In my report June 10, I wrote: “The major sources of physician discontent are administrative hassles and unwelcome clinical oversight that create dissonance. They conflict with a false sense of autonomy that the majority of physicians imagined when choosing medicine. Cuts to reimbursement, participation in alternative payment models and medical inflation are manifestations of a system in which ‘suits’ are intruders who make rules, exact handsome salaries, generate corporate profits and distance physicians from patient care purposely… “

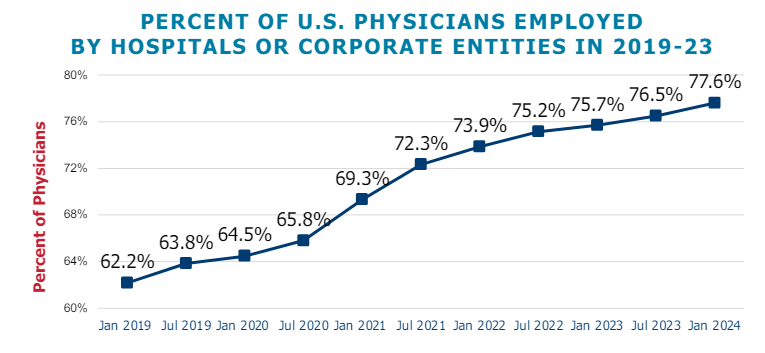

This assessment remains true today. Discontent among physicians is palpable and it’s magnified by a growing sense of financial despair among many clinicians. And it poses a unique challenge to hospitals that now employ more than half of America’s physician workforce.

In the “good ole days”, hospitals provided a place for physicians to ply their trade. They were credentialled to practice their chosen specialty, granted special parking, food and amenities and treated as the hospital’s most welcome customer. Made sense: physicians controlled most patient decisions about the hospital services they use. Physicians controlled the hospital’s revenue, sustainability and bonuses earned by administrators. Insurers brought privately-insured patients to doctors who charged them 1.6-2.5 times what Medicare paid and physician income was not threatened. That was then. This is now.

Today, insurers play a larger role. Consumer expectations have changed. Policymakers are paying more attention. And demand has shifted from inpatient services to outpatient, home and office settings for health and wellbeing services in addition to acute care. And the current forecast by CMS through 2032 predicts spending for hospitals will increase at a compound rate of 5.7% vs. 5.6% for physicians adding more hospital-physician financial tension to the system. Both well-above inflation and CDP growth prompting heightened pressure to spend less.

In anticipation, consolidation of hospitals into multi-hospital systems has been a staple in recent years: only 1 in 5 hospitals is independent these days, and most of these are small, rural or otherwise destined to independence for their uncertain future. Whether public, investor-owned or not-for-profit (or tax exempt as some prefer), the economic realities of running hospitals coupled with the regulatory constraints imposed by state and federal law forced all to re-think their future.And, for most, employing physicians directly was a means to an end of staying alive while the dust settles.

But the unintended consequence of physician employment is soured relationships between the employed physicians and their hospital:

their financial and emotional security has become tangled up by interactions with hospital leaders and former peers appointed to oversee their work.

And their views about their hospital have morphed to negativity based on four underlying beliefs:

Hospitals spend too much on overhead and executive salaries and not enough on direct patient care.

Hospitals are run poorly: we could run them better but they don’t listen to us.

Hospitals get rate increases from Medicare and physicians get screwed.

Hospitals need us more than we need them. But they don’t understand that.

On March 9, 2024, President Biden signed the Consolidated Appropriations Act, 2024, which included a 2.93% update to the CY 2024 Physician Fee Schedule (PFS) Conversion Factor (CF) for dates of service March 9 through December 31, 2024. But physicians saw that as not enough since their overhead increased even more. And for 2025, CMS is proposing to reduce average payment rates under the MPFS by2.93% compared to the average amount reimbursed for these services in CY 2024 based on CY 2025 MPFS conversion factor decrease of $0.93 (or 2.8%) from the current CY 2024 conversion factor.

Understandably, physicians are upset. They’re not delusional that private insurers will make up the difference nor imagining hospitals will divert funds their way from brick, stick and tech priorities. But they’re speaking out expressing their views to anyone who’ll listen.

For hospitals that employ physicians, the issue of their financial anxiety requires urgent attention–not as one of many alongside 340B, site neutral payments and others but as the one at the top of the list. The issue is not whether physician income relative to other professions and average households is high. The issue is about managing physician expectations about their livelihood realistically and practically while improving their clinical acumen as professionals.

The core beliefs held by employed physicians about their hospitals may not be fair, objective or accurate, but they’re no less deeply felt and impactful. Hospital boards and C suite leaders would be well-served to refresh plans accordingly.

On October 15, the open enrollment period for Medicare begins running through December 7 for coverage starting in January 2025. In this period, 67 million Medicare eligible seniors can review features of Medicare plans offered in their area, switch from traditional Medicare to a Medicare Advantage (MA) plan (or vice versa), change their MA selection and add/change their Medicare Part D prescription drug plans.

