The CBO projects that 10.9 million more people would be uninsured under President Trump’s sweeping budget bill — mostly from the way it would overhaul Medicaid, including new work requirements.

Why it matters:

That would amount to major coverage losses that are certain to fuel Democratic attacks on the measure, and put new pressure on vulnerable Republicans heading into the midterm election cycle, Peter Sullivan wrote first on Pro.

By the numbers:

The CBO on Wednesday projected that 7.8 million more people would be uninsured due to the Medicaid changes, with the rest likely due to Affordable Care Act marketplace changes, including new barriers to signing up that are aimed at fighting fraud.

The estimate includes 1.4 million people without verified citizenship “or satisfactory immigration status,” a reference to undocumented immigrants that some states opt to cover with non-federal dollars in their Medicaid programs.

The CBO was responding to a request from congressional Democrats about the number of uninsured people stemming from the package the House passed last month.

Republicans say the changes would ensure that Medicaid is targeted at beneficiaries deserving of coverage, and that taxpayer money should not be spent on healthy adults who are choosing not to work.

Opponents say people who are working will be caught up in the red tape from the changes and could still lose coverage.

The CBO also said another 5.1 million would become uninsured if Congress opts to let Affordable Care Act premium tax credit subsidies expire next year.

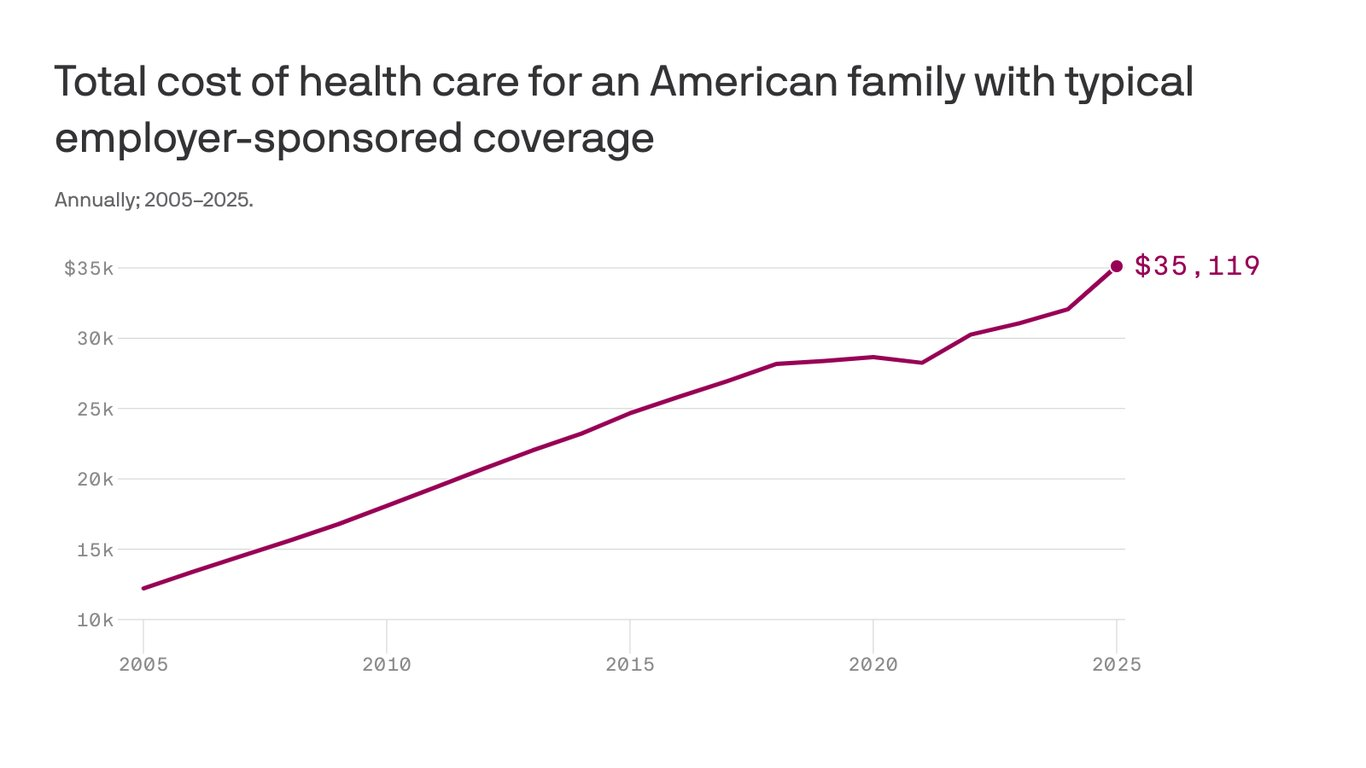

The cost to cover a family of four through workplace insurance now exceeds $35,000, nearly triple what it cost 20 years ago as annual growth in health costs have far outpaced wages.

