https://www.bloomberg.com/news/articles/2017-09-19/senate-gop-has-12-days-to-repeal-obamacare-and-no-room-for-error

Senate Republicans making one last-ditch effort to repeal Obamacare have the daunting task of assembling 50 votes for an emotionally charged bill with limited details on how it would work, what it would cost and how it would affect health coverage — all in 12 days.

They need to act by Sept. 30 to use a fast-track procedure that prevents Democrats from blocking it, but the deadline doesn’t leave enough time to get a full analysis of the bill’s effects from the Congressional Budget Office. The measure would face parliamentary challenges that could force leaders to strip out provisions favored by conservatives. Several Republicans are still withholding their support or rejecting it outright.

And even if Republicans manage to get it through the Senate by Sept. 30, the House would have to accept it without changing a single comma.

Most Senate Republicans are still trying to figure out what it’s in the bill, which was authored by Republicans Lindsey Graham of South Carolina and Bill Cassidy of Louisiana. Until the past few days, most assumed that GOP leaders had no interest in reviving the Obamacare repeal effort after their high-profile failure to pass a measure this summer.

Republican Senator Steve Daines of Montana said he’s still trying to figure out how the bill will affect his state and wants to hear what GOP leaders say at a closed-door lunch Tuesday.

‘Active Discussion’

“It will be a very active discussion,” he said.

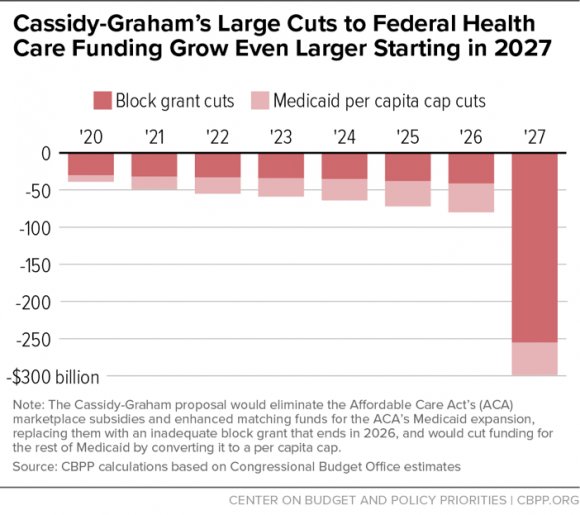

The new repeal bill would replace the Affordable Care Act’s insurance subsidies with block grants to states, which would decide how to help people get health coverage. The measure would end Obamacare’s requirements that individuals obtain health insurance and that most employers provide it to their workers, and it would give states flexibility to address the needs of people with pre-existing medical conditions.

But lawmakers won’t have much more information about the legislation by the time the Senate would have to vote. The CBO said Monday it will offer a partial assessment of the measure early next week, but that it won’t have estimates of its effects on the deficit, health-insurance coverage or premiums for at least several weeks. That could make it hard to win over several Republicans who opposed previous versions of repeal legislation.

So far, President Donald Trump has suggested he’d support the bill, but he hasn’t thrown his full weight behind it.

Majority Leader Mitch McConnell has told senators he would bring up the bill if it had 50 votes, and under fast-track rules he could do so at any time before Sept. 30. That’s the end of the government’s fiscal year, when the rules expire and the GOP would have to start over.

Several Holdouts

Republicans can only lose two votes in the 52-48 Senate and still pass the measure, with Vice President Mike Pence’s tie-breaker. There are at least four holdouts, and getting any of them to back the measure would require the senators to change their past positions. Pence, who would cast the potentially deciding vote, will return to Washington from New York Tuesday, where he’s been taking part in United Nations General Assembly events, to attend Senate GOP lunches.

Republican Rand Paul of Kentucky said Monday he’s opposed to the Graham-Cassidy bill, saying it doesn’t go far enough. John McCain of Arizona said he’s “not supportive” yet, citing the rushed legislative process.

