Inflation moderated as economists forecasted last month, according to the Federal Reserve’s favored inflation metric, bringing welcome news for investors, home buyers and consumers alike looking for interest rate cuts.

KEY FACTS

Americans spent 2.4% more in January than they did in January 2023, according to the personal consumption expenditures (PCE) price index released Thursday morning by the Bureau of Economic Analysis.

That meets consensus economist estimates of 2.4% annual PCE inflation and comes in lower than last month’s 2.6%.

It’s the lowest PCE reading since March 2021.

Core PCE inflation, which tracks expenditures for goods and services other than the less sticky food and services inputs, was 2.8% in January, in line with forecasts of 2.8%.

It’s similarly the lowest core PCE reading since March 2021 and checks in significantly lower than January 2023’s 4.7% inflation.

KEY BACKGROUND

Core PCE inflation, which is Fed Chairman Jerome Powell’s inflation measure of choice, is still well above the Fed’s long-term 2% target.

Earlier this month, PCE’s sister consumer price index (CPI)revealed far worse CPI inflation than economists projected, sending the S&P 500 stock index to its biggest loss in almost 12 months as sticky inflation would likely cause the Fed to delay the much-anticipated rate cuts until more tangible progress toward 2% inflation is apparent. CPI measures the average prices nationwide of a predetermined basket of goods and services, while PCE measures how much Americans actually spend monthly, earning the latter policymakers’ affection as it arguably paints a better picture of the health of Americans’ wallets.

The series of hotter than anticipated inflation data has dramatically pushed back expectations of when and by how much the Fed will slash rates in 2024. Higher inflation typically keeps rates higher for longer, making loans such as mortgages more expensive, exemplified by mortgage rates more than doubling over the last two years to their highest levels since the turn of the century.

The futures market currently prices in June as the most likely date of the first cut and 75 basis points of cuts as the most likely outcome, according to the CME Group’s FedWatch Tool, much softer than a month ago’s implied forecasts of the first reduction coming in May and 125 basis points of cuts.

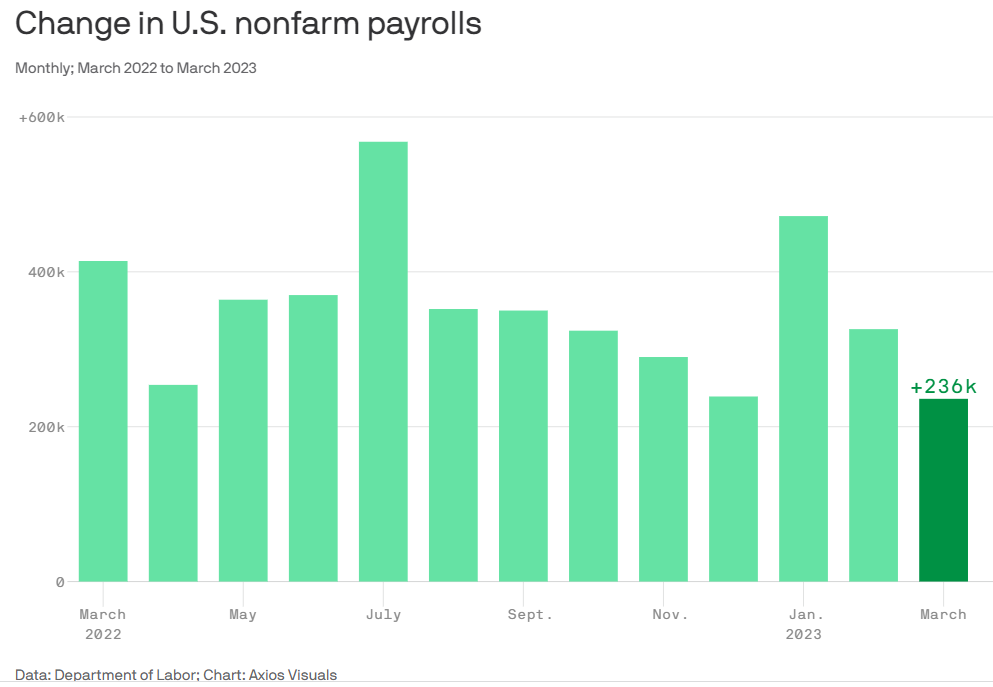

The U.S. economy added 353,000 jobs in January, while the unemployment rate held at 3.7%, the Labor Department said Friday.

Why it matters:

The first look at the 2024 labor market shows it’s on fire — not slowing down as previously thought.

Details:

The January payroll figures show hiring picked up from the 333,000 added the prior month, which itself was revised higher by 117,000.

Job gains in November were revised slightly higher, too, by 9,000 to 182,000 jobs added.

What’s new:

The hiring boom last month came amid strong job gains in health care, retail and professional and business services, while mining and oil and gas extraction are among the sectors that shed jobs.

