The Trump administration is expected to spell out its intentions for Medicare Advantage soon — a program that enrolls about half of U.S. seniors but has drawn intensifying criticism for costing the government too much.

Why it matters:

Centers for Medicare and Medicaid Services chief Mehmet Oz called the system “upside down” during his confirmation hearings, hinting at possible changes to the way the federal government pays and regulates plans.

Any big changes would be a departure from a history of friendly treatment from Republican administrations.

Those could become apparent in the proposed 2027 Medicare Advantage rule, which may come out before the end of this year.

How it works:

Many privately run Medicare plans charge no monthly premium and provide supplemental benefits that traditional Medicare doesn’t cover,like dental coverage and help paying for over-the-counter drugs.

The program was created on the premise that private insurers could manage care better and at a lower price point than the federal government.

But some insurers have since drawn fire for categorizing patients as sicker than they are to get higher payments, and for overly complicated pretreatment reviews.

Advisors to Congress projected the federal government would spend about $84 billion more on Medicare Advantage enrollees this year than for people in traditional Medicare. (Insurers say the advisors’ methodology is flawed.)

Oz has a history of promoting Medicare Advantage plans on his popular television show and advocating for an “MA for All” policy.

But he’s been more openly skeptical since joining the administration, as a growing cadre of GOP policymakers ask questions about the program’s finances and insurers’ role in driving up costs.

“I came both to celebrate what you’re trying to do, but also be honest about some of the issues that we’re seeing at CMS,” Oz said at the industry lobby’s conference last month.

Oz believes choice and competition are needed for a strong Medicare program, but also that CMS has a responsibility to keep “program payments fair, transparent, and grounded in data,” Catherine Howden, the agency’s director of media relations, told Axios in response to a request for comment.

This is an opportunity for Medicare Advantage insurers to have some strategic conversations with CMS about Oz’s vision for the program, said Daniel Fellenbaum, senior director at Penta Group.

UnitedHealthcare, Humana and Aetna are the three biggest Medicare Advantage insurers and cover more than 20 million seniors combined.

Where it stands:

This year CMS announced what it termed an “aggressive” strategy to increase audits of the diagnoses Medicare Advantage plans document for enrollees, which could claw back money from insurers.

Medicare’s Innovation Center said it’s working on pilot programs that could change the way thegovernment pays the plans.

Industry onlookers are also expecting the administration to propose changes to the star ratings system, which measures Medicare Advantage plan quality and dictates bonus payments to plans.

What they’re saying:

Insurers and advocates of private Medicare plans remain optimistic that Oz has their best interests at heart.

“He seems to stress good oversight and holding the program to high standards without losing sight of what’s working for seniors,” said Susan Reilly, vice president of communications at Better Medicare Alliance.

Insurance trade group AHIP welcomes “constructive, data-driven conversations with policymakers on actions that strengthen Medicare Advantage,” CEO Mike Tuffin said in a statement to Axios.

AHIP wants a focus on stability in the program after several years of medical costs increasing faster than Medicare Advantage payment, it said.

Reality check:

The 2026 update to plan payment, the first of this administration, is better than anticipated for insurers, giving them more than $25 billion increase in federal payments.

The Trump administration also struck voluntary agreements with insurers to simplify the rules for authorizing procedures and treatments ahead of time, rather than using its regulatory authority to require changes.

“We hear rhetoric talking tough on MA, but we’ve not seen them put that into actual reality,” said Chris Meekins, managing director at Raymond James.

Any big policy changes next year would also become apparent to seniors right before the midterm elections. Bigger policy swings from the administration might be more likely to go into effect for 2028, Meekins said.

What we’re watching:

President Trump has been vocal about his distaste for health insurance companies on social media lately as Congress debates extending enhanced premium subsidies for Obamacare coverage.

That ire could seep into how he directs his administration to regulate Medicare Advantage.

Wall Street reacts to the failed ACA subsidy extension — and to the president’s swipe at “money sucking insurance companies.”

Wall Street got the jitters yesterday after Donald Trump’s pointed remarks about “money sucking insurance companies” and a Congressional deal that failed to extend the enhanced subsidies under the Affordable Care Act (ACA) marketplace plans. According to one market analysis, shares of Centene (CNC) plunged about 8.15% in pre-opening trade, while competitors such as Molina (MOH) fell 4.6%, Elevance (ELV) dropped 3.7%, UnitedHealth Group (UNH) slipped 1.9% and Humana (HUM) declined 1.45%.

Why the sell-off? Because the enhanced ACA subsidies — which reduce premiums for some marketplace enrollees — expire at the end of the year and without renewal, an estimated 3.8 million people could lose coverage, and premiums would rise significantly for others. Insurers that rely on the stability and growing enrollee base of the ACA marketplace face heightened risk when that funding is in question – especially when the dollars are guaranteed – like when they are shoveled out from the federal government.

Still, it’s worth noting that the ACA marketplace business is not the primary profit engine for most large payers. Their bigger gains typically come from taxpayer-funded programs like Medicare Advantage, Medicaid managed-care contracts and veterans’ / VA contracts.

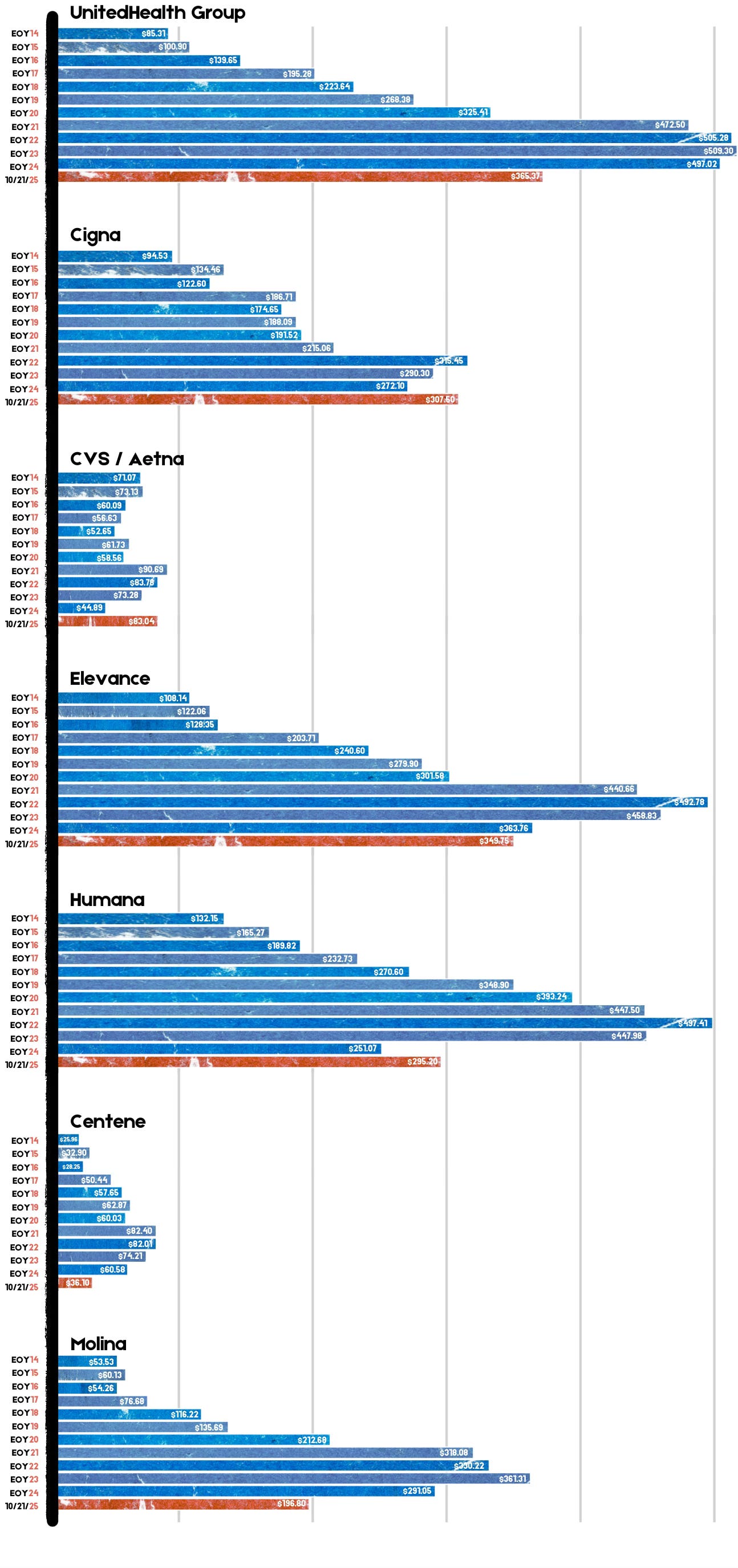

Here’s how five of the major players fared in 2024 profits:

Centene: $3.2 billion (+590% since 2014)

UnitedHealth Group: $32.2 billion (+214% since 2014)

Elevance: $9.1 billion (+78% since 2014)

Humana: $2.6 billion (+8.3% since 2014)

Molina: $1.18 billion (+780% since 2014)

Because most of their gains have not come from ACA exchange plans (and especially not the thin margin employer market) but through their other government-subsidized businesses, investors can have some certainty their investments in those companies are still largely safe and Big Insurance will be able to weather this storm.