In 2024, Medicare Advantage plans enrolled 33 million seniors and Medicare paid private insurers $462 billion to pay for their care.

But conditions for Medicare Advantage have changed in recent years prompting many to ask ‘what is the Medicare Advantage?’

Background:

Medicare began July 30, 1965 as a key element in President Lyndon Baines Johnson’s Great Society program offering federal-government-paid insurance coverage for seniors at the age of 65. “Original Medicare” had two parts: Part A to cover hospitals and Part B to cover physicians and outpatient services. In 1972, coverage for adults with disabilities was added, and in 2003, coverage for prescription drugs (Part D) was added.

Its funding comes from payroll taxes paid by employers and their employees, and those who are self-employed PLUS income taxes paid on Social Security benefits, interest earned on the Medicare trust fund’s investments and Part A premiums from people who aren’t eligible for premium-free Part A.

Along the way, Congress authorized seniors the option of accessing Medicare through private insurers aka Part C (Balanced Budget Act of 1997), expanded its scope (Medicare Modernization Act of 2003) and supplemented its funding differential above Original Medicare (Patient Protection and Affordable Care Act 2010) to stimulate enrollment growth. The rationale for MA was straightforward: it offered federal regulators a lab to test care management for seniors with the dual aims of lowering their health costs and improving their health. Private insurers responded. By design, funding for MA was set above Original Medicare rates to encourage private insurer participation.

It worked. This year, the average MA enrollee had 43 plans from which to choose. By three measures, Medicare Part C has been successful:

Enrollment growth: Enrollment in MA plans has increased from 31% of Medicare eligible adults in 2014 to 51% in 2024 and is projected to increase in 2025. Notably, enrollment in special needs and employer-sponsored MA plans has increased faster than the individual MA market which is subject to open enrollment periods. Satisfaction appears high (69% of members do not shop for another plan during open enrollment periods) and member churn is low.

Medicare has saved money: Per the 2024 Medicare Trustees’ Report, MA has contributed to slower growth in Medicare spending than forecast. “The Social Security and Medicare programs both continue to face significant financing issues…The Hospital Insurance (HI) Trust Fund will be able to pay 100% of total scheduled benefits until 2036, 5 years later than reported last year. At that point, that fund’s reserves will become depleted and continuing program income will be sufficient to pay 89% of total scheduled benefits.”

Private insurer participation has been strong: For health insurers, Medicare Advantage is profitable: PMPM contribution margins are 50-100% higher than individual and group lines of business. And, as CMS payments to MA have tightened, the MA insurer market consolidated with 3 (UnitedHealth, Humana, CVS-Aetna) taking advantage of operating pressures on small players to increase their share to 58% of total enrollment. Advantage: Seniors, Medicare and Corporate Insurance.

But conditions going forward suggest the MA advantage might not be as strong. The market signals are clear:

Insurer belt tightening: Since 2023, seniors’ use of hospitals, specialty care and prescription drugs has returned to pre-pandemic normalcy cutting into insurer margins. In its CY 2025 Rate Announcement September 27, CMS announced “The average monthly plan premium for all MA plans, which includes MA plans that provide prescription drug coverage and MA Special Needs Plans (SNPs), is projected to decrease from $18.23 in 2024 to $17.00 in 2025. Benefit options will remain stable, including MA supplemental benefit offerings such as hearing, dental, and vision. The amount of rebate dollars, which can be used for supplemental benefits, will remain stable, with a slight increase, from 2024 to 2025. Enrollment in MA is projected to be 35.7 million in 2025, an increase from 2024, with MA enrollment representing approximately 51% of all people enrolled in Medicare.” This translates to lower margins for MA plans, fewer supplemental benefits for enrollees and lower payments to hospitals and physicians.

Increased regulatory scrutiny: The Medicare Payment Advisory Commission (MedPAC) concluded that MA plans receive payments from CMS that are 122%of spending for similar beneficiaries in traditional Medicare, on average, translating to an estimated $83 billion in overpayments in 2024. Congress is investigating. In 2023, CMS adopted tougher audit standards specific to diagnosis codes used by private MA plans to bill Medicare on behalf of their enrollees. Audits conducted by the U.S. Department of Human Services’ Office of Inspector General (OIG) applying the new standards found the majority of private MA plans guilty of upcoding and thereby overpaid by Medicare. In 2025, cut points used by CMS to award star ratings have been modified resulting in fewer plans getting 4-star ratings that enable their participation in 5% bonus payments—a major reason recent stock declines for UHG, HUM, CVS and others. Regulatory scrutiny of MA plan marketing practices, coding, denials and prior authorization procedures will intensify reflecting bipartisan intent to constrain MA profits.