The big picture:

Growing pharmacy and outpatient facility costs drove most of the increase, which includes employee and employer shares,according to the 2025 Milliman Medical Index.

Employers have been wary of passing health cost hikes to workers in a tight labor market, but the rising demand for costly care may force a reckoning.

State of play:

The $35,119 annual cost to cover a hypothetical family of four this year factors in drug costs, inpatient and outpatient care, and professional services, along with an “other” category that includes home health, ambulance transport, medical equipment and prosthetics.

A year of health care cost a family of four $12,214 in 2005, the year Milliman launched the index. The 20-year cumulative gain of 188% outpaced the 84% growth in wages over the same time.

Health costs have increased about 6% per year on average over the past two decades, according to Milliman, compared with an average inflation rate of 2.5% over that time.

Between the lines:

Employers in 2025 still shoulder 58% of employee health care costs, but their share has shrunk since 2005, when it was more than 60%.

Reality check:

Health care costs vary significantly by age, geography and pharmacy rebate arrangements.

Milliman calculates family cost based on a family with a 47-year-old male, 37-year-old female, and children ages 4 and under 1.

This was a “mathematically average” family in 2005, and Milliman continues to use that formula to keep data comparable year-to-year.

The firm has an online tool that allows readers to input other family configurations to see their estimated 2025 health care costs.

The analysis is based on Milliman’s proprietary research tools and analyzes commercialclaims data. The family cost figure reflects nationwide average negotiated provider fees and average PPO benefit levels.

The GOP’s reconciliation bill, the “One Big Beautiful Bill Act” (yes, it’s actually called that), is a cruel exercise in slashing benefits for the poor, the elderly, and the sick to free up fiscal space for yet more tax cuts for the rich. Compounding the harm, these benefit cuts are nowhere near enough to pay for the bill’s tax cuts for the wealthy.

Central to this effort are massive cuts to Medicaid and the Affordable Care Act (ACA) marketplaces that, as I argued in my recent paper, will exacerbate our ongoing medical debt crisis.

The GOP reconciliation package that the Senate and House recently agreed to instructed the House Energy and Commerce Committee, which oversees spending on health-care programs including Medicaid and the Children’s Health Insurance Program (CHIP), to identify up to $880 billion in savings over the next 10 years.

Under the rules of the budget reconciliation process, Republicans need to offset any tax cuts they wish to make permanent with an equal dollar value in cuts to spending so as to remain deficit neutral. Trillions of dollars in tax cuts for the wealthier therefore necessitate trillions of dollars in cuts to spending that fall mostly on the social safety net.

Although they did not quite reach that target, the committee still returned a proposed package of deep cuts and changes to Medicaid and to the ACA marketplaces that would reduce federal medical spending by at least $715 billion over 10 years, with about $625 billion in reduced Medicaid spending.1

After public backlash, Republicans seem to have backed off some of their most radical plans for Medicaid (at least for now—one of the challenges of taking health care from people is that it’s terrible politics, so the precise details of the cuts are likely to remain a moving target until the bill passes).

But all options they are close to settling on would still do horrific damage to the well-being of working-class families.

This includes requiring all Medicaid recipients above the federal poverty line to “cost share” by paying (larger) premiums and copayments,2 cutting federal matching to states that provide public health insurance coverage to undocumented and perhaps documented immigrants (on their own dime), and imposing harsh work requirements on “able-bodied adults without dependent children.” This latter provision will cut federal Medicaid spending by roughly $300 billion over 10 years even though the vast majority (92 percent) of nondisabled, non-elderly adult Medicaid recipients are already working, studying full time, or serving as caregivers. This is because work requirements create burdensome reporting requirements to demonstrate compliance that will cause Medicaid recipients who are already employed to lose their insurance as well—blaming the victim for losing their health care, in essence.

The Congressional Budget Office estimates that the reconciliation bill would decrease Medicaid enrollment by 10.3 million in 2034(the end of the reconciliation bill budget window).

According to this same analysis, most of these individuals would not obtain other insurance (e.g., through an employer) and would thus become uninsured.

When combined with the bill’s changes to the ACA marketplace and the expiration of the enhanced premium tax credits—a wildly successful policy that was introduced as part of the American Rescue Plan Act (ARPA) and one that Republicans have shown no inclination to extend—this would result in an additional 13.7 million uninsured individuals in 2034, a 30 percent increase, according to KFF estimates.

Republicans seem hell-bent on undoing the remarkable progress made in the 15 years since the passage of the ACA in reducing the non-elderly uninsured rate from 17.8 percent in 2010 to roughly 9.5 percent today (plus ça change).

But we’ve seen less focus on how this will affect the problem of underinsurance.

Republicans’ Medicaid cost-sharing requirements, the changes they have proposed to the ACA marketplaces, and their determination to let the ARPA premium tax credit enhancements expire will also worsen the problem of underinsurance, an area where we have made considerably less progress.

