that confidence boost is not expected to translate into more hiring — an unusual dynamic for the economy.

“Although the results signal that CEOs are approaching the first half of 2026 with some caution, they are starting to see opportunities for growth,” Cisco CEO Chuck Robbins, who chairs the Business Roundtable, said in a statement.

“With the Index near its average, it reflects the resilience of the U.S. economy,” he added, citing pro-growth tax policies and fewer regulations.

The economic fortunes of mom-and-pop businesses are diverging from those of their larger counterparts — a pre-existing gap that now appears to be getting bigger, faster.

Why it matters:

The evidence is in the private-sector labor market, that in recent months, has been propped up by large companies as smaller firms — typically responsible for 40% of U.S. employment — shed workers.

The big picture:

Larger businesses have been able to adapt to a tough economic backdrop — historic tariffs, high interest rates and a more cautious consumer — in ways far more challenging for small companies with fewer resources.

“It’s evident that medium and large firms are better positioned to weather what’s going on,” said ADP chief economist Nela Richardson.

“They can set prices, they can change suppliers. They can hire contractors instead of permanent employees in a more sophisticated way. They can hire globally, not just in their local region. They have more tools in the toolbox,” Richardson said.

By the numbers:

The hiring gap between small and big businesses is getting worse, a fresh sign that small business firings are holding down jobs growth across the economy.

As we mentioned yesterday, the private sector shed 32,000 jobs in November, according to payroll processor ADP. Small firms — those with fewer than 50 employees — accounted for all of the losses.

Those businesses reported a net loss of 120,000 jobs, the most small businesses have cut since the pandemic’s onset. Larger businesses grew, but not enough to offset the cuts elsewhere.

“Small business hiring reallystarted to slow in April and I attribute some of this to tariffs and the higher cost of doing business that small companies are much less able to absorb,” Peter Boockvar, chief investment officer at One Point BFG Wealth Partners, wrote in a note.

“The natural reaction is to cut costs elsewhere and we know that labor is their biggest cost,” Boockvar added.

The intrigue:

Bloomberg recently reported that there are more small businesses filing for bankruptcy under a special federal program this year than at any point in the program’s six-year history.

Subchapter V filings, which allow firms to shed debt faster and cheaper, are up 8% from last year, according to data from Epiq Bankruptcy Analytics.

Chapter 11 filings — a process used by larger businesses — are up roughly 1% over the same time frame.

Threat level:

Main Street is bearing the brunt of an economic slowdown in ways that might make it even harder for small shops to compete with larger companies.

One bright spot: Despite that pain, applications to start new businesses — ones likely to employ other people — remain notably higher than in pre-pandemic times, according to the latest data available from the Census Bureau.

What to watch:

The Trump administration shrugged off the ADP data that indicated a hiring bust. Commerce Secretary Howard Lutnick told CNBC that the cuts were due to factors unrelated to tariffs, like immigration crackdowns.

That hints at a debate among monetary policymakers, who are trying to gauge how much weak jobs growth is a byproduct of fewer available workers.

But ADP had earlier told reporters that small businesses generally had less demand for workers — not that staff weren’t available for hire.