For instance, the industry has always been able to strongarm rough patches in the consumer market – as long as they can stave off any meaningful changes to their bread and butter taxpayer-funded programs. As we reported last month, the industry’s outside PR and lobbying friends – Better Medicare Alliance and Medicare Advantage Majority – have hit the airwaves and the halls of Congress to halt the advancement of the No UPCODE Act. The bipartisan bill, sponsored by Senators Bill Cassidy (R-LA) and Jeff Merkley (D-OR) would end wasteful, fraudulent practices in Big Insurance’s Medicare Advantage businesses that funnel taxpayer money into the pockets of industry executives and Wall Street shareholders and could save taxpayers as much as $124 billion over the next decade and keep the Medicare Trust Fund solvent for years longer.

As of this morning, insurers seem to be fairing better. Centene, UnitedHealth Group, Elevance, Humana and Molina are all back in the green.

As open enrollment begins and Congress remains deadlocked on whether to extend the ACA’s enhanced premium subsidies, one question looms large: Where does all the money we pay for health coverage actually go?

It’s a fair question. Premiums and out-of-pocket costs have risen relentlessly over the past decade. Since the Affordable Care Act was fully implemented, the average premium for an ACA marketplace plan has doubled, and the average deductible for a Silver plan has increased by 92%. Every year, families pay more, yet the coverage often feels thinner.

What the Insurers Say

Health insurance companies routinely claim these increases simply reflect rising medical costs and higher utilization. For example, when justifying rate hikes in 2024, Cigna of Texas wrote:

“The increasing cost of medical and pharmacy services and supplies accounts for a sizable portion of the premium rate increases.”

But the financial filings of these same companies tell a different story.

What the Numbers Show

As Wendell Potter recently wrote, from 2014 to 2024 the seven largest publicly traded health insurance companies, UnitedHealth Group, CVS/Aetna, Cigna, Elevance (formerly Anthem), Humana, Centene, and Molina, reported that they collectively made more than half a trillion dollars in profits.

That’s money collected from individuals, employers and taxpayers for health coverage — dollars that didn’t go to medical care but instead flowed to corporate shareholders and executive bonuses. To put this in perspective, those profits alone could fund the enhanced ACA premium subsidies for another ten years, at an estimated cost of $350 billion.

Over the same period, these seven companies spent $146 billion buying back their own stock or, in other words, using premium dollars from patients and employers to boost share prices and executive compensation (the CEOs and many other top executives of big insurers are compensated primarily through stock grants and options).

Stock buybacks don’t lower premiums, expand networks, or improve care. They simply make investors and executives richer. If that same money had been reinvested in enrollees, it could have provided premium-free health coverage to more than 5 million families for an entire year, based on the average employer-sponsored plan cost of $27,000 in 2026.

Lobbying With Our Premium Dollars

Insurers aren’t just rewarding shareholders, they’re also shaping the political system that protects their profits. Since 2014, the seven largest insurers and their trade association, AHIP, have spent $618 million on lobbying.

That’s money that could have been used to lower out-of-pocket costs or improve patient care, but instead it’s spent to influence Congress and federal agencies to maintain the status quo.

The Real Problem — and the Real Solution

As the cost of health insurance continues to climb, politicians debate how to control those costs and expand coverage. But the truth is, there’s already enough money in the system to cover everyone. It’s just being siphoned off by insurance corporations for profits, lobbying, and stock buybacks.

Though some have been calling for less regulation of Big Insurance, that is not the answer and is partly how we ended up in this situation. Right now, Big Insurance is allowed to use premium dollars and tax dollars on things that do nothing to improve anyone’s health – such as stock buybacks and lobbying – instead of on medical care.

Rather than asking families and taxpayers to pay more, it’s time to demand accountability from insurers. At a minimum, they should not be allowed to use premium dollars, or taxpayer dollars, to enrich shareholders through stock buybacks (which wasn’t even legal until the 1980s) or lobby for policies that drive up costs.

If we want to contain health care costs, the first step is simple: Stop the profiteering by Big Insurance.

Elevance’s Anthem Blue Cross plans are joining Big Insurance’s latest profit play — cutting payments to hospitals and providers under the pretense of reducing patients’ out-of-pocket costs.

Anthem Blue Cross plans have joined UnitedHealth and Cigna in taking extreme measures to satisfy Wall Street but penalize hospitals and potentially thousands of doctors and physician groups that Anthem excludes from its provider networks.

What Anthem is proposing is not only extreme but brazen in that it goes way beyond what any managed care company I know of has ever undertaken to pad its bottom line by reducing patient choice. It wouldn’t just restrict access to certain providers, it would effectively eliminate access.

Anthem, which is owned by the for-profit corporation Elevance Health Inc., has notified hospitals in 11 of the 14 states where it operates that starting in January it will slash reimbursements by 10% every time a doctor who works in the hospital – but who is not in Anthem’s network – provides care to a patient enrolled in an Anthem health plan.

The move clearly will save Elevance money and help it meet its shareholders’ profit expectations, but it will be a potential nightmare and administrative expense for thousands of hospitals and outpatient facilities. And it could put many independent physician practices out of business.

As Fierce Healthcare reported Friday, Anthem will impose an administrative penalty equal to 10% of the allowed amount on a hospital or outpatient facility’s claims that include out-of-network providers. If those facilities don’t meet Anthem’s terms, they will be at risk of being dropped from Anthem’s network.

Anthem’s announcement comes on the heels of UnitedHealth’s disclosure to investors last month that it plans to dump thousands of doctors from its networks to boost profits. A UnitedHealth executive said during the company’s third quarter call with shareholders that there were too many doctors in the company’s network who were not aligned with UnitedHealth’s business model, which he called “value-based care.”

“We are moving to employed or contractually dedicated physicians wherever possible,” said Patrick Conway, CEO of UnitedHealth’s Optum division, which has bought hundreds of physician practices over the past several years. UnitedHealth is already the biggest employer of doctors in the country.

And last month, Cigna began reducing payments to many doctors automatically by resurrecting a practice called downcodingthat was banned by a federal court more than two decades ago. Cigna also is threatening to drop hundreds of hospitals and outpatient facilities operated by Tenet Health from its provider network next year.

The stock prices of all three insurers have been under pressure this year as shareholders have sold millions of their shares in reaction to what they consider bad news from the companies. Most investors consider increases in paid medical claims to be bad news and a threat to the value – and earnings potential – of their holdings.

Anthem claimed in its notice to hospitals and other facilities last month that it is implementing the new policy “to support patient care and to help reduce out-of-pocket expenses for our members.” The notice went on to say that, “As a participating facility in Anthem’s care provider network, your role in guiding members to in-network care providers is vital in ensuring members receive high-quality, cost-effective, and coordinated care.”

Sounds good, right? But how is a patient to know that the doctors in Anthem’s network are really the ones that truly deliver high-quality coordinated care? Could it be that the top priority of the insurer is to include providers in its network who agree, first and foremost, to reimbursement terms especially favorable to the insurer?

And for hospitals, this could lead to higher administrative costs in trying to figure out which doctors are available at any given time to treat an Anthem patient. A highly regarded anesthesiologist might be just fine – and available – to treat patients insured by Cigna or Aetna or Humana, but off limits to treat an Anthem-insured patient. The hospital will have to be especially vigilant to keep that doctor out of the operating room when an Anthem patient needs surgery. If it slips up the hospital could get booted out of Anthem’s network. The doctor, however, would not be able to bill the patient for any amount because of the federal No Surprises Act (NSA), which prohibits balance-billing.

