Pittsburgh-based UPMC’s operating income hit $100.4 million in the first quarter — up from $50.4 million in the prior year period — due to increased patient volumes, the growth of its insurance division and equity earnings in its investment in CarepathRx.

UPMC said quarterly results were partially offset by reduced pandemic-related funding and increased labor costs. First-quarter revenue increased 12 percent year over year to $6.9 billion and expenses rose 11 percent to $6.8 billion.

Year over year, UPMC’s admissions and observations increased 6 percent, while its health plan grew by almost 500,000 members to 4.5 million. UPMC attributed the 12 percent jump to the expansion of its behavioral health and Medicaid programs in eastern Pennsylvania.

“While meeting strong patient preference for care to be provided more conveniently in ambulatory settings closer to home, UPMC’s outpatient revenue increased 9 percent compared to a year ago,” CFO Edward Karlovich said in a May 25 news release. “Our patient volumes continue to shift from inpatient to outpatient settings.”

After including the performance of its investment portfolio and other nonoperating items, the 40-hospital system reported an overall gain of $187.3 million, compared with a loss of $226.2 million in the first quarter of 2022.

Fitch Ratings Senior Director Kevin Holloran dubbed 2022 the worst operating year ever and most nonprofit health systems reported large losses. However, the losses are shrinking and some systems have even reported gains during 2023 so far.

Cleveland Clinic reported $335.5 million net income for the first quarter of the year, compared with a $282.5 million loss over the same period in 2022. The health system reported revenue of $3.5 billion for the quarter. Cleveland Clinic has 321 days cash on hand, which puts it in a strong position for the future.

Boston-based Mass General Brighamreported $361 million gain for the second quarter ending March 31, which is up from a $867 million loss in the same period last year. The health system reported quarterly revenue jumped 11 percent year over year to $4.5 billion. The system’s quarterly loss on operations was down significantly this year, hitting $8 million, compared to $183 million last year.

Renton, Wash.-based Providence reported first quarter revenues were up 5.1 percent in 2023 to $7.1 billion, and operating loss is also moving in the right direction. The system reported $345 million operating loss in the first quarter of 2023, down from $510 million last year.

All three systems cited ongoing labor shortages and labor costs as a challenge, but are working on initiatives to reduce expenses. Cleveland Clinic and Mass General Brigham reported operating margin improvement to nearly positive numbers.

Kaiser Permanente, based in Oakland, Calif., also reported operating income at $233 million for the first quarter of the year, an increase from $72 million operating loss over the same period last year. The system is focused on advancing value-based care for the remainder of the year and its health plan grew more than 120,000 members year over year.

Even more regional systems are stemming their losses. SSM Health, based in St. Louis, went from a $57.4 million loss for the first quarter of 2022 to $16.5 million quarterly loss this year. Revenue increased 13.3 percent to $2.5 billion for the quarter, with increased labor expenses and inflation on supply costs continuing to weigh on the system.

UCHealth in Aurora, Colo., also reported a first quarter income of $61.8 million and revenue of more than $5 billion.

Not every system is seeing losses decline. Chicago-based CommonSpirit Health, which reported larger operating losses in the first quarter year over year, hitting $658 million and $1.1 billion for the nine-month’s end March 31. The system was able to reduce contract labor costs, but still finds hiring a challenge and spent time last year recovering from a cybersecurity incident.

Hospitals face a long road to financial recovery from the pandemic as inflation persists and labor shortages become the norm, but movement in the right direction is welcome.

Renton, Wash.-based Providence has reported a $345 million operating loss in the first quarter on revenue of $6.8 billion.

While revenues were up on the same period in 2022, expenses also rose 5.1 percent to total $7.1 billion. The operating loss compares with a $510 million loss in the first quarter of 2022.

Improving non-operating income, mainly from investment returns, helped mitigate the net loss to $117 million compared with an $840 million net loss in the same period last year, excluding the disaffiliation of Newport Beach, Calif.-based Hoag.

The 51-hospital system reiterated it is taking a number of initiatives to reduce some of its costs under its Destination Health 2025 Recover and Renew plan. One of those prime areas of focus is reducing staffing costs, particularly in regard to contract labor, which continues to be a challenge for Providence.

“With current labor shortages, the use of premium labor, including the number and wage rate of agency nurses, continues to be significantly higher than in previous years,” management said in its filing. “Several initiatives are underway to reduce those expenses in combination with increasing core productivity.”