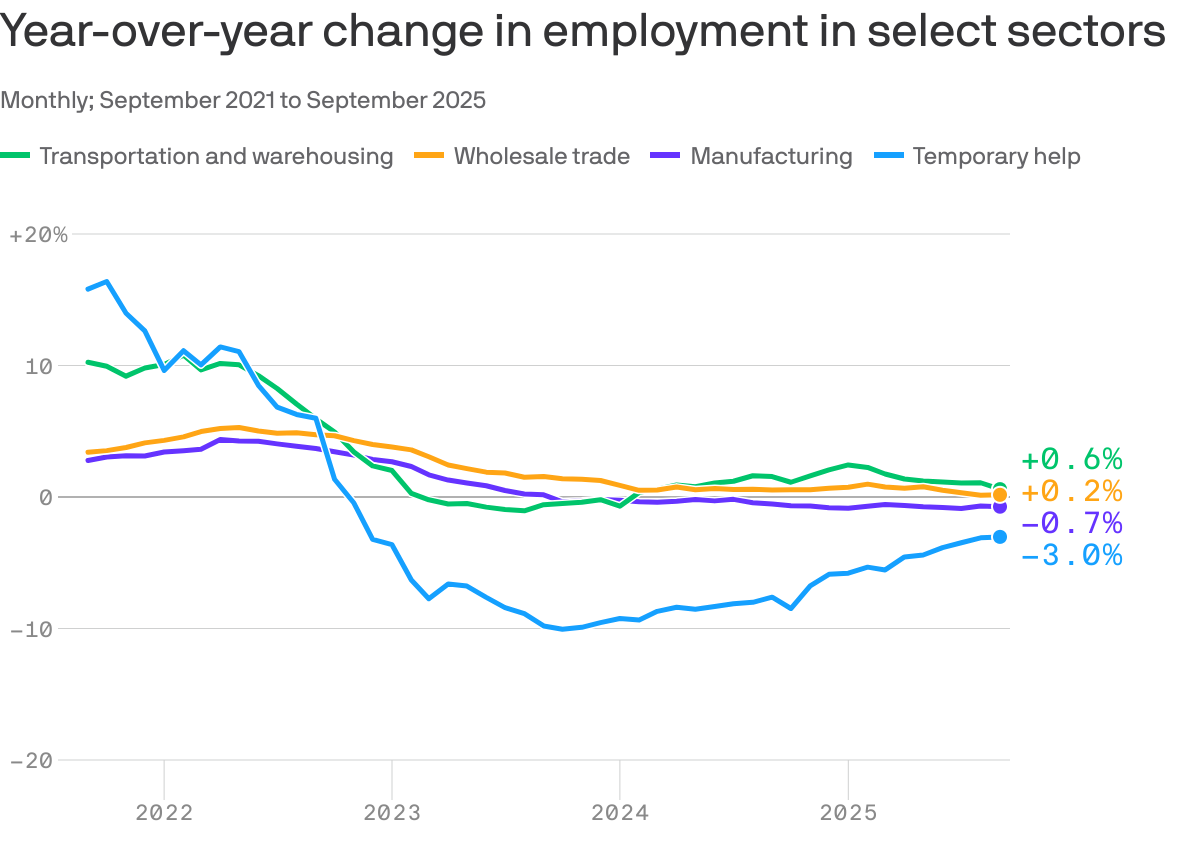

For an economy that’s rapidly expanding, the usual drivers of job creation sure aren’t carrying their weight.

Why it matters:

Anemic job growth in key sectors is a sign that there is more underlying weakness in worker demand than the low unemployment rate might suggest.

It makes for a weaker starting point, as companies see new opportunities around the corner to use AI to automate their work.

It’s not a new trend: These sectors showed weak job creation or outright job losses for the last couple of years of the Biden administration.

But it is striking that a GDP surge fueled by data center and AI investment hasn’t been enough to generate more robust hiring.

By the numbers:

Overall employment is up 0.8% over the 12 months ended in September, but the hiring has been driven in significant part by health care, state and local government, and other less cyclical sectors.

Manufacturing employment is down 0.7% over the last 12 months. Tariffs are weighing on the sector, but its job losses long predate the Trump trade wars, with year-over-year job losses for more than two years.

Temporary help employment, which tends to be a volatile indicator underlying growth trends, is down 3%. It has been losing jobs for three consecutive years.

Two other sectors that tend to correlate with overall economic momentum, transportation and warehousing and wholesale trade, are also adding jobs at rates below that of overall job growth (0.6% and 0.2%, respectively).

Stunning stat:

As Bloomberg flagged, two sectors — health care and social assistance, and leisure and hospitality — accounted for more than 100% of net job gains so far in 2025.

Excluding those sectors, employment dropped by 6,000 jobs in the first nine months of the year.