Anthem’s claim that it is taking this action to reduce patients’ out-of-pocket expenses is especially rich when you remember that Anthem and other big insurers created the problem Anthem says it is seeking to address. Anthem, Cigna, UnitedHealth and other big insurers led what became an industry-wide strategy in the early 2000s to force as many of their health plan enrollees as possible – and as soon as possible – into high-deductible plans. That strategy was so successful that more than 100 millions Americans – the vast majority of whom have health insurance – are mired in medical debt.

Fierce Healthcare quoted an Elevance executive as saying that the new Anthem policy “was designed in response to provider behavior under the independent dispute resolution (IDR) process” established by the No Surprises Act. He said Anthem had seen “a consistent pattern of IDR being used as a ‘back-door payment channel’ for pricey, nonemergent procedures.”

But as HEALTH CARE un-covered reported recently, research is showing that insurers are manipulating the IDR process to their advantage by exploiting loopholes in the NSA. Doctors have told me that even when they prevail in a dispute, insurers often refuse to pay promptly, if at all, and they report long delays, repeated administrative hurdles, and in some cases outright nonpayment of arbitration awards. And a report published last week in Health Affairs describes the “hidden incentives” of insurers in the IDR process that the authors say add costs to health plans and beneficiaries “and the health care system at large.”

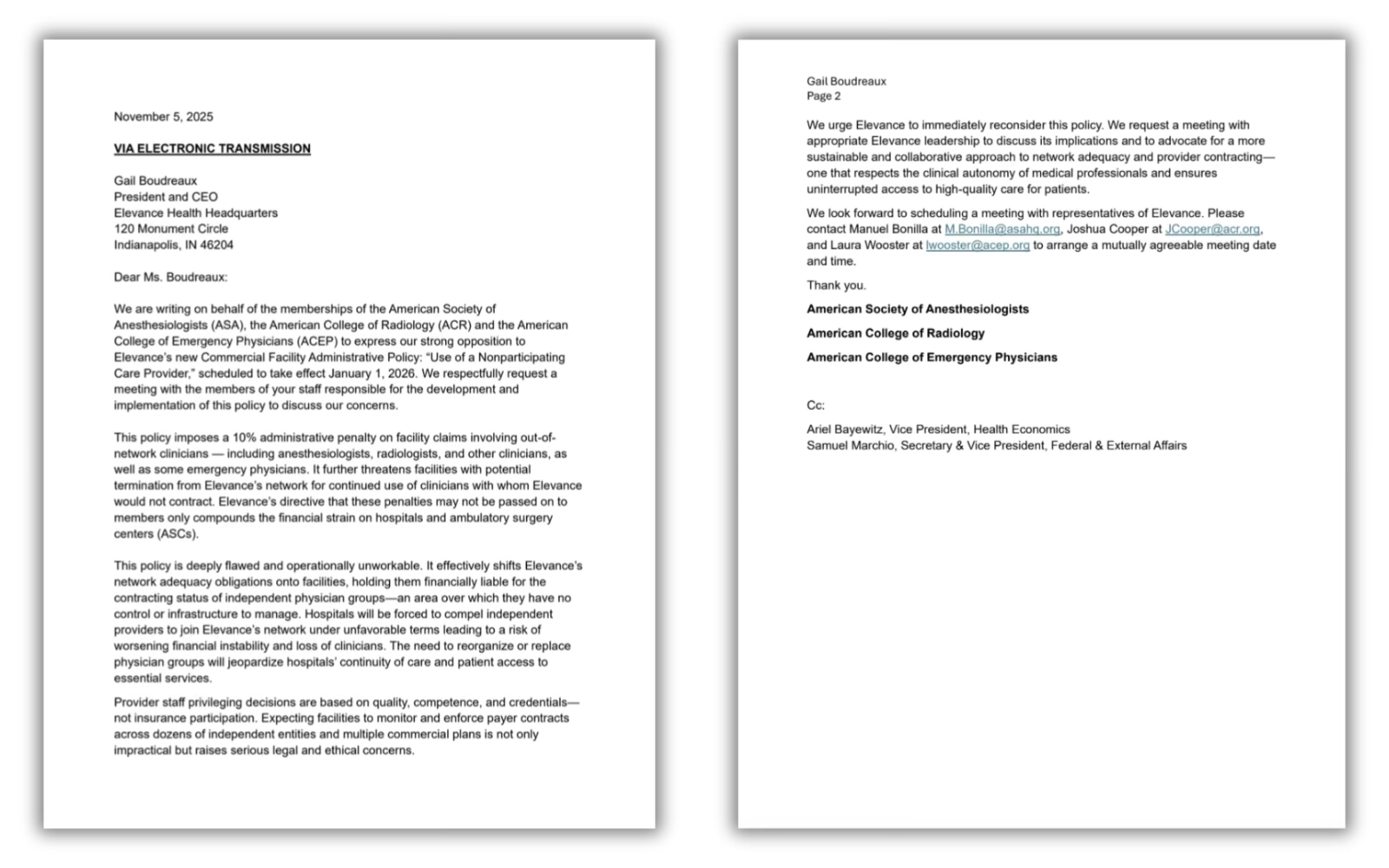

Independent practice physicians have begun raising alarms about Anthem’s new policy. And on Wednesday, medical societies representing thousands of doctors sent a letter to Elevance CEO Gail Boudreaux protesting Anthem’s plans and asking for a meeting.

Letter sent to Elevance CEO Gail Boudreaux, by the American Society of Anesthesiologists, American College of Radiology and American College of Emergency Physicians.

“This policy is deeply flawed and operationally unworkable,” they wrote. “It effectively shifts Elevance’s network adequacy obligations onto facilities, holding them financially liable for the contracting status of independent physician groups–an area over which they have no control or infrastructure to manage. Hospitals will be forced to compel independent providers to join Elevance’s network under unfavorable terms leading to a risk of worsening financial instability and the loss of clinicians. The need to reorganize or replace physician groups will jeopardize hospitals’ continuity of care and patient access to care.”

The letter went on to say that, “Expecting facilities to monitor and enforce payer contracts across dozens of independent entities and multiple commercial plans is not only impractical but raises serious legal and ethical concerns.”

If the doctors can’t persuade Boudreaux to ditch the new policy, people enrolled in Anthem plans who need care in a hospital or outpatient facility next year could face confusion and delays in getting that care, and the facilities currently in their network might be kicked out of it if they make any mistakes.

Doctors’ concern about Anthem’s policy cannot be dismissed as an overreaction to one company’s business decision. It poses an existential threat to physician practices that want to stay independent and not sell out to either a hospital system or an insurance company. If the other health insurers follow Anthem’s lead – and there is no reason to think they will not – the number of doctors in independent practice in the United States will dwindle to extinction. There aren’t many left as it is.

Because of the control Wall Street now has over the health insurance industry, Boudreaux is likely less concerned about physician autonomy than what investors think and want, and she is under the gun to get back into their good graces in a matter of months. Her company’s shares have lost a third of their value since the first of this year. If she can’t demonstrate that she’s getting Elevance back on track to profitable growth, she’ll be out of a job soon.

Lawmakers and regulators at all levels of government need to keep an eye on this and intervene if doctors and Anthem patients can’t change her mind.

The U.S. health system’s future is uncertain but outside forces will define its direction.

9 structural changes appear necessary to a transformed system of health that’s affordable, comprehensive and effective.

Last week, I had a 27-hour stay in a hospital emergency room waiting for an open bed and a morning at the food pantry loading boxes in anticipation of a possible SNAP program suspension surge. It wasn’t the week I expected. So much for plans!

Such is the case for health insurance coverage for millions in the U.S. as the federal government shutdown enters Week 6. Democrats are holding out for continuation of Affordable Care Act (ACA) insurance subsidies that enable 22 million to “buy” insurance cheaper, and Republicans are holding out for federal spending cuts reflected in the One Big Beautiful Act (July 2025) that included almost a trillion reduction in Medicaid appropriations thru 2036.

ACA subsidies at the heart of the shutdown successfully expanded coverage in tandem with Medicaid expansion but added to its costs and set in motion corporatization and consolidation in every sector of the health system. The pandemic exposed the structural divide between public health programs and local health systems, and insurance premium increases and prior authorization protocols precipitated hostility toward insurers and blame games between hospitals, insurers and drug companies for perpetual cost increases.

