Concierge primary care company One Medical is reportedly considering a sale after receiving interest from CVS Health, according to Bloomberg. While talks with CVS are no longer active, sources familiar with the situation say the company is weighing offers from other suitors. Also this week, there were rumors that Humana is interested in acquiring Florida-based Cano Health, which provides comprehensive care to over 200K seniors enrolled in Medicare Advantage plans across six states.

The Gist: We’ve long thought that the ultimate buyer for these primary care startups would be large, vertically integrated insurers, as many have struggled to achieve profitability while maintaining strong enrollment growth.

Competition among insurers to acquire care delivery assets has intensified, as payers look to Medicare Advantage as their primary growth vehicle, and aim to amass primary care networks capable of managing their growing senior care businesses.

A recent conversation with a health system CFO made us realize that a long-standing nugget of received healthcare wisdom might no longer be true. For as long as we can remember, economic observers have said that healthcare is “recession-proof”—one of those sectors of the economy that suffers least during a downturn. The idea was that people still get sick, and still need care, no matter how bad the economy gets. But this CFO shared that her system was beginning to see a slowdown in demand for non-emergent surgeries, and more sluggish outpatient volume generally.

Her hypothesis: rising inflation is putting increased pressure on household budgets, and is beginning to force consumers into tougher tradeoffs between paying for daily necessities and seeking care for health concerns. This is having a more pronounced effect than during past recessions, because we’ve shifted so much financial risk onto individuals via high deductibles and cost-sharing over the past decade.

There’s a double whammy for providers: because the current inflation problems are happening in the first half of year, most consumers are nowhere near hitting their deductibles, leading this CFO to forecast softer volumes for at least the next several months, until the usual “post-deductible spending spree” kicks in.

Combined with the tight labor market, which has increased operating costs between 15 and 20 percent, this inflation-driven drop in demand may have hospitals and health systems experiencing their own dose of recession—contrary to the old chestnut.

The momentum behind Medicare Advantage is only growing as more baby boomers age into eligibility, and experts don’t expect the energy around the program to slow down any time soon.

A recent analysis from the Kaiser Family Foundation found that a record 3,834 plans were available for the 2022 plan year in MA, which represents an 8% increase over 2021 and the largest number on the market in a decade.

Open enrollment for Medicare ended Dec. 7, and enrollment numbers will begin trickling out as the year winds down. In 2021, 26 million Medicare beneficiaries, or about 42% of those eligible for the program, were enrolled in an MA plan.

“As Medicare Advantage enrollment continues to grow, insurers seem to be responding by offering more plans and choices to the people on Medicare,” the KFF analysts said.

Part of the appeal of MA to an increasingly savvy consumer base is that it offers additional benefits beyond those afforded people in traditional Medicare, such as vision and dental coverage as well as supports for members’ social needs.

Sachin Jain, M.D., CEO of SCAN Health Plan, told Fierce Healthcare that people are increasingly shopping around for plans, building greater awareness of MA as a whole as well as of the different types of benefits beneficiaries could select.

“We’re seeing that consumers are more sophisticated today than they were a decade ago,” he said. “I think people are realizing that fee-for-service Medicare doesn’t cover a lot of things.”

The KFF report shows that more than 90% of non-group MA plans offer some kind of vision, hearing, telehealth or dental benefits and that most (89%) include prescription drug coverage as well.

Elena McFann, president of Medicare at Anthem, told Fierce Healthcare that throughout the open enrollment period, plans built with benefits that target the social determinants of health and promote whole-person care resonated strongly with members.

Anthem, for example, offers plans that include a slate of essential extra benefits that members can choose from based on what they need the most. Options include grocery cards, transportation benefits and in-home supports.

She said that the grocery benefits and flex cards that allow members to purchase additional hearing, vision and dental coverage have proven particularly popular in this enrollment season.

“What those all point to is the concept of flexibility and helping them lead healthier lives where they really need the help where they are in their journey,” McFann said.

As these benefits prove popular, an increasing number of plans are offering them in tandem. The Better Medicare Alliance released a survey late last month that found the number of plans including supplemental benefits grew by 43% for the 2022 plan year.

The Centers for Medicare & Medicaid Services (CMS) has issued additional flexibilities that allow MA plans to address members’ social determinants of health as the program’s enrollment continues to swell.