Providence is also undergoing portfolio management reassessment to try and improve efficiencies and save costs, according to the filing.

The system, which had $7.8 billion long-term debt as of March 31, provided $563 million in community benefit in the first quarter, up from $412 million in the same period of 2022.

“Together, we will continue meeting the health care needs of our communities, no matter how challenging the environment gets, and will ensure the mission of Providence thrives for years to come,” Rod Hochman, MD, Providence president and CEO said in the filing.

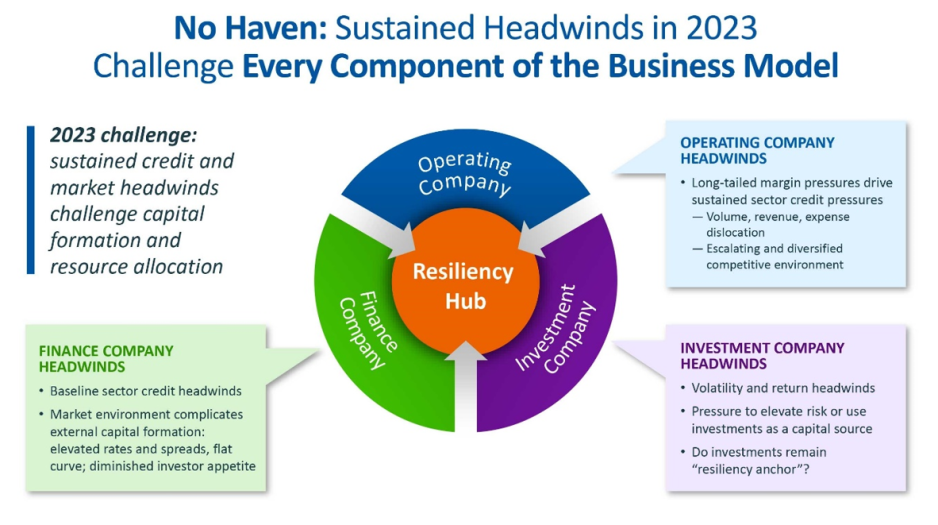

For the first time in recent history, we saw all three functions of the not-for-profit healthcare system’s financial structure suffer significant and sustained dislocation over the course of the year 2022 (Figure above).

The headwinds disrupting these functions are carrying over into 2023, and it is uncertain how long they will continue to erode the operating and financial performance of not-for-profit hospitals and health systems.

The Operating Function is challenged by elevated expenses, uncertain recovery of service volumes, and an escalating and diversified competitive environment.

The Finance Function is challenged by a more difficult credit environment (all three rating agencies

now have a negative perspective on the not-forprofit healthcare sector), rising rates for debt, and a diminished investor appetite for new healthcare debt issuance. Total healthcare debt issuance in 2022 was $28 billion, down sharply from a trailing two-year average of $46 billion.

The Investment Function is challenged by volatility and heightened risk in markets concerned with the Federal Reserve’s tightening of monetary policy and the prospect of a recession. The S&P 500—a major stock index—was down almost 20% in 2022. Investments had served as a “resiliency anchor” during the first two years of the pandemic; their ability to continue to serve that function is now in question.

A significant factor in Operating Function challenges is labor: both increases in the cost of labor and staffing shortages that are forcing many organizations to run at less than full capacity. In Kaufman Hall’s 2022 State of Healthcare Performance Improvement Survey, for example, 67% of respondents had seen year-over-year increases of more than 10% for clinical staff wages, and 66% reported that they had run their facilities at less-than-full capacity because of staffing shortages.

These are long-term challenges,

dependent in part on increasing the pipeline of new talent entering healthcare professions, and they will not be quickly resolved. Recovery of returns from the Investment Function is similarly uncertain. Ideally, not-for-profit health systems can maintain a one-way flow of funds into the Investment Function, continuing to build the basis that generates returns. Organizations must now contemplate flows in the other direction to access

funds needed to cover operating losses, which in many cases would involve selling invested assets at a loss in a down market and reducing the basis available to generate returns when markets recover.