Having mediated discussions between the White House and industry trade groups as part of the ACA’s design (2009), I witnessed first hand the process of its development into law, the underlying assumptions on which it is based and the politics before and after its passage in March 2010. Its hanging chads were obvious. Its implementation stalled. Its potential to lower costs and improve quality never realized. It was a Plan disabled by special interests that rightly exploited its flaws and political brinksmanship that divided the country. But more fundamentally, it has failed to lower costs and improve affordability because it failed to integrate outside considerations—private capital, employers, technologies, clinical innovations and consumer finances—in its calculus.

Sixteen years later, healthcare is once again the eye of the economic storm. Insiders blame inconsistent regulatory enforcement and lack of adequate funding as root causes. Outsiders blame lack of cost controls. consolidation and disregard for affordability. Thus, while attention to subsidized insurance coverage and SNAP benefits might temporarily calm public waters, they’re not the solution.

All parties and all sides seem to agree the health system broken. For example, in my trustee surveys before planning sessions with Boards of health systems, medical groups and insurers, the finding is clear:

92% says the future of the U.S. health system in 7-10 years is fundamentally changed and not repeat of its past.

84% say their organizations are not prepared because short-term issues limit their ability to long-term planning.

Republicans think market forces will fix it. Democrats think federal policy will fix it. The public thinks it’s become Big Business that puts its interests before theirs. And the industry’s trade groups—AMA, AHA, AHIP, PhRMA, Adame, APHA, et al—face intense pressure from members adversely impacted by unwanted regulatory policies.

Few enjoy the luxury of long-term planning. That doesn’t excuse the need to address it. If a clear path to the system’s future is not built, incrementalism will enable its inevitable insolvency and forced re-construction.

What’s the solution? When comparing the U.S. health system to high performing systems in other high-income countries, these findings jump out:

All spend less on healthcare services and more on social services than the U.S.

All include government and privately-owned operators

All fund their systems primarily through a combination of federal appropriations and private payments by employers and citizens.

All pursue clinical standardization based on evidence.

All are dealing with funding constraints as their governments address competing priorities.

All are transitioning from episodic to chronic health as their populations age and healthiness erodes.

All are focused on workforce modernization and technologic innovations to lower costs and reduce demand for specialty services.

All enable private investment in their systems to increase competition and stimulate innovation.

All facilitate local/regional regulatory oversight to address distinctions in demand and resources.

All face with growing public dissatisfaction.

All are expensive to operate.

No system is perfect. None offers a copy-paste solution for U.S. taxpayers. And even if one seemed dramatically better, it would be a generational surge rooted in futility that welcome it.

What’s the answer? At the risk of oversimplicity, the future seems most likely built on these 9 structural changes:

Integrate social services (public health) with delivery.

Create comprehensive primary and preventive health gatekeeping inclusive of physical and behavioral health, nutrition, prophylactic dentistry and consumer education.

Rationalize specialty services and therapies to high value providers.

Incentivize responsible health behaviors across the entire population.

Increase private capital investments in healthcare.

Modernize the workforce.

Fund the system strategically.

Define and disclose affordability, quality and value systemically.

Facilitate technology-enabled self-care.

This will not happen quickly nor result from current momentum: the inertia of the status quo leans substantially toward protectionism not because it’s unaware. The risks are high. And while the majority of Americans are frustrated by its performance, there’s no referent to which look as a better mousetrap.

I anticipated last week would be pretty uneventful. It wasn’t. My Plan didn’t work out due, in part, to circumstances I didn’t foresee or control.

Healthcare’s the same. Outside forces seen or not will impact its future dramatically. Plans have to be made though Black Swans like the pandemic are inevitable. But long-term planning built on plausible bets are necessary to every healthcare organization’s future.

America’s health care system is neither healthy, caring, nor a system.

– Walter Cronkite

Healthcare policy in America is too short-sighted and vulnerable to party-politics. We need a system that’s built to last.

As open enrollment through the ACA marketplace begins November 1, millions of Americans will soon discover their health insurance rates going up in 2026 as the direct result of ACA tax subsidies expiring because party politicians in charge of the Senate refuse to budge. If you know how much your rates will be increasing in 2026, please share so I can see the impact that this inaction will have on regular folks.

Career politicians like my opponent Mike Rounds aren’t willing to stray from the party line to make sure Americans and their families get affordable healthcare, and in the process they are causing innumerable harm to not just those Americans on ACA, but also all the furloughed federal employees and families on SNAP. Something needs to change.

As an Independent candidate who supports pragmatic solutions, I will not claim my proposals are the best or only choices, but I will claim just about anything will be overall less expensive and more effective than the status quo. The bottom line is that our dysfunctional politics have us fighting over half-measure solutions to today’s problems instead of complete solutions to tomorrow’s.

Overhauling American healthcare is a complex challenge, but that cannot let it deter us. Americans deserve access to affordable, quality care. According to a KFF analysis, healthcare accounted for 27% of federal spending in fiscal year 2024. The U.S. spends far more per person on healthcare than any of the other 37 members of the Organization for Economic Co-operation and Development (OECD). Despite spending nearly twice as much per person as similar wealthy countries, we still rank poorly on key health outcomes.

America does, however, hold a commanding lead in medical debt, accounting for between 50% and 66% of annual personal bankruptcies. Other wealthy countries clearly understand better how to set up a healthcare system that is both less expensive and produces the same or better outcomes.

Considering the immense costs and mediocre outcomes, I am reminded of the famous observation from Dr. Amos Wilson: “If you want to understand any problem in America, you need to look at who profits from that problem, not at who suffers from that problem.” Having done so, I support an incremental reinvention of the American healthcare system that doesn’t just solve immediate problems such as premium hikes, expiring ACA subsidies, or Medicare cuts, but also secures a stable and healthy future for the American people.

My plan for America’s healthcare system has three basic steps, ensuring folks can get the care they need, now and in the future.

Stage 1: Fixing the Supply Side: Regulate Healthcare Companies, Lower Drug Prices, & Encourage Preventive Care

The healthcare industry (from insurers to providers) is a functional monopoly, especially at the local/regional level, similar to electric, gas, and telecommunications companies. It deserves to be treated the same way. Drawing from how the South Dakota Public Utilities Commission (and similar entities in other states) regulate utility companies to ensure that they provide “reliable service” and “reasonable rates,” creating a regulatory framework for healthcare companies (including insurers) is a good first step in adapting our current system into one that considers the needs of regular folks. Providers shouldn’t have to butt heads with insurers to provide the services that patients need, so creating a more transparent and regulated system would benefit every level of the process.

Pharmaceutical companies have the highest profit margins in the healthcare industry. According to a RAND report, Americans pay 278% higher prescription drug prices than similar countries where the government negotiates drug pricing. The common-sense solution is for the federal government to negotiate pricing for all drugs. Doing so will yield much greater savings for both the government and consumers.

To offset reduced pharmaceutical company profits and also help more consumers, the U.S. should negotiate a treaty with the European Union and other G7 countries to establish a pharmaceutical common market based on uniform drug development/approval standards enabling the elimination of trade barriers for drugs.

RFK Jr.’s “Make America Healthy Again” (MAHA) agenda includes multiple nonsensical proposals that are likely to do the opposite, but there are a handful of beneficial ideas. A MAHA focus on preventive care that strengthens primary care, expands access to screenings, and incentivizes healthy lifestyles will lower long-term healthcare spending the same way that keeping up routine maintenance on your car prevents big repair bills in the future.

Investing in community health centers, mobile clinics, and telehealth services will make preventive care more accessible, particularly in underserved rural and urban areas. Similarly, reducing reliance on highly processed foods and ensuring government nutrition assistance programs incentivize and enable healthy foods would also pay dividends.

Many states approve the rates that insurers charge consumers, but these rates increase as the base cost of providing healthcare services increases. Holding healthcare companies, providers and insurers alike, to uniform standards and making information transparently available for comparison will remove the various pressures driving up the cost of care, keeping rates down for consumers.

Stage 2: Fixing the Demand Side: Create a Public Option, Streamline Administration, Increase Residency Slots

Profits are up 230% for the top 5 health insurance companies since the Affordable Care Act (ACA) was adopted, while family premiums have also skyrocketed. While I think it was a step in the right direction to provide folks with healthcare, it isn’t a viable permanent solution. Creating a broadly available public option would enable Americans to buy into a health insurance plan administered by the government.

