A number of health systems have recently noted increasing financial challenges for Medicare Advantage (MA) patient admissions.

One CFO shared, “our rates from MA plans are roughly on par with fee-for-service Medicare. Denials have always been a problem, making our [revenue] capture about 90 percent. But this year it’s dropped to 80 percent…it’s a crisis for us, given fast how MA volumes are growing.”

His team investigated the change and found the cause: mean length of stay for MA patients has jumped sharply. The rise was almost entirely due to difficulties in discharging patients to rehab and skilled nursing facilities.

Key insurers have narrowed their postacute networks, resulting in patients spending days waiting for a bed. “The payers told us they had focused the network on ‘high-performing’ providers. Our data and doctors’ experiences say otherwise. They chose a handful of facilities that are cheap, with questionable quality,” their CMO reported. Attempts to engage payers to solve the problem have gone nowhere:

“They have a disincentive to work with us on this. With case rates, they are saving money if patients are languishing in an expensive hospital bed rather than going to rehab.”

This system is exploring expedited placement and expanding their portfolio of home-based care and postacute offerings, while even considering guaranteeing payment themselves. If you’re having similar challenges or have found solutions to help with transitions of care, we’d love to hear from you and learn more.

Studies show healthcare affordability is an issue to voters as medical debt soars (KFF) and public disaffection for the “medical system” (per Gallup, Pew) plummets. But does it really matter to the hospitals, insurers, physicians, drug and device manufacturers and army of advisors and trade groups that control the health system?

Each sector talks about affordability blaming inflation, growing demand, oppressive regulation and each other for higher costs and unwanted attention to the issue.

Each play their victim cards in well-orchestrated ad campaigns targeted to state and federal lawmakers whose votes they hope to buy.

Each considers aggregate health spending—projected to increase at 5.4%/year through 2031 vs. 4.6% GDP growth—a value relative to the health and wellbeing of the population. And each thinks its strategies to address affordability are adequate and the public’s concern understandable but ill-informed.

As the House reconvenes this week joining the Senate in negotiating a resolution to the potential federal budget default October 1, the question facing national and state lawmakers is simple: is the juice worth the squeeze?

Is the US health system deserving of its significance as the fastest-growing component of the total US economy (18.3% of total GDP today projected to be 19.6% in 2031), its largest private sector employer and mainstay for private investors?

Does it deserve the legal concessions made to its incumbents vis a vis patent approvals, tax exemptions for hospitals and employers, authorized monopolies and oligopolies that enable its strongest to survive and weaker to disappear?

Does it merit its oversized role, given competing priorities emerging in our society—AI and technology, climate changes, income, public health erosion, education system failure, racial inequity, crime and global tension with China, Russia and others.

In the last 2 weeks, influential Republicans leaders (Burgess, Cassidy) announced plans to tackle health costs and the role AI will play in the future of the system. Last Tuesday, CMS announced its latest pilot program to tackle spending: the States Advancing All-Payer Health Equity Approaches and Development Model (AHEAD Model) is a total cost of care budgeting program to roll out in 8 states starting in 2026. The Presidential campaigns are voicing frustration with the system and the spotlight on its business practices intensifying.

So, is affordability to the federal government likely to get more attention?

Yes. Is affordability on state radars as legislatures juggle funding for Medicaid, public health and other programs?

Yes, but on a program by program, non-system basis.

Is affordability front and center in CMS value agenda including the new models like its AHEAD model announced last week? Not really.

CMS has focused more on pushing hospitals and physicians to participate than engaging consumers. Is affordability for those most threatened—low and middle income households with high deductible insurance, the uninsured and under-insured, those with an expensive medical condition—front of mind? Every minute of every day.

Per CMS, out-of-pocket spending increased 4.3% in 2022 (down from 10.4% in 2021) and “is expected to accelerate to 5.2%, in part related to faster health care price growth. During 2025–31, average out-of-pocket spending growth is projected to be 4.1% per year.” But these data are misleading. It’s dramatically higher for certain populations and even those with attractive employer-sponsored health benefits worry about unexpected household medical bills.

So, affordability is a tricky issue that’s front of mind to 40% of the population today and more tomorrow.