Understandably, tension between MA insurers and providers has intensified as insurers seek to protect their margins. The Change Healthcare (CH) cyber-attack (February 21, 2024) that disabled insurer payments to hospitals and physicians stoked animosity since CH is a subsidiary of UnitedHealth Group–the largest sponsor of MA plans and the healthcare juggernaut. Though operating margins for half of U.S. hospitals have recovered, insurer cuts coupled with labor and prescription drug costs have decimated care delivery in almost every community. Participation in MA plan provider networks, once SOP is now a tough call for hospitals, medical groups and other providers.

My take:

What is the Medicare Advantage?

As a lab for innovation in care management for seniors, it’s promising.

As an engine to drive lower costs for senior health and extended solvency to the Medicare program, it’s unclear.

As a platform to shift incentives from fee-for-service to value across the system, it’s helpful.

But until and unless hospitals, physicians, insurers, business leaders and regulators commit to implement a transformed system of health that’s comprehensive, affordable, efficient and accountable, the Medicare Advantage will be marginalized.

In many ways, the headwinds facing MA are part of the larger narrative facing healthcare:

public sentiment against consolidation and corporatization has eroded its cherished trust and confidence. It’s true for insurance, hospitals, prescription drug companies and PBMs. The blame is shared: no one of these owns the moral high ground (though a few organizations in their ranks aspire).

With days before voters decide the composition of the 119th U.S. Congress and the next White House occupant, the immediate future for U.S. healthcare is both predictable and problematic:

It’s predictable that…

1-States will be the epicenter for healthcare legislation and regulation; federal initiatives will be substantially fewer.

At a federal level, new initiatives will be limited: continued attention to hospital and insurer consolidation, drug prices and the role of PBMs, Medicare Advantage business practices and a short-term fix to physician payments are likely but little more. The Affordable Care Act will be modified slightly to address marketplace coverage and subsidies and CMSs Center for Medicare and Medicaid Innovation (CMMI) will test new alternative payment models even as doubt about their value mounts. But “BIG FEDERAL LAWS” impacting the U.S. health system are unlikely.

But in states, activity will explode: for example…

In this cycle, 10 states will decide their abortion policies joining 17 others that have already enacted new policies.

3 will vote on marijuana legalization joining 24 states that have passed laws.

24 states have already passed Prescription Drug Pricing legislation and 4 are considering commissions to set limits.

40 have expanded their Medicaid programs

35 states and Washington, D.C., operate CON programs; in 12 states, CONs have been repealed.

14 have legislation governing mental health access.

5 have passed or are developing commissions to control health costs.

And so on.

Given partisan dysfunction in Congress and the surprising lack of attention to healthcare in Campaign 2024 (other than abortion coverage), the center of attention in 2025-2026 will be states. In addition to the list above, attention in states will address protections for artificial intelligence utilization, access to and pricing for weight loss medications, tax exemptions for not-for-profit health systems, telehealth access, conditions for private equity ownership in health services, constraints on contract pharmacies, implementation of site neutral payments, new 340B accountability requirements and much more. In many of these efforts, state legislatures and/or Governors will go beyond federal guidance setting the stage for court challenges, and the flavor of these efforts will align with a state’s partisan majorities: as of September 30th, 2024, Republicans controlled 54.85% of all state legislative seats nationally, while Democrats held 44.19%. Republicans held a majority in 56 chambers, and Democrats held the majority in 41 chambers. In 2024, 27 states are led by GOP governors and 23 by Dems and 11 face voters November 5. And going into the election, 22 states are considered red, 21 are considered blue and 7 are tagged as purple.

The U.S. Constitution affirms Federalism as the structure for U.S. governance: it pledges the pursuit of “life, liberty and the pursuit of happiness” as its purpose but leaves the lion’s share of responsibilities to states to figure out how. Healthcare may be federalism’s greatest test.

2-Large employers will take direct action to control their health costs.

Per the Kaiser Family Foundation’s most recent employer survey, employer health costs are expected to increase 7% this year for the second year in a row. Willis Towers Watson, predicts a 6.4% increase this year on the heels of a 6% bump last year. The Business Group on Health, which represents large self-insured employers, forecasts an 8% increase in 2025 following a 7% increase last year. All well-above inflation, ages and consumer prices this year.

Employers know they pay 254% of Medicare rates (RAND) and they’re frustrated. They believe their concerns about costs, affordability and spending are not taken seriously by hospitals, physicians, insurers and drug companies. They see lackluster results from federal price transparency mandates and believe the CMS’ value agenda anchored by accountable care organizations are not achieving needed results. Small-and-midsize employers are dropping benefits altogether if they think they can. For large employers, it’s a different story. Keeping health benefits is necessary to attract and keep talent, but costs are increasingly prohibitive against macro-pressures of workforce availability, cybersecurity threats, heightened supply-chain and logistics regulatory scrutiny and shareholder activism.

Maintaining employee health benefits while absorbing hyper-inflationary drug prices, insurance premiums and hospital services is their challenge. The old playbook—cost sharing with employees, narrow networks of providers, onsite/near site primary care clinics et al—is not working to keep up with the industry’s propensity to drive higher prices through consolidation.

