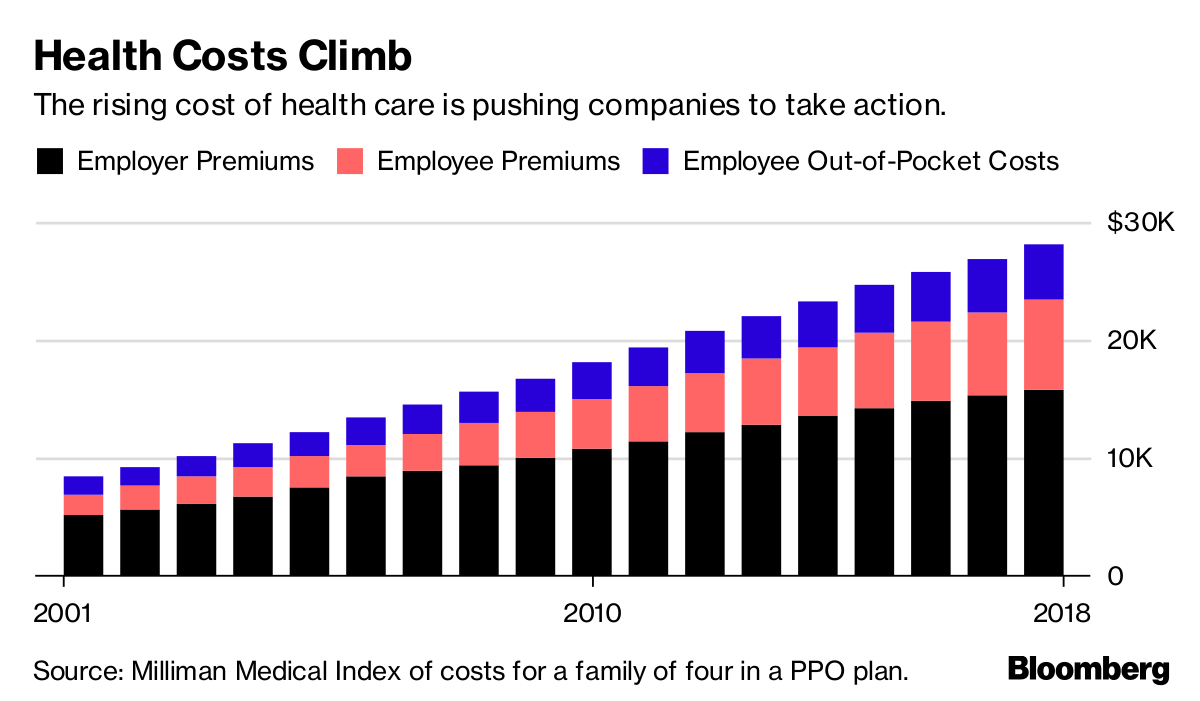

Each year, for well over a decade, more people have faced higher health insurance deductibles. The theory goes like this: The more of your own money that you have to spend on health care, the more careful you will be — buying only necessary care, purging waste from the system.

But that theory doesn’t fully mesh with reality: High deductibles aren’t working as intended.

A body of research — including randomized studies — shows that people do in fact cut back on care when they have to spend more for it. The problem is that they don’t cut only wasteful care. They also forgo the necessary kind. This, too, is well documented, including with randomized studies.

People don’t know what care they need, which is why they consult doctors. There’s nothing inherently wrong with relying on doctors for medical advice. They’re trained experts, after all. But it runs counter to the growing trend to encourage people to make their own judgments about which care, at what level of quality, is worth the price — in other words, to shop for care.

Shopping for health care may sound ludicrous on its face — and sometimes is. People don’t have time, let alone the cognitive focus, to shop for treatments while having a heart attack, or during any other emergency.

But not all care we need is related to an emergency. Some care is elective, and so potentially “shoppable.” Scholars have estimated that as much as 30 or 40 percent of care falls into this category. It includes things like elective joint replacements and routine checkups.

And yet very few people shop for this type of care, even when they’re on the hook for the bill. Maybe it’s just too complex. Even when price transparency tools are offered to consumers to make it easier, almost nobody uses those them.

A National Bureau of Economic Research working paper published Monday adds a lot more to the story. The study team from Yale, Harvard and Columbia considered a health care service that should be among the easiest to shop for: nonemergency, outpatient, lower-limb M.R.I.s.

This is the kind of imaging you might get if you’re having some trouble with a knee or ankle, but not bad enough to need the image right away.

The study, which focused on more than 50,000 adults between 19 and 64, strongly suggests that people get their M.R.I.s wherever their doctors advise, with little regard to price. The authors didn’t eavesdrop on patients, so they don’t know exactly what the doctors said about where to get M.R.I.s.

But the identity of a patient’s orthopedist explains a lot more about where he or she got her M.R.I. than any other factor considered, including price and distance. Less than 1 percent of patients in the study sample availed themselves of a price comparison tool to shop for M.R.I.s before receiving one.

By this reasoning, the authors concluded that doctors sent people to more expensive locations than they had to. On the way to their M.R.I., patients drove by an average of six other places where the procedure could have been done more cheaply.

“Many patients are going to very expensive providers when lower-price options with equal quality are available,” said Zack Cooper, a health economist at Yale and a co-author of the study. Though patients seem to follow the advice of their doctors on where to go, their doctors don’t have all the information on hand to make the best decisions for the patient either.

There are over 15 M.R.I. locations within a half-hour drive for most patients. As with many health care services, there is a large variation of prices across these locations, which means a tremendous opportunity to save money by selecting lower-priced ones. In one large, urban market, prices for the procedure are as low as about $280 and as high as about $2,100.

If patients went to the lowest-cost M.R.I. that was no farther than they already drove, they’d save 36 percent. Savings rise if they’re willing to travel farther. Within an hour’s drive, for example, savings of 55 percent are available. Savings are split between patient and insurer, depending on cost sharing. On average, patients pay just over $300 toward the cost of the procedure.

There is no evidence that the quality of low- and high-priced M.R.I.s differs, at least enough to be clinically meaningful. The study found that virtually none of the M.R.I.s at any price level had to be repeated — strong evidence that the doctors relying on them are satisfied even with the lower-priced images.

At almost $1,500, the average price of a hospital M.R.I. is more than double that of one at an imaging center. The study found that doctors who work for hospitals (rather than independently) are more likely to send their patients for more expensive hospital-based imaging. Just getting all patients to use M.R.I.s that are no farther away and not in a hospital could save 16 percent.

What this latest study suggests, in the context of other studies, is that if people can’t shop for elective M.R.I.s, there’s hardly a chance they are going to do so with other health care procedures that are more complicated and variable.

Even if 40 percent of health care is shoppable, people are not shopping. What seems likelier to work is doing more to influence what doctors advise.

For example, we could provide physicians with price, quality and distance information for the services they recommend. Further, with financial bonuses, we could give physicians (instead of, or in addition to, patients) some incentive to identify and suggest lower-cost care. An alternative approach is for insurers to refuse to pay more than a reasonable price — like the market-average — for a health care service, though patients could pay the difference if they prefer a higher-priced provider.

Leaving decisions solely to patients, and just making them spend more of their own money, doesn’t work.