A public option like this wouldn’t have a profit motive, so it would be able to offer lower-cost plans, creating a baseline for other companies to compete with. Increased competition would drive down premiums and improve quality of service across the market, even amongst private for-profit insurers.

Technology can also help lower costs by reducing the complicated bureaucracy healthcare administrators must navigate. Healthcare providers currently spend enormous time and money dealing with insurance paperwork, eligibility verification, and billing disputes. Universally interoperable electronic health records (EHRs) and streamlined billing systems would significantly reduce costs. Uniform standards for these processes and better technology infrastructure would free up providers’ time to focus more on patient care.

By 2036, the U.S. is projected to need 86,000 more physicians than it will have. The primary cause of the growing shortage is a 1997 law freezing federal support for Medicare-funded residency positions. Limiting the number of doctors in training also fosters misallocation of training slots across the country, creating a mismatch between where they train and where they are needed most. Correcting this self-inflicted shortage is essential to maximizing access.

On the subject of innovative approaches to providing healthcare, fee-for-service payment models reward volume over value, encouraging unnecessary tests and procedures. Transitioning to value-based care, where providers are paid based on patient outcomes, can lead to better health outcomes at a lower cost. Accountable Care Organizations (ACOs), bundled payments, and capitation models (in which providers receive a fixed fee per patient for a specific time period regardless of services delivered) have shown promise in reducing spending while maintaining or improving quality.

Stage 3: Use The Foundation To Build a Better System

While I believe that our leaders today should be looking towards the future with long-lasting solutions rather than scrambling for band-aid policies, I also know that we shouldn’t put the cart before the horse. I believe that Stages 1 and 2 lay the foundation for a healthier America and a more streamlined healthcare system. Stage 3 of my plan is geared towards keeping our options open for the future of American healthcare.

All OECD countries with lower per-person healthcare spending provide universal or near-universal coverage to their citizens. Various universal healthcare systems seem to be an effective way to improve access and reduce systemic costs. In particular, I think that looking to our allies such as Canada (with a single-payer system) and Germany (with a multi-payer system) would be a good place to start. In both systems, the government negotiates prices directly with providers and pharmaceutical companies, leading to significant cost savings for consumers.

Conclusion

In summary, the American healthcare system doesn’t suffer from a lack of resources but rather anti-competitive profit-seeking, inefficiency, and a lack of imagination. Creative solutions lie in addressing the supply and demand side of the healthcare industry, continuously blending technological innovation, community-based delivery, and incentivizing healthier living.

No single policy will fix the U.S. healthcare system overnight, but a combination of reforms can dramatically improve access and lower costs. Providing a public option is a foundational step that keeps options open for other innovations. In tandem, reforms such as drug price negotiation, investment in preventive care, value-based payments, and administrative simplification can deliver a more efficient and equitable healthcare system. Political will and public support are crucial, but the long-term benefits for individuals, businesses, and the broader economy make these changes not only possible but necessary.

The path forward is not and cannot be a purely partisan choice of public versus private. It must be guided solely by a simple question: What is most effective at making healthcare cheaper, faster, and more accessible for everyone? At this point, I believe a robust public option is essential, but I remain unsure whether a single-payer or a refined version of a multi-payer universal system is warranted. I’m keeping an open mind.

I am sure that Washington politicians shouldn’t be screwing over regular Americans by making their healthcare inaccessible or more expensive. As South Dakota’s Independent senator, I would be empowered to break through party-first politics to make sure people always come first.

The American healthcare is complicated, so this article leans on the longer side to try and do it justice. Thank you for reading.

For four years, people buying health care on the Affordable Care Act (ACA) marketplace have benefited from government subsidies that made their plans more inexpensive, and thus more accessible.

Now, those subsidies have become a key point of contention between Democrats and Republicans in a government shutdown that went into effect on Oct. 1 after both sides failed to reach a deal.

Democrats want Congress to extend the enhanced premium tax credits first added in 2021; without an extension, the tax credits expire at the end of 2025 and experts say premium prices could double in 2026.

“They know they’re screwed if this debate turns into one about healthcare. And guess what? That’s just what we’re doing. We are making this debate a debate on healthcare,” said U.S. Senator Chuck Schumer, a Democrat from New York, hours before the government shut down.

Republicans say that Democrats want to extend free health care for unauthorized immigrants, a talking point that is not true but that has nevertheless been repeated many times by GOP politicians. (Democrats want to reverse health policy changes that the GOP’s tax law enacted, including limits to federal funding for health care for “lawfully present” immigrants.)

Neither side appears ready to budge, which means that as of right now, people who buy health care on the Affordable Care Act (ACA) marketplace are about to be in for some sticker shock. Monthly out-of-pocketcosts are set to jump as much as 75% for 2026 because of the disappearance of federal subsidies and higher rates from insurers.

“Most enrollees are going to be facing a double whammy of both higher insurance bills and losing the subsidies that lower much of the cost,” says Matt McGough, a policy analyst at KFF for the Program on the ACA and the Peterson-KFF Health System Tracker.

KFF recently calculated that the median rate increase proposed by insurers is 18%, more than double last year’s 7% median proposed increase. But the actual blow to patients is going to be much higher. That’s because enhancements to premium tax credits are set to expire at the end of 2025.

Around 93% of marketplace enrollees—19.3 million people—received the enhanced premium tax credits, according to the Center on Budget and Policy Priorities, saving them $700 yearly on average. For some people, the tax credits meant that they wouldn’t have to pay an insurance premium if they chose certain plans. For others, it meant getting hundreds of dollars off a health plan they otherwise wouldn’t have been able to afford.

Premium tax credits helped people afford plans on the Affordable Care Act marketplaces between 2014 and 2021. Then, in 2021, enhancements to those premium tax credits went into effect with the American Rescue Plan. Before 2021, premium tax credits were only available to people making between 100-400% of the federal poverty limit—so between $25,8200 and $103,280 for a family of three in 2025. The enhanced tax credits were expanded to households with incomes over 400% of the federal poverty limit, and were also made more generous for everyone. That wide range meant they subsidized coverage for people who otherwise would not have gotten any break on their premiums.

The enhancements to the premium tax credits, which are set to expire at the end of 2025, significantly boosted enrollment in Affordable Care Act marketplace plans. More than 20 million people enrolled in marketplace coverage in 2024, according to the Center on Budget and Policy Priorities, up from 11.2 million in February 2021, before the enhancements to the tax credits.

With costs being lowered by half, individuals and families decided, ‘OK, maybe this is financially worthwhile,’” says McGough. “Whereas previously, they thought that they didn’t utilize that much health care, so it wasn’t worth it to purchase health care on the marketplaces.”

Why insurers want to increase rates

Every year, health insurers submit filings to state regulators that detail how much they need to change rates for their ACA-regulated health plans. KFF analyzed 312 insurers across 50 states and the District of Columbia; they found that insurers are requesting the largest rate changes since 2018.

They are requesting the median 18% increase for a few reasons, including rising health care costs, tariffs, and the expiration of the premium tax credit enhancements, KFF found. Health care costs have been rising for years, but insurers say that the cost of medical care is up about 8% from last year. They say that tariffs may put upward pressure on the costs of pharmaceuticals and that growing demand for GLP-1 drugs such as Ozempic and Wegovy is driving up their expenses.

Worker shortages are also driving health care costs up, according to the KFF analysis. It also found that consolidation among health care providers was leading to higher prices because those providers had more market power.

Everyone’s bottom line could be affected

When they went into effect, the enhanced premium tax credits pushed some people into the marketplace who might otherwise have been uncertain about whether to get health insurance. The tax credits were graduated so that people with the lowest incomes got the most help, but they also reached people with slightly higher incomes.

Many people don’t know that those enhancements to the premium tax credits are going away, says Jennifer Sullivan, director of health coverage access for the Center on Budget and Policy Priorities (CBPP). Her organization has been talking to people across the country about how they may be affected if Congress does not extend the enhancements, and has found that even increases of $100 or $200 a month may be enough to force some people out of the marketplace.

“It’s a huge increase in anyone’s budget, particularly at a time when groceries are up and the cost of housing is up and so is everything else,” Sullivan says.

There are other reasons the ACA marketplace may see fewer enrollees, she says. A handful of policies passed by Congress require more verification to enroll in ACA plans and cut immigrant eligibility, for example.