Legislation that limits surprise medical bills, requires drug, hospital and insurer price transparency, expands scope of practice opportunities for mid-level professionals, avails consumers of telehealth services, restricts aggressive patient debt collection policies and others has done little to assuage affordability issues for consumers.

Ditto CMS’ value agenda which is more about reducing Medicare spending through shared savings programs with hospitals and physicians than improving affordability for consumers. That’s why outsiders like Walmart, Best Buy and others see opportunity: they think patients (aka members, enrollees, end users) deserve affordability solutions more than lip service.

Affordability to consumers is the most formidable challenge facing the US healthcare industry–more than burnout, operating margins, reimbursement or alternative payment models. Today, it is not taken seriously by insiders. If it was, evidence would be readily available and compelling. But it’s not.

Last Monday, four U.S. Senators took aim at the tax exemption enjoyed by not-for-profit (NFP) hospitals in a letter to the IRS demanding detailed accounting for community benefits and increased agency oversight of NFP hospitals that fall short.

Last Tuesday, the Elevance Health Policy Institute released a study concluding that the consolidation of hospitals into multi-hospital systems (for-profit/not-for-profit) results in higher prices without commensurate improvement in patient care quality. “

Friday, Kaiser Health News Editor in Chief Elizabeth Rosenthal took aim at Ballad Health which operates in TN and VA “…which has generously contributed to performing arts and athletic centers as well as school bands. But…skimped on health care — closing intensive care units and reducing the number of nurses per ward — and demanded higher prices from insurers and patients.”

And also last week, the Pharmaceuticals’ Manufacturers Association released its annual study of hospital mark-ups for the top 20 prescription drugs used on hospitals asserting a direct connection between hospital mark-ups (which ranged from 234% to 724%) and increasing medical debt hitting households.

(Excerpts from these are included in the “Quotables” section that follows).

It was not a good week for hospitals, especially not-for-profit hospitals.

In reality, the storm cloud that has gathered over not-for-profit health hospitals in recent months has been buoyed in large measure by well-funded critiques by Arnold Ventures,Lown Institute, West Health, Patient Rights Advocate and others. Providence, Ascension, Bon Secours and now Ballad have been criticized for inadequate community benefits, excessive CEO compensation, aggressive patient debt collection policies and price gauging attributed to hospital consolidation.

This cloud has drawn attention from lawmakers: in NC, the State Treasurer Dale Folwell has called out the state’s 8 major NFP systems for inadequate community benefit and excess CEO compensation.

In Indiana, State Senator Travis Holdman is accusing the state’s NFP hospitals of “hoarding cash” and threatening that “if not-for-profit hospitals aren’t willing to use their tax-exempt status for the benefit of our communities, public policy on this matter can always be changed.” And now an influential quartet of U.S. Senators is pledging action to complement with anti-hospital consolidation efforts in the FTC leveraging its a team of 40 hospital deal investigators.

In response last week, the American Hospital Association called out health insurer consolidation as a major contributor to high prices and,

in a US News and World Report Op Ed August 8, challenged that “Health insurance should be a bridge to medical care, not a barrier.

Yet too many commercial health insurance policies often delay, disrupt and deny medically necessary care to patients,” noting that consumer medical debt is directly linked to insurer’ benefits that increase consumer exposure to out of pocket costs.

My take:

It’s clear that not-for-profit hospitals pose a unique target for detractors: they operate more than half of all U.S. hospitals and directly employ more than a third of U.S. physicians.

But ownership status (private not-for-profit, for-profit investor owned or government-owned) per se seems to matter less than the availability of facilities and services when they’re needed.

And the public’s opinion about the business of running hospitals is relatively uninformed beyond their anecdotal use experiences that shape their perceptions. Thus, claims by not-for-profit hospital officials that their finances are teetering on insolvency fall on deaf ears, especially in communities where cranes hover above their patient towers and their brands are ubiquitous.

Demand for hospital services is increasing and shifting, wage and supply costs (including prescription drugs) are soaring, and resources are limited for most.

The size, scale and CEO compensation for the biggest not-for-profit health systems pale in comparison to their counterparts in health insurance and prescription drug manufacturing or even the biggest investor-owned health system, HCA…but that’s not the point.