Taken together, this will worsen the ongoing medical crisis because medical debt is driven by uninsurance and underinsurance.

Medical debt is, unlike in most other countries, and despite the successes of the ACA, a major problem in the United States. KFF found that 20 million adults (almost 1 in 12) owed “significant” medical debt to a health-care provider.3 This number rises when we consider a more expansive definition of medical debt including credit card balances and bank loans used to pay medical providers. Under that definition, an estimated 41 percent of American adults (~107 million people) carried some form of medical debt and 24 percent of American adults (~62 million people) had medical debt that was past due or that they were unable to pay. Among those with medical debt using this more expansive definition, nearly half (44 percent) reported owing at least $2,500, and about one in eight (12 percent) said they owe $10,000 or more. The poor, the sick, the middle-aged, and Black and Hispanic individuals disproportionately bear the brunt of this problem.

The crisis of medical debt and underinsurance is so widely recognized by Americans that a state attorney general candidate can go viral just by talking about the reality of a GoFundMe health-care system millions of Americans face.

The consequences of all this debt are dire—and reflect a health-care system that heals people physically but leaves many permanently scared financially. In 2022, medical debt (using the narrow definition) made up an estimated 58 percent of all debts that had gone to collections, and 62 percent of bankruptcies were attributed in part to medical debt. Medical debt also damages credit scores, leading to a wide variety of negative impacts on financial well-being that can follow families for years.

A poor credit score means that families may be unable to obtain a mortgage or a car loan or may end up paying much higher interest rates.

Credit scores are commonly used by landlords to screen tenants and by employers as part of a background check during the hiring process. Even for those who manage to maintain their credit after taking on medical debt, there are real costs. For those with limited income and assets, debt service may displace spending on food, clothing, and other essentials, leading to material hardship. It can make savings impossible and limit economic mobility.

Medical debt is a problem largely generated by poor policy decisions including, as I argue in my paper, prioritizing and incentivizing health insurance coverage through the private market rather than through Medicaid and Medicare, which offer comprehensive coverage more cheaply. The problem would rapidly disappear if we could extend comprehensive health insurance coverage to the millions of uninsured and underinsured people who live with the constant risk that a sudden medical event could ruin their finances and constrain their futures.

But rather than fix the problem, the GOP plans to throw millions off Medicaid and saddle those who remain with higher costs and more limited coverage. The results of these poor policy decisions will be more sickness, more debt, and higher costs for everyone in exchange for on-paper “savings.” And all this in service of tax cuts for the wealthy they haven’t even bothered to justify.

If you ask Eleanor

“If the old people cannot afford their medical care under their own Social Security allowances, then the burden is going to fall on their children who are in their earning years. This will mean that just at the time when these children who may be having young children of their own and needing medical care, a young couple will also have to consider shouldering the burden for parents as well. This is not fair, and leads to both the children and the older people not getting full coverage, since both will try to shave a little off their needs in order not to make the burden impossible to carry.”

In chaos theory, there’s a concept known as the butterfly effect—the idea that a seemingly small action, occurring at just the right moment, can trigger ripple effects that grow across time and space. A butterfly flaps its wings in Brazil, the saying goes, and a tornado forms weeks later in Texas.

Presidential decisions can carry the same weight, especially those made in the first 100 days of a new administration. Time and again, these early choices unleash far-reaching consequences that reshape a nation.

As Donald Trump wraps up the opening stretch of his second term, his healthcare-focused executive actions underscore the consequentiality of this early window. And when compared with Barack Obama’s approach in 2009 (the last time a president pursued major healthcare reforms right out of the gate), the contrast becomes even more striking.

Two presidents. Two defining moments. And one fundamental question that both men had to answer in the first 100 days: Where should healthcare reform begin — by expanding coverage, improving quality or cutting costs?

Crisis, Control And A Key Healthcare Choice

The idea that a president’s first 100 days matter dates back to Franklin D. Roosevelt. In 1933, during the depths of the Great Depression, FDR passed a wave of New Deal reforms that redefined the role of government in American life.

Ever since, the opening months of a new presidency have served as both proving ground and preview. They reveal how a president intends to govern and what he values most.

For both presidents Obama and Trump, their answer to the healthcare question — where to begin? — would shape what followed. Obama chose to expand coverage. Trump has chosen to cut costs. Those decisions set them on opposing paths. And with every subsequent policy decision, the gap between their contrasting approaches only grows.

’09 Obama: Health Coverage And Congressional Action

In the quiet calculus of early governance, President Obama concluded that without health insurance coverage, access to high-quality medical care would remain out of reach for tens of millions of Americans.

Confronting a system that left 60 million uninsured, he believed that expanding access to coverage was a vital first step — not only to improve individual health outcomes, but to create a healthier nation that ultimately would require less medical care (and spending) overall.