Zoom out:

There’s not much reason to think these numbers are driven by AI-related opportunities for companies to increase productivity and rely on fewer human workers, particularly given that the phenomenon isn’t new.

But it is more plausible that seeing such opportunities on the horizon has made companies more reluctant to hire in the absence of overwhelming need.

BlackRock chief investment officer for global fixed income Rick Rieder wrote in a note after last week’s jobs report that “what we think we are seeing now is … essentially a hiring pause in anticipation of AI.”

Of note:

A report out this morning from the McKinsey Global Institute finds that AI and robotics technologies could, in theory, automate 57% of U.S. work hours.

“AI will not make most human skills obsolete, but it will change how they are used,” the authors find. “As AI takes on common tasks, people will apply their skills in new contexts,” they write, such as less time researching and preparing documents and more time framing questions and interpreting results.

The bottom line:

Beneath the headline numbers, there is some good reason that attitudes toward the job market are glum.

Layoff trends in 2025 indicate an increase in job cuts compared to 2024, with US employers announcing nearly 950,000 cuts through September, the highest number since 2020. Key drivers include cost-cutting measures, the strategic implementation of artificial intelligence (AI), and a cooling labor market.

Key Trends

Elevated Numbers: Total US job cuts through October 2025 were over one million, a 65% increase from the same period in 2024. October 2025 had the highest number of layoffs for that month in 22 years.

AI as a Primary Driver: AI adoption is a leading cause for job cuts as companies restructure for efficiency and reallocate resources. Companies like Amazon and Intel have cited AI as a reason for significant workforce reductions.

“Forever Layoffs”: A new trend involves smaller, more regular rounds of layoffs (fewer than 50 people) that create ongoing worker anxiety and impact company culture. These rolling cuts often stay out of headlines but contribute significantly to the overall job cuts.

Method of Notification: The process is becoming more impersonal, with many employees being notified of their termination via email or phone call rather than in-person meetings.

Hiring Slowdown: Alongside the layoffs, there has been a sharp drop in hiring plans, with planned hires for the year at their lowest level since 2011.

Affected Industries

While tech has been significantly impacted since late 2022, other industries are also facing substantial cuts in 2025:

Technology: Remains a leading sector for cuts as companies continue to restructure after pandemic-era overhiring and focus on AI.

Retail and Warehousing: Companies like Target and UPS are cutting thousands of jobs due to changing consumer demands, automation, and a push for efficiency.

Energy and Manufacturing: Oil giants such as Chevron and BP are making cuts as part of cost-reduction strategies and market consolidation.

Finance and Consulting: Firms like PwC and Morgan Stanley are trimming staff, citing factors like low attrition rates and the need to realign resources.

Media and Communications: Companies like CNN and the Washington Post have made cuts to pivot toward digital services and reduce costs.

Economic Context

The overall U.S. labor market remains relatively healthy despite the uptick in layoffs, though it is showing signs of cooling. The unemployment rate has inched up, and consumer sentiment has declined. The Federal Reserve is monitoring the situation and has implemented interest rate cuts to help stabilize the job market.

Hospital financial and operational performance could be threatened by a trend showing a growth in the cost of expenses outpacing that of revenue, according to a Kaufman Hall National Hospital Flash Report.

“While performance has generally been strong this year, profitability has decreased slightly over the past few months. Bad debt and charity care also continue to rise. In addition, operating margins for health systems are about one percent lower than hospital margins. This points to potential challenges for hospitals and health systems to weather future uncertainty,” said Erik Swanson, managing director and group leader, Data and Analytics, at Kaufman Hall.

WHY THIS MATTERS

What the report shows is that hospital performance has softened in recent months.

While patient volumes and revenues are trending upward, bad debt and charity care are also elevated.

Expense growth is outpacing revenue growth, with non-labor expenses putting pressure on hospitals. Supplies are up 26% compared to 2022, and drugs costs are up 31% compared to 2022.

Margins have improved over prior years, though there has been some softening in recent months. Given an uncertain future outlook, many hospitals are taking steps to build long-term resiliency, the report said.