Meanwhile, the labor force participation rate — the share of workers with or looking for a job — was 62.5% in January.

Average hourly earnings, a measure of wage growth, soared by 0.6%. Over the past 12 month, average hourly earnings increased by 4.5%.

The big picture:

The data is the latest in recent weeks to show that the economy is revving up, with fading inflation and steady hiring — a welcome development for the Biden administration that is touting its economic agenda ahead of the 2024 election.

The intrigue:

The strong growth in both jobs and earnings will make the Federal Reserve reluctant to cut interest rates soon, out of fear that labor market strength could reverse progress on inflation.

Already this week, Fed chair Jerome Powell threw cold water on the idea of a March rate cut.

The bottom line:

Despite high profile layoffs at media and technology companies, the report shows that broader labor market is heating up.

Forget the much-discussed prospect of a soft landing for the U.S. economy. In 2023, there was no landing at all.

Why it matters:

Big economic rules broke last year. The latest data to confirm that is the new GDP report showing very strong economic growth to conclude 2023, even amid a big cooldown in inflation.

Mainstream economists and policymakers believed a period of below-trend growth would be necessary to make progress on inflation.

Instead, above-trend growth in 2023 coincided with inflation falling sharply, reflecting improvement in the economy’s supply potential.

Driving the news:

The economy expanded at a 3.3% annualized rate in the fourth quarter, well above the 2% forecasters expected. That followed the previous quarter’s blockbuster 4.9% growth.

GDP was 3.1% higher in the fourth quarter than a year earlier.

That represents an acceleration from 0.7% GDP growth in 2022, and trounced the growth rates of most other advanced countries — and the 1.8%-ish rate that economists consider the United States’ long-term trend.

Details:

The fourth quarter’s hot growth resulted from bustling activity across the economy.

Consumers spent more on goods and services, with personal consumption expenditures rising at a 2.8% annualized pace. That was responsible for nearly 2 percentage points of the fourth quarter’s GDP rise.

Businesses spent on equipment, factories and intellectual property at a solid pace, with nonresidential fixed investment increasing at 1.9% — up from the previous quarter.

The intrigue:

For two years now, Fed officials have spoken of the need for a period of below-trend growth to bring inflation into line. Now, they face the decision of whether to cut rates — to essentially declare victory on inflation — even as below-trend growth is nowhere to be seen.

A flourishing labor market, strong productivity gains and supply-side improvements — more workers joining the workforce, for instance — has (at least so far) meant the economy can keep growing at a solid pace without risking a pickup in price pressure.

“[W]e had significant supply-side gains with strong demand,” Fed chair Jerome Powell said in his December press conference, adding that potential growth may have been higher than usual “just because of the healing on the supply side.”

“So that was a surprise to just about everybody,” Powell said.

What they’re saying:

“This report feels like a supersonic Goldilocks: very strong GDP reading with cool inflation,” Beth Ann Bovino, chief economist at U.S. Bank, tells Axios. “Good news is good news.”

“With high productivity levels, we can have strong growth with less inflation. That was the case during the last soft landing in the 90s,” Bovino adds.

The U.S. economy added 216,000 jobs last month while the unemployment rate held at 3.7%, the Labor Department said on Friday.

Why it matters:

The final snapshot of the 2023 labor market shows hot hiring — the latest sign that the American job market continues to defy expectations of a slowdown.

The figure is well-above the roughly 170,000 jobs economists expected.

The big picture:

The Federal Reserve has hinted it likely won’t raise interest rates again with encouraging signs that inflation is easing and the labor market is cooling.

That concludes an aggressive rate hiking cycle that began in 2022 and lasted through much of last year.

For now, however, there is little evidence those rate hikes translated into pain for workers in 2022.

American consumers, however, remain dissatisfied with the economy — a problem that may continue to weigh on the Biden White House as the 2024 election heats up.

Details:

Friday’s jobs report shows the labor market stayed strong. Hiring increased in sectors including government, health care, and construction. Transportation and warehousing shed jobs.

Average hourly earnings, a measure of wages, rose by 0.4% last month. Compared to the prior year, average hourly earnings rose 4.1%.

The share of the population with in the labor force — that is, with a job or looking for one — was 62.5% in December, roughly 0.3 percentage point less than the prior month.

The Labor Department also said the economy added a combined 71,000 fewer jobs than initially estimated in October and November.

The bottom line:

The hotter-than-expected jobs figures are one of several more key economic reports due before Federal Reserve officials meet at the end of the month.

Two important reports released last Wednesday point to a disconnect in how policymakers are managing the U.S. economy and how the health economy fits.