That belief was grounded in lived experience: his mother’s battle with cancer and the insurance disputes that followed, as well as his years as a community organizer working with families who couldn’t afford medical care.

He also understood that only Congressional legislation — rather than executive action — would make those gains durable. So, in his first 100 days, he pursued a strategy grounded in consensus-building. He convened healthcare stakeholders, hosted public healthcare summits, expanded the Children’s Health Insurance Program (CHIP) and proposed a federal budget that included a $634 billion “down payment” on healthcare reform.

’25 Trump: Cost Cutting And Executive Control

Donald Trump didn’t ease into his second term. He charged in, pen in hand. His priorities for the country were clear: cut taxes, impose tariffs and reduce federal spending.

For Trump, speed was of the essence. So, he bypassed Congress in favor of executive orders, downsizing healthcare agencies and dismantling regulatory oversight wherever possible.

At the center of Trump’s domestic agenda is an ambitious income tax overhaul, dubbed the “big beautiful bill.” But passing it will require support from fiscal conservatives in his own party. To offset the steep drop in tax revenue, Trump has signaled a willingness to slash federal spending, starting with healthcare programs.

What Comes Next: Mapping Health Policy Consequences

Presidents make thousands of decisions over the course of a four-year term, but those made in the first few months typically matter most. Both Obama and Trump had to decide whether to prioritize expanding coverage or cutting costs, and that choice would shape the steps that follow.

For Obama, the consequences of his choice were sweeping. His early focus on increasing health insurance coverage laid the foundation for the Affordable Care Act, the most ambitious healthcare reform since Medicare and Medicaid in the 1960s. The ACA provided affordable insurance to more than 30 million Americans, offered subsidies to low- and middle-income families, cut the uninsured rate in half and guaranteed protections for those with preexisting conditions. The law survived political opposition, legal challenges and subsequent presidencies.

Trump’s early decisions are reshaping healthcare, too, but in ways that reflect a very different set of priorities and a sharply contrasting vision for the federal government’s role.

1. Cost-Driven Actions: Reducing Government Healthcare Spending

Guided by a business-oriented focus on cost containment, Trump has sought to reduce the federal government’s role in healthcare through sweeping budget and staffing changes. Among the most significant:

Agency layoffs: The Department of Health and Human Services has initiated mass layoffs across the CDC, NIH and FDA, reducing staff capacity by 20,000 and cutting critical programs, including HIV research grants and initiatives targeting autism, chronic disease, teen pregnancy and substance abuse.

ACA support rollbacks: The administration slashed funding for ACA navigators and rescinded extended enrollment periods, making it more difficult for individuals (especially low-income Americans) to obtain coverage.

Planned Parenthood and family planning cuts: Freezing Title X funds has reduced access to reproductive healthcare in multiple states.

Medicaid at risk: A proposed $880 billion reduction over 10 years could eliminate expanded Medicaid coverage in many states. Additional moves (like work requirements or application hurdles) would likely reduce enrollment further.

2. Cultural And Executive Power Moves: Redefining Government’s Role In Health

While cutting costs has been the central goal, many of Trump’s actions reflect a broader ideological stance. He’s using executive authority to reshape the values, norms and institutions that have defined American healthcare. These include:

Withdrawal from the World Health Organization (WHO): The administration formally ended U.S. participation, citing concerns about funding and governance.

Restructuring USAID’s health portfolio: Multiple contracts and programs related to maternal health, infectious disease prevention and international public health have been ended or scaled back.

Policy changes on federal language and research topics: Executive directives have modified how agencies are allowed to address topics related to gender and sexuality, leading to the removal of LGBTQ+ content from health resources and websites.

Reorganization of DEI programs: Diversity, equity and inclusion initiatives have been rolled back or eliminated across several federal departments.

The Likely Consequences Of Trump’s First 100 Days

President Trump’s early actions reveal two defining trends: cutting government healthcare spending and reshaping federal priorities through executive authority. Both are already changing how care is accessed, funded and delivered. And both are likely to produce lasting consequences.

The most immediate impact will come from efforts to reduce healthcare spending. Cuts to Medicaid, ACA enrollment support and family planning programs are expected to lower insurance enrollment, particularly among low-income families, young adults and people with chronic illness.

As coverage declines, care becomes harder to access and more expensive when it’s needed. The results: delayed diagnoses, avoidable complications and rising levels of uncompensated care.

His second set of actions — including reduced investment in federal science agencies — will slow drug development and weaken the infrastructure needed to respond to future public health threats.

Meanwhile, a more constrained and domestically focused healthcare agenda is likely to diminish trust in federal health agencies, limit access to culturally competent care and produce a loss of global leadership in health innovation.

The U.S. Constitution gives presidents broad power to chart the nation’s course. And the decisions made in their first 100 days shape the trajectory of an entire presidency.

