Blue Shield of California announced a plan to diversify its pharmacy benefit management (PBM) contracts in a bid to improve transparency and reduce costs.

Instead of relying on Woonsocket, RI-based CVS Health’s Caremark as its sole PBM, the health plan and its 4.8M members will be served by five companies, including Amazon Pharmacy for at-home deliveries, Mark Cuban Cost Plus Drugs Company (MCCPDC) for a transparent pricing model, and Prime Therapeutics for negotiations with pharmaceutical companies.

Caremark will remain responsible for Blue Shield’s specialty pharmacy needs, which CVS noted in an investor filing represents over 50 percent of nationwide pharmacy benefit spending.

Blue Shield intends to implement this new system by 2025, and is targeting savings of $500M annually, which translates to 10 to 15 percent of its current spending.

The Gist: Whether Blue Shield saves money with this initiative depends on the whether the benefit of competition in its PBM contracts outweighs the costs of more complex coordination between vendors.

Keeping half of its business tied up with CVS through specialty pharmacy will further limit the potential impact. Nonetheless, it’s noteworthy that pharmacy disruptors like Amazon and MCCPDC have found a major health plan willing to work with them.

Consumers, employers, payers without PBMs, and members of Congress are increasingly dissatisfied with the current pharmacy benefit market structure, and Blue Shield’s move could serve as a catalyst for future shakeups.

Last week Johnson & Johnson followed Merck, Bristol Myers Squibb, and Astellas Pharma by filing a lawsuit against the Biden administration in federal court over the Medicare Drug Price Negotiation Program, established through the 2022 Inflation Reduction Act. PhRMA, the industry trade group, and the US Chamber of Commerce have also filed suits.

The lawsuits claim that the program violates the First and Fifth Amendments by compelling speech, and taking private property for public use without just compensation. The US Chamber of Commerce also filed a motion earlier this month requesting a preliminary injunction.

This flurry of legal activity comes just a month before the Centers for Medicare & Medicaid Services is due to publish its list of the first ten drugs selected for negotiations. The makers of those drugs will then have a month to decide if they will participate in negotiations, risking significant financial penalties if they do not. Any negotiated prices would take effect in 2026.

The Gist:Theability for Medicare to negotiate drug prices is a key pillar of the Biden administration’s healthcare agenda, one the President plans to tout in his upcoming reelection campaign. But the pharmaceutical industry’s legal challenges—multiple, separate suits in different federal courts nationwide—are destined for the Supreme Court if these cases generate conflicting rulings, which is likely. A protracted legal fight will delay or potentially alter the program before it is fully implemented.

With more than two in five American adults considered obese, the potential for GLP-1 agonist drugs like Wegovy, Ozempic, and Mounjaro to revolutionize obesity treatment seems limitless.

In the graphic above, we looked to quantify how much these drugs could potentially change healthcare expenditures and demand. Using Wegovy’s list price of $1.3K per month, a GLP-1 drug prescription for every obese American adult would cost as much as $1.3T annually—30 percent of total US healthcare expenditures.

Analyst projections of GLP-1 drugs forecast revenue to grow by over 5x by 2028, from $3 billion to $16 billion annually. While it’s unlikely that every overweight American will access the drugs, growing use of GLP-1 agonists will likely drive down obesity rates, and downstream care demand could shift in expected and unpredictable ways. Demand for weight-related surgeries, including joint replacements and bariatric surgery, will likely drop. Incidence of chronic diseases like diabetes and cardiovascular disease could also drop, potentially raising life expectancy.

But even if we’re living longer thanks to the new drugs, we’ll still die of something eventually: expect a secondary rise in cancers and Alzheimer’s, as well as surging demand for eldercare. While these effects will take years to materialize, leaders planning for long-term care needs would be wise to consider scenarios where these and other potential “blockbuster” drugs may disrupt demand patterns and spending for a wide range of services.

This month, a panel of expert advisers recommended the Food and Drug Administration (FDA) grant full approval to Leqembi, a drug developed by Eisai and Biogen that targets amyloid plaques in the brain that are linked to the development of Alzheimer’s.

The drug was found to slow cognitive decline in patients by 27 percent over 18 months, though not without some serious side effects, including brain swelling and bleeding. While Leqembi received accelerated FDA approval in January 2023, it is now likely to become the first Alzheimer’s drug that slows the progression of the disease to secure full FDA approval. The Centers for Medicare and Medicaid Services (CMS) recently announced that it intends to cover this new class of Alzheimer’s drugs, as long as prescribing physicians participate in patient registries designed to continue collecting data about the drugs and their efficacy. The FDA is expected to make a final decision on Leqembi by early July.

