Published this week in the Washington Post, this unsparing article packages a year of investigative reporting into a thorough accounting of why US life expectancy is undergoing a rapid decline.

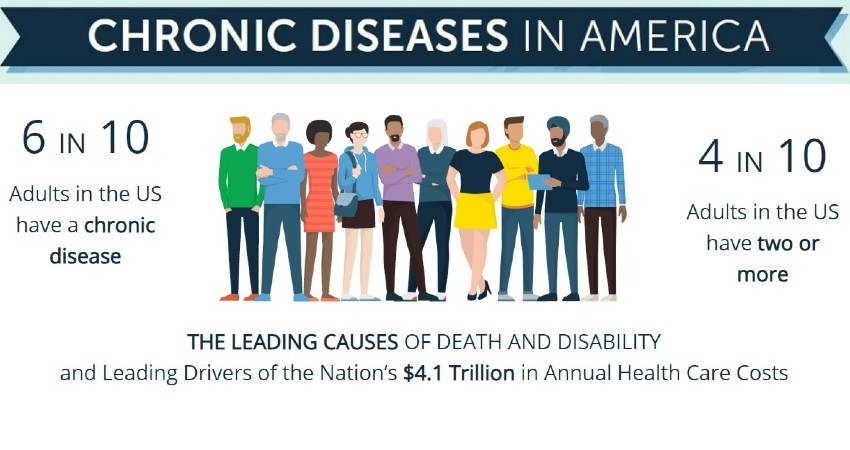

After peaking in 2014, US life expectancy has declined each subsequent year, trending far worse than peer countries. In a quarter of US counties, working-age Americans are dying at the highest rates in 40 years, reversing decades of progress. While deaths from firearms and opioids play a role, chronic diseases remain our nation’s greatest killer, erasing more than double the years of life as all overdoses, homicides, suicides, and car accidents combined.

The drivers of this trend are too numerous to list, but experts suggest targeting “the causes of the causes”, namely social factors, as the death rate gap between the rich and poor has grown almost 15x faster than the income gap since 1980.

The Gist: This reporting is a sobering reminder of the responsibilities—and failures—borne by our nation’s healthcare system.

The massive death toll of chronic disease in this country is not an indictment of the care Americans receive, but of the care and other resources they cannot access or afford.

While it’s not the mandate of health systems to reduce systemic issues like poverty, there is no solution to the problem without health systems playing a key role in increasing access to care, while convening community resources in service of these larger goals.

On Tuesday, the White House issued a proposal to enhance the 2008 Mental Health Parity and Addiction Equity Act, which requires insurers to cover mental healthcare at the same level as physical care.

Health plans would be required to evaluate mental health coverage policies, including network size, prior authorization rules, and out-of-network payment policies.

The proposal also includes closing a loophole in the original law that excludes non-federal government health plans from these parity standards.

The Gist: Fewer than half of the one in five US adults experiencing mental illness in 2020 received care for their illness, and fewer than one in 10 received treatment for a substance abuse disorder.

But while insurance companies’ failure to establish adequate mental health networks is part of the problem, there are other, larger access issues at play, including the nationwide shortage of mental health clinicians, many of whom don’t accept insurance.

A report from the Center for Healthcare Quality and Payment Reform (CHQPR) found that over 600 rural hospitals are at risk of closing in 2023, citing persistent financial challenges related to patient services or depleted financial resources.

More than 600 rural hospitals are at risk of closing in 2023

In the report, which was released in January, CHQPR identified 631 rural hospitals — over 29% nationwide — at risk of closing in 2023. However, compared to pre-pandemic levels, fewer rural hospitals are at immediate risk of closing because of the federal relief they received during the pandemic.

Among rural hospitals at risk of closing, CHQPR found two common contributing factors. First, these hospitals reported persistent financial losses of patient services over a multi-year period, excluding the first year of the COVID-19 pandemic. Second, these hospitals reported low financial reserves, with insufficient net assets to counter losses on patient services over a period of more than six years.

In most states, at least 25% of the rural hospitals are at risk of closing, and in 12 states, 40% or more are at risk.