Report One: The Federal Reserve Open Market Meeting

At its meeting last week, the Governors of the Federal Open Market Committee (FOMC) voted unanimously to keep the target range for the federal funds rate at 5% to 5.25%–the first time since last March that the Fed has concluded a policy meeting without raising interest rates.

In its statement by Chairman Powell, the central bank left open the possibility of additional rate hikes this year which means interest rates could hit 5.6% before trending slightly lower in 2024.

In conjunction with the (FOMC) meeting, meeting participants submitted projections of the most likely outcomes for each year from 2023 to 2025 and over the longer run:

Median

2023

2024

2025

Longer Run

Longer Run Range

% Change in GDP

1.1

1.1

1.8

1.8

1.6-2.5

Unemployment rate &

4.1

4.5

4.5

4.0

3.6-4.4

PCE Inflation rate

3.2

2.5

2.1

2.0

2.0

Core PCE Inflation

3.9

2.6

2.2

*

*

*Longer-run projections for core PCE inflation are not collected.

Notes re: the Fed’s projections based on these indicators:

The GDP (a measure of economic growth) is expected to increase 1% more this year than anticipated in its March 2023 analysis while estimates for 2024 were lowered just slightly by 0.1%. Economic growth will continue but at a slower pace.

The unemployment rate is expected to increase to 4.1% by the end of 2023, a smaller rise in joblessness than the previous estimate of 4.5%. (As of May, the unemployment rate was 3.7%). Unemployment is returning to normalcy impacting the labor supply and wages.

inflation: as measured by the Personal Consumption Expenditures index, will be 3.2% at the end of 2023 vs. 3.3% they previously projected. By the end of 2024, it expects inflation will be 2.5% reaching 2.1% at the end of 2025. Its 2.0% target is within reach on or after 2025 barring unforeseen circumstances.

Core inflation projections, which excludes energy and food prices, increased: the Fed now anticipates 3.9% by the end of 2023–0.3% above the March estimate. Price concerns will continue among consumers.

Based on these projections, two conclusions about nation’s monetary policy may be deduced the Fed’s report and discussion:

The Fed is cautiously optimistic about the U.S. economy in for the near term (through 2025) while acknowledging uncertainty exists.

Interest rates will continue to increase but at a slower rate than 2022 making borrowing and operating costs higher and creditworthiness might also be under more pressure.

Report Two: CMS

On the same day as the Fed meeting, the actuaries at the Centers for Medicare and Medicaid Services (CMS) released their projections for overall U.S. national healthcare spending for the next several years:

“CMS projects that over 2022-2031, average annual growth in NHE (5.4%) will outpace average annual growth in gross domestic product (GDP) (4.6%), resulting in an increase in the health spending share of GDP from 18.3% in 2021 to 19.6% in 2031. The insured percentage of the population is projected to have reached a historic high of 92.3% in 2022 (due to high Medicaid enrollment and gains in Marketplace coverage). It is expected to remain at that rate through 2023. Given the expiration of the Medicaid continuous enrollment condition on March 31, 2023 and the resumption of Medicaid redeterminations, Medicaid enrollment is projected to fall over 2023-2025, most notably in 2024, with an expected net loss in enrollment of 8 million beneficiaries. If current law provisions in the Affordable Care Act are allowed to expire at the end of 2025, the insured share of the population is projected to be 91.2%. In 2031, the insured share of the population is projected to be 90.5%, similar to pre-pandemic levels.”

The report includes CMS’ assumptions for 4 major payer categories:

Medicare Part D: Several provisions from the Inflation Reduction Act (IRA) are expected to result in out-of-pocket savings for individuals enrolled in Medicare Part D. These provisions have notable effects on the growth rates for total out-of-pocket spending for prescription drugs, which are projected to decline by 5.9% in 2024, 4.2% in 2025, and 0.2% in 2026.

Medicare: Average annual expenditure growth of 7.5% is projected for Medicare over 2022-2031. In 2022, the combination of fee-for-service beneficiaries utilizing emergent hospital care at lower rates and the reinstatement of payment rate cuts associated with the Medicare Sequester Relief Act of 2022 resulted in slower Medicare spending growth of 4.8% (down from 8.4% in 2021).

Medicaid: On average, over 2022-2031, Medicaid expenditures are projected to grow by 5.0%. With the end of the continuous enrollment condition in 2023, Medicaid enrollment is projected to decline over 2023-2025, with most of the net loss in enrollment (8 million) occurring in 2024 as states resume annual Medicaid redeterminations. Medicaid enrollment is expected to increase and average less than 1% through 2031, with average expenditure growth of 5.6% over 2025-2031.

Private Health Insurance: Over 2022-2031, private health insurance spending growth is projected to average 5.4%. Despite faster growth in private health insurance enrollment in 2022 (led by increases in Marketplace enrollment related to the American Rescue Plan Act’s subsidies), private health insurance expenditures are expected to have risen 3.0% (compared to 5.8% in 2021) due to lower utilization growth, especially for hospital services.