In 2025, they will carefully test a new playbook while mindful of inherent risks. They will use reference pricing, narrow specialty specific networks, technology-enabled self-care and employee gainsharing to address health costs head on while adjusting employee wages. Federal and state advocacy about Medicare and Medicaid funding, insurer and hospital consolidation and drug pricing will intensify. And some big names in corporate America will step into a national debate about healthcare affordability and accountability.

Employers are fed up with the status quo. They don’t buy the blame game between hospitals, insurers and drug companies. And they don’t think their voice has been heard.

3-Private equity and strategic investors will capitalize on healthcare market conditions.

The plans set forth by the two major party candidates feature populist themes including protections for women’s health and abortion services, maintenance/expansion of the Affordable Care Act and prescription drug price controls. But the substance of their plans focus on consumer prices and inflation: each promises new spending likely to add to the national deficit:

Per the Non-Partisan Committee for a Responsible Federal Budget, over the next 10 years, the Trump plan would add $7.5 trillion to the deficit; the Harris plan would add $3.5 trillion.

Per the Wharton School at the University of Pennsylvania, Harris’ proposals would add $1.2 trillion to the national deficits over 10 years and Trump’s proposals would add $5.8 trillion over the same period

Per the Congressional Budget Office, federal budget deficit for FY2024 which ended September 30 will be $1.8 trillion– $139 billion more than FT 2023. Revenues increased by an estimated $479 billion (or 11 percent). Revenues in all major categories, but notably individual income taxes, were greater than they were in fiscal year 2023. Outlays rose by an estimated $617 billion (or 10 percent). The largest increase in outlays was for education ($308 billion). Net outlays for interest on the public debt rose by $240 billion to total $950 billion.

The federal government spent $6.75 trillion in 2024, a 10% increase from the prior year. Spending on Social Security (22% of total spending) and healthcare programs (28.5% of total spending) also increased substantially. The U.S. debt as of Friday was $37.77 trillion, or $106 thousand per citizen.

The non-partisan Congressional Budget Office (CBO) reports that federal debt held by the public averaged 48.3 % of GDP for the half century ending in 2023– far above its historic average. It projects next year’s national debt will hit 100% for the first time since the US military build-up in the second world war. And it forecast the debt reaching 122.4% in 2034 potentially pushing interest payments from 13% of total spending this year to 20% or more.

Adding debt is increasingly cumbersome for national lawmakers despite campaign promises, and healthcare is rivaled by education, climate and national defense in seeking funding through taxes and appropriations. Thus, opportunities for private investors in healthcare will increase dramatically in 2025 and 2026. After all, it’s a growth industry ripe for fresh solutions that improve affordability and cost reduction at scale.

Combined, these three predictions foretell a U.S. healthcare system that faces a significant pressure to demonstrate value.

They require every healthcare organization to assess long-term strategies in the likely context of reduced funding, increased regulation and heightened attention to prices and affordability. This is problematic for insiders accustomed to incrementalism that’s protected them from unwelcome changes for 3 decades.

Announcements last week by Walgreens and CVS about changes to their strategies going forward reflect the industry’s new normal: change is constant, success is not. In 2025, regardless of the election outcome, healthcare will be a major focus for lawmakers, regulators, employers and consumers.

Like everyone else, I am thankful the election end is in sight and a degree of “normalcy” might return. By next week, we should know who will sit in the White House, the 119th Congress and 11 new occupants of Governors’ offices. But a return to pre-election normalcy in politics is a mixed blessing.

“Normalcy” in our political system means willful acceptance that our society is hopelessly divided by income, education, ethnic and political views. It’s benign acceptance of a 2-party system, 3-branches of government (Executive, Legislative, Judicial) and federalism that imposes limits on federal power vis a vis the Constitution.

Our political system’ normalcy counts success by tribal warfare and election wins. Normalcy is about issues de jour prioritized by each tribe, not longer-term concern for the greater good in our country. Normalcy in our political system is near-sightedness—winning the next election and controlling public funds.

Comparatively, “normalcy” in U.S. healthcare is also tribal:

while the majority of U.S. adults believe the status quo is not working well but recognize its importance, each tribe has a different take on its future. The majority of the public think price transparency, limits on consolidation, attention to affordability and equitable access are needed but the major tribes—hospitals, insurers, drug companies, insurers, device-makers—disagree on how changes should be made. And each is focused on short-term issues of interest to their members with rare attention to longer-term issues impacting all.

Near-sightedness in healthcare is manifest in how executives are compensated, how partnerships are formed and how Boards are composed.

Organizational success is defined by 1-access to private capital (debt, private equity, strategic investors), 2-sustainnable revenue-growth, 4- scalable costs, 4-opportunities for consolidation (the exit strategy of choice for most) and 5-quarterly earnings. A long-term view of the system’s future is rarely deliberated by boards save attention to AI or the emergence of Big Tech. A vision for an organization’s future based on long-term macro-trends and outside-in methodologies is rare: long-term preparedness is “appreciated” but near-term performance is where attention is vested.