One president decided to prioritize coverage, while a second chose cost-cutting. And like the flap of a butterfly’s wings, these early actions generate ripples — expanding in size over time and radically altering American healthcare, for better or worse.

The massive Republicanbudget bill working its way through Congress has mostly drawn attention for its tax cuts and Medicaid changes.

But it would also take steps to significantly roll back coverage under the Affordable Care Act, with echoes of the 2017 repeal-replace debate.

Why it matters:

The bill that passed the House before Memorial Day includes an overhaul of ACA marketplaces that would result in coverage losses for millions of Americans and savings to help cover the cost of extending President Trump’s tax cuts, Peter Sullivan wrote first on Pro.

It comes after a growth spurt that saw ACA marketplace enrollment reach new highs, with more than 24 million people enrolling for 2025, according to KFF. The House’s changes would likely reverse that trend, unless the Senate goes in a different direction when it picks up the bill next week.

Driving the news:

The changes are not as sweeping as the 2017 effort at repealing the law, but many of them erect barriers to enrollment that supporters say are aimed at fighting fraud.

Brian Blase, president of Paragon Health Institute and a health official in Trump’s first administration, said Republicans are focusing on rolling back Biden-era expansions “that have led to massive fraud and inefficiency.”

The Congressional Budget Office estimates the ACA marketplace-related provisions would lead to about 3 million more people becoming uninsured.

Cynthia Cox, a vice president at KFF, said while the changes “sound very technical” in nature, taken together “the implications are that it will be much harder for people to sign up for ACA marketplace plans.”

What’s inside:

The bill would end automatic reenrollment in ACA plans for people getting subsidies, instead requiring them to proactively reenroll and resubmit information about their incomes for verification.

It would also prevent enrollees from provisionally receiving ACA subsidies in instances where extra eligibility checks are needed, which can take months.

If people wound up making more income than they had estimated for a given year, the bill removes the cap on the amount of ACA subsidies they would have to repay to the government.

Some legal immigrants would also be cut off from ACA subsidies, including people granted asylum and those in their five-year waiting period to be eligible for Medicaid.

What they’re saying:

In a letter to Congress, patient groups pointed to the various barriers as “unprecedented and onerous requirements to access health coverage” that would have “a devastating impact on people’s ability to access and afford private insurance coverage.”

The letter was signed by groups including the American Cancer Society Cancer Action Network, American Diabetes Association and American Lung Association.

Between the lines:

A last-minute addition to the bill would also make a technical but important change that increases government payments to insurers in ACA marketplaces.

That would have the effect of reducing the subsidies that help people afford premiums and save the government money, by reducing the benchmark silver premiums that are used to set the subsidy amounts.

Democrats are concerned that if Congress also allows enhanced ACA subsidies to expire at the end of this year, the combined effect would be even higher premium increases for enrollees next year.

Insurers that already are planning their premium rates for next year say the Republican funding changesare throwing uncertainty into the mix.

“Disruption in the individual market could also result in much higher premiums,” the trade group AHIP warned in a statement on the bill.

The big picture:

Blase said changes like ending automatic reenrollment are needed to increase checks that ensure people are not claiming higher subsidies than they’re entitled to.

Cox said another way to address fraud would be to target shady insurance brokers, rather than enrollees themselves. She estimated that marketplace enrollment could fall by roughly one-third from all the changes together.

“The justification for many of these provisions is to address fraud,” she said. “The question is, how many people who are legitimately signed up are going to get lost in that process?”

In what’s becoming an all-too-familiar pattern, CVS Health announced it will pull Aetna out of the Affordable Care Act (ACA) marketplace in 2026, leaving about a million people across 17 states searching for new health coverage — and in some cases, fighting to afford any at all.

This marks yet another retreat by a major for-profit insurer from a program designed to provide affordable health coverage to Americans who don’t get it through work. CVS made the announcement while simultaneously celebrating a 60% increase in quarterly profit and revealing a new deal to boost sales of the pricey weight-loss drug Wegovy through its pharmacy and pharmacy benefit manager (PBM) arms.

Let me repeat that: Aetna is exiting the ACA because it claims it can’t make enough money on people enrolled in those plans, on the same day its parent company posted nearly $1.8 billion in profits in just the first three months of this year.

This is the same company, by the way, that dumped hundreds of thousands of seniors and disabled people at the end of 2024 because some of them were using more medical care than Wall Street found acceptable. If this doesn’t tell you everything you need to know about who the health insurance industry is really working for, I don’t know what will.

From “Commitment” to Abandonment

Aetna first bailed on the ACA exchanges in 2018, then re-entered in 2022 when insurers could see more clearly how they could make significant profits on that book of business. Now, after just a few years of moderate participation, it’s heading for the exits again. CVS Health executives blamed “regulatory uncertainty” and “highly variable economic factors,” according to a statement to The Columbus Dispatch.

