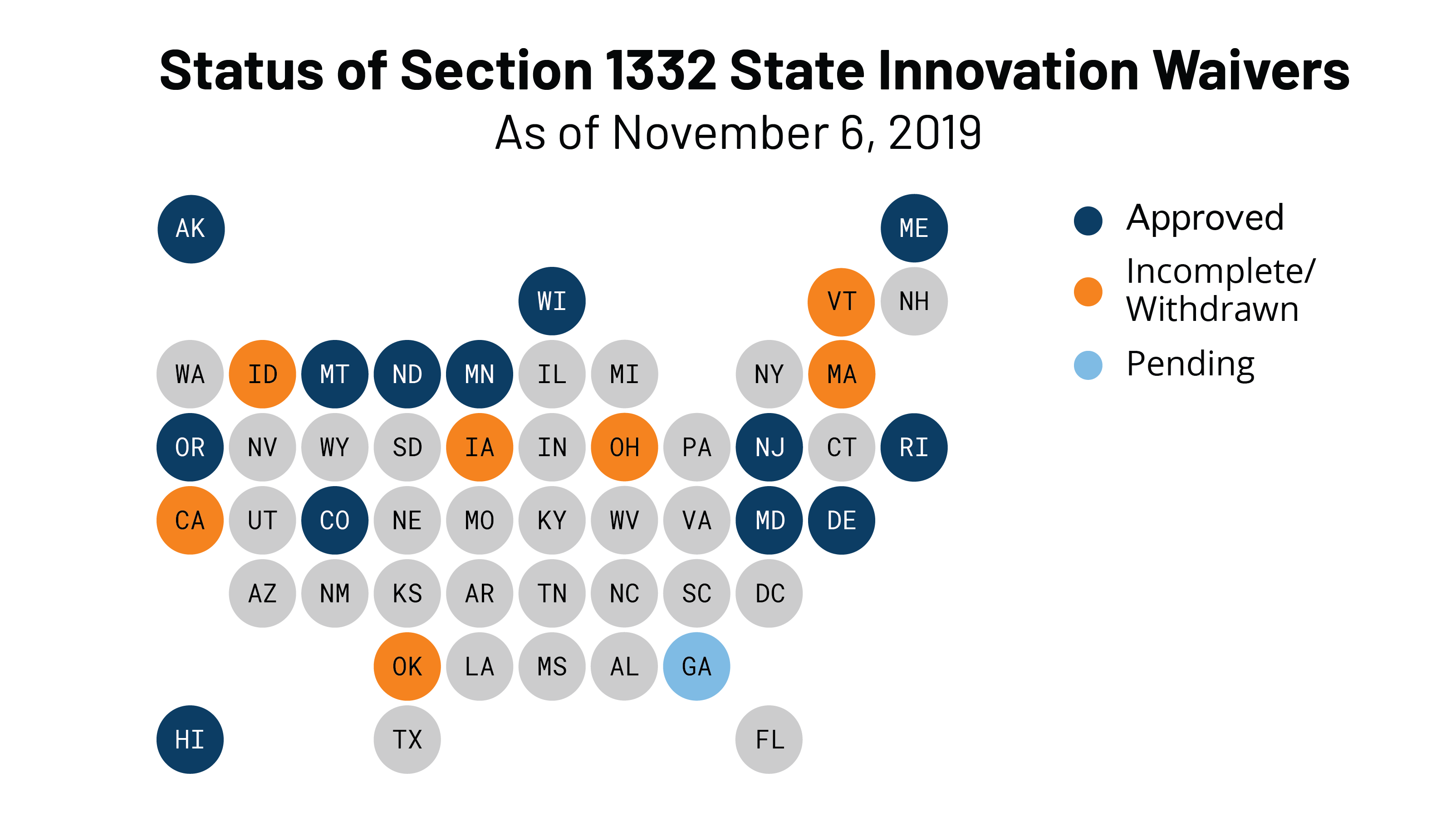

States with 1332 reinsurance waivers will have more pass-through funding to implement the waivers.