Operating margins in August 2024 were 4.6% but fell to 5% in December 2024. Starting in January, margins jumped to 6.9% and remained in the 6.2% range until this past June, when they fell to 5.5% and in July, 5.3%.

Profitability is down from 48% in July 2024 to 27% this year.

THE LARGER TREND

Data for the report came from more than 1,300 hospitals sampled on a monthly basis from Strata Decision Technology.

The sample of hospitals for the report represents all types of hospitals in the United States, from large academic to small critical access hospitals, geographically and by bed size.

Kaufman Hall, a Vizient company, provides advisory services and management consulting.

The U.S. health care industry is approaching a critical inflection point, according to veteran health care strategist Paul Keckley. In a candid and thought-provoking keynote at the 2025 Healthcare Marketing & Physician Strategies Summit (HMPS) in Orlando, Keckley outlined the challenges and potential opportunities health care leaders must navigate in an era of unprecedented economic uncertainty, regulatory disruption, and consumer discontent.

Drawing on decades of policy experience and his signature candid style, Keckley delivered a sobering yet actionable assessment of where the industry stands and what lies ahead.

Paul Keckley, PhD, health care research and policy expert and managing editor of The Keckley Report

Health care now accounts for a staggering 28 percent of the federal budget, with Medicaid expenditures alone ranging from the low 20s to 34 percent of individual state budgets. Despite its fiscal significance, Keckley points out that health care remains “not really a system, but a collection of independent sectors that cohabit the economy.”

In the article that follows, Keckley warns of a reckoning for those who remain entrenched in legacy assumptions. On the flip side, he notes, “The future is going to be built by those who understand the consumer, embrace transparency, and adapt to the realities of a post-institutional world.”

A Fractured System in a Fractured Economy

Fragmentation complicates any effort to meaningfully address rising costs or care quality. It also heightens the stakes in a political climate marked by what Keckley termed “MAGA, DOGE, and MAHA” factions, shorthand for various ideological forces shaping health care policy under the Trump 2.0 administration.

Meanwhile, macroeconomic conditions are only adding to the strain. At the time of Keckley’s address, the S&P 500 was down 8 percent, the Dow down 10 percent, and inflationary pressures were squeezing both provider margins and household budgets.

“Economic uncertainty is not just about Wall Street,” Keckley warns. “It’s about kitchen-table economics — how households decide between paying for care or paying the cable bill.”

Traditional Forecasting Is Failing

One of Keckley’s key messages was that conventional methods of strategic planning in health care, based on lagging indicators like utilization rates and demographics, are no longer sufficient. Instead, leaders must increasingly look to external forces such as capital markets, regulatory volatility, and consumer behavior.

“Think outside-in,” he urges. “Forces outside health care are shaping its future more than forces within.”

He encourages health systems to go beyond isolated market studies and adopt holistic scenario planning that considers clinical innovation, workforce shifts, AI and tech disruption, and capital availability as interconnected variables.

Affordability and Accountability: The Hospital Reckoning

Keckley pulls no punches in addressing the mounting criticism of hospitals on Capitol Hill, particularly not-for-profit health systems. Public perception is faltering, with hospital pricing increasing faster than other categories in health care and only a third of providers in full compliance with price transparency rules.

“Economic uncertainty is not just about Wall Street. It’s about kitchen-table economics — how households decide between paying for care or paying the cable bill.”

“We have to get honest about trust, transparency, and affordability,” he says. “I’ve been in 11 system strategy sessions this year. Only one even mentioned affordability on their website, and none defined it.”

Keckley also predicts that popular regulatory targets like site-neutral payments, the 340B program, and nonprofit tax exemptions will face intensified scrutiny.

“Hospitals are no longer viewed as sacred institutions,” he says. “They’re being seen as part of the problem, especially by younger, more educated, and more skeptical Americans.”

The Consumer Awakens

Perhaps the most urgent shift Keckley outlines is the redefinition of the health care consumer. “We call them patients,” he says, “but they are consumers. And they are not happy.”