The current situation demonstrates why financial reserves are so important:

many not-for-profit hospitals and health systems will have to rely on them to cover losses until they can reach a point where operations and markets have stabilized, or they have been able to adjust their business to a new, lower margin environment. As noted above, relief funding and the MAAP program helped bolster financial reserves after the initial shock of the pandemic. As the impact of relief funding wanes and organizations repay remaining balances under the MAAP program, Days Cash on Hand has begun to shrink, and the need to cover operating losses is hastening this decline. From its highest

point in 2021, Days Cash on Hand had decreased, as of September 2022, by:

29% at the 75th percentile, declining from 302 to 216 DCOH (a drop of 86 days)

28% at the 50th percentile, declining from 202 to 147 DCOH (a drop of 55 days)

49% at the 25th percentile, declining from 67 to 34 DCOH (a drop of 33 days)

Financial reserves are playing the role for which they were intended; the only question is whether enough not-for-profit hospitals and health systems have built sufficient reserves to carry them through what is likely to be a protracted period of recovery from the pandemic.

KEY TAKEAWAYS

All three functions of the not-for-profit healthcare system’s financial structure—operations, finance, and investments—suffered significant and sustained dislocation over the course of 2022.

These headwinds will continue to challenge not-forprofit

hospitals and health systems well into 2023.

Days Cash on Hand is showing a steady decline, as the impact of relief funding recedes and the need to cover operating losses persists.

Financial reserves are playing a critical role in covering operating losses as hospitals and health systems struggle to stabilize their operational and financial performance.

Conclusion

Not-for-profit hospitals and health systems serve many community needs. They provide patients access to healthcare when and where they need it. They invest in new technologies and treatments that offer patients and their families lifesaving advances in care. They offer career opportunities to a broad range of highly skilled professionals, supporting the economic health of the communities they serve.

These services and investments are expensive and cannot be covered solely by the revenue received from providing care to patients.

Strong financial reserves are the foundation of good financial stewardship for not-for-profit hospitals and health systems.

Financial reserves help fund needed investments in facilities and technology, improve an organization’s debt capacity, enable better access to capital at more affordable interest rates, and provide a critical resource to meet expenses when organizations need to bridge periods of operational disruption or financial distress. Many hospitals and health systems today are relying on the strength of their reserves to navigate a difficult

environment; without these reserves, they would not be able to meet their expenses and would be at risk of closure.

Financial reserves, in other words, are serving the very purpose for which they are intended—ensuring that hospitals and health systems can continue to serve their communities in the face of challenging operational and financial headwinds.

When these headwinds have subsided, rebuilding these reserves should be a top priority to ensure that our not-for-profit hospitals and health systems can remain a vital resource for the communities they serve.

Using data from Kaufman Hall’s National Hospital Flash Report, as well as publicly available investor reports for some of the nation’s largest nonprofit health systems, the graphic above takes stock of the current state of health system margins.

The median US hospital has now maintained a negative operating margin for a full year. Some good news may be on the horizon, as the picture is slightly less gloomy than a year ago, with year-over-yearrevenues increasing seven points more than total expenses.

However, the external conditions suppressing operating margins aren’t expected to abate, and many large health systems are still struggling.

Among large national non-profits Ascension, CommonSpirit Health, Providence, and Trinity Health, operating income in FY 2022 decreased 180 percent on average, and investment returns fell by 150 percent on average, compared to the year prior.

While health systems’ drop in investment returns mirrors the overall stock market downturn, and is largely comprised of unrealized returns, systems may not be able to rely on investment income to make up for ongoing operating losses.

Renton, Wash.-based Providence suffered its third credit downgrade in less than three weeks when Moody’s revised a rating on bonds the 51-hospital system holds to “A2” from “A1.”

Such a rating reflects an expectation margins will remain weak in 2023. The outlook is negative.

The move follows similar actions by Fitch Ratings March 17 and S&P Global March 21 amid an anticipated multiyear process of financial recovery.

Capital expenditure for Providence is expected to be restricted after the completion of a couple of major projects this year to effect “margin recovery,” Moody’s said.

Providence reported a $1.7 billion operating loss in 2022.

Sacramento, California-based Sutter Health crossed the finish line strong but ultimately wrapped up 2022 with a $249 million net loss, a substantial decline from the $1.1 billion profit of 2021.

A $628 million dip in investment income, a $578 million decrease in net unrealized gains and losses on investments and the $208 million disaffiliation of Samuel Merritt University all contributed to the nonprofit’s year-over-year decline.

Still, the tally is a $289 million improvement over the $538 million net loss the system had reported at the year’s nine-month mark.

The loss was also blunted by a 12-month operating income of $278 million—a bump over the $199 million operating income of 2021 and a feather in Sutter’s cap at a time when several other major nonprofit systems are reporting hundreds of millions in operating losses.