NFPs are being challenged to demonstrate they merit the tax-exempt treatment they enjoy unlike their investor-owned and public hospital competitors and that’s been a moving target.

Thus, the methodology for consistently defining and accounting for community benefits needs attention. That would be a good start but alone it will not solve the more fundamental issue: what’s the future for the U.S. health system, what role do players including hospitals and others need to play, and how should it be structured and funded?

The issues facing the U.S. health industry are complex. The role hospitals will play is also uncertain. If, as polls indicate, the majority of Americans prefer a private health system that features competition, transparency, affordability and equitable access, the remedy will require input from every major healthcare sector including employers, public health, private capital and regulators alongside others.

It will require less from DC policy wonks and sanctimonious talking heads and more from frontline efforts and privately-backed innovators in communities, companies and in not-for-profit health systems that take community benefit seriously.

No sector owns the franchise for certainty about the future of U.S. healthcare nor its moral high ground. That includes not-for-profit hospitals.

The darkening cloud that hovers over not-for-profit health systems needs attention, but not alone, despite efforts to suggest otherwise.

Clarifying the community-benefit standard is a start, but not enough.

Are NFP hospitals a problem? Some are, most aren’t but all are impacted by the darkening cloud.

Last week, six notable associations representing health insurers and large employers announced Better Solutions for Healthcare (BSH):“An advocacy organization dedicated to bringing together employers, consumers, and taxpayers to educate lawmakers on the rising cost of healthcare and provide ideas on how we can work together to find better solutions that lower healthcare costs for ALL Americans.”

BSH, which represents 492 large employers, 34 Blue Cross plans, 139 insurers and 42 business coalitions, blames hospitals asserting that “over the last ten years alone, the cost of providing employee coverage has increased 47% with hospitals serving as the number one driver of healthcare costs.”

Its members, AHIP, the Blue Cross Blue Shield Association, the Business Group on Health, Public Sector Health Care Roundtable, National Alliance of Healthcare Purchaser Coalitions and the American Benefits Council, pledge to…

Promote hospital competition

Enforce Federal Price Transparency Laws for Hospital Charges

Rein in Hospital Price Mark-ups

Insure Honest Billing Practices

And, of particular significance, BSH calls out “the growing practice of corporate hospitals establishing local monopolies and leveraging their market dominance to charge patients more…With hospital consolidation driving down competition, there’s no pressure for hospitals to bring costs back within reach for employees, retirees and their families…prices at monopoly hospitals are 12% higher than in markets with four or more competitors.”

The BSH leadership team is led by DC-based healthcare policy veterans with notable lobbying chops: Adam “Buck” Buckalew, a former Sen. Lamar Alexander (R-TN) staffer who worked on the Health Education, Labor and Pensions (HELP) committee and is credited with successfully spearheading the No Surprises Act legislation that took effect in January 2022, and Kathryn Spangler, another former HELP staffer under former Sen. Mike Enzi (R-WY) who most recently served as Senior Policy Advisor at the American Benefits Council.

It’s a line in the sand for hospitals, especially large not-for-profit systems that are on the defensive due to mounting criticism.

Examples from last week: Atrium and Caremont were singled in NC by the state Treasurer for their debt collection practices based on a Duke study that got wide media coverage. Allina’s dispute with 550 of its primary care providers seeking union representation based on their concerns about patient safety. Jefferson Health was called out for missteps under its prior administration’s “growth at all costs” agenda and the $35 million 2021 compensation for Common Spirit’s CEO received notice in industry coverage.

My take:

BSH represents an important alignment of health insurers with large employers who have shouldered a disproportionate share of health costs for years through the prices imposed for the hospitals, prescriptions and services their employees and dependents use.

Though it’s too early to predict how BSH vs. Corporate Hospitals will play out, especially in a divided Congress and with 2024 elections in 14 months, it’s important to inject a fair and balanced context for this contest as the article of war are unsealed:

Health insurers and hospitals share the blame for high health costs along with prescription drug manufacturers and others. The U.S. system feasts on opaque pricing, regulated monopolies and supply-induced demand. Studies show unit costs for hospitals along with prescription drug costs bear primary responsibility for two-thirds of health cost increases in recent years—the result of increased demand and medical inflation. But insurers are complicit: benefits design strategies that pre-empt preventive health and add administrative costs are parts of the problem.

