Last week Johnson & Johnson followed Merck, Bristol Myers Squibb, and Astellas Pharma by filing a lawsuit against the Biden administration in federal court over the Medicare Drug Price Negotiation Program, established through the 2022 Inflation Reduction Act. PhRMA, the industry trade group, and the US Chamber of Commerce have also filed suits.

The lawsuits claim that the program violates the First and Fifth Amendments by compelling speech, and taking private property for public use without just compensation. The US Chamber of Commerce also filed a motion earlier this month requesting a preliminary injunction.

This flurry of legal activity comes just a month before the Centers for Medicare & Medicaid Services is due to publish its list of the first ten drugs selected for negotiations. The makers of those drugs will then have a month to decide if they will participate in negotiations, risking significant financial penalties if they do not. Any negotiated prices would take effect in 2026.

The Gist:Theability for Medicare to negotiate drug prices is a key pillar of the Biden administration’s healthcare agenda, one the President plans to tout in his upcoming reelection campaign. But the pharmaceutical industry’s legal challenges—multiple, separate suits in different federal courts nationwide—are destined for the Supreme Court if these cases generate conflicting rulings, which is likely. A protracted legal fight will delay or potentially alter the program before it is fully implemented.

With more than two in five American adults considered obese, the potential for GLP-1 agonist drugs like Wegovy, Ozempic, and Mounjaro to revolutionize obesity treatment seems limitless.

In the graphic above, we looked to quantify how much these drugs could potentially change healthcare expenditures and demand. Using Wegovy’s list price of $1.3K per month, a GLP-1 drug prescription for every obese American adult would cost as much as $1.3T annually—30 percent of total US healthcare expenditures.

Analyst projections of GLP-1 drugs forecast revenue to grow by over 5x by 2028, from $3 billion to $16 billion annually. While it’s unlikely that every overweight American will access the drugs, growing use of GLP-1 agonists will likely drive down obesity rates, and downstream care demand could shift in expected and unpredictable ways. Demand for weight-related surgeries, including joint replacements and bariatric surgery, will likely drop. Incidence of chronic diseases like diabetes and cardiovascular disease could also drop, potentially raising life expectancy.

But even if we’re living longer thanks to the new drugs, we’ll still die of something eventually: expect a secondary rise in cancers and Alzheimer’s, as well as surging demand for eldercare. While these effects will take years to materialize, leaders planning for long-term care needs would be wise to consider scenarios where these and other potential “blockbuster” drugs may disrupt demand patterns and spending for a wide range of services.

This month, a panel of expert advisers recommended the Food and Drug Administration (FDA) grant full approval to Leqembi, a drug developed by Eisai and Biogen that targets amyloid plaques in the brain that are linked to the development of Alzheimer’s.

The drug was found to slow cognitive decline in patients by 27 percent over 18 months, though not without some serious side effects, including brain swelling and bleeding. While Leqembi received accelerated FDA approval in January 2023, it is now likely to become the first Alzheimer’s drug that slows the progression of the disease to secure full FDA approval. The Centers for Medicare and Medicaid Services (CMS) recently announced that it intends to cover this new class of Alzheimer’s drugs, as long as prescribing physicians participate in patient registries designed to continue collecting data about the drugs and their efficacy. The FDA is expected to make a final decision on Leqembi by early July.

The Gist: In addition to risks of patient harm, much of the controversy around Leqembi surrounds its $27K list price. Payers, especially Medicare, are worried that it will balloon spending while exposing patients to unaffordable cost-sharing.

With the number of Americans diagnosed annually with Alzheimer’s and other dementias projected to double by 2050, Leqembi has the potential both to help millions and to drive unsustainable spending patterns, and it will be difficult to achieve the former without the latter.

But with full approval likely, a coming frenzy of investor activity to launch memory treatment centers for drug infusion services, capitalizing on the expected huge demand for the drug, seems inevitable.

Billionaire investor Charlie Munger has been vocal in expressing his concerns about U.S. healthcare, stating that it is “shot through with rampant waste” and has become “immoral.”

Munger says there are substantial problems that need to be addressed, including the presence of unnecessary costs and inefficiencies that plague the medical field.

Drawing a vivid analogy at a Daily Journal Annual Meeting, Munger compared the experience of a dying old person in many American hospitals to that of a carcass on the plains of Africa. He painted a bleak picture, describing how vultures, jackals, hyenas and other scavengers swarm around the helpless creature.

In an attempt to address these issues, Berkshire Hathaway, Amazon.com Inc., and JPMorgan Chase joined forces to establish Haven Healthcare a venture that despite their combined efforts failed to achieve its objectives.