It pays to be near-sighted in healthcare: our complex regulatory processes keep unwelcome change at bay and our archaic workforce rules assure change resistance. …until it doesn’t. Industries like higher education, banking and retailing have experienced transformational changes that take advantage of new technologies and consumer appetite for alternatives that are new and better. The organizations winning in this environment balance near-sightedness with market attentiveness and vision.

Looking ahead, I have no idea who the winners and losers will be in this election cycle. I know, for sure, that…

The final result will not be known tomorrow and losers will challenge the results.

Short-term threats to the healthcare status quo will be settled quickly. First up: Congress will set aside Medicare pay cuts to physicians (2.8%) scheduled to take effect in January for the 5th consecutive year. And “temporary” solutions to extend marketplace insurance subsidies, facilitate state supervision of medication abortion services and telehealth access will follow quickly.

Think tanks will be busy producing white papers on policy changes supported by their funding sponsors.

And trade associations will produce their playbooks prioritizing legislative priorities and relationship opportunities with state and federal officials for their lobbyists.

Near-term issues for each tribe will get attention: the same is true in healthcare. Discussion about and preparation for healthcare’s longer-term future is a rarity in most healthcare C suites and Boardrooms. Consider these possibilities:

Medicare Advantage will be the primary payer for senior health: federal regulators will tighten coverage, network adequacy, premiums and cost sharing with enrollees to private insurers reducing enrollee choices and insurer profits.

To address social determinants of health, equitable access and comprehensive population health needs, regional primary care, preventive and public health programs will be fully integrated.

Large, organized groups/networks of physicians will be the preferred “hubs” for health services in most markets.

Interoperability will be fully implemented.

Physicians will unionize to assert their clinical autonomy and advance their economic interests.

The federal government (and some states) will limit tax exemptions for profitable not-for-profit health systems.

The prescription drug patent system will be modernized to expedite time-to-market innovations and price-value determinations.

The health insurance market will focus on individual (not group) coverage.

Congress/states will impose price controls on prescription drugs and hospital services.

Employers will significantly alter their employee benefits programs to reduce their costs and shift accountability to their employees. Many will exit altogether.

Regional integrated health systems that provide retail, hospital, physician, public health and health insurance services will be the dominant source of services.

Alternative-payment models used by Medicare to contract with providers will be completely overhauled.

Consumers will own and control their own medical records.

Consolidation premised on community benefits, consumer choices and lower costs will be challenged aggressively and reparation pursued in court actions.

Voters will pass Medicare for All legislation.

And many others.

A process for defining of the future of the U.S. health system and a bipartisan commitment by hospitals, physicians, drug companies, insurers and employers to its implementation are needed–that’s the point.

Near-sightedness in our political system and in our health, system is harmful to the greater good of our society and to the voters, citizens, patients, and beneficiaries all pledge to serve.

As respected healthcare marketer David Jarrard wrote in his blog post yesterday “As the aggravated disunity of this political season rises and falls, healthcare can be a unique convener that embraces people across the political divides, real or imagined. Invite good-minded people to the common ground of healthcare to work together for the common good that healthcare must be.”

Thinking and planning for healthcare’s long-term future is not a luxury: it’s an urgent necessity. It’s also not “normal” in our political and healthcare systems.

In 1975, researchers at Stanford invited a group of undergraduates to take part in a study about suicide. They were presented with pairs of suicide notes. In each pair, one note had been composed by a random individual, the other by a person who had subsequently taken his own life. The students were then asked to distinguish between the genuine notes and the fake ones.

Some students discovered that they had a genius for the task. Out of twenty-five pairs of notes, they correctly identified the real one twenty-four times. Others discovered that they were hopeless. They identified the real note in only ten instances.

As is often the case with psychological studies, the whole setup was a put-on. Though half the notes were indeed genuine—they’d been obtained from the Los Angeles County coroner’s office—the scores were fictitious. The students who’d been told they were almost always right were, on average, no more discerning than those who had been told they were mostly wrong.

In the second phase of the study, the deception was revealed.

The students were told that the real point of the experiment was to gauge their responses to thinking they were right or wrong. (This, it turned out, was also a deception.) Finally, the students were asked to estimate how many suicide notes they had actually categorized correctly, and how many they thought an average student would get right. At this point, something curious happened. The students in the high-score group said that they thought they had, in fact, done quite well—significantly better than the average student—even though, as they’d just been told, they had zero grounds for believing this. Conversely, those who’d been assigned to the low-score group said that they thought they had done significantly worse than the average student—a conclusion that was equally unfounded.

“Once formed,” the researchers observed dryly, “impressions are remarkably perseverant.”