Corporatization of the U.S. system cuts across every sector: Healthcare’s version of Moneyball is decidedly tilted toward bigger is better: in healthcare, that’s no exception. 3 of the top 10 in the Fortune 100 are healthcare (CVS-Aetna, United, McKesson)) and HCA (#66) is the only provider on the list. The U.S. healthcare industry is the largest private employer in the U.S. economy: how BSH addresses healthcare’s biggest employers which include its hospitals will be worth watching. And Big Pharma companies pose an immediate challenge: just last week, HHS called out the U.S. Chamber of Commerce for siding with Big Pharma against implementation of drug price controls in the Inflation Reduction Act—popular with voters but not so much in Big Pharma Board rooms.

The focus will be on Federal health policies. BSH represents insurers and employers that operate across state lines–so do the majority of major health systems. Thus, federal rules, regulations, administrative actions, executive orders, and court decisions will be center-stage in the BSH v. corporate hospitals war. Revised national policies around Medicare and federal programs including military and Veterans’ health, pricing, equitable access, affordability, consolidation, monopolies, data ownership, ERISA and tax exemptions, patent protections and more might emerge from the conflict. As consolidation gets attention, the differing definitions of “markets” will require attention: technology has enabled insurers and providers to operate outside traditional geographic constraints, so what’s next? And, complicating matters, federalization of healthcare will immediately impact states as referenda tackle price controls, drug pricing, Medicaid coverage and abortion rights—hot buttons for voters and state officials.

Boards of directors in each healthcare organization will be exposed to greater scrutiny for their actions: CEO compensation, growth strategies, M&A deals, member/enrollee/patient experience oversight, culture and more are under the direct oversight of Boards but most deflect accountability for major decisions that pose harm. Balancing shareholder interests against the greater good is no small feat, especially in a private health system which depends on private capital for its innovations.

8.6% of the U.S. population is uninsured, 41% of Americans have outstanding medical debt, and the majority believe health costs are excessive and the U.S. system is heading in the wrong direction.

Compared to other modern systems in the world, ours is the most expensive for its health services, least invested in social determinants that directly impact 70% of its costs and worst for the % of our population that recently skipped needed medical care (39.0% (vs. next closest Australia 21.2%), skipped dental care (36.2% vs. next closest Australia 31.7%) and had serious problems/ were unable to pay medical bills (22.4% next closest France 10.1%). Thus, it’s a system in which costs, prices and affordability appear afterthoughts.

Who will win BSH vs. Corporate Hospitals? It might appear a winner-take all showdown between lobbyists for BSH and hospital hired guns but that’s shortsighted. Both will pull out the stops to win favor with elected officials but both face growing pushback in Congress and state legislatures where “corporatization” seems more about a blame game than long-term solution.

Each side will use heavy artillery to advance their positions discredit the other. And unless the special interests that bolster efforts by payers are hospitals are subordinated to the needs of the population and greater good, it’s not the war to end all healthcare wars. That war is on the horizon.

Blue Shield of California announced a plan to diversify its pharmacy benefit management (PBM) contracts in a bid to improve transparency and reduce costs.

Instead of relying on Woonsocket, RI-based CVS Health’s Caremark as its sole PBM, the health plan and its 4.8M members will be served by five companies, including Amazon Pharmacy for at-home deliveries, Mark Cuban Cost Plus Drugs Company (MCCPDC) for a transparent pricing model, and Prime Therapeutics for negotiations with pharmaceutical companies.

Caremark will remain responsible for Blue Shield’s specialty pharmacy needs, which CVS noted in an investor filing represents over 50 percent of nationwide pharmacy benefit spending.

Blue Shield intends to implement this new system by 2025, and is targeting savings of $500M annually, which translates to 10 to 15 percent of its current spending.

The Gist: Whether Blue Shield saves money with this initiative depends on the whether the benefit of competition in its PBM contracts outweighs the costs of more complex coordination between vendors.

Keeping half of its business tied up with CVS through specialty pharmacy will further limit the potential impact. Nonetheless, it’s noteworthy that pharmacy disruptors like Amazon and MCCPDC have found a major health plan willing to work with them.