Some startups have seen success where they failed. iRemedy, for example, is a startup using artificial intelligence (AI) technology, that offers a solution to the healthcare system’s challenges through its large procurement marketplace. Its platform streamlines the supply chain, enabling faster and more affordable access to lifesaving supplies for doctors, hospitals and healthcare providers.

Munger, vice chairman of Berkshire Hathaway Inc., criticized the high costs and inefficiencies in medical care as both expensive and wrong. In a CNBC interview, he went on to claim that some medical providers artificially prolong death to increase their profits.

With over 35 years of experience as board chairman of Good Samaritan Hospital in Los Angeles, Munger expressed his belief that certain healthcare practices are absurd.

“A lot of the medical care we do deliver is wrong — so expensive and wrong. It’s ridiculous,” he said in a “Squawk Box” interview.

In 2018, Munger predicted that when Democrats gain control of all three branches of government, there will be a push for a single-payer healthcare system. He highlighted the need for a complete change forced by the government because of the severity of the issues in the current system. He suggested that a universal healthcare system with an opt-out option would be a reasonable solution.

Warren Buffett, Munger’s longtime investing partner, shares similar concerns regarding healthcare spending, referring to it as a “tapeworm on the economic system.” Buffett believes the private sector can make substantial contributions to cost-reduction efforts.

A recent investigation conducted by Kaiser Health News-NPR shed light on the alarming reality of medical debt in the United States. The study reveals that over 100 million Americans are burdened with medical debt, placing a significant financial strain on their lives. Further analysis of the data reveals that approximately one-fourth of American adults carrying this debt owe more than $5,000.

What makes this issue even more concerning is the fact that it is not primarily driven by a lack of insurance coverage. Contrary to popular belief, the majority of people grappling with medical debt are not uninsured. Instead, it is the problem of being underinsured that is prevalent.

Many people have health insurance plans that do not offer sufficient coverage, leaving them vulnerable to high out-of-pocket expenses and accumulating medical debt.

A majority of Americans with health insurance said they had encountered obstacles to coverage, including denied medical care, higher bills and a dearth of doctors in their plans, according to a new survey from KFF, a nonprofit health research group. As a result, some people delayed or skipped treatment.

Those who were most likely to need medical care — people who described themselves as in fair or poor health — reported more trouble; three-fourths of those receiving mental health treatment experienced problems.

“The consequences of care delayed and missed altogether because of the sheer complexity of the system are significant, especially for people who are sick,” said Drew Altman, the CEO of KFF, formerly known as the Kaiser Family Foundation.

The survey also underscored the persistent problem of affordability as people struggled to pay their share of health care costs. About 40% of those surveyed said they had delayed or gone without care in the last year because of the expense. People in fair or poor health were more than twice as likely to report problems with paying medical bills than those in better health, and Black adults were more likely than white adults to indicate they had trouble.

Why It Matters: Delayed care can endanger health.

Nearly half of those who encountered a problem with their insurance said they could not satisfactorily resolve it. Some could not obtain the care they had sought, while others said they paid more than expected. Among the nearly 60% who reported difficulty with their insurance coverage, 15% said their health had declined.

“This survey shows it’s not enough to just get a card in your pocket — the insurance has to work or it’s not exactly coverage,” said Karen Pollitz, the co-director for KFF’s patient and consumer protections program.

People have a hard time understanding their coverage and benefits, with 30% or more reporting difficulty figuring out what they will be required to pay for care or what exactly their insurance will cover.

“Insurances are way more complicated than they should be,” said Amanda Parente, a 19-year-old college student in Nashville, Tennessee, who is covered under her mother’s employer plan. She was surprised to find that her out-of-pocket costs spiked recently when she sought treatment for strep throat. While she realized her copayments would be higher, “I guess we didn’t know how drastic it was going to be,” she said.

Background: Insurance coverage is confusing to everyone.

Navigating the intricacies of coverage and benefits were similar regardless of what kind of insurance people had. At least half of those surveyed with private coverage, through an employer, those with an “Obamacare” plan, or a government program like Medicare or Medicaid, said they experienced difficulties.

People might be unhappy with their coverage because they were already concerned about higher inflation and potential layoffs, said Christopher Lis, the managing director of global health care intelligence at J.D. Power, which found that consumer satisfaction with insurers had declined in a recent study. “We’ve got economic conditions that set the stage for concern around coverage and benefits,” he said.