And for the 3 major recipient/payee categories:

Hospitals: Over 2022-2031, hospital spending growth is expected to average 5.8% annually. In 2023, faster growth in hospital utilization rates and accelerating growth in hospital prices (related to economy wide inflation and rising labor costs) are expected to lead to faster hospital spending growth of 9.3%. For 2025-2031, hospital spending trends are expected to normalize (with projected average annual growth of 6.1%) as there is a transition away from pandemic public health emergency funding impacts on spending.

Physicians and Clinical Services: Growth in physician and clinical services spending is projected to average 5.3% over 2022-2031. An expected deceleration in growth in 2022, to 2.4% from 5.6% in 2021, reflects slowing growth in the use of services following the pandemic-driven rebound in use in 2021. For 2025-2031, average spending growth for physician and clinical services is projected to be 5.7%, with an expectation that average Medicare spending growth (8.1%) for these services will exceed that of average Private Health Insurance growth (4.6%) partly as a result of comparatively faster growth in Medicare enrollment.

Prescription Drugs: Total expenditures for retail prescription drugs are projected to grow at an average annual rate of 4.6% over 2022-2031. For 2025-2031, total spending growth on prescription drugs is projected to average 4.8%, reflecting the net effects of key IRA provisions: Part D benefit enhancements (putting upward pressure on Medicare spending growth) and price negotiations/inflation rebates (putting downward pressure on Medicare and out-of-pocket spending growth).

Thus, CMS Actuaries believe spending for healthcare will be considerably higher than the growth of the overall economy (GDP) and inflation and become 19.6% of the total US economy in 2031. And it also projects that the economy will absorb annual spending increases for hospitals (5.8%) physician and clinical services (5.3%) and prescription drugs (4.6%).

My take:

Side-by-side, these reports present a curious projection for the U.S. economy through 2031: the overall economy will return to a slightly lower-level pre-pandemic normalcy and the healthcare industry will play a bigger role despite pushback from budget hawks preferring lower government spending and employers and consumers frustrated by high health prices today.

They also point to two obvious near-term problems:

1-The Federal Reserve pays inadequate attention to the healthcare economy. In Chairman Powell’s press conference following release of the FOMC report, there was no comment relating healthcare demand or spending to the broader economy nor a question from any of the 20 press corps relating healthcare to the overall economy. In his opening statement (below), Chairman Powell reiterated the Fed’s focus on prices and called out food, housing and transportation specifically but no mention of healthcare prices and costs which are equivalent or more stressful to household financial security:

“Good afternoon. My colleagues and I remain squarely focused on our dual mandate to promote maximum employment and stable prices for the American people…My colleagues and I are acutely aware that high inflation imposes hardship as it erodes purchasing power, especially for those least able to meet the higher costs of essentials like food, housing, and transportation. We are highly attentive to the risks that high inflation poses to both sides of our mandate, and we are strongly committed to returning inflation to our 2% objective.”

2-Congress is reticent to make substantive changes in Medicare and other healthcare programs despite its significance in the U.S. economy. It’s politically risky. In the June 2 Congressional standoff to lift the $31.4 debt ceiling, cuts to Medicare and Social Security were specifically EXCLUDED. Medicare is 12% of mandated spending in the 2022 federal budget and is expected to grow from a rate of 4.8% in 2022 to 8% in 2023—good news for investors in Medicare Advantage but concerning to consumers and employers facing higher prices as a result.

Even simplifying the Medicare program to replace its complicated Parts A, B, C, and D programs or addressing over-payments to Medicare Advantage plans (in 2022, $25 billion per MedPAC and $75 billion per USC) is politically tricky. It’s safer for elected officials to support price transparency (hospitals, drugs & insurers) and espouse replacing fee for service payments with “value” than step back and address the bigger issue: how should the health system be structured and financed to achieve lower costs and better health…not just for seniors or other groups but everyone.

These two realities contribute to the disconnect between the Fed and CMS. Looking back 20 years across 4 Presidencies, two economic downturns and the pandemic, it’s also clear the health economy’s emergence did not occur overnight as the Fed navigated its monetary policy. Consider:

National health expenditures were $1.366 trillion (13.3% of GDP) in 2000 and $4.255 billion in 2021 (18.3% of the GDP). This represents 210% increase in nominal spending and a 37.5% increase in the relative percentage of the nation’s GDP devoted to healthcare. No other sector in the economy has increased as much.

In the same period, the population increased 17% from 282 million to 334 million while per capita healthcare spending increased 166% from $4,845 to $12,914. This disproportionate disconnect between population and health spending growth is attributed by economists to escalating unit costs increases for the pills, facilities, technologies and specialty-provider services we use—their underlying cost escalation notably higher than other industries.