The Gist: In addition to risks of patient harm, much of the controversy around Leqembi surrounds its $27K list price. Payers, especially Medicare, are worried that it will balloon spending while exposing patients to unaffordable cost-sharing.

With the number of Americans diagnosed annually with Alzheimer’s and other dementias projected to double by 2050, Leqembi has the potential both to help millions and to drive unsustainable spending patterns, and it will be difficult to achieve the former without the latter.

But with full approval likely, a coming frenzy of investor activity to launch memory treatment centers for drug infusion services, capitalizing on the expected huge demand for the drug, seems inevitable.

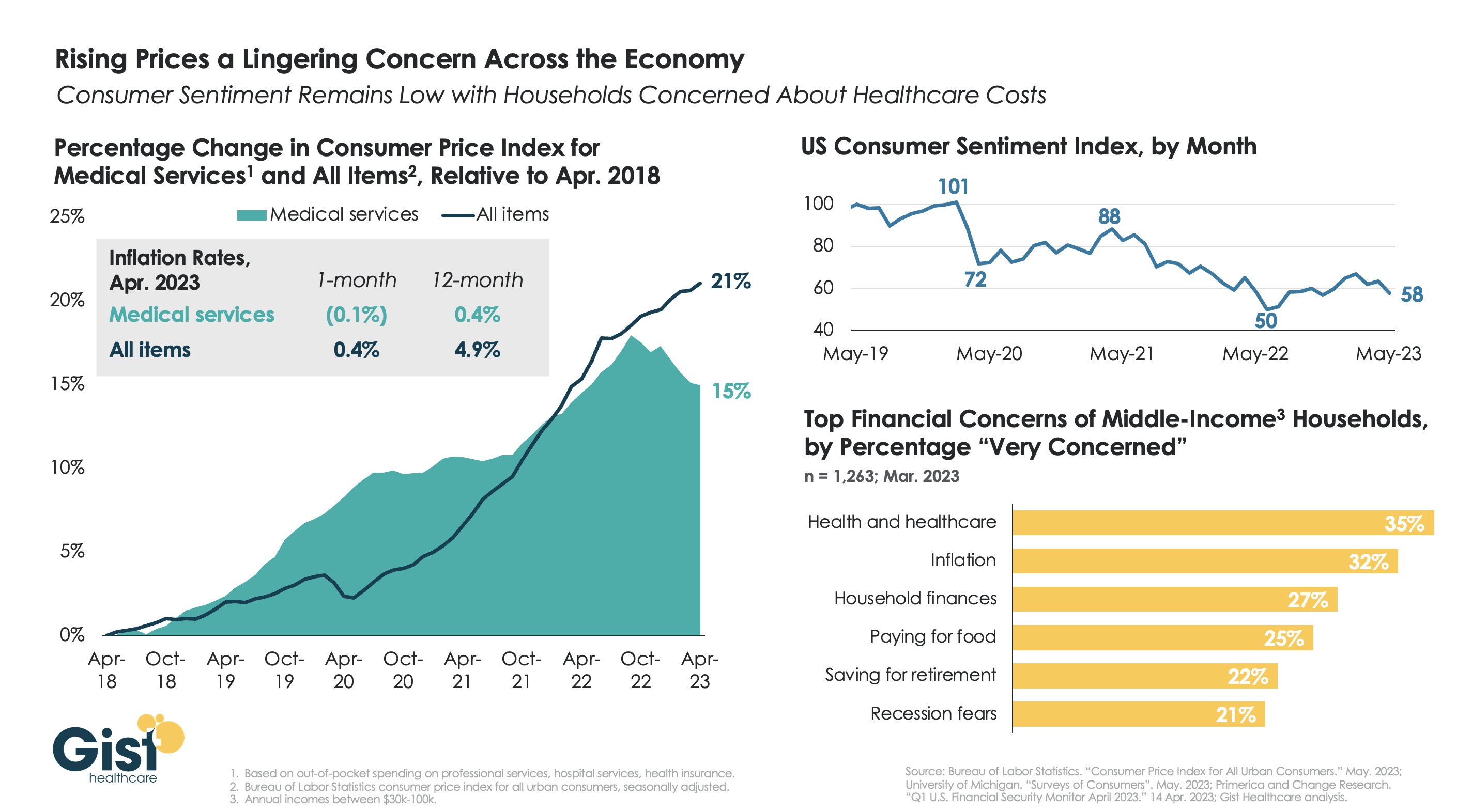

With the latest Bureau of Labor Statistics’ Consumer Price Index (CPI) report revealing the 12-month inflation rate in April 2023 rose again after hitting a recent low in March, we’re using this week’s graphic to show the cumulative picture on price and consumer sentiment changes across the last five years.