Insurers say people generally report being happy with their plan, and 81% of those surveyed by KFF gave their insurance high ratings. “Health insurance providers are committed to improving access, affordability and convenience for all Americans and will continue to find innovative solutions to work toward this common goal,” said David Allen, a spokesperson for AHIP, a trade group that represents insurers.

What’s Next: How to haggle with insurers or appeal?

Also striking among the survey’s findings was how unaware people were about pursuing appeals of denied coverage and how to go about doing so.

“Most people don’t know who to call,” Pollitz said. Sixty percent of insured adults surveyed did not know they had a legal right to appeal, and about three-fourths said they did not know which government agency to contact for help, particularly respondents with private insurance.

State insurance regulators oversee fully insured policies sold to individuals and small businesses, and the federal Department of Labor has jurisdiction over employer-sponsored insurance.

Many of the problems people have with their insurance could be solved by enforcing existing rules, like federal regulations requiring private insurers to issue understandable explanations of benefits and to maintain accurate, current lists of doctors and hospitals within their networks.

On April 1st, Medicaid’s pandemic-era continuous enrollment policy began to sunset, kicking off a 14-month window for states to reassess their Medicaid rolls. In this week’s graphic, we highlight new Congressional Budget Office projections showing the impact of Medicaid redeterminations on insurance coverage rates over the next decade for the under-65 population.

The Medicaid and Children’s Health Insurance Program (CHIP) coverage rate is expected to drop from 31 percent of all Americans under 65 in 2023, to 27 percent in 2024.

Meanwhile, after reaching an all-time low in 2023,the under-65 uninsured rate is projected to surpass nine percent in 2024 and climb to over 10 percent by 2033.

While over 15M Americans are expected to lose Medicaid coverage during redeterminations, a majority of those disenrolled will gain health insurance either through an employer-sponsored or non-group plan.

But over 6M people, nearly 40 percent of those losing Medicaid coverage, are projected to become uninsured, erasing nearly half the progress the country has made since 2019 at lowering the uninsured rate.