Jain said SCAN has seen similar interest in supplemental benefits, and that flexibility afforded to MA plans to adapt to seniors’ needs and expectations is a critical factor in the program’s success.

“When you’re in the business of serving seniors, a lot of what you have to do is anticipate needs that those seniors may not anticipate that they have, give them things they didn’t know they needed,” he said.

McFann said that beneficiaries value plans like these that unite brands they trust and recognize and that partners like Kroger enable insurers to more effectively meet seniors where they are. In its co-branded plans, members can access benefits like Healthy Grocery Cards and stipends to purchase over-the-counter health items.

She said that there has been significant “excitement” around those plans, which are available in four states, during the current enrollment period.

“It gives the Medicare eligibles a sense of familiarity and a sense of comfort, again meeting them on their terms,” McFann said.

However, while many established insurers have set ambitious growth targets in this market and new startups enter the space regularly, they still have plenty of work to do if they want to catch up with the market’s dominant forces: UnitedHealthcare, Humana and Blues plans.

UHC and Humana together account for 45% of the MA market in 2021, according to the KFF analysis. Humana offers plans in 85% of counties and UHC in 74% for 2022.

That means, 89% of Medicare eligibles have access to a Humana plan and 90% have access to a UHC MA plan if they choose, according to the report.

Competition is continuing to grow, though, and both McFann and Jain said they don’t feel the momentum around MA slowing down anytime soon.

“It is those extras and social drivers of health solutions that really have caught on with the Medicare-eligible segment and we expect to see that expand even further,” McFann said.

The Massachusetts Health and Hospital Association is planning to release its semiannual health plan performance report next month and will focus on payers’ finances and enrollment in 2021.

In a May 23 newsletter, the association highlights the 22 percent increase in payers’ net worth during the COVID-19 pandemic, which totals $6.1 billion for all plans in the state. The newsletter also points to the combined $1.2 billion profit made in 2020 and 2021, which exceeds the previous five years combined.

The newsletter does point to the important role insurers played during the pandemic, including providing coverage of medical care, new therapies, vaccinations and COVID-19 testing. Under federal law, payers also provided rebates to premium payers as healthcare utilization decreased significantly. Some payers independently provided financial support to stabilize providers and used their resources to support the pandemic response.

“Despite these new expenses and efforts related to the COVID-19 emergency, health insurance company profits were substantially higher than at any point in recent history given the overwhelming effect of decreased medical utilization,” the newsletter said.

The association also criticized the decrease in claims payouts during the pandemic, arguing surplus revenue should have been used to increase payouts and not increase profits.

The hospital group stated that four specific payers, Harvard Pilgrim Health Care, UnitedHealthcare of New England, Tufts Associated HMO and HMO Blue from BCBS Massachusetts have risk-based capital ratios that approach or exceed 600 percent.

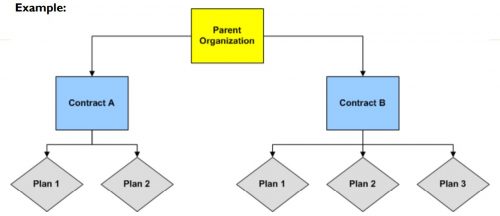

Medicare Advantage (MA) is the private insurance alternative to traditional Medicare. MA organizations contract with Centers for Medicare and Medicaid Services (CMS) to offer eligible beneficiaries residing in a defined geographic service area (a collection of counties) a selection of private plans. Insurers may offer multiple plans across different plan types under one contract. The service area is defined at the contract-level, and for most MA plans, service areas can include a single county or a collection of multiple counties. (There are other types of plans for which there are constraints on the boundaries of the service area, but these don’t account for very much of MA enrollment.)

As MA-offering insurers contract with CMS, they establish networks that govern patient liability for seeing in- and out-of-network providers. Consequently, plans will vary in their cost-sharing structures and benefit designs as they assume different levels of liability for the cost of out-of-network providers. Overall, plans will cover the cost of care (less copays and deductibles) for patients seeing providers in-network, and certain plan types may require that patients pay more for out-of-network services or receive referrals/prior authorization from primary care providers (PCP) to see specialists.

Preferred Provider Organizations (PPOs) are considered the most flexible type of plan in providing access to care and covering it out-of-network. PPO enrollees can use out-of-network providers for covered services without a referral from a PCP, albeit at greater cost to them than in-network providers.