Meanwhile, more than 200 of these rural hospitals are facing an immediate risk of closing. According to CHQPR, these hospitals have inadequate revenues to cover expenses and very low financial reserves.

“Costs have been increasing significantly and payments, particularly from commercial insurance plans, have not increased correspondingly with that,” said Harold Miller, president and CEO of CHQPR. “And the small hospitals don’t have the kinds of financial reserves to be able to cover the losses.”

How rural hospital closures impact communities

In many cases, the closure of a rural hospital leads to a loss of access to comprehensive medical care in a community. Most of the at-risk hospitals are in areas where closure would result in community residents being forced to travel a long distance for emergency or inpatient care.

“In many of the smallest rural communities, the only thing there is the hospital,” Miller said. “The hospital is the only source. Not only is it the only emergency department and the only source of inpatient care, it’s the only source of laboratory services, the only place to get an X-ray or radiology. It may even be the only place where there is primary care.”

Many small hospitals also run health clinics. “There literally wouldn’t be any physicians in the community at all if it wasn’t for the rural hospital running that rural health clinic,” Miller said. “So if the hospital closes, you’re literally eliminating all health care services in the community.”

According to Miller, there has to be a fundamental change in the way hospitals are paid. “The problem that hospitals have faced though, is that they do two fundamentally different things — but they are only paid for one of them,” Miller said.

“Hospitals deliver services to patients when they are sick, and they are paid for that. But the other thing that hospitals do, which is essential for a community, is that they are available when somebody needs them — that standby capacity is critical for a community. But hospitals aren’t paid for that,” he added. (Higgs, Cleveland.com, 3/16; CHQPR report, accessed 3/20)

Advisory Board’s take

Why it is ‘not enough’ to simply stave off hospital closures

Hospital closures are a big deal — for all the reasons outlined above (and more) — but we cannot understate the importance of monitoring hospitals that are in or moving into the “at risk” category.

When hospitals fall into the “at risk” category, they are more likely to cut services to reduce costs. While this may help preserve hospital survival, it can have a devastating effect on patient access. For instance, a 2019 Health Affairsstudy found that rural hospital closures are associated with an 8% annual decrease in the supply of general surgeons in the years preceding closure.

While dangerous trends persist in maternal mortality, especially among Black women, obstetrics (OB) care is often placed on the chopping block for hospitals looking to rationalize services and stave off closure. According to the American Hospital Association (AHA), nearly 90 rural community hospitals closed OB units between 2015-2019. As of 2020, only 53% of rural community hospitals offered OB services, AHA reports.

Ultimately, these service closures carry massive implications for patient access and outcomes. As care delays result in higher-acuity downstream presentation, they can also increase the strain on the rest of the healthcare system.

So, yes, we need to stave off hospital closures. But to say “that’s not enough” is a massive understatement. In fact, many of the strategies hospitals deploy to stave off closure can create gaps that stakeholders must work together to fill.

This is especially true as we near the end of the COVID-19 public health emergency. As Medicaid redeterminations start ramping up, rural hospitals may see an increase in bad debt, especially among states that have not expanded Medicaid.

For example, the Alabama Rural Health Association reported that 55 of 67 counties in Alabama are considered rural, and CHQPR reported that 48% of rural hospitals in the state are at risk of closing. Meanwhile, the Wyoming Department of Health reported that 17 of 23 counties in the state are considered “Frontier,” which means there are fewer than six residents per square mile, and CHQPR reported that 29% of the state’s rural hospitals are at risk of closure.

When rural hospitals close their doors, the surrounding communities are left without access to timely, quality health care.

There is no silver bullet here — but Advisory Board researchers have created several resources to help stakeholders understand how to support rural hospitals:

Rural providers aren’t providing “rural healthcare” — they’re providing healthcare in a rural setting. While niche policies can help in pockets, rural providers need federal policymakers to consider rural needs in overall health policy to meet the magnitude of the crisis.

Healthcare leaders now need to strike a delicate balance that requires managing financial and growth metrics, increasing the speed of transformation, and building the health systems of tomorrow. So how do we redefine compensation models to reward all these behaviors?

