The recent assassination of the CEO of UnitedHealthcare — the health insurance company with, reportedly, the highest rate of claims rejections (and thus dead, wounded, and furious customers and their relations) — gives us a perfect window to understand the stupidity and danger of the Musk/Trump/Ramaswamy strategy of “cutting government” to “make it more efficient, run it like a corporation.”

Consider health care, which in almost every other developed country in the world is legally part of the commons — the infrastructure of the nation, like our roads, public schools, parks, police, military, libraries, and fire departments — owned by the people collectively and run for the sole purpose of meeting a basic human need.

The entire idea of government — dating all the way back to Gilgamesh and before — is to fulfill that singular purpose of meeting citizens’ needs and keeping the nation strong and healthy. That’s a very different mandate from that of a corporation, which is solely directed (some argue by law) to generate profits.

The Veterans’ Administration healthcare system, for example, is essentially socialist rather than capitalist. The VA owns the land and buildings, pays the salaries of everybody from the surgeons to the janitors, and makes most all decisions about care. Its primary purpose — just like that of the healthcare systems of every other democracy in the world — is to keep and make veterans healthy. Its operation is nearly identical to that of Britain’s beloved socialist National Health Service.

UnitedHealthcare similarly owns its own land and buildings, and its officers and employees behave in a way that’s aligned with the company’s primary purpose, but that purpose is to make a profit. Sure, it writes checks for healthcare that’s then delivered to people, but that’s just the way UnitedHealthcare makes money; writing checks and, most importantly, refusing to write checks.

Think about it. If UnitedHealthcare’s main goal was to keep people healthy, they wouldn’t be rejecting 32 percent of claims presented to them. Like the VA, when people needed help they’d make sure they got it.

Instead, they make damn sure their executives get millions of dollars every year (and investors get billions) because making a massive profit ($23 billion last year, and nearly every penny arguably came from saying “no” to somebody’s healthcare needs) is their real business.

On the other hand, if the VA’s goal was to make or save money by “being run efficiently like a company,” they’d be refusing service to a lot more veterans (which it appears is on the horizon).

This is the essential difference between government and business, between meeting human needs (social) and reaching capitalism’s goal (profit).

It’s why its deeply idiotic to say, as Republicans have been doing since the Reagan Revolution, that “government should be run like a business.” That’s nearly as crackbrained a suggestion as saying that fire departments should make a profit (a doltish notion promoted by some Libertarians). Government should be run like a government, and companies should be run like companies.

Given how obvious this is with even a little bit of thought, where did this imbecilic idea that government should run like a business come from?

Turns out, it’s been driven for most of the past century by morbidly rich businessmen (almost entirely men) who don’t want to pay their taxes. As Jeff Tiedrich notes:

“The scariest sentence in the English language is: ‘I’m a billionaire, and I’m here to help.’”

Rightwing billionaires who don’t want to pay their fair share of the costs of society set up think tanks, policy centers, and built media operations to promote their idea that the commons are really there for them to plunder under the rubric of privatization and efficiency.