Fewer enrollees are bad news for everyone else. The people who are likely to drop coverage are those who don’t need it for lifesaving treatment or medicine. That means the pool of people who are still covered by ACA plans will be sicker and more expensive to care for.

“The people who are left are statistically more likely to be people with higher health care needs,” says Sullivan, with CBPP. “Those are the folks that are going to jump through extra hoops, whether it’s more paperwork or higher premiums or higher out-of-pocket costs, because they absolutely know they need the coverage.”

There are other society-wide effects to people dropping their health insurance coverage. Many uninsured people end up in emergency rooms for care because that’s their only option, and sometimes, they can’t pay. That increases the cost of health care for everyone else, says Sullivan.

Amy Bielawski, 60, is one of the people who is going to look at her options when rates for marketplace plans are listed in October and decide whether or not to enroll. Bielawski, an entrepreneur and entertainer who performs belly dancing at parties, has spent much of her life without health care.

She finally signed up for an ACA plan in 2019, and was able to go to a doctor and diagnose her hypothyroidism and uterine fibroids. Last year, because of the enhanced premium tax credits, she paid $0 a month in premiums—which will almost certainly go up.

“I’m afraid, I’m very afraid,” says Bielawski, who lives in Georgia. “I can’t wrap my head around it because there are so many things that can go wrong with my health.”

Where politicians stand now

Addressing this uncertainty is one key reason the Affordable Care Act passed in the first place in 2010. It has dramatically improved health coverage for Americans; nearly 50 million people, or one in seven U.S. residents, have been covered by health insurance plans through ACA marketplaces since they first launched in late 2013.

But it has also faced numerous challenges, and Republicans have long said that weakening or revamping the law is a high priority.

It’s unclear if the hassle of a government shutdown will make them change their tune. In September, Senate Majority Leader John Thune, a Republican from South Dakota, said he was open to addressing the expiration of the subsidies, but that he did not want to tie any of those policy changes to government funding measures. Sen. Mike Rounds, also a Republican of South Dakota, has suggested a one-year extension to the subsidies, after which the tax credits return to pre-pandemic levels.

Many Republicans appear determined to end the subsidies eventually, and their insistence on scaling back spending on health care policy seems to be having an impact.

Sullivan, with the CBPP, says that the changes to the Affordable Care Act and looming cuts to Medicaid have the potential to dramatically reduce the number of people able to afford regular medical care in the country. These cuts come at a time when key indicators like infant mortality rates and life expectancy rates are worsening.

“We are seeing a real weakening of that safety net that we spent the last 10-15 years fortifying,” she says.

After a long career as a nurse, Lisa Bower, now 61, retired, started working as a part-time nanny, and, in 2021, realized she needed health insurance. The Illinois resident took to the Internet to sign up for a plan on the Affordable Care Act (ACA) marketplace.

But something went wrong and she somehow ended up on another website that looked a lot like a health insurance marketplace. She entered her phone number and soon started getting calls and texts from people who wanted to help her get health insurance.

Within a few minutes, she was registered for a plan that she thought was ACA-compliant. But Bower had instead signed up for what’s called a fixed indemnity plan, which is not actually health insurance and which just pays a small amount for covered services. She didn’t realize that she didn’t have proper health insurance until the fall of 2025, when her son was looking for a tax form that proved she had marketplace insurance and, unable to find it, started digging into her health care paperwork.

Over three years, he found, she’d paid about $16,000 to the fixed indemnity company while receiving very little benefit. During this time, she’d paid out of pocket for costs like doctor’s appointments and medications. Had she gotten an ACA-compliant plan, she probably wouldn’t have had to pay much in premiums at all, her son says, because her low income would have qualified her for subsidies.

“I did think at the time that it was less painful to sign up than I thought it would be,” says Bower. “I just chose what I thought was a cheap plan and didn’t think much about it.”

Bower’s son, Jack, says that Illinois’s real health care marketplace found evidence of Lisa starting to sign up in 2021, but says that she did not complete the application. Instead, he guesses, she got lured away by Google ads and ended up somewhere else.

“I think she holds a third of the blame, and another third of the blame goes to this company that knowingly does this marketing to get people to pay for things they don’t actually want,” Jack says. “But the other third of the blame goes to our health care system, which is so complicated that companies just thrive in the confusion and an astute person can’t make heads or tails of it.”

The Bowers’ experience is not particularly unusual. Confusion about navigating insurance writ large and the Affordable Care Act marketplace in particular has led many people to end up with plans that they think are health insurance which in fact are not health insurance. They mistakenly click away from healthcare.gov, the website where people are supposed to sign up for ACA-compliant plans, and end up on a site with a misleading name that may provide them with an ACA-compliant plan but also might not.

Experts are predicting that this will happen to a larger degree when ACA open enrollment begins in most states on November 1. Because Congress did not extend enhanced premium tax credits, prices for ACA plans are going up an average of 75%. This may spur more people to search for less expensive plans and end up with something that is not health insurance, whether they know it or not.

“There’s no question that more people will end up with these kinds of plans if the premium tax credits are not extended,” says Claire Heyison, senior policy analyst for health insurance and marketplace policy at the Center on Budget and Policy Priorities, a research and policy institute.

Under the Affordable Care Act, health insurance must cover 10 essential benefits, including outpatient services, emergency services, maternity and newborn care, behavioral health treatment, prescription drugs, and pediatric services. But if people stray from the ACA marketplace, they can end up with plans that don’t cover some—or any—of these essential health benefits. People may end up with short-term plans that don’t last for a full year, or with the type of fixed indemnity plan that Bower got. Others may end up in health care sharing ministries, in which people pitch in for other peoples’ medical costs, but which sometimes do not cover preexisting conditions.

These non-insurance products “have increasingly been marketed in ways that make them look similar to health insurance,” Heyison says. To stir further confusion, some even deploy common insurance terms like PPO (preferred provider organization) or co-pay in their terms and conditions. But people will pay a price for using them, Heyison says, because they can charge higher premiums than ACA-compliant plans, deny coverage based on pre-existing conditions, impose annual or lifetime limits on coverage, and exclude benefits like prescription drug coverage or maternity care.

Often, the websites where people end up buying non-ACA compliant insurance have the names and logos of insurers on them. Sometimes, they are lead-generation sites—like the one Lisa Bower mistakenly visited—that ask for a person’s name and phone number and then share that information with brokers who get a commission for signing up people for plans, whether they are health insurance or not.

“This can definitely happen if someone starts Googling and clicks on the first thing they see,” says Louise Norris, health policy analyst at healthinsurance.org, an independent site providing information about insurance plans. “People might not realize that what they’re seeing isn’t real health insurance.”

These mistakes are enabled by a legal gray area in which websites can imply that they can help people sign up for health insurance and then actually sign them up for something else. Brokers, who often work for particular health insurance companies, can often sign people up for both ACA-compliant plans and non-ACA compliant plans. But they typically get more money signing up someone for a non-ACA compliant plan than an ACA-compliant plan, says Heyison.

Non-ACA compliant plans can spend more on administration costs like brokers and marketing because they aren’t regulated in the same way as ACA-compliant plans and have more cash to spare.

Health insurance is complicated, and brokers exist to help walk people through the process of signing up for health insurance. But they sometimes don’t have consumers’ best interest at heart, says Emma Freer, senior policy analyst for the American Economic Liberties Project. “It’s just very predatory because people clearly want information and guidance,” she says, “but many middlemen are incentivized to operate with their own financial interest in mind, not the consumer’s.”

There has been some legal action against companies who have represented what they’re selling as health insurance, even though it’s not. In May 2025, the U.S. Attorney’s Office for the Eastern District of Pennsylvania charged four businessmen and two companies with conspiracy and wire fraud offenses, alleging they had executed a national telemarketing fraud scheme in which they collected tens of millions of dollars by “systematically deceiving and misleading consumers seeking health insurance through bait-and-switch sales tactics.” And in August 2025, two companies agreed to pay a total of $145 million to settle Federal Trade Commission charges that they deceived consumers into purchasing health care plans that did not provide the comprehensive coverage that was promised.

But because many of these companies are actually offering products that are legal—they just aren’t comprehensive health insurance—it can usually be difficult for people to recover any money, or to even get out of the plans. People who discover they signed up for the wrong plan during their state’s open enrollment period should still be able to cancel the plan and sign up for real health insurance, says Heyison, of CBPP. But those who don’t find out for months—or years—that they signed up for non-ACA compliant plans may have a harder time.

