In a concession to Wall Street investors, starting this summer, UnitedHealth will stop paying commissions to agents and brokers for some new enrollees in nearly 200 UnitedHealthcare Medicare Advantage plans across 39 markets.

And it’s happening not because UnitedHealth can’t afford to pay. As we’ve published previously, the company reported $9.1 billion in profits during the first quarter of 2025 — up from $7.9 billion the year before. But that wasn’t enough to satisfy Wall Street, which punished UnitedHealth with the steepest one-day stock drop in 26 years — a $110 billion free fall in market value — after the company revised its full-year profit guidance downward.

Why the drop?

Because UnitedHealth admitted it may not squeeze quite as much profit from taxpayers this year as expected — mainly due to unexpectedly high care utilization from some of the new Medicare Advantage enrollees it brought on during the last open enrollment period. Particularly enrollees who, as then-CEO Andrew Witty described, came from other insurers exiting the market and hadn’t been properly coded. Yawn.

For Now, Brokers Are UNH’s Patsy

This recent commission cut is less about operational efficiency and more about damage control. UnitedHealth is signaling to investors that it’s willing to shrink its Medicare Advantage footprint — at least temporarily — if that helps preserve profit margins. And Wall Street analysts are eating it up, seeing it as a way to slow the flow of high-cost members and stabilize earnings, according to BarChart.

Off Wall Street, the move has already come under fire. As the National Association of Benefits and Insurance Professionals put it, UnitedHealth is “cutting off the very people best equipped to help” seniors — especially low-income and rural enrollees who depend on brokers to explain their options.

While we would warn seniors against enrolling in a Medicare Advantage plan in the first place – without brokers, many beneficiaries will be left to fend for themselves in a system that’s already infamously confusing, expensive and deadly.

A Strategic Retreat Disguised as a Cost-Containment Strategy

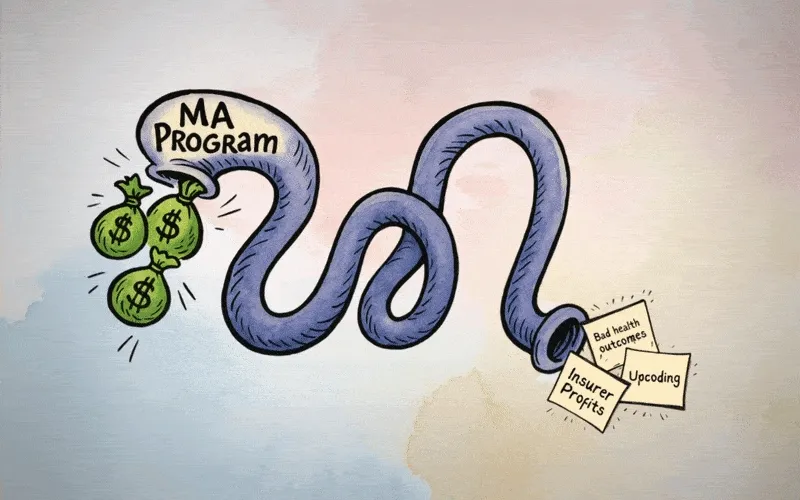

The problem is the perverse incentive structure UnitedHealth and other insurers helped build — one that rewards risk-coding gamesmanship more than it rewards delivering care. For years, the company thrived by maximizing revenue through “coding intensity” and by acquiring everything from doctors’ offices to behavioral health firms to control more of the health care ecosystem.

Now, UnitedHealth is responding the way Wall Street expects: by slashing anything that isn’t bolted down – including brokers.

So here we are:

UnitedHealth is still wildly profitable, still drawing billions from taxpayer-funded programs like Medicare and Medicaid — and now it’s cutting out the professionals who presumably help seniors navigate a convoluted health care system. All this, mind you, to appease jittery investors. And despite UnitedHealth’s current wobbly share price, analysts expect it to rebound, especially with a continuation of share buybacks on the horizon.

During the first quarter of this year alone, the company bought back $3 billion worth of its own shares. Over the past year, buybacks totaled more than $12 billion. When you factor in dividends, the company said it “returned” more than $16 billion to shareholders in 2024. That’s how you keep investors at least partially satisfied.