Cartoon – Leadership Types

Peter Drucker, the hall of fame management guru, once famously said that the hardest business organization to run in America was a hospital. If that comment was true so many years ago, imagine what Drucker would have to say about the difficulty of hospital management right now.

Hospital financial performance suffered significantly in 2022 and recovery during 2023 has been quite slow. This trend suggests the question, “What steps are hospital C-suites taking to recover pre-Covid financial stability?”

Erik Swanson manages all analyses for our monthly Kaufman Hall Flash Report and he and I speculated that an industry-wide hospital recovery could not be achieved without reductions in force across the hospital ecosystem.

Some research on our part determined that no official organization tracks hospital layoffs over time but we wondered if we could use our Flash Report data, which is provided to us by Syntellis Performance Solutions, to reach an informed conclusion.

What we were able to do was prepare three types of charts, as follows:

The first chart measures net employee percentage change by month. This chart shows whether overall hospital employment is increasing or decreasing over time and by how much.

The second chart attempts to establish the median turnover for hospitals over an annual period and then measure the deviation from that turnover rate. A greater deviation from what might be termed “normal turnover” suggests that an increasing number of hospitals are using reductions in force to more quickly reduce the cost of doing business.

The third chart shows average FTEs per occupied bed on a comparative basis looking at month-to-month and year-to-year statistics.

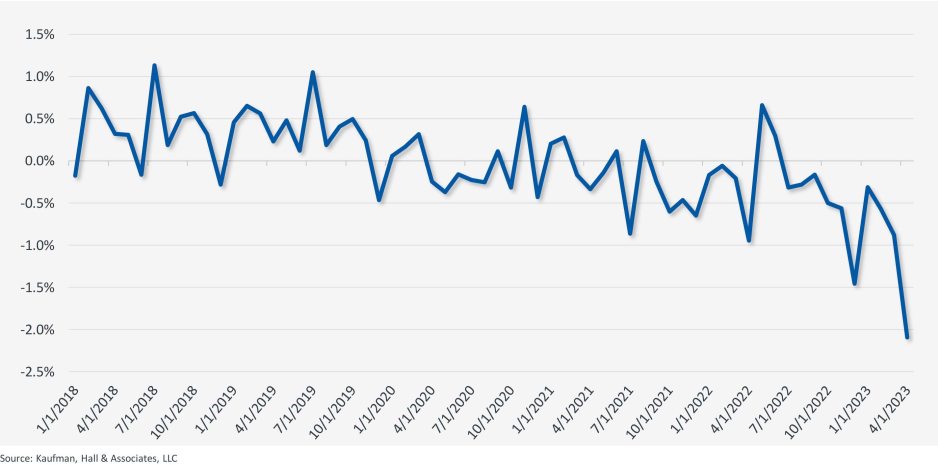

The first chart, Net Employee Percentage Change by Month, begins at January 1, 2018, and continues to March 1, 2023 (Figure 1). Overall additions to hospital employment remained generally positive through January 1, 2020. Overall hospital employment then went generally negative from March 2020 (the onset of Covid restrictions) to March 2022. The reductions in hospital employees during this period were likely the result of the “great resignation” during the worst of the Covid pandemic. But then, from July 2022 to March 2023, overall hospital employees demonstrated by the Flash Report dropped dramatically with an overall 2% decrease at the March 2023 date. This statistic suggests more than simply increased hospital turnover, but rather a formal layoff process initiated across many hospital organizations, along with aggressive management of contract labor.