Executive compensation might not spring to mind as a key driver of healthcare transformation, nor does it seem naturally connected to critical issues such as health equity, patient safety, or quality of care – just a few of the areas where significant changes can be made to transform healthcare. But, in fact, executives leading not-for-profit health systems today are tasked with delivering measurable results that improve the health status of their patients and their communities. And to ensure that these new performance metrics are met, we must change how we think about —and deliver—compensation.

Defining a new model

While executive compensation has always been tied to specific objectives, they have historically leaned heavily toward financial performance, volume and margins, with a modest portion of compensation aligned to quality of care and patient outcomes. But transformative approaches such as population health, value-based care, patient wellness and health outcomes are shifting the mark.

Healthcare leaders now need to strike a delicate balance that requires managing financial and growth metrics, increasing the speed of transformation, and building the health systems of tomorrow. So how do we redefine compensation models to reward all these behaviors?

Some might say that the answer lies in adjusting incentive plans. While incentive plans across health care have not changed significantly in the past decade, the sophistication of the plans has changed, reflecting greater attention to delivering a better patient experience. But delivering better experiences does not imply that health systems have transformed from the top down. In my mind, adjusting incentive plans only solves part of the problem.

If we want true health care transformation—and we should, in order to best serve patients and communities—health systems need to re-evaluate the outcomes for each stakeholder and create incentives to evolve leadership as a whole. We need to rethink executive compensation models to align with value-based care, patient experience, and the resulting outcomes, along with traditional performance measurements.

Leading through lingering disruption

But rethinking executive compensation models won’t be an easy task, especially given the external challenges and changes thrust upon the health care system over the last few years.

As with nearly every other aspect of health care, pay for performance was disrupted during the pandemic. Demand for health services changed dramatically, labor and attrition issues intensified, and supply chain problems and operational costs increased. These new pressures required executives to manage through long periods of uncertainty where meeting operational pay-for-performance goals was nearly impossible. Fast-forward to today, the executive talent market remains extraordinarily competitive. Demand outpaces supply due to higher-than-typical retirements, effects of the great resignation, the need for new skill sets and overall burnout.

As a result, there has been upward pressure on compensation to address and fulfill unexpected but immediate needs such as rewarding executives for managing in a unique and challenging performance environment, increasing efforts to recruit and retain, and recognizing leaders for their hard-won accomplishments.

Considerations and changes

When considering adjusting models for 2023 and beyond, CEOs and compensation committees need to take these pressures and disruptions into account. They should look closely at their own compensation data from the past two years – not as a lighthouse for future compensation, but as data that may need to be set aside due to the volume of performance goals and achievements that were up-ended by the pandemic. When relying on external industry data, the same rules apply; smaller data sets or those that don’t account for the past two years may be misleading, so review carefully before using limited data sets to inform adjusted models.

Just as important, CEOs and compensation committees should consider new performance measurements tied to both financial and quality or value-based transformation metrics. We don’t need to eliminate traditional financial and operational goals because viability is still a business mandate. But how can we articulate compensation-driven KPIs for stewardship of patient and community health, improved outcomes and reduced cost of care? Too many measures are akin to having no measures at all.

The compensation mix should take into account a more focused approach to long-term measures. The old paradigm of 12-month incentive cycles is not enough to address the time required to truly transform health care. Another consideration should be performance-based funding of deferred compensation based on achieving transformation goals, and greater use of retention programs to support the maintenance of a stable executive team during the transformation period. Covid-19 proved how crisis can be an accelerator for change. True transformation should blend the skills gained from crisis management with planful, thoughtful and intentional change.

In addition, some metrics may need to incorporate a discretionary component, considering ongoing disruption within the workforce, supply chain limitations, and energy, equipment and labor cost increases. More organizations are also including health equity, DE&I, and ESG goals in incentive programs to tighten alignment with mission-critical board-mandated goals.

Transformative change

There are four elements that are vital in the journey to transform health care from “heads in beds” to the public-service-oriented organizations that they were meant to be—and can be again. With mounting pressure from patients, communities, and payers to boards and employees, CEOs and compensation committees must become key drivers of change, setting the right goals and incentives from the top down.

Affordability: can patients afford the care they need?

Quality: is the care being delivered of the utmost quality?