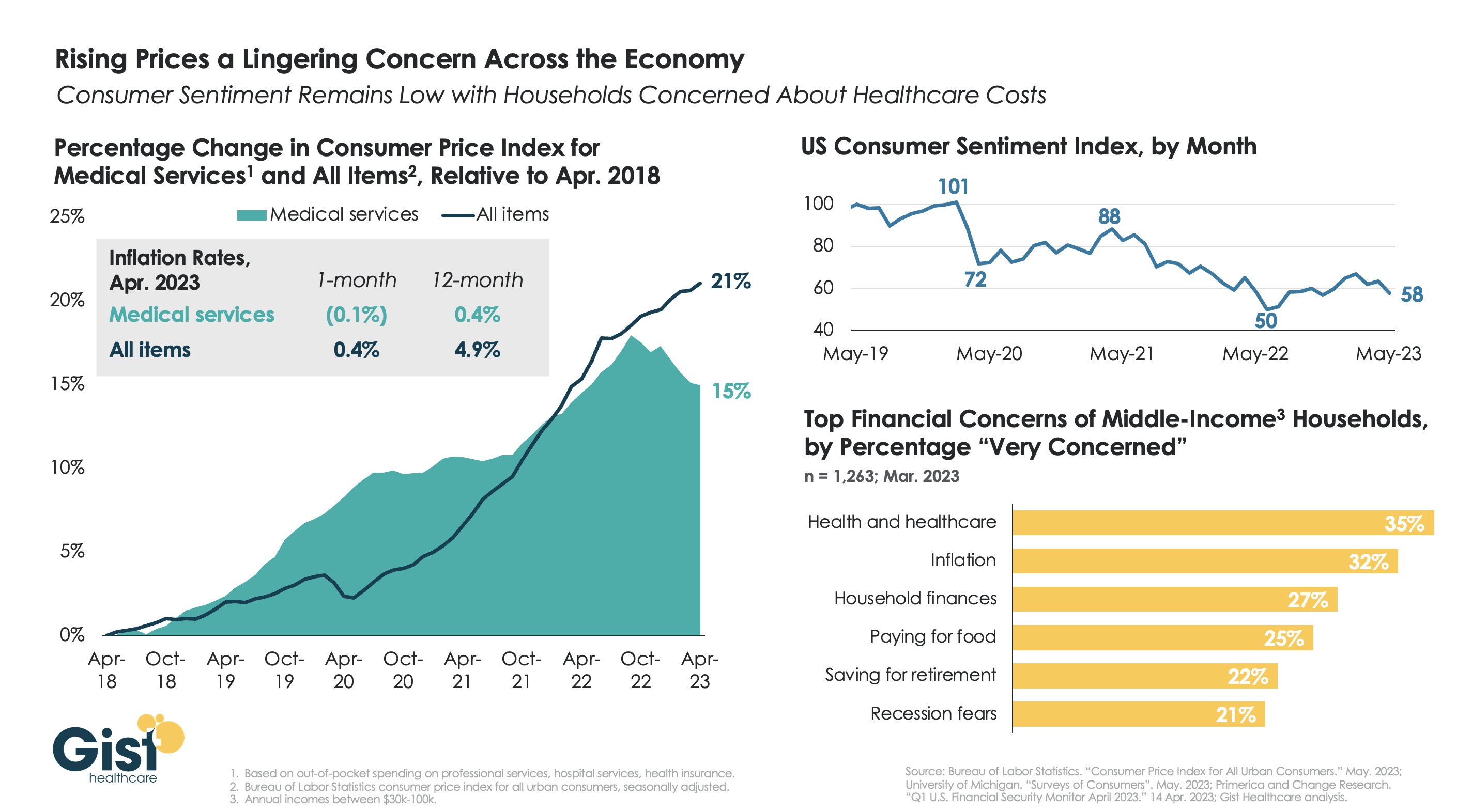

With the latest Bureau of Labor Statistics’ Consumer Price Index (CPI) report revealing the 12-month inflation rate in April 2023 rose again after hitting a recent low in March, we’re using this week’s graphic to show the cumulative picture on price and consumer sentiment changes across the last five years.

Since 2018, the CPI for all goods has risen 21 percent, while medical services have become 15 percent more expensive, in terms of consumer out-of-pocket spending. Leading into COVID, medical service prices were rising faster than general inflation, but the cumulative rise in the price of all goods caught up to medical services in early 2022.

Since December of last year, the price of medical services has actually experienced some deflation, partly due to a lagging decline in insurer profits. Reports of easing inflation had elicited a slight rebound in consumer sentiment, but last month’s 9 percent drop, the largest since June 2022, suggests this confidence is easily shaken.

Unfortunately for healthcare providers, according to a recent poll, fewer consumers worrying about elevated grocery and gas prices means that healthcare has reclaimed the top spot for household financial concerns.

A lack of data about Medicare Advantage plans means there are several unanswered questions about the program, according to an analysis from Kaiser Family Foundation.

The analysis, published April 25, breaks down the kinds of Medicare Advantage data not publicly available. Some missing data is not collected from insurers by CMS, and some data is collected by the agency but not available to the public.

Here are five questions researchers can’t answer without more data, according to Kaiser Family Foundation:

Insurers are not required to report how many enrollees use supplemental benefits and if members incur out-of-pocket costs with their supplemental benefits. Without this data, researchers can’t answer what share of enrollees use their supplemental benefits, how much members spend out of pocket for supplemental benefits, and if these benefits are working to achieve better health outcomes.

CMS does not require Medicare Advantage plans to report prior authorizations by type of service. Without more granular data, researchers can’t determine which services have the highest rates of denial and if prior authorization rates vary across insurers and plans.

Insurers are also not required to report the reasons for prior authorization denials to CMS. This leaves unanswered questions, including what is the most common reason for denials and if rates of denials vary across demographics.

Medicare Advantage plans do not report complete data on denied claims for services already provided. Without this data, researchers cannot determine how often payers deny claims for Medicare-covered services and reasons why these claims are denied.

CMS does not publish the names of employers or unions that receive Medicare funds to provide Medicare Advantage plans to retired employees. Without more data, researchers can’t tell which industries use Medicare Advantage most often and how rebates vary across employers.

On Wednesday, Indianapolis, IN-based pharmaceutical giant Eli Lilly announced that it will cut its list price for both Humalog and Humulin, its two most commonly prescribed insulin products, by 70 percent. While these changes will go into effect later this year, the company is also immediately expanding its Insulin Value Program, available at participating pharmacies for the commercially insured and upon program enrollment for the uninsured, to match Medicare Part D’s $35 per month out-of-pocket insulin cap. Eli Lilly shared that 30 percent of the US’s 8M insulin users rely on its products, though the company is only cutting prices for its older insulin products.

The Gist: Nearly 30 percent of uninsured and 20 percent of commercially insured insulin users in the US report having to ration their doses due to cost concerns.While it still won’t be providing its insulin for free, as some have demanded, Lilly’s move should help the company gain market share, in addition to generating some good PR—and it’s expected that other large insulin manufacturers will be pressured to follow suit.

But even if a $35 out-of-pocket cap was adopted nationally, Americans would still be paying three times more for their insulin than people in comparable countries.