Health Maintenance Organizations (HMOs), in comparison to PPOs, are more restrictive plans that provide less access to care and less coverage for out-of-network providers, with the exception of emergency, urgent, and dialysis care. HMO members are required to select a PCP and must get authorization for most specialty services. For any out-of-network services received, the patient bears the full cost, up to the traditional Medicare rate.

Health Maintenance Organization Point-of- Service (HMO-POS) are a hybrid plan between PPOs and HMOs. Like an HMO, members must select a PCP for care coordination, but they do not need a referral for specialty services. (However, some services may require prior authorization for coverage.) Like a PPO, this plan does provide some coverage for out-of-network providers.

The differences across plan types in access to and cost sharing for out-of-network providers leads to the important question, do MA networks vary by plan within contract? For example, in Figure 1 below, do the beneficiaries enrolled in Plan 1 or 2 under Contract A have the same set of in- and out-of-network providers (likewise for the beneficiaries in Plans 1-3 under contract B)? More specifically, what if Plan 1 is an HMO and Plan 2 is a HMO-POS plan, do they share the same network?

The simple answer seems to be: not necessarily, though more recent regulations attempt to push insurers toward having the same networks across plans within contracts.

For instance, prior to 2019, CMS only reviewed the adequacy of an MA organization’s contracted network under a “triggering event,”like if an organization were to operate a new plan, expand coverage to additional service areas, or in a response to inadequate network complaints. The scope of CMS’ review varied depending on the triggering event that occurred. In some cases, CMS could only conduct partial reviews of a contract’s network, looking at a select set of specialties or counties. A study by the US Government Accountability Office found that between 2013 and 2015, CMS had reviewed less than 1% of all networks. Without regular scrutiny by regulators, it seems likely that networks varied across plans within contracts.

Under the current MA Network Adequacy Criteria Guidance, CMS assesses network adequacy requirements both under triggering events (as explained above) and, separate from that, on a triennial-basis at the contract-level. CMS has previously commented in the 2021 Final Rule that this approach allows them to assess the adequacy of organizations’ networks across all of their plan types (HMOs, PPOs, SNPs) and consider the broadest availability of providers and facilities for an organization. Again, this suggests that insurers may vary networks across plans within contracts.

There are at least two scenarios for which we know certain plans can and likely do have different networks compared with other plans in the contract.

Special Needs Plans (SNPs) are plans designed for individuals with specific diseases or characteristics, such as those who are dual-eligible, have institutional care needs, or have a chronic condition. SNPs can be allowed by regulators to augment the contract’s network to integrate care management teams and specialty providers to accommodate beneficiaries’ complex care needs under the plan’s Model of Care. While SNPs may be granted additional flexibility to alter the contract-level networks established, CMS does not allow SNPs to narrow or shrink that network. They can only expand it.

Provider Specific Plan (PSPs) are plans often found under large, integrated medical groups or provider groups that are the primary bearers of risk. PSP enrollees have access to a smaller subset of in-network providers. Since this plan type has a network of fewer providers than the overall contracted network, organizations must request to offer a PSP from CMS and attest that these plans are in compliance with network adequacy requirements.

Future work with Vericred provider-network data could be one approach to exploring variations in networks among plans under the same contract and service area, beyond the cases listed above. If networks are varying across HMO, PPO, and HMO-POS plans within contracts, it would be interesting to explore just how different they are from one another. Moreover, as CMS reviews continues to review network adequacy requirements at the contract-level (and if networks do differ by plan), one should consider the breadth of the network that organizations are submitting for evaluation. To what extent all plans in a contract are in compliance with network adequacy rules warrants future investigation.

The American Hospital Association, on behalf of its nearly 5,000 healthcare organizations, is urging the Justice Department to probe routine denials from commercial health insurance companies.

Specifically, the AHA is asking the Justice Department to establish a task force to conduct False Claims Act investigations into the insurers that routinely deny payments to providers, according to a May 19 letter to the department.

The request from the AHA comes after HHS’ Office of Inspector General released a report April 27 that found Medicare Advantage Organizations sometimes delayed or denied enrollees’ access to services although the provider’s prior authorization request met Medicare coverage rules.