“It is definitely a situation where people need to pay close attention now, because in most cases you don’t get a do-over,” says Norris, of healthinsurance.org.

Brandon A., a 27-year-old Maryland resident, didn’t have a lot of experience signing up for health insurance because he’d been in the military and gotten health insurance there. When he went to research plans on the ACA marketplace in mid-October, he searched online for Maryland Health Connection, the state’s marketplace, but ended up on marylandhealthcoverage.org instead.

After entering his zip code and some personal information like his social security number, he got a quote for a plan. He also started getting bombarded with texts and phone calls from people who wanted to sign him up for health insurance. He chose a plan that was just a $300 deposit and $100 a month afterwards. After a few days, and checking with some friends, something seemed off to him, so he called the company back to cancel. They argued with him, telling him it was “the best healthcare nationwide,” he says, but eventually allowed him to cancel the plan.

In retrospect, Brandon, who didn’t want his last name used because he’s embarrassed about his error, saw that in the website’s fine print at the very bottom, in very small text, it says it is not a federal or state health insurance marketplace. “It seems too easy for these sites to pose as real marketplaces,” he says.

Marylandhealthcoverage.org is operated by NextGen Leads, a lead-generation site that collects the information of people looking for health insurance and then charges companies for that information. It has more than 100 complaints on the Better Business Bureau of San Diego, where the company’s website says it is based. Many of the people filing these complaints say that they thought they were signing up for marketplace health insurance in states like Maryland and Georgia, entered their personal information on a site owned by NextGen Leads—often with a domain name ending in .org— and then got spammed with hundreds of calls and texts from people trying to sell them health insurance products. “Their fraudulent website to mimic a health marketplace for [redacted] resulted in selling my information where now I received so many calls from spammers that I literally can not use my phone due to the insane amount of calls,” one person wrote, in January 2025. The company did not reply to TIME’s request for comment.

Experts recommend that people who are stuck in plans that they didn’t mean to buy contact their state insurance commissioner to report the problem. They should also contact a health care navigator or assister—federally funded individuals who exist solely to provide unbiased information—to see if they might qualify to sign up for a comprehensive health insurance plan through a special enrollment period because of a qualifying life event.

Navigators and assisters are also helpful for those seeking new insurance, rather than engaging with brokers. Healthcare.gov is the best place for people to sign up for health insurance who want to do it on their own. Though about 20 states run their own marketplaces that use a different URL, healthcare.gov will direct them to the state marketplaces. It can also direct them to local assisters and navigators.

Signing up for a plan on the true ACA marketplace should not lead consumers to get bombarded with texts or calls—if this happens to you, it probably means you ended up on a lead-generation site instead of on the real marketplace.

Heyison, of CBPP, recommends that consumers never rely on verbal promises that someone selling health insurance gives over the phone, they should instead ask for the plan documents. They should avoid companies offering an upfront gift for signing up, and ones that say that a certain price will only last a few days. Consumers should also spend a few days researching a plan, rather than buying the first thing they see, Heyison says. They should be looking for a plan on healthcare.gov and one that is ACA-compliant.

Some states are attempting to further regulate brokers and non-ACA compliant plans, Heyison says. In California, for instance, agents and brokers are required to assess people for Medicaid and the ACA’s premium tax credit because they enroll them in health care sharing ministries, which could save them money by signing them up for government health insurance instead of a product that is not health insurance. And some states, including California, Illinois, and Massachusetts, prohibit the underwriting of short-term health insurance coverage, making it nearly impossible to sell non-ACA compliant plans in those states.

But most other states haven’t taken action, leaving people like Lisa Bower out of luck. Her son Jack tried to call the company that issued her indemnity plan and get a refund, but he knows he likely has no legal recourse. She should have read the paperwork more closely, they both admit. This year, they’re ready for open enrollment—and are determined not to look anywhere but healthcare.gov, the official Affordable Care Act marketplace.

We learned yesterday that the average cost of a family health insurance policy through an employer reached nearly $27,000 this year, 6% higher than what it cost in 2024. As if that weren’t alarming enough, researchers are predicting that the total likely will soar toward $30,000 next year because of rising medical costs and the unrelenting pressure insurers are under from Wall Street to increase their profits. Small businesses will be hit the hardest.

Despite repeated assurances from insurers that we can count on them to hold down the cost of health care – and consequently the premiums they charge – there are now many years of evidence – from researchers like KFF, which tracks annual changes in employer-sponsored coverage – that they have not and cannot deliver on their promises.

Nevertheless, Big Insurance is doing just fine financially as they force America’s employers and workers to shell out increasingly absurd amounts of money for policies that actually cover less than they did ten years ago. A health insurance policy today is generally less valuable than it was a decade ago because families have to spend more and more money out of their own pockets every year before their coverage kicks in. In addition, they are far more likely to be notified that their insurers will not cover the care their doctors say they need.

When you look at KFF’s reports over time, you’ll see that the cost of a family policy has increased 60% since 2014 when it cost an average of $16,834. That is a rate of increase much higher than general inflation and also higher than medical inflation.

Not only has the total cost of an employer-sponsored plan skyrocketed, so has the share of premiums workers must pay. This year, employers deducted an average of $6,850 from their workers’ paychecks for family coverage, up from $4,823 in 2014, a 42% increase.

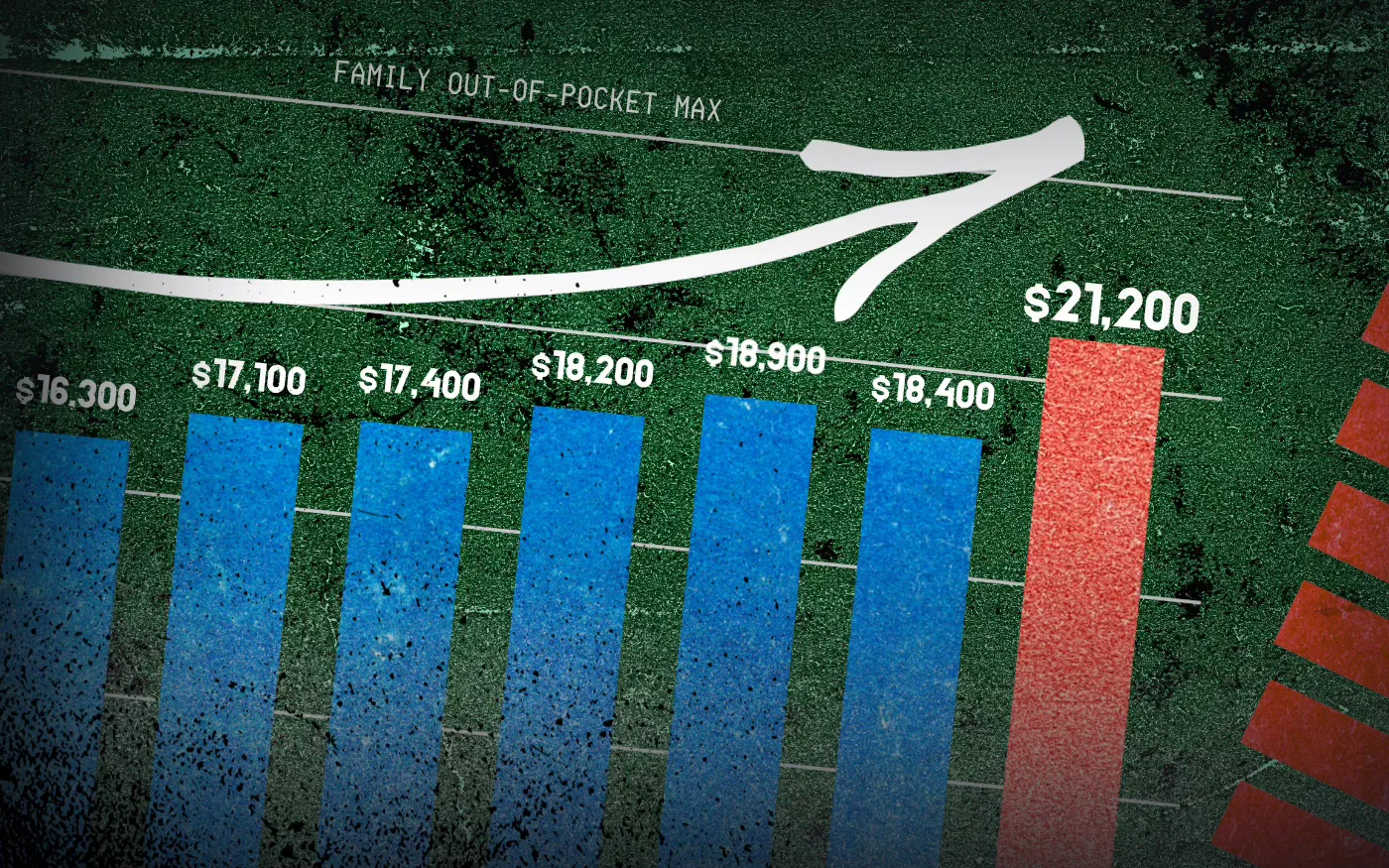

And as premiums have risen, so has the amount of money workers and their dependents are required to spend out of their pockets in deductibles, copayments and coinsurance. The Affordable Care Act, to its credit, instituted a cap on out-of-pocket expenses in 2014, but that cap has been increasing annually along with premiums. (The U.S. Department of Health & Human Services sets the out-of-pocket max every year, pegging it to the average increase in premiums.)