The Centers for Medicare and Medicaid Services and the Biden Administration have earmarked $452 million in federal funding through the American Rescue Plan for efforts to lower costs and improve health insurance access in 13 states.

Due to the changes made to the ARP, states with 1332 reinsurance waivers will have more pass-through funding to implement the waivers, and may also have their own state funding available to pursue further strategies to promote insurance affordability.

This funding, said CMS, might otherwise have been spent on 2021 reinsurance costs.

The “pass-through funding” is determined on an annual basis by the Department of Health and Human Services and the Department of the Treasury. They’re available to states with approved section 1332 waivers that have also lowered premiums to implement their waiver plans.

WHAT’S THE IMPACT?

State-based reinsurance programs created through section 1332 waivers are designed to improve health insurance affordability and market stability by reimbursing issuers for a portion of healthcare provider claims that would otherwise be paid by some consumers and by the federal government through higher premiums.

As a result, said CMS, these programs hold the potential to lower premiums for consumers with individual health insurance coverage, and may increase access to coverage and provide more health plan options for people in those reinsurance states, without increasing net federal costs.

The additional funds announced by CMS range from $2.5 million to $139 million per state – varying based on factors such as the size of the state’s reinsurance program. The funds are the result of expanded subsidies provided under the ARP, which will result in new people enrolled, and will cover a portion of the states’ costs for these reinsurance programs.

States with approved section 1332 state-based reinsurance waivers have experienced reduced premiums in the individual market, CMS said. Overall, from plan years 2018 to 2021, states that have implemented section 1332 state-based reinsurance waivers for the individual market have seen statewide average premium reductions ranging from 3.75% to 41.17%, compared to premiums absent the waiver, according to the agency’s internal data.

For example, in 2021, statewide average premium reductions due to the waiver were 4.92% in Pennsylvania, 18.47% in Colorado, and 34% in Maryland, compared to a scenario with no waiver in place.

Beyond reduced premiums, it’s expected that section 1332 state-based reinsurance waivers may help states maintain and increase issuer participation, and may increase the number of qualified health plans available in each county in such states from year to year. For example, states like Colorado, Wisconsin, Alaska and Maryland have seen additional issuers enter or re-enter the individual marketplace since their state reinsurance programs have been implemented.

The agency’s current thinking is that stronger issuer participation in the individual market may increase competition and translate to consumers having more opportunities to obtain affordable health insurance coverage. Nationally, on average, there are more QHP offerings in 2021 than in 2020, and in states with section 1332 state-based reinsurance waivers, the average number of QHPs weighted by enrollment increased by 30.6% from 2020 to 2021.

The states, and their pass-through funding amounts, include Alaska ($43,827,328), Colorado ($49,892,498), Delaware ($10,821,203), Maine ($8,562,238), Maryland ($139,159,548), Minnesota ($64,969,985), Montana ($7,129,995), New Hampshire ($8,820,847), North Dakota ($5,798,044), Oregon ($18,948,114), Pennsylvania ($28,558,672), Rhode Island ($2,590,540) and Wisconsin ($63,408,562). New Jersey’s pass-through funding amount will be announced at a later time.

THE LARGER TREND

In April 2021, the departments announced a total of $1.29 billion in pass-through funding for the 2021 plan year and posted a FAQ that noted that the departments would inform states of additional pass-through to account for the ARP.

ON THE RECORD

“This investment is a testament to our administration-wide commitment to making healthcare more accessible and affordable,” said HHS Secretary Xavier Becerra. “This funding from the American Rescue Plan will reduce monthly healthcare costs for consumers, increase coverage, and provide more options. We will continue to work with states to strengthen the healthcare system as we respond to the COVID-19 pandemic.”

“Reducing a family or individual’s average monthly health coverage costs frees up that money for other needs,” said CMS Administrator Chiquita Brooks-LaSure. “The Biden-Harris Administration continues to work with states to reduce costs and deliver more affordable health coverage options. This is another example of how the American Rescue Plan is helping more people meet their healthcare needs.”