“It is time for the Department of Justice to exercise its False Claims Act authority to both punish those MAOs that have denied Medicare beneficiaries and their providers their rightful coverage and to deter future misdeeds,” the AHA said in a letter to the Justice Department. “This problem has grown so large — and has lasted for so long — that only the prospect of civil and criminal penalties can adequately prevent the widespread fraud certain MAOs are perpetrating against sick and elderly patients across the country.”

For the quarter ending March 31, 2022, Kaiser Foundation Health Plan, Inc., Kaiser Foundation Hospitals, and their respective subsidiaries (KFHP/H) reported total operating revenues of $24.2 billion and total operating expenses of $24.3 billion compared to total operating revenues of $23.2 billion and total operating expenses of $22.2 billion in the same period of the prior year. There was an operating loss of $0.07 billion, or (0.3%) of total operating revenues, for the first quarter of the year compared to operating income of $1.0 billion, or 4.4%, in the first quarter of 2021.

During the first quarter of 2022, a surge in COVID-19 cases — the steepest since the start of the pandemic — led to a substantial increase in the demand for related care and testing. COVID-19 expenses drove an additional $1.4 billion in expenses. Those expenses, along with the costs of providing care to our members that was deferred earlier in the pandemic, were the primary drivers of additional expenses. In the first quarter of 2022, Kaiser Permanente cared for more than 688,000 patients with COVID-19, including more than 26,000 hospitalized patients, performed 2.5 million COVID-19 diagnostic tests, supplied 1.3 million COVID-19 home tests, and administered 1.4 million vaccine doses. In addition, like the rest of the industry, Kaiser Permanente experienced significant increases in labor costs during the first quarter of 2022, compared to the same period last year and when compared to year-end 2021.

“I am incredibly proud of the extraordinary people of Kaiser Permanente, who have stepped up time and time again to provide high-quality care and service to our members and communities during unparalleled challenges,” said chair and chief executive officer Greg A. Adams. “While in the first quarter, the ongoing effects of the pandemic strained our workforce, communities, and operations, our operating model, which provides both care and coverage, enabled us to continue providing that care even in the face of an unprecedented omicron surge and industrywide labor shortage. Our underlying operating performance remains solid and aligned with expectations.”

In the category of other income and expense, the quarterly loss totaled $889 million, driven largely by investment losses, compared to $1.0 billion in income in the same period of the prior year. For the quarter, there was a net loss of $961 million compared to net income of $2.0 billion in 2021.

Capital spending

Capital spending in the first quarter totaled $872 million compared to $906 million in the same period of the prior year. During the first 3 months of 2022, Kaiser Permanente opened a new, 220,000-square-foot medical facility in Timonium, Maryland, that features 24-hour advanced urgent care and a 24-hour pharmacy, along with an ambulatory surgery center.

“While the increase in pandemic-related expenses, overall rising costs, and investment market losses impacted our finances this quarter, Kaiser Permanente navigated this challenging time providing high-quality care and continued investing in our integrated model including ongoing capital investments to best serve our members. We controlled discretionary spending, optimized COVID-19 testing, addressed surgical backlogs, and managed outside medical expenses,” said executive vice president and chief financial officer Kathy Lancaster. “As we face the ongoing uncertainty and prolonged effects the pandemic is having on the health care industry, we are well positioned to continue delivering high-quality, affordable care and remain vigilant stewards of resources entrusted to us in this dynamic environment.”

Membership

Membership as of March 31, 2022, was 12.6 million, reflecting a growth of more than 88,000 members since December 31, 2021. Medicaid enrollees accounted for almost 33,000 of Kaiser Permanente’s new members.

Each of the six major national payers exceeded Wall Street’s expectations for profit in the first quarter, with UnitedHealth Group out in front as the most profitable company.

The health insurance giant continues its streak of profitability in the first quarter, earning $5 billion in profit. The next-highest company, CVS Health, earned $2.3 billion in profit.

UnitedHealth executives said that the company saw double-digit growth at both UnitedHealthcare, its health plan arm, and Optum. Optum, in particular, has been a bright spot for growth over the past several quarters.

UHG also beat the Street for revenue, bringing in $80.1 billion. That’s a hike of nearly $10 billion compared to the first quarter of 2021, where the company brought in $70.2 billion.