There were notable changes in where dollars were spent: hospitals were unchanged (from $415 billion/30.4% of total spending to $1.323 trillion/31.4% of total spending), physician services shrank (from $288.2 billion/21.1% of total spending to 664.6 billion/15.6% pf total spending), prescription drugs were unchanged (from $122.3 billion/8.95% to $378 billion/8.88% of total spending) and public health increased slightly (from $43 billion/$3.2% of total spending to $187.6 billion/4.4% of total spending).

And striking differences in sources of funding: out of pocket spending shrank from $193.6/14.2% of payments to $433 billion/10.2% % of payments; private insurance shrank from $441 billion/32.3% of payments to $1.21 trillion/28.4% of total payments; Medicare grew from $224.8 billion/16.5% of payments to $900.8 billion/21.2% of payments; Medicaid + CHIP grew from $203.4 billion/14.9% to $756.2 billion/17.8% of payments; and Veterans Health grew from $19.1 billion/1.4% of payments to $106.0 billion/2.5% of payments.

Thus, if these trends continue…

Aggregate payments to providers from government programs will play a bigger role and payments from privately insured individuals and companies will play a lesser role.

Hospital price increases will exceed price increases for physician services and prescription drugs.

Spending for healthcare will (continue to) exceed overall economic growth requiring additional funding from taxpayers, employers and consumers AND/OR increased dependence on private investments that require shareholder return AND/OR a massive restructure of the entire system to address its structure and financing.

What’s clear from these reports is the enormity of the health economy today and tomorrow, the lack of adequate attention and Congressional Action to address its sustainability and the range of unintended, negative consequences on households and every other industry if left unattended. It’s illustrative of the disconnect between the Fed and CMS: one assumes it controls the money supply while delegating to the other spending and policies independent of broader societal issues and concerns.

The health economy needs fresh attention from inside and outside the industry. Its impact includes not only the wellbeing of its workforce and services provided its users. It includes its direct impact on household financial security, community health and the economic potential of other industries who get less because healthcare gets more.

Securing the long-term sustainability of the U.S. economy and its role in world affairs cannot be appropriately addressed unless its health economy is more directly integrated and scrutinized. That might be uncomfortable for insiders but necessary for the greater good. Recognition of the disconnect between the Fed and CMS is a start!

The U.S. economy added 339,000 jobs in May, while the unemployment rate jumped to 3.7% from 3.4%, the Labor Department said Friday.

Why it matters:

Job gains came in well above forecasters’ expectations — the latest sign that the economy is still underpinned by a hot labor market.

Economists expected a gain of 190,000 jobs last month. The May jobs figures are a pickup from the 294,000 added in April, which was revised up by 41,000. Job gains in March were revised up, too.

Details:

Economic policymakers have kept a close eye on other details from the payrolls report — whether more Americans are joining the workforce and how quickly pay is rising.

The labor force participation rate — the share of workers with a job or hunting for one — held at 62.6% in May.

Meanwhile, average hourly earnings, a measure of pay, rose by 0.3% in May. Compared to the same period a year ago, wages are up 4.3%.

What we’re watching:

The May jobs report is among the final data points Federal Reserve officials will consider before deciding whether to continue the interest rate hiking campaign that began more than a year ago.

Inflation remains too high, and there are concerns that rapid price gains are being fueled by the tight labor market and strong consumer demand.

Still, a top Fed official this week signaled the central bank may skip a rate hike at its meeting later this month.

The labor market added 253,000 payrolls in April, while the unemployment rate dipped to 3.4% — a historically low level.

Why it matters:

Job growth continued to boom last month, the latest sign that economy has strong momentum despite recent bank failures.

Economists expected a gain of 185,000 jobs last month.

Details:

The April job figures are a pickup from the 165,000 jobs added the previous month, which were revised down by 71,000, the Labor Department said on Friday.

The Labor Department said that jobs growth in the previous two months was lower than first estimated: jobs growth was revised down by a combined 149,000 for February and March.

The big picture:

In recent months, more Americans have joined the workforce, helping to ease labor force shortages.

The labor force participation rate — or the share of workers employed or looking for work — held at 62.6% in April.

Average hourly earnings, a measure of wage growth, rose to 0.5% in March. Wages rose 4.4% from the same time last year.

But Fed Chair Jerome Powell said this week that there were signs that the workforce was “coming back into better balance,” though it remained “very tight.”

Wednesday’s inflation print showed a March increase of 0.1% versus February and a year-over-year increase of 5.0%, both of which were better than expected. Markets rallied following the news, at least until the specter of recession caused a reversal of equity gains. The game remains the same: markets want easy money and inflation plus unemployment plus recession equals Fed policy and interest rate levels. Memories of the long 1970s slog through declining and then accelerating inflation levels suggest that it’s too early to declare victory (5.00% is still a long way from the Fed’s 2.00% target range). Nevertheless, hopes increased that the Fed may truly be at or very near the end of its tightening cycle.