But make no mistake—this was a cold business calculation. Uncertainties and economic variabilities are constants in the insurance game.

CVS’ CEO David Joyner told investors:

“We are disappointed by the continued underperformance from our individual exchange products … this is not a decision we made lightly.”

That’s corporate-speak for “our Wall Street friends weren’t impressed.”

Aetna’s ACA exchange business, covering roughly 1 million people, is just a sliver of CVS’ overall medical membership of 27.1 million. But even though the profits weren’t massive, the people depending on this coverage — many of them self-employed, working multiple part-time jobs, or recently uninsured — will now be thrown into chaos.

And it’s happening at a time when health insurance for many Americans hangs by a thread. Unless Congress acts in the coming months, the ACA’s enhanced tax subsidies—first implemented under the American Rescue Plan—are set to expire at the end of this year.Without them, premiums could spike by 50% to 100% depending on income and geography.

The Congressional Budget Office projects that the lapse in subsidies could leave 3.8 million more Americans uninsured— and now, 1 million more will be forced to find new plans as CVS/Aetna walks away.

Same Song: Prioritizing Profit, Not Patients

Let’s be clear about what CVS is doing here: It’s ditching an essential safety net for millions in order to chase higher profits elsewhere—most notably, in the exploding market for GLP-1 drugs like Wegovy. On the same day it abandoned the ACA, CVS announced a new deal to give Wegovy preferred placement on its PBM formulary, displacing Eli Lilly’s Zepbound. This will help CVS dominate the obesity drug market—and rake in profits through its Caremark PBM and nearly 9,000 retail pharmacies.

It’s a powerful example of vertical integration in action.

CVS owns the insurer (Aetna), the PBM (Caremark), and the pharmacy (CVS retail stores). When it walks away from lower-margin business like ACA plans and doubles down on high-dollar drug deals, we see its true priorities: selling expensive drugs, saddling individuals, families and employers with the costs, and keeping Wall Street happy.

Even worse, the decision is taking place against a troubling political backdrop. The Trump administration has already taken steps to undermine ACA infrastructure and expressed skepticism toward core public health programs. Cuts to navigator funding, changes to vaccine guidelines, and looming uncertainty around tax credits are all part of a slow-motion sabotage of the ACA. This is not to say that the ACA doesn’t have its flaws that need to be addressed.

But instead of penalizing hard-working Americans and their families, lawmakers and the Trump administration should focus instead on lowering the ridiculously high out-of-pocket maximum that the ACA established (and that keeps going up every year) and fixing the medical loss ratio provision that has fueled the vertical integration in the insurance industry.

Whether they owe providers directly or carry the financial burden in long-term loans and credit card bills, an estimated 41 percent of Americans hold some form of medical debt.

“Medical debt is not inevitable. Rather, it is the product of decades of dysfunctional health-care policy, a market-oriented insurance system, and a patchwork of safety net programs with notable gaps,” writes Stephen Nuñez, Roosevelt’s director of stratification economics, in a new brief.

Health-care policy permeates every stage of American life—whether it’s students applying for Medicaid, workers struggling to find insurance coverage between jobs, or the elderly signing up for Medicare—and the scale of the resulting debt crisis is massive. But these problems are also solvable.

“Biden administration efforts over the past several years have shown that our health-care system can be strengthened to extend insurance to millions more working-class people and help millions more upgrade their insurance coverage with better plans, at incrementally small costs,” Nuñez explains. “But the Trump administration is now poised not only to undo these steps but to enact savage cuts to federal health-care spending that will supercharge the medical debt crisis and together leave millions of people, disproportionately Black and Hispanic, uninsured and underinsured.”

Ultimately, a crisis created by policy choices must also be solved by policy choices:

In 2025, Congress should protect Medicaid and the American Rescue Plan tax credits.

In upcoming state legislative sessions, the 10 states withholding federal Medicaid funds from their residents should expand coverage as stipulated in the Affordable Care Act.

In the coming years, the federal government should implement a comprehensive plan to close the gaps in the American health insurance system.

Millions of people could lose coverage under potential policy changes to Medicaid under consideration by Republicans in Congress, according to a letter sent to lawmakers this week from the Congressional Budget Office.

One option, reducing the federal government’s share of costs for enrollees covered under Medicaid expansion, would reduce the federal deficit by $710 billion over the next decade. But in 2034, 5.5 million people would be removed from the safety-net program, with 2.4 million of these enrollees becoming uninsured, according to the CBO.

Another potential policy, placing a per-enrollee cap on federal spending, would remove 5.8 million people from Medicaid. Nearly 3 million of those people would lose coverage entirely. The policy would reduce the deficit by $682 billion, the analysis found.

Dive Insight:

Debates surrounding potential cuts to Medicaid — and their implications for patients and providers — have been heating up in Congress for weeks.