CVS came in second on profit and also on revenue, bringing in $76.8 billion. That’s a double-digit revenue increase from its first-quarter 2021 haul of $69.1 billion.

Revenues were up across its business lines, including a 9% increase at CVS Pharmacy despite a downturn in COVID-19 vaccinations and testing volume in the quarter. Revenues at Aetna, the company’s health plan wing, were up by 12.8%.

Anthem slots in at third place for profitability, earning $1.8 billion in the quarter. That’s up from $1.7 billion in the prior-year quarter. The insurer also had the fourth-highest revenue in the quarter, earning $38.1 billion.

Cigna lands in fourth place for profit and third place for revenue in the quarter, according to its report released Friday. It earned $1.18 billion in profit for the quarter, up from $1.16 billion a year before.

Revenues at Cigna hit $44 billion, up from $41 billion in the first quarter of 2021.

Humanaearned $930 million in profit for the quarter for the fifth-highest earnings among the six companies. Its profits increased from $828 million in the first quarter of 2021. The insurer does land last on the list in revenue, with $24 billion for the quarter.

Centene is in sixth for profitability, earning $849 million for the quarter. That’s up from $699 million in the first quarter of 2021. Centene earned $37.2 billion in revenue for first quarter of 2022, up from $30 billion in the prior-year quarter.

The Minneapolis-based insurer was fined $1M by the Colorado Department of Insurance for failing to complete basic health plan functions, including paying claims, communicating with members, and processing consumer payments. Bright claims its rapid growth, along with COVID-related challenges, contributed to its failures in the Colorado individual and family plan market, where it serves about 50,000 enrollees.

But there are also signs of other problems. After posting $1.2B in losses in 2021, Bright laid off five percent of its employees in March, and says it plans to exit the individual market in six states, which make up less than five percent of its revenue. Bright is instead focusing on integrating its provider arm, NeueHealth, into its insurance business in fast-growing markets like Texas, North Carolina, and Florida.

The Gist: While Bright, along with other insurtechs, has garnered attention with promises of an enhanced customer experience and lower costs, its stumbles with basic health plan functions in Colorado may signal more systemic problems. This news could deter health systems and other providers from partnering with the insurer.

After years of hype, most insurtechs still have minimal market share, and most have yet to turn a profit. Unless performance improves, it may not be long before Bright, Oscar, and others become acquisition targets for larger, more established players.

Anthem has captured the attention of multiple hospitals and health systems across the U.S. as allegations of underpayment and inappropriate denials accumulate.

The insurer has been forced to pay millions already and continues to face off with providers.

Anthem is facing allegations of $70 million in unpaid claims from Portland-based MaineHealth. The health system said earlier this year that its flagship hospital, Maine Medical Center, would no longer contract with the insurer after its contract expires next year. Jeffrey Barkin, MD, president of the Maine Medical Association, said other providers in the state are leaving Anthem for the same reason.

In Georgia, the state insurance commissioner fined Anthem Blue Cross Blue Shield $5 million in March for failing to pay in a timely manner, delays in loading provider contracts and inaccurate provider directories.

VCU Health in Richmond, Va., said last year that 40 percent of its claims with Anthem were more than 90 days old and the insurer owed $385 million, according to the Richmond Times-Dispatch. The Virginia Hospital and Healthcare Association said Anthem has hundreds of millions of dollars in late and unpaid claims to hospitals across the state.

Eleven Indiana hospitals have also had trouble with Anthem. The hospitals alleged Anthem’s reimbursement system added a $50 triage fee and asked for additional patient records to avoid denial for 60 to 70 percent of thousands of emergency room claims from 2017-20. The hospitals alleged the strategy breached their contract with Anthem because hospitals are required to stabilize all patients requesting emergency services. A federal arbiter recently ordered Anthem to pay $4.5 million to the hospitals and said the insurer cannot use its list of diagnostic codes to downgrade or deny claims.

The Indiana hospitals are still counting the denied claims and said they are owed $12 million from Anthem due to downgraded claims.

The American Hospital Association accused Anthem of asking for prior authorizations for routine surgeries as roadblocks to patient care in a letter sent to the insurer last year.In 2021, 53 percent of Anthem’s medical bills for the second quarter were unpaid, amounting to $2.5 billion, according to the Times-Dispatch report.