A few years later, a new set of Stanford students was recruited for a related study. The students were handed packets of information about a pair of firefighters, Frank K. and George H. Frank’s bio noted that, among other things, he had a baby daughter and he liked to scuba dive. George had a small son and played golf. The packets also included the men’s responses on what the researchers called the Risky-Conservative Choice Test. According to one version of the packet, Frank was a successful firefighter who, on the test, almost always went with the safest option. In the other version, Frank also chose the safest option, but he was a lousy firefighter who’d been put “on report” by his supervisors several times. Once again, midway through the study, the students were informed that they’d been misled, and that the information they’d received was entirely fictitious. The students were then asked to describe their own beliefs. What sort of attitude toward risk did they think a successful firefighter would have? The students who’d received the first packet thought that he would avoid it. The students in the second group thought he’d embrace it.

Even after the evidence “for their beliefs has been totally refuted, people fail to make appropriate revisions in those beliefs,” the researchers noted. In this case, the failure was “particularly impressive,” since two data points would never have been enough information to generalize from.

The Stanford studies became famous. Coming from a group of academics in the nineteen-seventies, the contention that people can’t think straight was shocking. It isn’t any longer. Thousands of subsequent experiments have confirmed (and elaborated on) this finding. As everyone who’s followed the research—or even occasionally picked up a copy of Psychology Today—knows, any graduate student with a clipboard can demonstrate that reasonable-seeming people are often totally irrational. Rarely has this insight seemed more relevant than it does right now. Still, an essential puzzle remains: How did we come to be this way?

In a new book, “The Enigma of Reason” (Harvard), the cognitive scientists Hugo Mercier and Dan Sperber take a stab at answering this question. Mercier, who works at a French research institute in Lyon, and Sperber, now based at the Central European University, in Budapest, point out that reason is an evolved trait, like bipedalism or three-color vision. It emerged on the savannas of Africa, and has to be understood in that context.

Stripped of a lot of what might be called cognitive-science-ese, Mercier and Sperber’s argument runs, more or less, as follows: Humans’ biggest advantage over other species is our ability to coöperate. Coöperation is difficult to establish and almost as difficult to sustain. For any individual, freeloading is always the best course of action. Reason developed not to enable us to solve abstract, logical problems or even to help us draw conclusions from unfamiliar data; rather, it developed to resolve the problems posed by living in collaborative groups.

“Reason is an adaptation to the hypersocial niche humans have evolved for themselves,” Mercier and Sperber write. Habits of mind that seem weird or goofy or just plain dumb from an “intellectualist” point of view prove shrewd when seen from a social “interactionist” perspective.

Consider what’s become known as “confirmation bias,” the tendency people have to embrace information that supports their beliefs and reject information that contradicts them. Of the many forms of faulty thinking that have been identified, confirmation bias is among the best catalogued; it’s the subject of entire textbooks’ worth of experiments. One of the most famous of these was conducted, again, at Stanford. For this experiment, researchers rounded up a group of students who had opposing opinions about capital punishment. Half the students were in favor of it and thought that it deterred crime; the other half were against it and thought that it had no effect on crime.

The students were asked to respond to two studies. One provided data in support of the deterrence argument, and the other provided data that called it into question. Both studies—you guessed it—were made up, and had been designed to present what were, objectively speaking, equally compelling statistics. The students who had originally supported capital punishment rated the pro-deterrence data highly credible and the anti-deterrence data unconvincing; the students who’d originally opposed capital punishment did the reverse. At the end of the experiment, the students were asked once again about their views. Those who’d started out pro-capital punishment were now even more in favor of it; those who’d opposed it were even more hostile.

If reason is designed to generate sound judgments, then it’s hard to conceive of a more serious design flaw than confirmation bias. Imagine, Mercier and Sperber suggest, a mouse that thinks the way we do. Such a mouse, “bent on confirming its belief that there are no cats around,” would soon be dinner. To the extent that confirmation bias leads people to dismiss evidence of new or underappreciated threats—the human equivalent of the cat around the corner—it’s a trait that should have been selected against. The fact that both we and it survive, Mercier and Sperber argue, proves that it must have some adaptive function, and that function, they maintain, is related to our “hypersociability.”

Mercier and Sperber prefer the term “myside bias.” Humans, they point out, aren’t randomly credulous. Presented with someone else’s argument, we’re quite adept at spotting the weaknesses. Almost invariably, the positions we’re blind about are our own.

A recent experiment performed by Mercier and some European colleagues neatly demonstrates this asymmetry. Participants were asked to answer a series of simple reasoning problems. They were then asked to explain their responses, and were given a chance to modify them if they identified mistakes. The majority were satisfied with their original choices; fewer than fifteen per cent changed their minds in step two.

In step three, participants were shown one of the same problems, along with their answer and the answer of another participant, who’d come to a different conclusion. Once again, they were given the chance to change their responses. But a trick had been played: the answers presented to them as someone else’s were actually their own, and vice versa. About half the participants realized what was going on. Among the other half, suddenly people became a lot more critical. Nearly sixty per cent now rejected the responses that they’d earlier been satisfied with.

This lopsidedness, according to Mercier and Sperber, reflects the task that reason evolved to perform, which is to prevent us from getting screwed by the other members of our group.