Figure 1: Net Employee Percentage Change by Month

Image

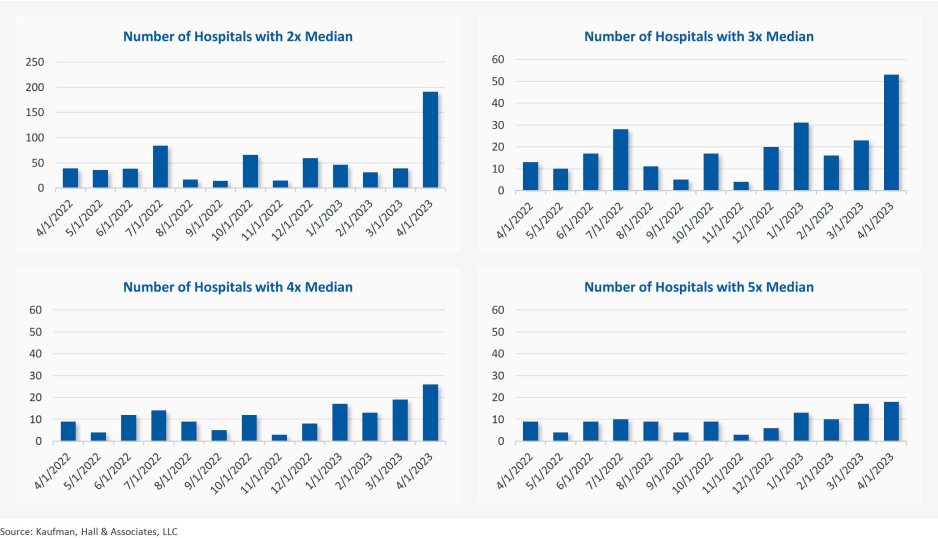

The second chart demonstrates the deviation from expected turnover at levels of 2x, 3x, 4x, and 5x by number of hospitals (Figure 2). No matter which measure you examine, the deviation of employees from expected turnover spiked significantly in April 2023 and even more so in May 2023. This again suggests the aggressive management of labor costs that likely could not occur without the intentional reduction of actual positions and/or the cost of these positions.

Figure 2: Number of Hospitals with Deviations from Expected Turnover at 2x, 3x, 4x, and 5x the Median

Image

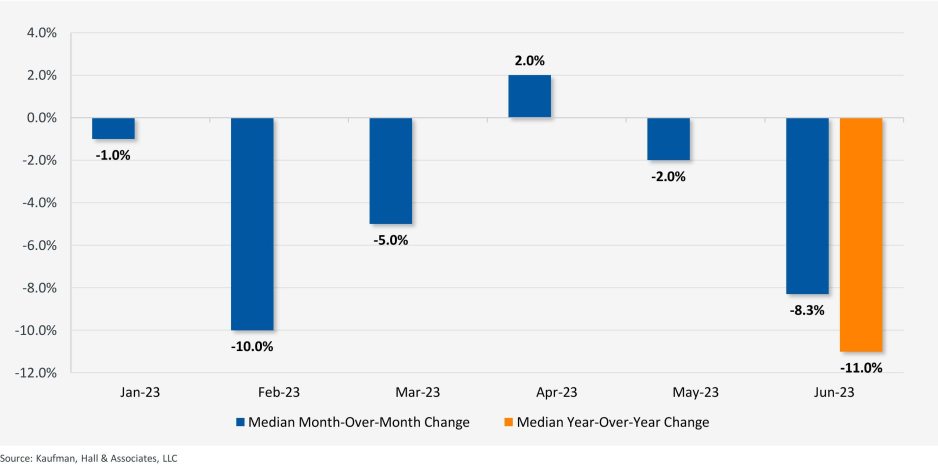

The last chart provides a remarkable set of observations (Figure 3). FTEs per adjusted occupied bed (AOB) declined by 8.3% between June 2023 and July 2023. The year-over-year variation for July 2023 was a decline of 11.01%. Our data further reveals that the FTE per AOB statistic has declined in five of the past six months on a month-over-month basis.

Figure 3: Median Change in FTEs per Adjusted Occupied Bed by Month

Image

The conclusion here is that the return of the hospital industry to pre-Covid financial results has been no walk in the park. 2022 was, of course, a dismal financial year for the hospital industry. And while 2023 has shown improvement, the usual management steps to recovery have been only moderately effective. The data and analysis above demonstrate that C-suites across America are moving to stronger measures to assure the financial survivability and competitiveness of their organizations.

There is no revenue solve here, or at least not in the current environment: costs must come down and they must come down materially. From the sense and the trend of the data it would seem that hospital executive teams get the joke.

A couple of months ago, I got a call from a CEO of a regional health system—a long-time client and one of the smartest and most committed executives I know. This health system lost tens of millions of dollars in fiscal year 2022 and the CEO told me that he had come to the conclusion that he could not solve a problem of this magnitude with the usual and traditional solutions. Pushing the pre-Covid managerial buttons was just not getting the job done.