Keckley cites polling data showing that two out of three Americans believe the health care system needs to be rebuilt from the ground up. Roughly 40 percent of U.S. households have at least one unpaid medical bill, with many choosing intentionally not to pay. Among Gen Y and younger households, dissatisfaction is particularly acute.

“[Consumers] expect digital, personalized, seamless experiences — and they don’t understand why health care can’t deliver.”

These consumers aren’t just passive recipients of care; they’re voters, payers, and critics. With 14 percent of health care spending now coming directly from households, Keckley argues, health systems must engage consumers with the same sophistication that retail and tech companies use.

“They expect digital, personalized, seamless experiences — and they don’t understand why health care can’t deliver.”

Tech Disruption Is Real

Keckley underscores the transformative potential of AI and emerging clinical technologies, noting that in the next five years, more than 60 GLP-1-like therapeutic innovations could come to market. But the deeper disruption, he warns, is likely to come from outside the traditional industry.

Citing his own son’s work at Microsoft, Keckley envisions a future where a consumer’s smartphone, not a provider or insurer, is the true hub of health information. “Health care data will be consumer-controlled. That’s where this is headed.”

The takeaway for providers: Embrace data interoperability and consumer-centric technology now, or risk irrelevance. “The Amazons and Apples of the world are not waiting for CMS to set the rules,” Keckley says.

Capital, Consolidation, and Private Equity

Capital constraints and the shifting role of private equity also featured prominently in Keckley’s remarks. With declining non-operating revenue and shrinking federal dollars, some health systems increasingly rely on investor-backed funding.

But this comes with reputational and operational risks. While PE investments have been beneficial to shareholders, Keckley says, they’ve also produced “some pretty dire results for consumers” — particularly in post-acute care and physician practice consolidation.

“Policymakers are watching,” he says. “Expect legislation that will limit or redefine what private equity can do in health care.”

Politics and Optics: Navigating the Policy Minefield

In the regulatory arena, Keckley emphasizes that perception often matters more than substance. “Optics matter often more than the policy itself,” he says.

He cautions health leaders not to expect sweeping policy reform but to brace for “de jure chaos” as the current administration focuses on symbolic populist moves — cutting executive compensation, promoting price transparency, and attacking nonprofit tax exemptions.

With the 2026 midterm elections looming large, Keckley predicts a wave of executive orders and rhetorical grandstanding. But substantive policy change will be incremental and unpredictable.

“Don’t wait for a rescue from Washington. The future is going to be built by those who understand the consumer, embrace transparency, and adapt to the realities of a post-institutional world.”

The Workforce Crisis That Wasn’t Solved

Keckley also addresses the persistent shortage of health care workers and the failure of Title V of the ACA, which had promised to modernize the workforce through new team-based models. “Our guilds didn’t want it,” Keckley notes, bluntly. “So nothing happened.”

He argues that states, not the federal government, will drive the next chapter of workforce reform, expanding the scope of practice for pharmacists, nurse practitioners, and even lay caregivers, particularly in behavioral health and primary care.

What Should Leaders Do Now?

Keckley closed his keynote with a challenge for marketers and strategists: Get serious about defining affordability, understand capital markets, and stop defaulting to legacy assumptions.

“Don’t wait for a rescue from Washington,” he says. “The future is going to be built by those who understand the consumer, embrace transparency, and adapt to the realities of a post-institutional world.”

He encouraged leaders to monitor shifting federal org charts, track state-level policy moves, and scenario-plan for a future where trust, access, and consumer empowerment define success.

Conclusion: A Health Care Reckoning in the Making

Keckley’s keynote was more than a policy forecast; it was a wake-up call. In a landscape shaped by economic headwinds, political volatility, and consumer rebellion, health care leaders can no longer afford to stay in their lane. They must engage, adapt, and transform, or risk becoming casualties of a system under siege.

“Health care is not just one of 11 big industries,” Keckley says. “It’s the one that touches everyone. And right now, no one is giving us a standing ovation.”