Living in small bands of hunter-gatherers, our ancestors were primarily concerned with their social standing, and with making sure that they weren’t the ones risking their lives on the hunt while others loafed around in the cave. There was little advantage in reasoning clearly, while much was to be gained from winning arguments.

Among the many, many issues our forebears didn’t worry about were the deterrent effects of capital punishment and the ideal attributes of a firefighter. Nor did they have to contend with fabricated studies, or fake news, or Twitter. It’s no wonder, then, that today reason often seems to fail us. As Mercier and Sperber write, “This is one of many cases in which the environment changed too quickly for natural selection to catch up.”

Steven Sloman, a professor at Brown, and Philip Fernbach, a professor at the University of Colorado, are also cognitive scientists. They, too, believe sociability is the key to how the human mind functions or, perhaps more pertinently, malfunctions. They begin their book, “The Knowledge Illusion: Why We Never Think Alone” (Riverhead), with a look at toilets.

Virtually everyone in the United States, and indeed throughout the developed world, is familiar with toilets. A typical flush toilet has a ceramic bowl filled with water. When the handle is depressed, or the button pushed, the water—and everything that’s been deposited in it—gets sucked into a pipe and from there into the sewage system. But how does this actually happen?

In a study conducted at Yale, graduate students were asked to rate their understanding of everyday devices, including toilets, zippers, and cylinder locks. They were then asked to write detailed, step-by-step explanations of how the devices work, and to rate their understanding again. Apparently, the effort revealed to the students their own ignorance, because their self-assessments dropped. (Toilets, it turns out, are more complicated than they appear.)

Sloman and Fernbach see this effect, which they call the “illusion of explanatory depth,” just about everywhere. People believe that they know way more than they actually do. What allows us to persist in this belief is other people. In the case of my toilet, someone else designed it so that I can operate it easily. This is something humans are very good at. We’ve been relying on one another’s expertise ever since we figured out how to hunt together, which was probably a key development in our evolutionary history. So well do we collaborate, Sloman and Fernbach argue, that we can hardly tell where our own understanding ends and others’ begins.

“One implication of the naturalness with which we divide cognitive labor,” they write, is that there’s “no sharp boundary between one person’s ideas and knowledge” and “those of other members” of the group.

This borderlessness, or, if you prefer, confusion, is also crucial to what we consider progress. As people invented new tools for new ways of living, they simultaneously created new realms of ignorance; if everyone had insisted on, say, mastering the principles of metalworking before picking up a knife, the Bronze Age wouldn’t have amounted to much. When it comes to new technologies, incomplete understanding is empowering.

Where it gets us into trouble, according to Sloman and Fernbach, is in the political domain. It’s one thing for me to flush a toilet without knowing how it operates, and another for me to favor (or oppose) an immigration ban without knowing what I’m talking about. Sloman and Fernbach cite a survey conducted in 2014, not long after Russia annexed the Ukrainian territory of Crimea. Respondents were asked how they thought the U.S. should react, and also whether they could identify Ukraine on a map. The farther off base they were about the geography, the more likely they were to favor military intervention. (Respondents were so unsure of Ukraine’s location that the median guess was wrong by eighteen hundred miles, roughly the distance from Kiev to Madrid.)

Surveys on many other issues have yielded similarly dismaying results. “As a rule, strong feelings about issues do not emerge from deep understanding,” Sloman and Fernbach write.

And here our dependence on other minds reinforces the problem. If your position on, say, the Affordable Care Act is baseless and I rely on it, then my opinion is also baseless. When I talk to Tom and he decides he agrees with me, his opinion is also baseless, but now that the three of us concur we feel that much more smug about our views. If we all now dismiss as unconvincing any information that contradicts our opinion, you get, well, the Trump Administration.

“This is how a community of knowledge can become dangerous,” Sloman and Fernbach observe. The two have performed their own version of the toilet experiment, substituting public policy for household gadgets. In a study conducted in 2012, they asked people for their stance on questions like: Should there be a single-payer health-care system? Or merit-based pay for teachers? Participants were asked to rate their positions depending on how strongly they agreed or disagreed with the proposals. Next, they were instructed to explain, in as much detail as they could, the impacts of implementing each one. Most people at this point ran into trouble. Asked once again to rate their views, they ratcheted down the intensity, so that they either agreed or disagreed less vehemently.

Sloman and Fernbach see in this result a little candle for a dark world. If we—or our friends or the pundits on CNN—spent less time pontificating and more trying to work through the implications of policy proposals, we’d realize how clueless we are and moderate our views. This, they write, “may be the only form of thinking that will shatter the illusion of explanatory depth and change people’s attitudes.”

One way to look at science is as a system that corrects for people’s natural inclinations.In a well-run laboratory, there’s no room for myside bias; the results have to be reproducible in other laboratories, by researchers who have no motive to confirm them. And this, it could be argued, is why the system has proved so successful. At any given moment, a field may be dominated by squabbles, but, in the end, the methodology prevails. Science moves forward, even as we remain stuck in place.