This organization is fiercely independent. It has been very successful in almost every respect for many years. It has had an effective and stable board and management team over the past 30 to 40 years.

But when the CEO looked at the current situation—economic, social, financial, operational, clinical—he saw that everything has changed and he knew that his healthcare organization needed to change as well. The system would not be able to return to profitability just by doing the same things it would have done five years or 10 years ago. Instead of looking at a small number of factors and making incremental improvements, he wanted to look across the total enterprise all at once. And to look at all aspects of the enterprise with an eye toward organizational renovation.

I said, “So, you want a makeover.”

The CEO is right. In an environment unlike anything any of us have experienced, and in an industry of complex interdependencies, the only way to get back to financial equilibrium is to take a comprehensive, holistic view of our organizations and environments, and to be open to an outcome in which we do things very differently.

In other words, a makeover.

Consider just a few areas that the hospital makeover could and should address:

There’s the REVENUE SIDE: Getting paid for what you are doing and the severity of the patient you are treating—which requires a focus on clinical documentation improvement and core revenue cycle delivery—and looking for any material revenue diversification opportunities.

There is the relationship with payers: Involving a mix of growth, disruption, and optimization strategies to increase payments, grow share of wallet, or develop new revenue streams.

There’s the EXPENSE SIDE: Optimizing workforce performance, focusing on care management and patient throughput, rethinking the shared services infrastructure, and realizing opportunities for savings in administrative services, purchased services, and the supply chain. While these have been historic areas of focus, organizations must move from an episodic to a constant, ongoing approach.

There’s the BALANCE SHEET: Establishing a parallel balance sheet strategy that will create the bridge across the operational makeover by reconfiguring invested assets and capital structure, repositioning the real estate portfolio, and optimizing liquidity management and treasury operations.

There is NETWORK REDESIGN: Ensuring that the services offered across the network are delivered efficiently and that each market and asset is optimized; reducing redundancy, increasing quality, and improving financial performance.

There is a whole concept around PORTFOLIO OPTIMIZATION: Developing a deep understanding of how the various components of your business perform, and how to optimize, scale back, or partner to drive further value and operational performance.

Incrementalism is a long-held business approach in healthcare, and for good reason. Any prominent change has the potential to affect the health of communities and those changes must be considered carefully to ensure that any outcome of those changes is a positive one. Any ill-considered action could have unintended consequences for any of a hospital’s many constituencies.

But today, incrementalism is both unrealistic and insufficient.

Just for starters, healthcare executive teams must recognize that back-office expenses are having a significant and negative impact on the ability of hospitals to make a sufficient operating margin. And also, healthcare executive teams must further realize that the old concept of “all things to all people” is literally bringing parts of the hospital industry toward bankruptcy.

As I described in a previous blog post, healthcare comprises some of the most wicked problems in our society—problems that are complex, that have no clear solution, and for which a solution intended to fix one aspect of a problem may well make other aspects worse.

The very nature of wicked problems argues for the kind of comprehensive approach that the CEO of this organization is taking—not tackling one issue at a time in linear fashion but making a sophisticated assessment of multiple solutions and studying their potential interdependencies, interactions, and intertwined effects.

My colleague Eric Jordahl has noted that “reverting to a 2019 world is not going to happen, which means that restructuring is the only option. . . . Where we are is not sustainable and waiting for a reversion is a rapidly decaying option.”

The very nature of the socioeconomic environment makes doing nothing or taking an incremental approach untenable. It is clearly beyond time for the hospital industry makeover.

However cynical it may seem, Machiavelli’s The Prince has long been recognized as a source of insights for anyone trying run a business or gain power in one. A ferocious little treatise of under 100 pages, The Prince was aimed at Lorenzo de’ Medici, the iron-handed Florentine ruler, by an author hoping to regain the proximity to power that he formerly enjoyed.