In 2014 the out-of-pocket cap for a family policy was $12,700. Next year, it will rise to $21,200 – a 67% increase. And keep in mind that the cap only applies to in-network care. If you go out of your insurer’s network or take a medication not covered under your policy, you can be on the hook for hundreds or thousands more. While most employer-sponsored plans have caps that are considerably lower, many individuals and families reach the legal max every year.

Meanwhile, the seven biggest for-profit health insurers have made hundreds of billions in profits since 2014 as they have jacked up premiums and out-of-pocket requirements and erected numerous barriers, including the aggressive use of prior authorization, that make it more difficult for Americans to get the care and medications they need. Collectively, those seven companies made $71.3 billion in profits last year alone. That was up slightly from $70.7 billion in 2023. Insurers said their 2024 profits were somewhat depressed because more of their health plan enrollees went to the doctor and picked up their prescriptions last year. Investors were furious that insurers couldn’t keep that from happening, as you’ll see in the charts below. Many of them sold some or all of their shares, sending insurers’ stock prices down. But overall, the stock prices of the big insurance conglomerates have increased steadily over the years as we and our employers have had to spend more for policies that cover less.

For example, UnitedHealth Group, the biggest of the seven, saw its stock price increase 483% between 2014 and 2024 – from $85.31 a share on Dec. 31, 2014, to $497.02 on Dec. 31, 2024. Most of the other companies saw similar growth in their shares over that time period.

By contrast, the Dow Jones Industrial Average increased 139% (from $17,823.07 to $42,544.22), and the S&P 500 increased 186% (from $2,058.90 to $5,881.63) during the same period.

Back to those premiums and out-of-pocket requirements. While the KFF numbers pertain to employer-sponsored coverage, people who have to buy health insurance on their own – mostly through the ACA (Obamacare) marketplace – have experienced similar increases. Most Americans who buy their insurance there could not possibly afford it if not for subsidies provided by the federal government on a sliding scale, which is based on income. The most generous subsidies have been available since 2014 to people with income up to 150% of the federal poverty level (FPL). During the pandemic, Congress expanded – or “enhanced” – the subsidies to make them available to people with incomes up to 400% of FPL. Those enhanced subsidies are scheduled to expire at the end of this year. Whether to let them expire or extend them is at the center of the ongoing government shutdown. Most Democrats are insisting they be extended while most Republicans want them to end. It’s important to note that the federal money goes to insurance companies, not to people enrolled in their health plans.

If the enhanced subsidies do end, millions of Americans who get their health insurance through the ACA marketplace will drop their coverage because the premiums will be unaffordable for them and their families. In Pennsylvania where I live, premiums for policies bought on the state’s insurance exchange are expected to increase 102% next year because of the anticipated end of the subsidies and premium inflation.

More than 24 million Americans now get their coverage through the ACA marketplace, primarily because their employers cannot offer health insurance as an employee benefit anymore. Over the past several years, a growing number of small businesses have stopped offering subsidized coverage to their workers because of the expense. Just slightly more than half of U.S. businesses are still in the game. The rest simply can’t afford the premiums. Small businesses can expect an average increase of 11% next year with some of them facing increases of 32%.

It is becoming more clear every passing year that the U.S. has one of the most insidious ways of rationing care. It is rationed based on a person’s ability to pay far more than on a person’s need for care. And among those most disadvantaged by the current system are hard-working low- and middle-income Americans with chronic conditions and those who suddenly get sick or injured.

While the Affordable Care Act prohibited insurers from charging people with pre-existing conditions more than healthier people, insurers have figured out a back door way to discriminate against them: by making them pay hundreds or thousands of dollars out of their own pockets every year – in addition to their premiums – and also by refusing to cover treatments and medications their doctors say they need.

Now you know why Big Insurance is doing so well while the rest of us are getting

Physicians for a National Health Program (PNHP) — in collaboration with Johns Hopkins University researchers — just released a report titled “No Real Choices: How Medicare Advantage Fails Seniors of Color”. It confirms that the handover of public programs like Medicare Advantage (MA) to Big Insurance doesn’t close racial, ethnic and economic health gaps — it deepens them.

Read Physician for a National Health Program’s report, No Real Choices: How Medicare Advantage Fails Seniors of Color, here.

PNHP’s researchers found that communities of color are being steered into MA plans not because they’re better — but because they’re cheaper upfront. This dynamic, dubbed the “Gap Trap,” means that affordability is driving people into coverage that often denies care, delays treatment and locks them into narrow networks.

“Medicare Advantage squanders billions, harms seniors and exacerbates racial inequities,” Dr. Diljeet K. Singh, gynecologic oncologist and president of Physicians for a National Health Program, said. “Americans need universal health Care which removes profit-motivated conflicts of interest, abolishes co-pays and deductibles, ends prior authorization burdens and guarantees protection from medical bankruptcy.”

HEALTH CARE un-covered is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.

Medicare Advantage is the health care equivalent of the subprime mortgage crisis — except the fine print here is costing Americans’ lives and depleting the Medicare Trust Fund.

The equity illusion

When Big Insurance boasts about “diverse” enrollment in MA, this report reminds us: “Diversity” is often just a buzzword used for PR reasons and has nothing to do with seniors receiving the care they deserve — especially when it is used as cover for a business model that profits from inequity.

Black, Hispanic and Asian/Asian-American beneficiaries are disproportionately concentrated in MA plans that score lowest on quality ratings, while white beneficiaries are more likely to live in counties served by higher-quality plans.

One study found that MA prior authorization requests were denied 23% of the time for Black seniors vs. 15% for their white counterparts.

Despite industry claims to the contrary, racial and ethnic health disparities in the United States are not being reduced by Medicare Advantage.

Studies show that Black enrollees are more likely than white enrollees to choose a 5-star MA plan when offered one. They’re just not offered them as often.

Racial minority enrollees in MA suffer from worse clinical outcomes and face barriers accessing best quality care because of restrictive networks and misaligned financial incentives. Black MA enrollees experience higher rates of hospital readmission compared to their white peers.

The MA paperwork burden isdriving doctors out of practice, worsening access for everyone — but especially in already underserved communities.

MA’s restrictive payment practices aren’t just harming patients — they’re pushing hospitals, especially those serving rural and minority communities, toward the edge of closure. Under-payment or delay of claims by MA insurers causes cascading financial harm in these vulnerable systems.

The big picture

As a reminder, even with the racial and ethnic issues aside, Medicare Advantage already severely restricts seniors’ access to providers, imposes unnecessary prior authorization hurdles that often result in deadly delays and denials — and cost taxpayers at least$84 billionmoreeach year than original Medicare. Meanwhile, original, traditional Medicare does not even have networks; almost all doctors participate and few treatments are subject to prior authorization.

PNHP’s report shows that despite insurers’ endless “health equity” pledges and glossy diversity campaigns, MA remains a rigged game that leaves millions of seniors — disproportionately people of color — with worse access, inferior care and fewer real choices.

Big Insurance’s MA plans are shaped by the same market incentives that have long rewarded exclusion and sorting risk, and – if history tells us anything – sorting has always leaned on racial dimensions. As the report sums it up:

“Regardless of the reasons, any system that traps and harms people — particularly in ways that map onto centuries of racial injustice — cannot be a solution to health inequity.”