“Our operating financial performance has put Sutter in a position to reinvest more within the system, which can help support even higher quality, equitable healthcare for patients throughout California,” CEO and President Warner Thomas said in a press release.

Sutter’s total operating revenues rose 3.9% year over year to $14.8 billion in 2022. This was just ahead of the 3.3% increase to $14.5 billion in total operating expenses. The system wrote in a release that “like other healthcare organizations around the country,” it was not immune from inflationary pressures on expenses like wages and benefits or supplies.

However, the strong results of its 2021 financial recovery initiative and patient volumes “returning to near-2019 levels by year’s end” give Sutter “a stable base to invest in the future,” the system said.

Here are 14 health systems with strong operational metrics and solid financial positions, according to reports from credit rating agencies Fitch Ratings, Moody’s Investors Service and S&P Global.

1. Ascension has an “AA+” rating and stable outlook with Fitch. The St. Louis-based system’s rating is driven by multiple factors, including a strong financial profile assessment, national size and scale with a significant market presence in several key markets, which produce unique credit features not typically seen in the sector, Fitch said.

2. Berkshire Health has an “AA-” rating and stable outlook with Fitch. The Pittsfield, Mass.-based system has a strong financial profile, solid liquidity and modest leverage, according to Fitch.

3. ChristianaCare has an “Aa2” rating and stable outlook with Moody’s. The Newark, Del.-based system has a unique position with the state’s largest teaching hospital and extensive clinical depth that affords strong regional and statewide market capture, and it is expected to return to near pre-pandemic level margins over the medium term, Moody’s said.

4. Cone Health has an “AA” rating and stable outlook with Fitch. The rating reflects the expectation that the Greensboro, N.C.-based system will gradually return to stronger results in the medium term, the rating agency said.

5. Harris Health System has an “AA” rating and stable outlook with Fitch. The Houston-based system has a “very strong” revenue defensibility, primarily based on the district’s significant taxing margin that provides support for operations and debt service, Fitch said.

6. Johns Hopkins Medicine has an “AA-” rating and stable outlook with Fitch. The Baltimore-based system has a strong financial role as a major provider in the Central Maryland and Washington, D.C., market, supported by its excellent clinical reputation with a regional, national and international reach, Fitch said.

7. Orlando (Fla.) Health has an “AA-” and stable outlook with Fitch. The system’s upgrade from “A+” reflects the continued strength of the health system’s operating performance, growth in unrestricted liquidity and excellent market position in a demographically favorable market, Fitch said.

8. Rady Children’s Hospital has an “AA” rating and stable outlook with Fitch. The San Diego-based hospital has a very strong balance sheet position and operating performance and is also a leading provider of pediatric services in the growing city and tri-county service area, Fitch said.

9. Rush System for Health has an “AA-” and stable outlook with Fitch. The Chicago-based system has a strong financial profile despite ongoing labor issues and inflationary pressures, Fitch said.

10. Salem (Ore.) Health has an “AA-” rating and stable outlook with Fitch. The system has a “very strong” financial profile and a leading market share position, Fitch said.

11. TriHealth has an “AA-” rating and stable outlook with Fitch. The rating reflects the Cincinnati-based system’s strong financial and operating profiles, as well as its broad reach, high-acuity services and stable market position in a highly fragmented and competitive market, Fitch said.

12. UCHealth has an “AA” rating and stable outlook with Fitch. The Aurora, Colo.-based system’s margins are expected to remain robust, and the operating risk assessment remains strong, Fitch said.

13. University of Kansas Health System has an “AA-” rating and stable outlook with S&P Global. The Kansas City-based system has a solid market presence, good financial profile and solid management team, though some balance sheet figures remain relatively weak to peers, the rating agency said.

14. Willis-Knighton Health System has an “AA-” rating and stable outlook with Fitch. The Shreveport, La.-based system has a “dominant inpatient market position” and is well positioned to manage operating pressures, Fitch said.

Financial analysts have said that 2022 may have been the worst year for hospital finances in decades. This year looks like it will be yet another year of financial underperformance, with rural providers in especially dire circumstances.

What’s driving this bleak financial reality? It’s “primarily an expense story,” said Erik Swanson, a senior vice president at Kaufman Hall‘s data analytics practice.

“Growth in expenses has vastly outpaced growth in revenues — since pre-pandemic levels since last year, and even the year prior — such that margins are ultimately being pushed downward. And hospitals’ median operating margin is still below zero on a cumulative basis,” he declared, referring to 2021 and 2020.