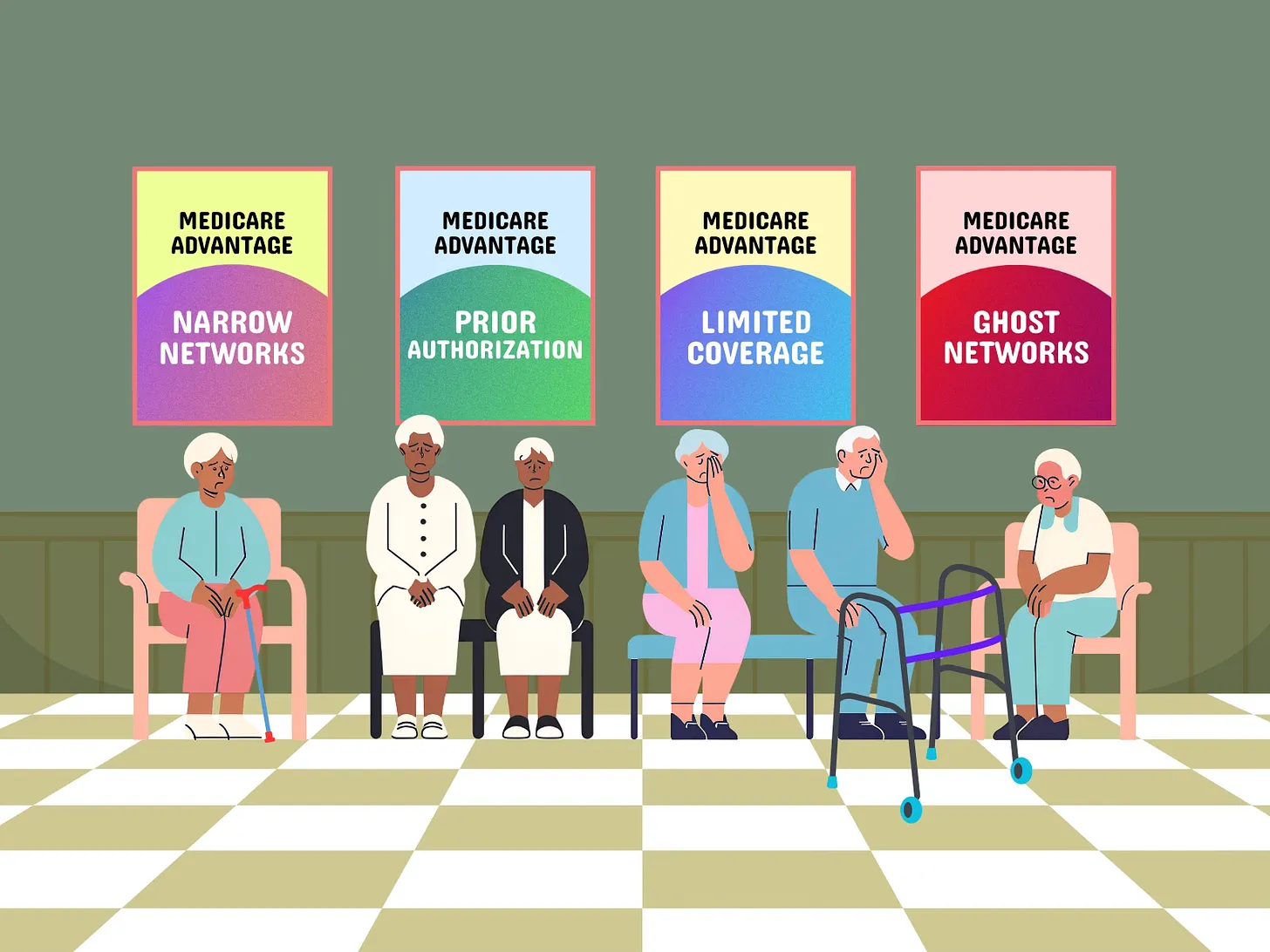

They’ve had considerable success. Slightly more than half of Medicare is now privatized, multiple Republican-controlled states are in the process of privatizing their public school systems, and the billionaire-funded Project 2025 and the incoming Trump administration have big plans for privatizing other essential government services.

The area where their success is most visible, though, is the American healthcare system. Because the desire of rightwing billionaires not to pay taxes have prevailed ever since Harry Truman first proposed single-payer healthcare like most of the rest of the world has, Americans spend significantly more on healthcare than other developed countries.

In 2022, citizens of the United States spent an estimated $12,742 per person on healthcare, the highest among wealthy nations. This is nearly twice the average of $6,850 per person for other wealthy OECD countries.

Over the next decade, it is estimated that America will spend between $55 and $60 trillion on healthcare if nothing changes and we continue to cut giant corporations in for a large slice of our healthcare money.

On the other hand, Senator Bernie Sanders’ single-payer Medicare For All plan would only cost $32 trillion over the next 10 years. And it would cover everybody in America, every man woman and child, in every medical aspect including vision, dental, psychological, and hearing.

Currently 25 million Americans have no health insurance whatsoever.

If we keep our current system, the difference between it and the savings from a single-payer system will end up in the pockets, in large part, of massive insurance giants and their executives and investors. And as campaign contributions for bought off Republicans. This isn’t rocket science.

And you’d think that giving all those extra billions to companies like UnitedHealthcare would result in America having great health outcomes. But, no.

Despite insanely higher spending, the U.S. has a lower life expectancy at birth, higher rates of chronic diseases, higher rates of avoidable or treatable deaths, and higher maternal and infant mortality rates than any of our peer nations.

Compared to single-payer nations like Canada, the U.S. also has a higher incidence of chronic health conditions, Americans see doctors less often and have fewer hospital stays, and the U.S. has fewer hospital beds and physicians per person.

No other country in the world allows a predatory for-profit industry like this to exist as a primary way of providing healthcare. Every other advanced democracy considers healthcare a right of citizenship, rather than an opportunity for a handful of industry executives to hoard a fortune, buy Swiss chalets, and fly around on private jets.

Sure, there are lots of health insurance companies in other developed countries, but instead of offering basic healthcare (which is provided by the government) mostly wealthy people subscribe to them to pay for premium services like private hospital rooms, international air ambulance services, and cosmetic surgery.

Essentially, UnitedHealthcare’s CEO Brian Thompson made decisions that killed Americans for a living, in exchange for $10 million a year. He and his peers in the industry are probably paid as much as they are because there is an actual shortage of people with business training who are willing to oversee decisions that cause or allow others to die in exchange for millions in annual compensation.

That Americans are well aware of this obscenity explains the gleeful response to his murder that’s spread across social media, including the refusal of online sleuths to participate in finding his killer.

It shouldn’t need be said that vigilantism is no way to respond to toxic individuals and companies that cause Americans to die unnecessarily. Hopefully, Thompson’s murder will spark a conversation about the role of government and the commons — and the very real need to end the corrupt privatization of our healthcare system (including the Medicare Advantage scam) that has harmed so many of us and killed or injured so many of the people we love.