But modern corporations aren’t principalities ruled by autocrats. They are, in fact, more like republics, their leaders dependent on the support of directors, employees, customers, investors, and one another. That is why, in turning to Machiavelli for management wisdom, we would be well served to leave aside The Prince in favor of another of his works, one that is less known but perhaps more to the point. Don’t be fooled by the academic-sounding title; Discourses on Livy has a great deal to teach us about leadership in any organization resembling a republic. Chances are, that includes your business.

Published posthumously in 1531, Discourses draws on the ancient Roman historian (among others) to analyze the nature of power in public life. Like The Prince, this is not a handbook for saints. But the author was a brilliant student of human nature, and not one to underestimate the potential of a determined individual. In Discourses, he firmly asserts the importance of an individual founder in establishing or renovating a republic—and by extension, for our purposes, a business. A prudent founder, he writes, “must strive to assume sole authority.”

Yet a single person cannot sustain an enterprise in the long run. That is only possible if the founder’s vision and talents result in an institution supported by stakeholders who can carry the venture into the future. “Kingdoms which depend only upon the exceptional ability of a single man are not long enduring,” Machiavelli writes, “because such talent disappears with the life of the man, and rarely does it happen to be restored in his successor.”

Besides, princes have no monopoly on wisdom. Despite the notorious unpredictability of the mob, the author acknowledged the wisdom of crowds when he asserted that “the multitude is wiser and more constant than a prince.” Machiavelli was also insightful about succession: “After an excellent prince, a weak prince can maintain himself,” he observed with admirable economy in one chapter’s epigraph, “but after a weak prince, no kingdom can be maintained with another weak one.”

Many of the epigraphs are bull’s-eyes of this kind. Take this one, for example: “Whoever wishes to reform a long-established state in a free city should retain at least the appearance of its ancient ways.” This is worth doing even if you make massive changes, because, Machiavelli notes, “men in general live as much by appearances as by realities; indeed, they are often moved more by things as they appear than by things as they really are.”

Honesty may be the best policy, but that is not a maxim ever attributed to Machiavelli. In keeping with the notion that people attend largely to appearances, he says leaders compelled to do something by necessity should consider pretending their course of action was undertaken out of generosity. In another chapter, he argues, “Cunning and deceit will serve a man better than force to rise from a base condition to great fortune.”

Machiavelli, of course, took a hard-headed view of humanity, believing that people act largely out of self-interest, whether to gratify their egos or sate their desire for material wealth, and that, for better or worse, actions tend to be judged by their consequences. Indeed, he was very much what philosophers call a consequentialist, arguing that, in some contexts, bad things must be done to achieve good ends achievable in no other way. This is not to say that law-breaking or other unethical acts are justified—even some of Machiavelli’s contemporaries considered such advice controversial—but every business leader knows that hard decisions must be made, be it the closing of a venerable division or taking a company in a risky new direction, for the long-term good of the enterprise.

Even when advocating something like mercy, Machiavelli did so with consequences in mind. He argued, for example, that failure should not be harshly punished, especially if it arises from ignorance rather than malice. Roman generals, he notes, had difficult and dangerous jobs, and Rome understood that if military leaders had to worry about “examples of Roman commanders who had been crucified or otherwise put to death when they had lost a day’s battles, it would be impossible for that commander, beset by so many suspicions, to make courageous decisions.”

If punishment should not be meted out lightly, neither should rewards be delayed. If you don’t cultivate loyalty and support from others in good times through open-handedness, Machiavelli says, those people certainly won’t have your back when things get rough. Doling out rewards only in the face of tough competition or harsh circumstances will lead subordinates to believe “that they gained this favour not from you but from your adversaries, and since they must fear that after the danger has passed you will take back from them what you have been forced to give them, they will feel no obligation to you whatsoever.”

Republics, in his view, have no choice but to grow, for “it is impossible for a republic to succeed in standing still.” Companies are the same. But acquisitions—whether in battle or by purchase—must be carried out with care, for “conquests made by republics which are not well organized, and which do not proceed according to Roman standards of excellence, bring about their ruin rather than their glorification.”

Finally, Machiavelli was well aware of the risks of advice-giving, so much so that he gave one chapter the title “Of the danger of being prominent in counselling any enterprise, and how that danger increases with the importance of such enterprise.” Consultants, take note. Just don’t let the clients catch you reading Machiavelli.