Two other Republicans — Susan Collins of Maine and Lisa Murkowski of Alaska — have voted against every repeal bill considered this year in the Senate, citing cuts to Medicaid and Planned Parenthood as well as provisions that would erode protections for those with pre-existing conditions. The Graham-Cassidy bill contains similar provisions on those three areas.

“I’m concerned about what the effect would be on coverage, on Medicaid spending in my state, on the fundamental changes in Medicaid that would be made,” Collins told reporters Monday evening.

She said that Maine’s hospital association has calculated the state would lose $1 billion in federal health spending over a decade compared to current law.

“That’s obviously of great concern to me,” she added.

Hard Sell

Murkowski is getting a hard sell from Republican backers of the bill.

“What I’m trying to figure out is the impact to my state,” Murkowski told reporters Monday. “There are some formulas at play with different pots of money with different allocations and different percentages, so it is not clear.”

McCain, who is close friends with Graham, cast the deciding vote to sink an earlier repeal bill in late July when he made a dramatic return to the Senate after a brain cancer diagnosis. At the time, he made an eloquent plea for colleagues to work with Democrats and use regular legislative procedures instead of trying to jam it through on a partisan basis.

John Weaver, a former top adviser to McCain, said supporting Graham-Cassidy would require the Arizona senator to renege on his word.

‘Fair Process’

“I cannot imagine Senator McCain turning his back not only on his word, but also on millions of Americans who would lose health care coverage, despite intense lobbying by his best friend,” Weaver said in an email. “Graham-Cassidy, if truly attempted to pass, will bypass every standard of transparency and inclusion important to people who care about fair process.”

Despite the obstacles, the bill’s backers are putting on a good face about the prospects.

“We’re making progress on it,” said Republican Senator Ron Johnson of Wisconsin. “I’m still cautiously optimistic, but there are a lot of moving parts.” Johnson is planning a Sept. 26 hearing on the measure in the Homeland Security and Governmental Affairs Committee, which he leads. The Senate Finance Committee is planning its own hearing Sept. 25 on the measure.

“There’s a lot of interest,” Senator Pat Toomey of Pennsylvania said Monday. “Those guys have done some very good work.”

A number of Republicans are still pushing for changes to the bill, so the final version may evolve. It’s also subject to parliamentary challenges under the reconciliation process being used to circumvent the 60-vote threshold in the Senate. That could allow Democrats to strike provisions that take aim at Obamacare’s regulatory structure.

Last Chance

If it passed the Senate, the House would have to pass the bill without any changes. House Speaker Paul Ryan said Monday that the measure is Republicans’ last best chance to repeal Obamacare.

“We want them to pass this, we’re encouraging them to pass this,” Ryan told reporters at a news conference in Wisconsin. “It’s our best, last chance of getting repeal and replace done.”

But that won’t be easy either. The measure strives to equalize Medicaid funding between states, which means that some House Republicans from Medicaid expansion states could find it hard to support. That includes states like New York and California, which stand to lose federal funds under Graham-Cassidy. Those states have only Democratic senators, but have some GOP House members.

Another Run

In some ways, it’s remarkable that Republicans are mounting another run at repeal.

Two months ago, Majority Leader Mitch McConnell’s effort to pass a replacement with only Republican support suffered a spectacular defeat in the Senate. When members of the Senate health committee then began working on a bipartisan plan to shore up Obamacare, Graham and Cassidy revved up a new bid to get their GOP-only bill to the Senate floor.

Graham and Cassidy are hoping to channel the GOP’s embarrassment at failing to repeal Obamacare this summer after seven years of promising to do so. But Paul said Monday this legislation shouldn’t be treated like a “kidney stone” you pass “just to get rid of it.”

Despite all the obstacles, Democrats quickly geared up for another campaign against repeal, warning that the latest bill is a serious threat.

“This bill is worse than the last bill,” Senate Democratic leader Chuck Schumer of New York told reporters Monday. “It will slash Medicaid, get rid of pre-existing conditions. It’s very, very bad.”