In “Denying to the Grave: Why We Ignore the Facts That Will Save Us” (Oxford), Jack Gorman, a psychiatrist, and his daughter, Sara Gorman, a public-health specialist, probe the gap between what science tells us and what we tell ourselves. Their concern is with those persistent beliefs which are not just demonstrably false but also potentially deadly, like the conviction that vaccines are hazardous. Of course, what’s hazardous is not being vaccinated; that’s why vaccines were created in the first place. “Immunization is one of the triumphs of modern medicine,” the Gormans note. But no matter how many scientific studies conclude that vaccines are safe, and that there’s no link between immunizations and autism, anti-vaxxers remain unmoved. (They can now count on their side—sort of—Donald Trump, who has said that, although he and his wife had their son, Barron, vaccinated, they refused to do so on the timetable recommended by pediatricians.)

The Gormans, too, argue that ways of thinking that now seem self-destructive must at some point have been adaptive. And they, too, dedicate many pages to confirmation bias, which, they claim, has a physiological component.

They cite research suggesting that people experience genuine pleasure—a rush of dopamine—when processing information that supports their beliefs. “It feels good to ‘stick to our guns’ even if we are wrong,” they observe.

The Gormans don’t just want to catalogue the ways we go wrong; they want to correct for them. There must be some way, they maintain, to convince people that vaccines are good for kids, and handguns are dangerous. (Another widespread but statistically insupportable belief they’d like to discredit is that owning a gun makes you safer.) But here they encounter the very problems they have enumerated. Providing people with accurate information doesn’t seem to help; they simply discount it. Appealing to their emotions may work better, but doing so is obviously antithetical to the goal of promoting sound science. “The challenge that remains,” they write toward the end of their book, “is to figure out how to address the tendencies that lead to false scientific belief.”

“The Enigma of Reason,” “The Knowledge Illusion,” and “Denying to the Grave” were all written before the November election.

The Federal Reserve cut its target interest rate Wednesday by an extra-large half-percentage point and projected more rate cuts this year and next, as its period of trying to put brakes on the economy to fight inflation comes to a close.

Why it matters:

The move lowers borrowing costs for consumers and businesses, as the central bank aims to keep the economy’s expansion going strong amid warning signs on the outlook.

What they’re saying:

“The labor market is actually in solid condition — and our intention with our policy move today is to keep it there,” Fed chair Jerome Powell told reporters at a press conference on Wednesday.

“The U.S. economy is in good shape. It’s growing at a solid pace,” Powell added. “We want to keep it there.”

Zoom in:

The rate cut reflects the U.S. entering a new phase where the softening job market is the predominant economic risk — rather than elevated inflation.

By going with an aggressive half-point cut instead of its more traditional quarter-point adjustment, the Fed moved to get ahead of some evident faltering in the job market.

However, new projections imply the Fed will shift toward smaller quarter-point rate cuts from here.

The cut also thrusts the Fed into election-year politics, as former President Trump has said the central bank should not ease monetary policy mere weeks before the election. Some Democrats have called for even more aggressive rate cuts.

Driving the news:

The policy-setting Federal Open Market Committee lowered its target range for the federal funds rate to 4.75%–5%, from the 5.25–5.5% range in place since last July.

The central bank also released new projections that anticipated the rate will be cut an additional half-point by December — implying a quarter-point cut at each of its two remaining 2024 meetings.

The median Fed officials anticipated their target rate will be down to 3.4% by the end of 2025, which implies four quarter-point rate cuts next year.

“Job gains have slowed,” the Fed’s policy statement noted, adding that the committee “has gained greater confidence that inflation is moving sustainably toward 2 percent.”

Of note:

The Fed policy meeting marked the first dissent from a board member in more than two years. Michelle Bowman, a Trump-appointed governor who focuses on community banking issues, preferred to cut by only a quarter point.

Bowman’s dissent is also the first by a member of the Fed’s seven-member Board of Governors — as opposed to a regional Fed bank president — since 2005.

Christopher Waller, the other Trump-appointed governor on the board, supported the action.

By the numbers:

The median official saw inflation for the full year coming in at 2.3%, not far from the Fed’s 2% target. By contrast, in June, officials saw 2.6% inflation this year.

They also anticipate slightly higher unemployment. The projections listed a 4.4% unemployment rate in the final quarter of the year. That rate was 4.2% in August, up from 3.7% at the start of the year.

However, the Fed officials’ forecasts also imply the jobless rate leveling out at that point and being flat at 4.4% in the final months of 2025.

The bottom line:

Powell and his colleagues elected to take more aggressive action Wednesday in hopes that it will be enough to forestall any further deterioration in the job market of the sort seen over the last few months — and is betting that the Fed can move to a more gradualist approach from here.

Speaking about the larger-than-anticipated rate cut, Powell said he was pleased the Fed made a strong start in lowering interest rates.

“The logic of this — both from an economic standpoint and also from a risk management standpoint — was clear,” Powell said.

He added: “We’re gonna take it meeting by meeting. … There’s no sense that the committee feels it’s in a rush to do this.”