Last month, lawmakers approved a budget resolution that called for the House Energy and Commerce Committee, which oversees Medicare and Medicaid, to find $880 billion in savings. That budget goal is likely impossible to hit without targeting major healthcare programs under the committee’s purview, according to an earlier analysis published in March by the CBO.

The committee is expected to meet next week to mark up its portion of the reconciliation package and hash out legislation.

However, cutting Medicaid is a politically contentious move for Republican lawmakers. Some legislators have pushed back on potential cuts, and others have argued they’ll preserve Medicaid for the most vulnerable by targeting fraud, waste and abuse in the safety-net insurance program.

But Rep. Frank Pallone Jr., D-N.J., and Sen. Ron Wyden, D-Ore., who requested the latest CBO analysis, said the policies will ultimately limit benefits and result in coverage losses.

“This analysis from the non-partisan, independent CBO is straightforward: the Republican plan for health care means benefit cuts and terminated health insurance for millions of Americans who count on Medicaid,” Wyden said in a statement. “Republicans continue to use smoke and mirrors to try to trick Americans into thinking they aren’t going to hurt anybody when they proceed with this reckless plan, but fighting reality is an uphill battle.”

The letter from the CBO analyzes five potential policy options for Medicaid: setting the federal matching rate for the expansion population at the same rate as other enrollees; limiting state taxes on providers; setting federal caps on spending for the entire Medicaid population or just the expansion group; and repealing two regulations linked to eligibility and enrollment.

Most of the options reduce the funds available to states, according to the CBO. The agency expects states will replace about half of the reduced support with their own resources, and then reduce spending by cutting provider payment rates, reducing optional benefits and cutting enrollment.

For example, if Congress decides to limit provider taxes, where states levy taxes that finance a portion of their Medicaid spending, thatwould result in 8.6 million fewer people enrolled in Medicaid in 2034, including nearly 4 million becoming uninsured. The move would ultimately lessen the federal deficit by $668 billion, as the government would offer reimbursement for lower state spending, the analysis found.

Another option, placing a cap on federal spending for the expansion population, would save $225 billion — but 3.3 million people would lose Medicaid coverage. Repealing regulations that aim to reduce barriers to enrollment and simplify the renewal process would reduce the federal deficit by $162 billion over the next decade, but 2.3 million fewer people would be enrolled in Medicaid, the CBO found.

Democrat lawmakers are urging Republicans debating cuts to Medicaid to focus instead on fraud, waste and abuse in another federal healthcare program: Medicare Advantage.

Curbing upcoding in the privatized Medicare plans, wherein insurers exaggerate the health needs of their members to inflate government reimbursement, is a better avenue for saving federal dollars than restricting benefits or cutting eligibility in Medicaid, the 36 Democrats wrote in a letter to GOP leadership on Wednesday.

The letter was addressed to Senate Majority Leader John Thune, R-S.D, and House Speaker Mike Johnson, R-La., and comes as Republicans debate different policies to reach savings targets.

Dive Insight:

Republicans in Congress are aiming to extend tax cuts from President Donald Trump’s first term. Their budget directs the House Energy and Commerce Committee to cut $880 billion in spending — a goal that’s impossible to reach without touching Medicaid, which (along with its sister program for children) provides safety-net insurance to some 80 million Americans.

Now, Democrats in both chambers are urging Republicans to redirect their attention from Medicaid to MA, privatized plans for Medicare seniors that can provide additional benefits but also restrict care in a way traditional Medicare is not allowed to do. Still, the plans have steadily grown in popularity and now cover more than half of the 68 million Americans in Medicare.

“Your directive to cut federal health care spending should come from reducing waste, fraud, and abuse like upcoding by for-profit insurance companies, not by cutting health care benefits for American families who rely on Medicaid to make ends meet,” the Democrats’ letter reads.

The letter cites a Wall Street Journal investigation into upcoding published last year that found MA insurers frequently added diagnoses for their members for which their members never received treatment or that went against doctors’ observations. The practice drove a total of $50 billion in additional payments to the private insurers over three years, according to the investigation.

Similarly, influential congressional advisory group MedPAC found CMS paid MA insurers $84 billion more in 2024 than the government would have if those members had been in traditional Medicare. Upcoding was responsible for almost half of those overpayments.

Traditionally, Republicans broadly support MA, which was created on the premise that private insurers could help the government manage Medicare more economically. However, there’s been rising bipartisan support for reforming the program in light of growing evidence of practices like upcoding that inflate government reimbursement to plans without helping enrollees.

In his confirmation hearing, Dr. Mehmet Oz, the surgeon and television personality tapped by Trump as the administrator of the CMS, agreed that tackling fraud, waste and abuse in MA was a “rational” way of lowering federal healthcare spending.

“We’re actually apparently paying more for Medicare Advantage than we’re paying for regular Medicare. So it’s upside down,” Oz said in front of the Senate Finance Committee in March.