Unsustainable Trends

The web version of The Wall Street Journal got rid of its special section on the “2023 Bank Turmoil,” which is a sign that we’re past the worst of this chapter in the Dickensian saga in which our financial system hero navigates all sorts of unfortunate characters and events in search of a new “normal.” Banking distrust ripples continue, with various clients sharing the work they are doing to peel back layers of counterparty risk to understand whether threats loom in downstream financial dependencies. Our regulatory infrastructure has shown itself to be a mile wide and an inch deep, which fuels the kind of skepticism about the reliability of designated watchdogs that leads to self-directed risk assessments.

At one level, this is a helpful and important exercise. The credit and financing structure of any complex healthcare organization is just another supply chain, and it is good to understand how yours works and whether there are vulnerabilities that should be investigated. But it is equally important to assess whether the progression of COVID to inflation to Silicon Valley Bank has caused your organization to drift from risk management into retrenchment. Organizations naturally migrate along a risk continuum as they shift between prioritizing returns or resiliency. The important question isn’t which of these bookends is right, but rather what shapes the migration; the defining event is the journey, and

the critical Board and C-suite conversation is whether your risk management program is enabling or constraining future growth.

We continue to monitor the extraordinary decline in not-for-profit healthcare debt issuance. Sources we rely on show healthcare public debt issuance through Q1 2023 down almost 70% versus Q1 2022. Similar data sources aren’t available, but anecdotal input from our team suggests a comparable drop-off in healthcare real estate as well as alternative funding channels. At the same time, although margins have recently improved, operating cash flow across the sector has been weak over the past 12-18 months. If capital formation from internal and external sources is a sign of vibrancy, healthcare is listless.

The primary culprit isn’t rates; the sector has raised capital in much higher rate environments with fewer financing channels (including most of the pre-2008 era). Instead, the rationale most frequently advanced is concern about the reaction from key credit market constituents during this time of unprecedented operating disruption. Of course, this makes sense, but sitting underneath this basic rationale is the question of what might be called “capital deployment conviction.” Long experience confirms that organizations armed with a growth thesis they believe in aren’t shy about “selling” their story to rating agencies and investors and are willing to suffer adverse outcomes on rates, ratings, or covenants, if that is the price of growth. This isn’t happening right now, which introduces the troubling idea that issuance trends are about much more than credit management.

No matter the root cause, recent capital formation is not sustainable.

Good risk management leads to caution in challenging times, but being too careful elevates the probability that temporary problems become permanent. $2.8 billion in quarterly external capital formation ($11.2 billion annualized—pause and let that annualized amount sink in) is not sufficient to maintain the not-for-profit healthcare sector’s care delivery infrastructure, especially when internal capital generation is equally anemic. But introduce any competitive paradigm and the underinvestment that accompanies this level of capital formation becomes a harbinger of hard times to come. To riff on Aristotle, capitalism abhors a vacuum, and organizations looking to avoid rating pressure today may be elevating the risk of competitive pressure tomorrow; and it is easier to cope with and eventually recover from rating pressure than it is to confront the long-term consequences of well-capitalized and aggressive competitors. Retrenchment might be the right risk management choice in times of crisis, but once that crisis moderates that same strategy can quickly become a risk driver.

Machiavelli, Sun-Tzu, Napoleon, George Washington, and other great tacticians all advanced some variation of the idea that “the best defense is a good offense.” In the world of risk response, this means that the better choice isn’t to de-risk and hibernate but rather to continuously reposition available risk capacity so that you keep the organization moving forward. Star Trek’s philosopher-king Captain James Tiberius Kirk captured the sentiment best when he said, “the best defense is a good offense, and I intend to start offending right now.”

While getting back on the capital horse is important, clearing rates, relative value ratios, risk premia, and flexibility drivers have all reset over the past 12-18 months, so recalibrating a good capital formation program requires reassessment and may lead to very different tactics.

This means that a critical step is to get organized around funding parameters:

debt versus real estate versus other channels; MTI versus non-MTI; tax-exempt versus taxable; public versus private; fixed versus floating. The other important part of this is gaining conviction about capital structure risk versus flexibility: do you want to retain flexibility at the “cost” of incurring the market risk embedded in short-tenor or floating rate structures or do you want to sell flexibility in exchange for capital structure risk reduction?