Usability: how can we reduce hurdles to undertaking the care plan?

Access: are all community members able to access needed care?

Solving for each of these elements is one of the biggest challenges we face, and as we begin to emerge from the disruption of the pandemic, leaders will be watched closely to ensure that they deliver—and can clearly show the path to delivery.

Ideally, end achievements would include patients spending less to achieve better health; payers controlling costs and reducing risk; providers realizing efficiencies and greater patient satisfaction; and alignment of medical supplier pricing to patient outcomes. And when you zoom out to reveal the bigger picture, all of these pieces come together to achieve healthier populations and lower overall health care costs, while still meeting the financial goals of the organization.

We’re asking a lot of already-overburdened health care executives. Stakeholders must prove that we value leaders with the right mindset and skillset in order to attract executives who can shepherd organizations through the transformation journey. This requires a setting where there is supportive leadership, a compelling mission and opportunity for personal growth and development. It will not be easy, but without rethinking how we design compensation models from the top down, it will be unnecessarily challenging.

This week’s contributor is Paula Chatterjee, a physician and assistant professor at the Perelman School of Medicine at the University of Pennsylvania. Her research focuses on improving the health of low-income patients and evaluating policies related to safety-net health care delivery and financing.

Low-income patients face many barriers to care, one of which is the high cost of prescription medications. The 340B program lets certain hospitals and clinics (like federally qualified health centers) receive discounts on outpatient medications. They can then use those savings to provide medication and additional care for little to no charge to low-income patients. However, policymakers and other stakeholders have raised concerns that the 340B program might not be reaching the patients it was designed to support.

A recent paper in the American Journal of Managed Care by Sayeh Nikpay*, Gabriela Garcia, Hannah Geressu and Rena Conti sheds light on one of the latest examples of 340B mistargeting: so-called contract pharmacies. These are retail pharmacies that fill 340B prescriptions and split the savings with the hospital or clinic. These relationships have been on the rise, with hospitals and clinics arguing they make it more convenient for patients to get their prescriptions. Given their growth, the authors looked at whether contract pharmacies were more likely to open up in areas where low-income and uninsured people live.

They found the pattern was different for pharmacies contracting with 340B clinics vs. 340B hospitals:

The number of counties with a pharmacy contracted with a 340B clinic grew from 20.8% to 64.8% over the past decade. Counties with higher poverty rates were more likely to gain a clinic-contracted pharmacy.

The number of counties with hospital-contracted pharmacies grew much more (from 3.2% to 76.3%), but those counties had fewer uninsured residents and were less likely to be medically underserved.

The researchers acknowledge that counties may be an imperfect geographical area to represent a pharmacy’s market and that they were unable to collect information on how many (if any) 340B prescriptions a pharmacy actually filled.

Nonetheless, their results reveal a mismatch between where the 340B program is growing and where low-income patients live, especially for pharmacies contracting with 340B hospitals. The authors argue that any 340B policy changes should take these differences between hospitals and clinics into account.

Despite decades of policies designed to bolster the safety-net, it remains perennially reliant on a patchwork of subsidies that are often mistargeted.

This study adds to a growing body of work highlighting the opportunity to improve the 340B program so that it achieves its intended goal of improving access for low-income patients.