Since 2018, the CPI for all goods has risen 21 percent, while medical services have become 15 percent more expensive, in terms of consumer out-of-pocket spending. Leading into COVID, medical service prices were rising faster than general inflation, but the cumulative rise in the price of all goods caught up to medical services in early 2022.

Since December of last year, the price of medical services has actually experienced some deflation, partly due to a lagging decline in insurer profits. Reports of easing inflation had elicited a slight rebound in consumer sentiment, but last month’s 9 percent drop, the largest since June 2022, suggests this confidence is easily shaken.

Unfortunately for healthcare providers, according to a recent poll, fewer consumers worrying about elevated grocery and gas prices means that healthcare has reclaimed the top spot for household financial concerns.

On Monday, the Mark Cuban Cost Plus Drugs Company (MCCPDC) announced via Twitter that it will begin to offer two branded diabetes drugs, Invokana and Invokamet, produced by Janssen, a Johnson & Johnson subsidiary. A month’s supply of these drugs, the first non-generics it has offered, will cost patients around $244, over 60 percent less than average retail prices. Prescriptions for these diabetes drugs fell from nearly 2M in 2020 to under 1M in 2022, and a key Invokama patent will expire next year, both factors that may have influenced Janssen’s decision to partner with MCCPDC.

The Gist: MCCPDC estimates that as many as 1M people who use these or similar drugs could benefit from the lower prices—not only the uninsured but also those considered “underinsured” due to high deductibles.

Even though the deal is for two drugs with declining revenues, selling brand-name drugs from a pharmaceutical heavyweight is a notable step for the company.

As Congress continues to investigate PBMs for driving up drug spending through their pricing tactics, MCCPDC’s move offers a path to PBM disruption through direct competition. By cutting out the rebates retained by health plans and PBMs, MCCDPC can potentially offerbetter net payments to pharmaceutical companies, as well as reduced cost-sharing for patients—an arrangement that benefits both parties at the expense of traditional PBMs.

At a meeting with hospital system CEOs last Wednesday, one asked: “has healthcare reached the tipping point?” I replied ‘not yet but it’s getting close.’

I iterated factors that make these times uniquely difficult in every sector:

An uncertain economy that’s unlikely to fully recover until next year.

The growth of Medicaid and Medicare coverage that shifts their financial shortfall to employers and taxpayers who are fed up and pushing back.

A vicious political environment that rewards partisan brinksmanship and focus-group tested soundbites to manipulate voters on complex issues in healthcare.

The growing domination of Big Business in each sector that have used acquisitions + corporatization to their advantage.

The widening role of private equity in funding non-conventional solutions that disrupt the status quo (and the uncertain future for many of these).

The federal courts system that’s increasingly the arbiter over access, fairness, quality and freedoms in healthcare.

The lingering impact of the pandemic.

And growing public disgust and distrust as the system’s altruism and good will is undermined by pervasive concern for profit.

Unprecedented! But events like those last week prompt hitting the pause button: not everyone pays attention to healthcare like many of us. The slaughter of 6 innocents in Nashville hit close to home: it’s about guns, mental health and life and death. The appeal of tech-giants to press the pause button on Generative AI for at least 6 months was sobering. The ravage of tornados that left thousands insecure without food, housing or hope seemed unfair. Mounting tensions with Russia and complex negotiations with China that reminded us that the U.S. competes in a global economy. And President Trump’s court appearance tomorrow will stoke doubt about our justice system at a time when it’s role in healthcare and society is expanding.

I am a healthcare guy. I am prone to see the world through the lens of the U.S. health industry and keen to understand its trends, tipping points and future. There’s plenty to watch: this week will be no exception. The punch list is familiar:

Medicaid coverage: Many will be watching the fallout of from state redetermination requirements for Medicaid coverage starting as soon as this week with disenrollment in Arizona, Arkansas, Idaho, New Hampshire and South Dakota.

Medicare Advantage: Health insurers will be modifying their Medicare Advantage strategies to adapt to CMS’ risk adjustment and Value-based Insurance Design modifications announced last week.

Prescription drug prices: PBMs and drug companies will face growing skepticism as Senate and House committees continue investigations about price gauging and collusion. Hospitals will be making adjustments to higher operating losses as states cut their Medicaid rolls.

Technology: The 7500 VIVA attendees will be doing follow-up to secure entrées for their technologies and solutions among prospective buyers.

Physicians: And physicians will intensify campaigns against insurers and hospitals now seen as adversaries while lobbying Congress for more money and greater income opportunities i.e., physician-owned hospitals.

Hospitals: On the offense against site-neutral payments, physician owned hospitals, drug prices and inadequate reimbursement from health insurers.

All will soldier on but the food fights in healthcare and broader headwinds facing the industry suggest a tipping point might be near.