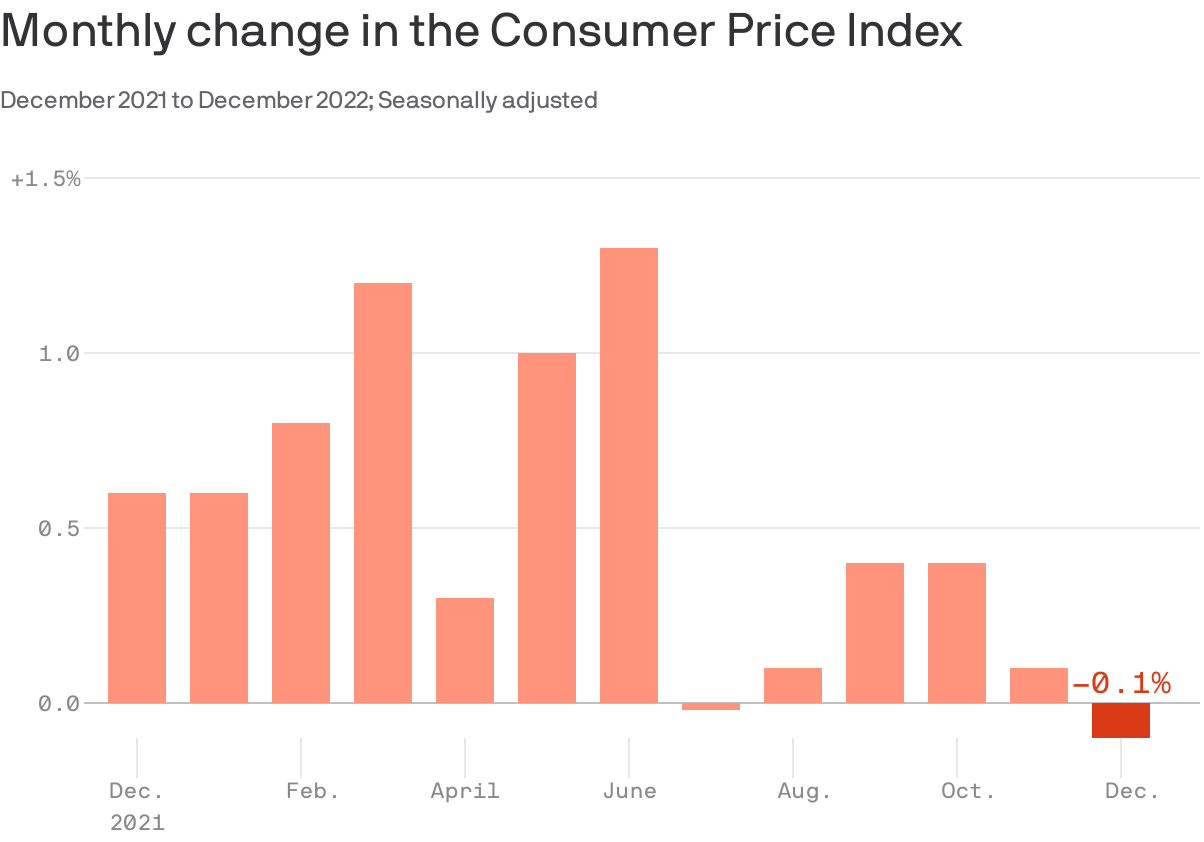

Inflation moderated notably in March as a decline in gas prices helped to pave the way for the slowest pickup in prices in nearly two years, providing relief for many American consumers and a positive talking point for President Biden.

The Consumer Price Index climbed 5 percent in the year through March, down from 6 percent in February. That marked the slowest pace since May 2021.

Still, the details of the report underlined that inflation retains concerning staying power under the surface: A so-called core index that aims to get a clearer sense of price trends by stripping out food and fuel costs, both of which can be volatile, picked up by 5.6 percent from a year earlier. That was up slightly from February’s 5.5 percent increase, and it marked the first acceleration in the yearly number since September.

The mixed signals in the fresh inflation data — which, taken as a whole, suggested that price increases are meaningfully moderating but the progress remains gradual — come at a challenging economic moment for the Federal Reserve. The central bank is the government’s main inflation fighter, and it has been trying to wrestle price increases back under control for slightly more than a year, raising interest rates to nearly 5 percent from near zero as recently as March 2022 to slow the economy and weigh down costs.

Officials are now assessing how their policy changes are working, and they are trying to gauge how much more they need to do to ensure that price increases come fully under control. Inflation has been slowing after peaking at about 9 percent last summer, but the process has been a slow one. It remains a long way back to the 2 percent inflation that was normal before the onset of the pandemic in 2020.

Uncertainty over how quickly and completely price increases will cool is being compounded by recent developments. A series of high-profile bank blowups last month could slow the economy, but it is unclear by how much. Some Fed officials are urging caution in light of the turmoil, even as others warn that the central bank should keep its foot on the economic brake and remain focused on its fight against rising prices.