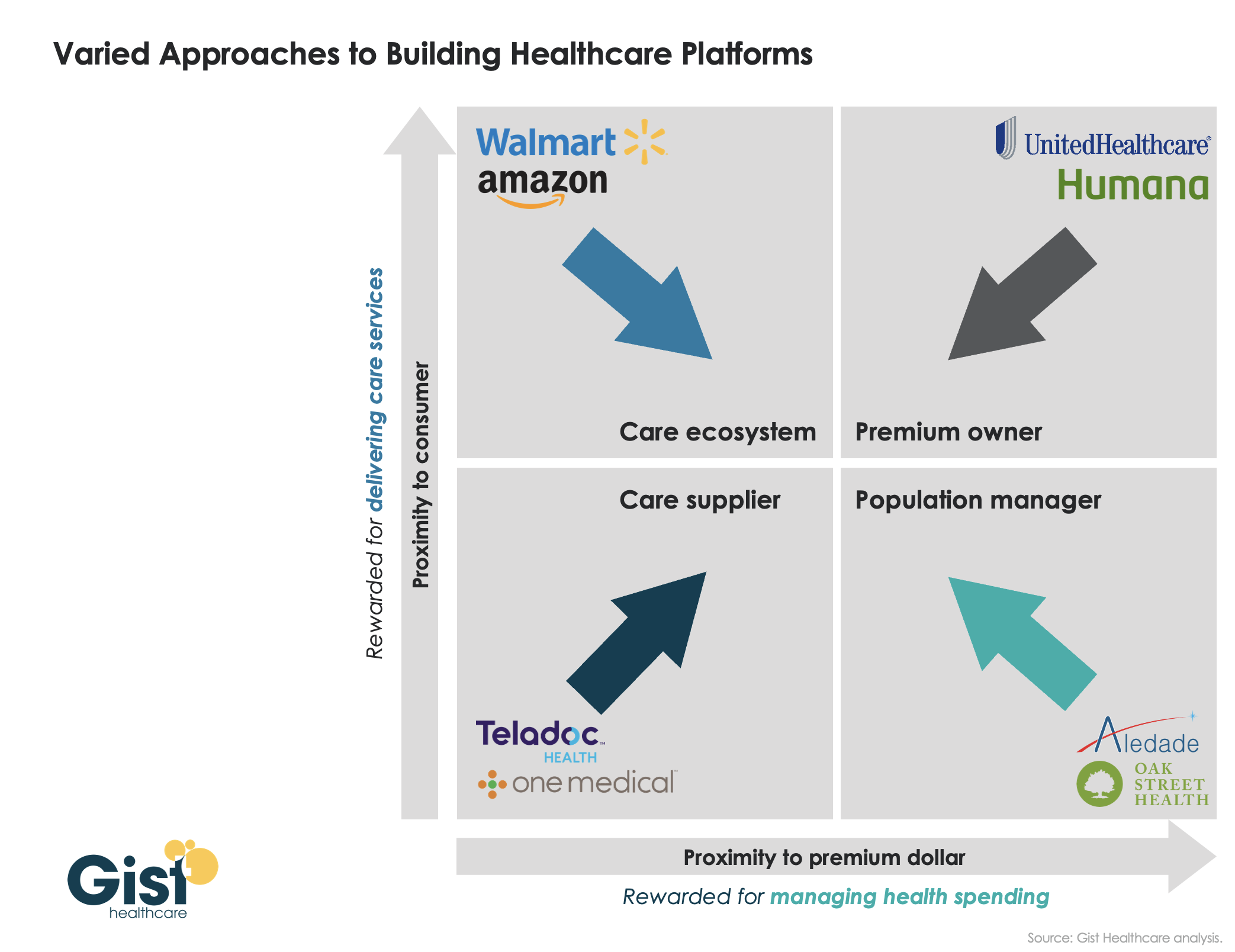

Last week, we introduced our framework for value delivery as a “healthcare platform”, in which an organization’s proximity to both the consumer and to the premium dollar determines how it competes as a “care supplier,” a “care ecosystem,” a “premium owner,” or a “population manager.” Traditionally, different healthcare companies have operated primarily in one of these four domains. However, as shown in the graphic below, we’ve recently seen many shift their business into one or more additional quadrants, as they seek to expand their value propositions. UnitedHealth Group is an obvious example: it has moved well beyond the traditional insurance business, via numerous provider and care delivery acquisitions across the continuum.

Other players have shifted from their own “pure play” positions toward more comprehensive “platform” strategies as well: One Medical adding Iora Health to enhance population health capabilities; Walmart moving beyond retail and pharmacy services, partnering with Oak Street Health to expand its ability to manage Medicare patients; Amazon getting into the employer health business.

There’s a clear pattern emerging—value propositions are converging on a “strategic high ground” that encompasses all four dimensions of platform value, creating a comprehensive set of solutions to deliver accessible care, promote health, and grow consumer loyalty, with an aligned financial model centered on managing the total cost of care. Health systems looking to build platform strategies will find many of these competitors also vying for pride of place as the “platform of choice” for healthcare consumers and purchasers.