I am not a fatalist: the future for healthcare is brighter than its past, but not for everyone. Strategies predicated on protecting the past are obsolete. Strategies that consider consumers incapable of active participation in the delivery and financing of their care are archaic. Strategies that depend on unbridled consolidation and opaque pricing are naïve. And strategies that limit market access for non-traditional players are artifacts of the gilded age gone by when each sector protected its own against infidels outside.

These times call for two changes in every board room and C Suite in of every organization in healthcare:

Broader vision: Understanding healthcare’s future in the broader context of American society, democracy and capitalism: Beltway insiders and academics prognosticate based on lag indicators that are decreasingly valid for forecasting. Media pundits on healthcare fail to report context and underpinnings. Management teams are operating under short-term financial incentives lacking longer-term applicability. Consultants are telling C suites what they want to hear. And boards are being mis-educated about trends of consequence that matter. Understanding the future and building response scenarios is out of sight and out of mind to insiders more comfortable being victims than creators of the new normal.

Board leadership: Equipping boards to make tough decisions: Governance in healthcare is not taken seriously unless an organization’s investors are unhappy, margins are shrinking or disgruntled employees create a stir. Few have a systematic process for looking at healthcare 10 years out and beyond their business. Every Board must refresh its thinking about what tomorrow in healthcare will be and adjust. It’s easier for board to approve plans for the near-term than invest for the long-term: that’s why outsiders today will be tomorrow’s primary incumbents.

So, is U.S healthcare near its tipping point? I don’t know for sure, but it seems clear the tipping point is nearer than at any point in its history. It’s time for fresh thinking and new players.

This week, California Governor Gavin Newsom announced the state has struck a 10-year, $50M partnership with nonprofit drugmaker Civica Rx to produce three versions of generic insulin.

These are intended to be made available nationwide for list prices of no more than $30 a vial.

Production is slated to begin in late 2023 at Civica’s Petersburg, VA plant, and Food and Drug Administration approval will be required. This deal advances California’s CalRx initiative to produce and distribute generic drugs at low costs; according to a Newsom administration official, the low-cost insulin will be available to state residents through mail-order and retail pharmacies. This is the first state-level partnership for Civica, a health system collaborative whose members now cover a third of all US hospital capacity.

The Gist:Since Congress capped insulin copays for Medicare beneficiaries at $35 per month, there’s been a remarkable sea change in the pricing of the drug. Last week, Sanofi joined Eli Lilly and Novo Nordisk, the three of which together control 90 percent of the US insulin market, in dramatically reducing insulin list prices and capping out-of-pocket costs (including for the uninsured), bringing them in line with the costs now paid by Medicare beneficiaries.

Given that most Americans needing insulin are already covered by these policies, the impact of California’s initiative may be muted. However, it sets an important precedent for state partnership in pharmaceutical productionthat will surely expand to other drugs (Newsom stated generic naloxone could be next)—and works to position Newsom as an advocate for lower drug costs, should he seek higher office.

On Wednesday, Indianapolis, IN-based pharmaceutical giant Eli Lilly announced that it will cut its list price for both Humalog and Humulin, its two most commonly prescribed insulin products, by 70 percent. While these changes will go into effect later this year, the company is also immediately expanding its Insulin Value Program, available at participating pharmacies for the commercially insured and upon program enrollment for the uninsured, to match Medicare Part D’s $35 per month out-of-pocket insulin cap. Eli Lilly shared that 30 percent of the US’s 8M insulin users rely on its products, though the company is only cutting prices for its older insulin products.

The Gist: Nearly 30 percent of uninsured and 20 percent of commercially insured insulin users in the US report having to ration their doses due to cost concerns.While it still won’t be providing its insulin for free, as some have demanded, Lilly’s move should help the company gain market share, in addition to generating some good PR—and it’s expected that other large insulin manufacturers will be pressured to follow suit.

But even if a $35 out-of-pocket cap was adopted nationally, Americans would still be paying three times more for their insulin than people in comparable countries.

This week, the Biden administration released a roadmap for implementing three new drug pricing pilots through the Centers for Medicare and Medicaid Innovation (CMMI). These models seek to offer certain common generic drugs to Medicare beneficiaries for two dollars per month, test new ways for how Medicaid pays for expensive cell and gene therapies, and explore alternative reimbursement models for drugs that receive accelerated Food and Drug Administration approval.

The Gist: On the heels of last week’s State of the Union Address, the announcement of these pilots exemplifies the kind of health policy efforts we expect across the remainder of President Biden’s current term: smaller, incremental initiatives to curb healthcare costs at the margins.

But given that all these initiatives have lengthy timelines, in part to allow for industry input, they will likely require the support of the next administration, Biden’s or otherwise, to reach full implementation.