Cartoon – Optimism is Tricky

Amazon Care, which contracts with employers, will now deliver its virtual care services nationwide. It also plans to expand its hybrid service offering—in which care is delivered by nurses dispatched to employees’ homes—to more than 20 new cities this year, including San Francisco, Miami, Chicago, and New York City. The company also announced it has secured new contracts with its subsidiary Whole Foods Market, as well as Hilton Hotels, semiconductor manufacturing company Silicon Labs, and staffing and recruiting firm TrueBlue.

The Gist: Amazon Care is looking to differentiate itself with a virtual-first, asset-light, hybrid service offering. But given the slow-moving and complex nature of employee health benefit contracting, Amazon’s recent moves could displace employer-facing point solutions, but present less of a threat to incumbent providers, instead offering a partnership opportunity for downstream care.

Ultimately, Amazon could combine its care delivery offerings with its pharmacy and diagnostics businesses to launch a robust direct-to-consumer offering—should the company find healthcare a lucrative and manageable market.

CVS Health announced it has struck a deal with Medable, a decentralized clinical trial software company, incorporating its offerings into MinuteClinics to help reach more patients for late-stage clinical trials. With over 40 percent of Americans living near a CVS pharmacy, CVS says it can help gather data and manage patients at MinuteClinic locations, and through its home infusion service, Coram. CVS has already cut its teeth in the clinical research space by conducting COVID-19 vaccine and treatment trials and testing home dialysis machines, and said it plans to engage 10M patients and open up to 150 community research sites this year.

The Gist: With this deal, CVS Health joins companies like Verily, Alphabet’s life sciences subsidiary, in taking advantage of patient appetite for clinical trials without regularly traveling to a research center, which became difficult during the pandemic.

Clinical research is a $50B market that has largely revolved around academic medical centers in large urban areas, which could see their dominance of the research business challenged. CVS’s entry into this space could lower the barriers to entry for community health systems to expand into clinical research.

Ultimately, the decentralization of the clinical trials business is a win for patients, especially groups that have historically been under-represented in medical research, including rural and lower-income individuals. They may find participation through a local pharmacy—or even completely virtually from the comfort of their own home—much more accessible, affordable, and convenient.

A brainstorming session with the CEO of a digital health startup this week highlighted a frustration familiar to anyone who’s tried to make innovation happen in the slow-moving world of health systems.

Meeting with a system executive team to discuss a new approach to virtual care delivery, he described the cross-enterprise collaboration required, and said, “You could see everyone looking around the table to see what everyone else thought, before anyone was willing to react.”

No surprise, as complex bureaucracies don’t reward risk-taking by leaders; often, innovation is slowly suffocated by internal politics and turf-protecting behavior.

That’s why we often repeat advice from one of the most progressive, successful system CEOs we’ve worked with: “You’ve got to eliminate the vetoes if you want to get stuff done. I don’t let people leave the room until we’ve managed to set aside all the reflexive objections and arrive at a resolution.

I expect leaders to be solution-driven, not objection-driven.” For all the times we’ve been asked how to build a successful “innovation infrastructure,” it strikes us often the answer lies in leadership, not org charts.

Last week, we examined how the fast-growing Medicare Advantage (MA) market remains heavily concentrated among a handful of large carriers. But amid this concentration, consumers have more options than ever before, both in terms of carriers and plans, as shown in the graphic below.

The average MA enrollee can now choose from among 39 health plans offered by nine different payers, the majority of which feature $0 insurance premiums. An increasing number of plans also now offer a variety of non-medical benefits.

Landing an MA consumer soon after they become eligible is critical for carriers, as more than seven in 10 Medicare beneficiaries stick with the plan they have year after year. While this “stickiness” may suggest enrollees are satisfied with their current coverage, it also calls into question whether the MA marketplace is actually working as intended.

With another revenue boost to MA plans proposed for 2023, competition between plans—as well as consolidation among carriers—will continue to heat up, especially as the number of Medicare-eligible Americans will increase by nearly 50 percent over the next three decades.

A commentary piece in Health Affairs argues that CMS’s value-based payment (VBP) initiatives have not reached their full potential because they fail to take into account conflicting market dynamics.

The authors argue that VBP models won’t take hold unless CMS both increases the “carrots”, or positive incentives, that market dominant providers receive to support true care transformation, and sharpens the “sticks” by requiring participation in accountable care organization (ACO) models, decreasing the attractiveness of fee-for-service (FFS) payments, and banning anti-competitive commercial deals that discourage steering referrals toward lower-cost providers.

The Gist: To date, CMS’s VBP efforts have largely fallen short of their two primary objectives: transforming care at scale across the country, and generating meaningful savings for the federal government.

With more and more seniors choosing Medicare Advantage (MA) each year, the federal government clearly views MA as the primary vehicle to control Medicare cost growth in the future—although savings will ultimately hinge on CMS cutting payments to insurers in the future.

Over time, continuing to foster the growth of MA may prove more successful than overcoming the myriad complications of FFS-based VBP programs.