Republicans in the House are currently trying to figure out how to achieve desired savings without slashing Medicaid, given the program’s political popularity, including among Republican voters.

GOP leadership recently appeared to rule out two Medicaid policies that would cause significant upheaval for enrollees in the program: lowering the portion of Medicaid costs borne by the federal government for the Medicaid expansion population, and per-capita caps on benefits for beneficiaries in expansion states.

“Moving forward with this dangerous plan to rip health care away from low- and middle-income Americans would be a man-made disaster for the health of the nation and the economy,” the Democrats’ letter reads. “We urge you instead to listen to Administrator Oz and tackle real fraud, waste, and abuse by private, for-profit health insurers in MA.”

House E&C is expected to hold its reconciliation markup next week.

Wall Street is speaking loudly to Medicare Advantage insurers: If you want us to stick with you, keep dumping seniors who are pinching your profit margins.

Investors continue to punish UnitedHealth Group since the company downgraded its 2025 profit expectations on April 17. On Friday, UnitedHealth’s stock price hit not only a 52-week low—$393.11—but its lowest point in years. The last time UnitedHealth’s stock price went below $400 a share was on October 14, 2021.

The company’s shares lost nearly 4.5% of their value during the past week, contributing to a decline that started soon after the company set an all-time high of $630.73 last November. UnitedHealth’s shares have lost more than 33% of their value since then.

Wall Street Sends a Message

Meanwhile, investors have once again embraced UnitedHealth’s top two rivals in the Medicare Advantage business–Humana and CVS/Aetna. Those companies told investors last year, when both were in the Wall Street dog house for spending more than investors expected on patients’ medical care, that they would dump hundreds of thousands of their costliest Medicare Advantage enrollees to improve their profits. They made good on that promise, shedding almost 650,000 seniors and people with disabilities by the end of the year.

Many of those people enrolled in a UnitedHealth Medicare Advantage plan. The company reported 400,000 more Medicare Advantage enrollees in the first quarter of 2025 than in the fourth quarter of 2024. That used to be a good thing, but UnitedHealth’s executives told investors on April 17 that it wouldn’t make as much money for them as the company had assured them just three months earlier because it likely will have to spend more than they expected on those new MA enrollees’ medical care. Investors responded by immediately dispatching the company’s shares to the cellar. Those shares lost about 23% of their value in a single day.

The Street had also punished Humana and CVS last year when they said they were paying more for seniors’ medical care than they’d expected. Shares of both companies cratered, losing around half their value. So, executives at both Humana and CVS started identifying Medicare markets to get out of entirely. The culling was ruthless. CVS shed 227,000 MA enrollees. Humana got rid of 419,000.

Locked Out of Traditional Medicare

Those seniors and disabled people had to scramble to find a new Medicare Advantage insurer because it is difficult for most people to go back to traditional Medicare and find an affordable Medicare supplement policy. Medicare supplement insurers must waive underwriting during the first six months of applicants’ eligibility for Medicare, but people who enroll in a Medicare Advantage plan and want or need to make a change months later find out that insurers will charge them more unless their health is nearly perfect.

Of the seven big for-profit health insurers, four (Cigna, CVS/Aetna, Humana and Centene) collectively cut 1.3 million of their Medicare Advantage enrollees adrift at the end of 2024 in an effort to stay in Wall Street’s good graces. Cigna dumped all 600,000 of its MA enrollees, selling them to the Blue Cross corporation HCSC. For-profit Blue Cross insurer Elevance picked up 227,000; Molina added 18,000, and, as noted, UnitedHealth signed up 400,000 new MA enrollees.

While UnitedHealth’s shares have lost a third of their value, CVS’s shares have increased more than 50% since the first of this year. They even set a 52-week high of $72.51 on Thursday. Humana’s shares closed Friday at $258.48, up 1.88% since January 1. They are out of the Wall Street dog house – for now, anyway.

Profits, Lobbying Soar

I trust you are not feeling sorry for UnitedHealth because of its misfortune on Wall Street. It is still a hugely profitable company–just not profitable enough lately to please investors. This huge corporation, the fourth largest in America, reported $9.1 billion in profits in just the first quarter of this year. If the company makes it more difficult for its health plan enrollees to get the care they need this year, it could make even more than the $34.4 billion in profits it made last year.

And as a group, the seven big for-profits, including those that spent more than Wall Street felt was necessary on patients’ medical care, made $70 billion in profits last year. (UnitedHealth made nearly as much as the other six combined.)

And collectively, those giant corporations took in a record $1.5 trillion in revenue from us as customers and taxpayers last year. They are doing quite well. But that won’t stop them from trying to keep lawmakers and Trump administration officials from cracking down this year on the widespread waste, fraud and abuse in the Medicare Advantage program. You can expect them to spend a record amount of our money on lobbying expenses in Washington this year to keep their Medicare Advantage cash cow well fed.