The new data “solidifies the case for the Fed to do another hike in May, and to proceed cautiously from here,” said Blerina Uruci, chief U.S. economist at T. Rowe Price, later adding that “it will take time to bring inflation down.”

Fed officials target 2 percent inflation, which they define using a different index: the Personal Consumption Expenditures measure, which uses some data from the consumer price measure but is calculated differently and released a few weeks later. That measure has also been sharply elevated.

While Wednesday’s report showed an uptick in core inflation on an annual basis — one that economists had largely expected — Ms. Uruci said that it also offered some encouraging signs. The core inflation measure slowed slightly on a monthly basis, when the March figures were compared to those in February.

And a few important services prices, which the Fed is watching closely for a sense of whether price increases are poised to fade, cooled notably. Rent of primary residences picked up 0.5 percent compared to the prior month, down from 0.8 percent in the previous reading, for instance. Housing inflation broadly is expected to slow in 2023, and that appears to be starting to take hold.

“There are signs in the details to suggest we’re making some progress toward slowing inflation,” Ms. Uruci said. “It’s not where it needs to be, but it’s progress.”

But those hopeful signs do not mean that inflation will fade smoothly and rapidly. The slowdown in the overall index, for instance, may not last: A big chunk of the decline is owed to a drop in gas prices that may not be sustained.

And a few other indexes continued to show quick price increases, including new vehicles and hotel rooms.

As they try to bring inflation to heel, some central bankers have suggested that they may need to further raise interest rates.

The Fed’s latest estimates, released shortly after the collapse of Silicon Valley Bank and Signature Bank in March, suggested that officials could lift rates another quarter-point this year, to just above 5 percent. The central bank will announce its next policy decision on May 3.

On Tuesday, John C. Williams, the president of the Federal Reserve Bank of New York, said that the Fed had more work to do in bringing down price increases and suggested that the central bank’s March forecast for one more quarter-point rate move was still a “reasonable starting place.”

But Austan D. Goolsbee, the president of the Federal Reserve Bank of Chicago, suggested that recent bank failures could make it tougher for businesses and consumers to access credit, slowing the economy, stoking uncertainty and creating a “need to be cautious.”

“We should gather further data and be careful about raising rates too aggressively until we see how much work the headwinds are doing for us in getting down inflation,” Mr. Goolsbee said.

Higher interest rates have made it much more expensive to borrow money to buy a house or expand a business. That is slowing economic activity. As demand cools and the labor market softens, wage growth is also moderating.

That could help to pave the way for cooler inflation. When wages are climbing quickly, companies might charge more to try to cover their labor bills, and their customers are likely to be able to afford the steeper prices. But as households become more strapped for cash, it could become harder for businesses to raise prices without scaring away shoppers.

It may be time to update your inflation narrative.

The ultra-hot readings that defined the first half of 2022 appear to be firmly in the rearview mirror, improving the odds that price pressures can dissipate further without excessive economic pain.

That’s the key takeaway from the December Consumer Price Index released this morning, which confirmed notably cooler inflation as the year came to a close.

Why it matters:

The nation’s inflation problem isn’t over, but so far inflation is slowing while the job market is still healthy, an enviable combination.

As Princeton economist Alan Blinder put it in an op-ed last week, inflation was “vastly lower” in the second half of 2022 than the first; yet, “hardly anyone seems to have noticed.”

By the numbers:

In the final three months of 2022, core inflation (which excludes food and fuel costs) came in at an annualized 3.1% — higher than the Fed aims for, but hardly crisis levels. In the second quarter of the year, that number was 7.9%.

It’s a stunning decline, occurring alongside a labor market that by nearly all measures is still flourishing. Just this morning, the Labor Department announced that jobless claims fell to an ultra-low 205,000 last week.

State of play:

Grocery prices rose 1.1% in the final three months of the year, an uncomfortably high rate, but not as extreme as the rates seen earlier in 2022.

Gasoline prices, pushed up by Russia’s invasion of Ukraine, were once the crucial reason why inflation was rising. In recent months, the opposite has been true: December pump prices slid 9.4%, helping drag the overall index into negative territory.

Disinflation was at work for many other goods, including used cars (-2.5%) and new vehicles (-0.1%) where prices have reversed, helped by easing supply chain bottlenecks.

Shelter costs pushed inflation upward, surging 0.8% in December. But private-sector data points to rents on new leases falling in recent months, which would only filter into the CPI data over time. That makes for a more benign inflation outlook in 2023.

What to watch:

That’s not to say there aren’t risks ahead. The war in Ukraine is ongoing, and another energy price shock could occur.

The Fed has also focused in on the services sector, where price increases have slowed from last summer but remain frothy. The risk is that business costs associated with the still-tight labor market (like higher wages) will pass through to prices for consumers.

The bottom line:

Inflation will still be a worry in 2023, but much less so than it seemed a few months ago.