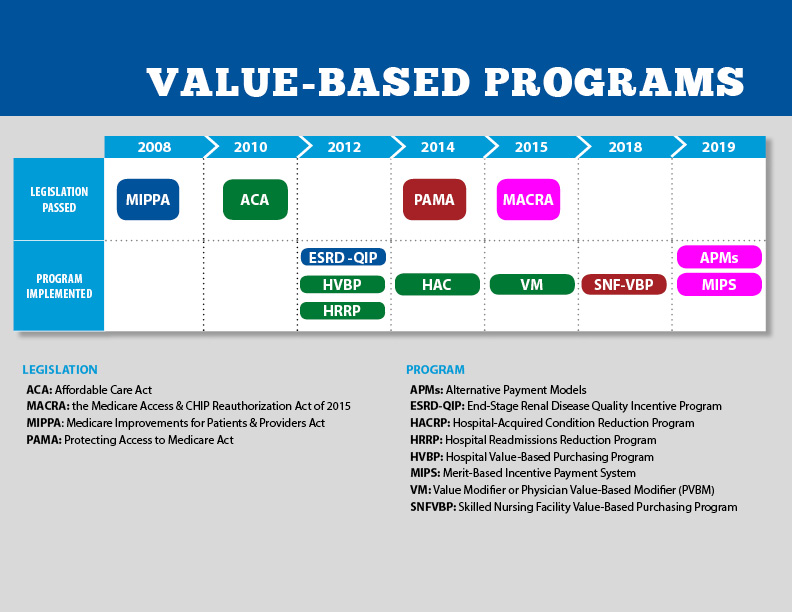

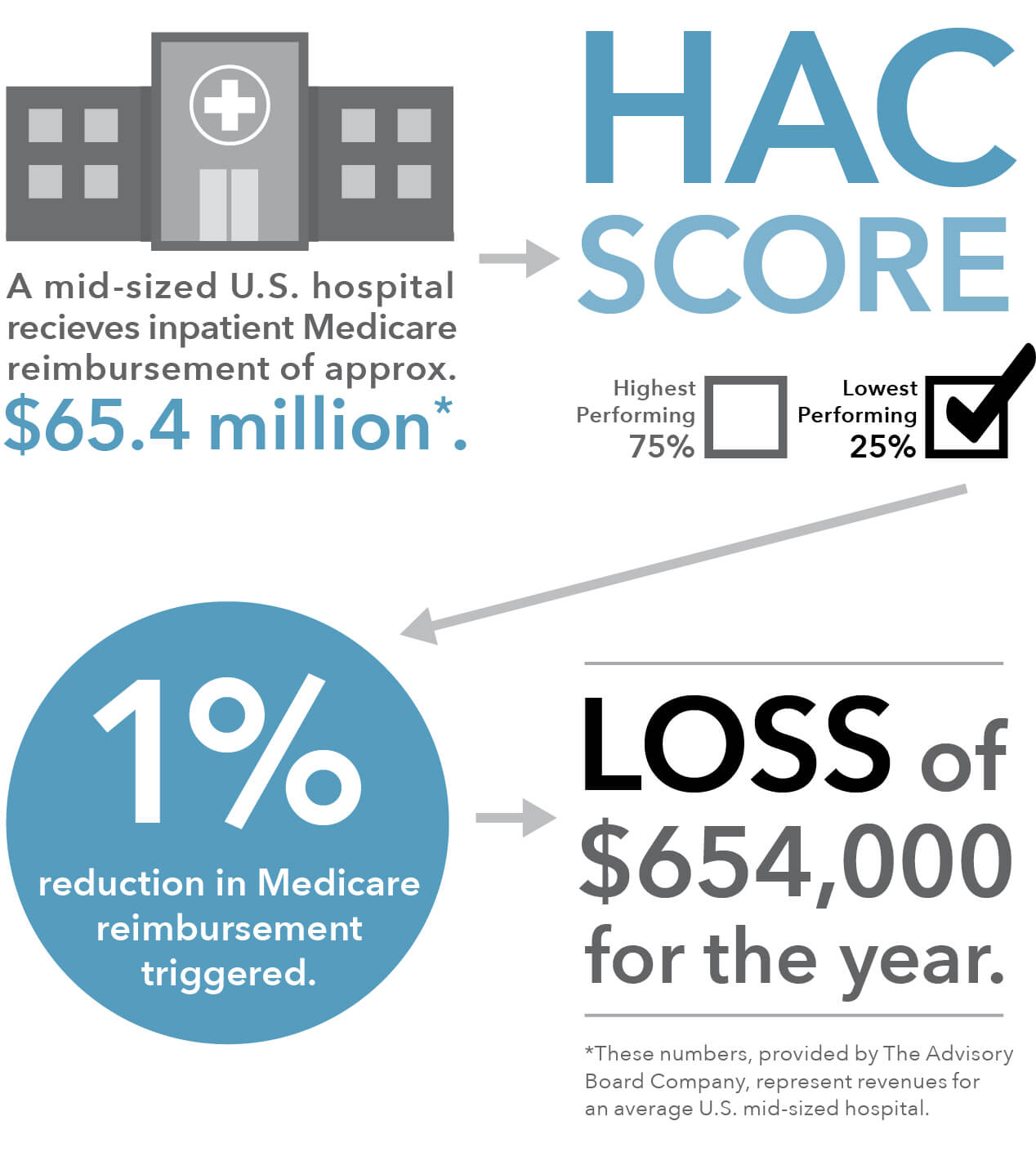

Of the 764 hospitals the Centers for Medicare and Medicaid Services (CMS) is penalizing this year with a one percent reduction in Medicare payments for scoring in the bottom quartile in the Hospital-Acquired Condition Reduction (HAC) Program, 38 also earned a five-star rating from CMS for overall quality of care.

This paradox is in part because Medicare’s star ratings compare a hospital’s safety and quality to a calculated average, whereas the HAC program requires Medicare to penalize the lowest-performing quartile of hospitals each year, even if they are showing improvement, or if the difference between low- and high-performing hospitals is miniscule.

The Gist: The promise of Medicare’s pay-for-performance incentive programs has not materialized, and is unlikely to be driving true clinical improvement. In addition to being confusing and tedious to comply with, the programs lack impact because penalties and rewards are too small to impact a hospital’s bottom line—the benefits don’t justify the costs of redesigning care processes or changing behavior. With years of evidence that many of these ACA-era quality programs aren’t producing the desired results, it’s time to find more effective ways of improving patient outcomes.