Here’s some context about how dismal this situation is: Even in 2020, a year in which hospitals saw extraordinary losses during the first few months of the pandemic, they still reported operating margins of 2%.

What’s even more disconcerting is that hospitals are underperforming financially pretty much across the board, Swanson said.

Even Kaiser Permanente, one of the country’s largest health systems with an integrated delivery model, reported a $1.5 billion loss for the third quarter of 2022.

Rural hospitals are in even worse shape, but more on that below.

Other hospitals have been forced to shutter service lines to offset these financial losses. Some are also turning to integration and consolidation.

For example, Hermann Area District Hospital in Missouri said last month that it is seeking a “deeper affiliation” with Mercy Health or another provider. This announcement came after the hospital eliminated its home health agency as a cost-cutting measure. In December, the hospital projected a loss of $2 million for 2022.

We can also look at the mega-merger between Atrium Health and Advocate Aurora Health, which was completed last month. The deal, which is designed for cost synergy, creates the fifth-largest nonprofit integrated health system in the U.S.

The merger was finalized one day after North Carolina Attorney General Josh Stein expressed concern about how the deal could impact rural communities. He said that while he didn’t have a legal basis within his office’s limited statutory authority to block the deal, he was worried that it could further restrict access to healthcare in rural and underserved communities.

Stein brings up an extremely valid concern. Rural hospitals’ dismal financial circumstances are becoming more and more worrisome — in fact, about 30% of all rural hospitals are at risk of closing in the near future, according to a recent report from the Center for Healthcare Quality and Payment Reform (CHQPR).

A crucial reason for this is that it is more expensive to deliver healthcare in rural areas — usually because of smaller patient volumes and higher costs for attracting staff. Another factor is that payments rural hospitals receive from commercial health plans isn’t enough to cover the cost of delivering care to patients in rural areas, said Harold Miller, CEO of CHQPR.

“Many people assume that private commercial insurance plans pay more than Medicare and Medicaid. But for small rural hospitals, the exact opposite is true,” he said. “In many cases, Medicare is their best payer. And private health plans actually pay them well below their costs — well below what they pay their larger hospitals. One of the biggest drivers of rural hospital losses is the payments they receive from private health plans.”

In Miller’s view, rural hospitals perform two main functions: taking care of sick people in the hospital and being there for people in case they need to go to the hospital.

To fulfill the latter job, rural hospitals must operate 24/7 emergency rooms. These hospitals get paid when there’s an emergency, but not when there isn’t — even though the hospital is incurring costs by operating and staffing these units.

“Rural hospitals have a physician on duty 24/7 to be available for emergencies. But they don’t get paid for that by most payers. Medicare does pay them for that, but other payers don’t. If the hospital is doing two different things, we should be paying them for both of those things. Hospitals should be paid for what I refer to as ‘standby capacity,’” Miller said.

He bolstered his argument by pointing to these analogies: Do we only pay firefighters when there’s a fire? Do we only pay police officers when there’s a crime?

It’s also important to remember that rural hospitals are in the midst of transitioning to a post-pandemic environment, now without the pandemic-era financial assistance they received from the government, said Brock Slabach, chief operations officer at the National Rural Health Association.

“Rural providers are looking to move into the future without the benefit of those extra payments. And they’re in an environment of really high inflation. It’s over 8%, and for some goods and services in the healthcare sector, that’s going to be over 20% in terms of increased prices. Wages and salaries have also gone up significantly. But patient volumes have maintained below average or average. That all presents a huge challenge,” Slabach said.

Rural providers across the country are dealing with the stressors Slabach described and clamoring for more government help. For example, the Michigan Health & Hospital Association sought more money from the state last month after having to take 1,700 beds offline.

Many rural hospitals can’t escape their fate. From 2010 to 2021, there were 136 rural hospital closures. There were only two closures in 2021, and Slabach said 2022 produced a similarly low number. But these low totals are due to government relief, he explained. Slabach said he’s expecting an increase in rural hospital closures in 2023.

When a rural hospital closes, it means community members have to travel far distances for emergency or inpatient care. Miller pointed out another problem: in many rural communities, the hospital is the only place people can go to get laboratory or imaging work done. The hospital might also be the only source of primary care for the community. Shuttering these hospitals would be a massive blow to rural Americans’ healthcare access.

In the face of these potentially devastating blows to patient access, financial analysts’ outlook is bleak.

Higher inflation and costly labor expenses will continue to have negative effects on hospitals — both rural and urban — in 2023, according to an analysis from Moody’s. Expenses will also continue to increase due to supply chain bottlenecks, the need for more robust cybersecurity investments and longer hospital stays due to higher levels of patient acuity.

All of this doom and gloom begs the question — are any hospitals doing well financially?

The answer is yes, a select few. Let’s look at the three largest for-profit health systems in the nation — Community Health Systems, HCA Healthcare and Tenet Healthcare. As of 2020, these three public health systems accounted for about 8% of hospital beds in the U.S.

These three systems all had positive operating margins for the majority of the pandemic, including most recently in the third quarter of 2022.

Large public health systems have shareholders to report to and stock prices to worry about. Does this mean they’re more likely to deny care to patients who can’t afford it while other hospitals pick up the slack?

Slabach said it’s tough to say.

“Obviously, hospitals try to mitigate their exposure to risk when it comes to taking care of patients. Most hospitals do a really good job of providing services and care to people who don’t have insurance or don’t have the means to pay. But that gets stressed in this current financial environment. So indeed, there may be instances where what you suggested might happen, but it’s not because they want to deny services or deny care. It’s because they have a bigger picture they have to maintain,” Slabach said.

And the big picture involving dollar signs for hospitals looks pretty bleak in 2023.

A number of health systems experienced downgrades to their financial ratings in recent weeks amid ongoing operating losses, declines in investment values and challenging work environments.

Here is a summary of recent ratings since Becker’s last roundup Nov. 15:

The following systems experienced downgrades:

Adventist Health (Roseville, Calif.): Saw a downgraded long-term credit rating on bonds it holds, declining from “A” (negative) to “A-” (stable) by S&P Global Ratings.

The December downgrade follows a 2021 downgrade from Fitch Ratings from “A+” to “A.” That downgrade reflected “a series of one-time events and the lingering deleterious impact from the novel coronavirus” which “resulted in lower than anticipated operating EBITDA margins,” Fitch said. In November, Fitch added to this assessment by downgrading Adventist’s outlook from stable to negative, reflecting “continued negative operational pressure.”

The group, which operates 23 hospitals in California, Hawaii and Oregon, was also assigned an “A” rating by Fitch to 2022 bonds and other outstanding debt.

Catholic Health (Buffalo, N.Y.): The group was downgraded on debt from “B1” to “Caa2” by Moody’s and is in danger of defaulting on its covenants.

The nonprofit health system, which serves residents in Western New York with four acute care hospitals and several other facilities, saw its rating drop in November on approximately $364 million of debt.

Duke University Health System (Durham, N.C.): Downgraded to an “AA-” credit rating by Fitch Ratings.

The December downgrade comes amid concern over Duke’s planned integration of the Private Diagnostic Clinic, a for-profit medical group with more than 1,800 physicians.

The rating, reduced from “AA,” applies both to specific bonds the group holds and to its overall issuer default rating. In addition to the integration of the Private Diagnostic Clinic, Fitch also cited concern over macro issues such as labor and inflationary pressures, which have helped to drag down operating results for the health group.

Main Line Health (Radnor Township, Pa.): – Had its bond rating downgraded to “A1” from “Aa3” by Moody’s.

The December downgrade reflects a multiyear trend of weak operating performance and expectations of tepid progress into 2023, Moody’s said.

In addition to Main Line’s revenue bond rating declining, its outlook has been revised to stable from negative at the lower rating. The hospital group has approximately $651 million in outstanding debt, Moody’s said.

Prime Healthcare (Ontario, Calif.): The group was downgraded on probability of default rating to “B2-PD” from “B1-PD” as well as its ratings of the system’s senior secured notes to “B3” from “B2” by Moody’s.

Moody’s also revised the outlook in November to negative from stable because it projects operating expenses will continue to pressure the 45-hospital system’s profitability in the near term, presenting challenges for “the company’s pace of deleveraging,” according to a Nov. 18 news release.

Westchester County Health Care Corp. and Charity Health System (Valhalla, N.Y): The group was downgraded from “Baa2” to “Baa3” by Moody’s.

The December downgrade for CHS is based on WCHCC’s legal guarantee to pay debt service on CHS’ Series 2015 bonds, if CHS is unable. The outlook for both systems remains negative with WCHCC and CHS having $773 million and $127 million of debt, respectively, at the end of fiscal year 2021, Moody’s said.