Consumers, employers, payers without PBMs, and members of Congress are increasingly dissatisfied with the current pharmacy benefit market structure, and Blue Shield’s move could serve as a catalyst for future shakeups.

Payers have historically been the financial support for patients receiving medical care. Through scale, predictive analytics and actuarial insights, large insurers have been able to smoothly calibrate pricing and earnings so that members have health coverage no matter the economic environment. Over time different insurance products such as Medicare Advantage, managed Medicaid, Commercial insurance, and self-funded benefits were created to provide optionality for consumers. The demand for more services under one umbrella has resulted in six large public insurers, known collectively as the “Nationals.” As for-profit public entities, these organizations have utilized M&A to drive growth by acquiring smaller health plans. This horizontal consolidation has grown membership and diversified their membership geographically, as well as by line of business. The diversification enables these Nationals to reduce volatility in earnings, which eases concerns of public investors, while sustaining top line growth each year. However, with the changing tide in healthcare business models, payers have begun to look elsewhere for new growth opportunities.

The emergence of value-based care has garnered significant interest within the healthcare ecosystem. Consumers of healthcare value their personalized interactions with their providers / doctors and are typically somewhat agnostic about their payer. The payers have come to the realization that to further drive profits, they must create stickiness with their members by aligning with the providers that are delivering the care. Collaboration between the payers and providers will help increase the efficiencies in care management and drive unnecessary costs out the care delivery process, when fully integrated. By being “closer” to the patients, payers can use the data from providers to create valuable insights that proactively address a patient’s needs before catastrophic, high-cost treatments are required. This trend of vertical integration, turning payers to pay-(pro)viders, has started to play out and should be beneficial to patients, payers, providers, investors, and U.S. healthcare as a whole.

UnitedHealthcare recently closed its $5.4 billion acquisition of LHC Group in February 2023. LHC Group provides home health solutions and community-based care to over 12 million patients annually in their homes. This acquisition is UnitedHealthcare’s opportunity to increase patient engagement for the high acuity populations that LHC Group traditionally services. UnitedHealthcare also announced the acquisition of Amedisys, another home health and hospice provider, for $3.3 billion in 2023. UnitedHealthcare will be able to leverage the expertise from these two organizations, while utilizing its data analytical capabilities to synchronize care efficiently and effectively. As the U.S. population continues to age, optimizing care for seniors will be a key focal point for the healthcare services industry.

CVS Health acquired Oak Street Health, a primary care provider that specializes in value-based care, for $10.6 billion in 2023. This acquisition will help CVS Health address costs and patient health in underserved communities that Oak Street Health currently services. CVS Health also acquired Signify Health, a technology and services company that focuses on care at home, in 2023 for $8 billion. The acquisitions of Oak Street Health and Signify Health will expand CVS Health’s healthcare delivery arm as it looks to become a one-stop shop for all patient’s needs.

As other payers see the value, both in better health outcomes and economics, created through the vertical integration of services by their competitors, they too will follow the trend. The definition of the payer will continue to evolve, and healthcare consumers will increasingly receive lower cost of care, greater accessibility to care and preferential outcomes into the future. It will be exciting to see which pay-vider acts next and capitalizes on this opportunity.

Hospital and insurer contract negotiations are often framed as an industry gauntlet, a defined period of time with an objective outcome where big talk does not translate to money. But reimbursement rates secured in new contracts are only one piece of hospitals’ payer-induced headaches.

Traditionally, a health system and commercial insurer would occasionally run into a wall in the contract negotiation process. This could play out into a dispute palpable enough to consumers that it warranted headlines. These impasses generally lasted a matter of weeks with no significant disruptions before outside pressure drove the parties to compromise.

Over the past five years or so, the nature of provider-payer conflicts intensified and may be on the cusp of unprecedented severity given health systems’ financial pressures. At the same time, agreed-upon reimbursement rates are only the tip of the iceberg when it comes to payment health systems can expect from commercial insurers, who have many more defensive plays in their playbook.

They boil down to a classic line from a 1968 movie: deny, deny, deny.

Russ Johnson is CEO of LMH Health, a 102-year-old, independent, nonprofit health system based in Lawrence, Kan. The $350 million organization is anchored by a 174-bed hospital. As he puts it: “We’re not tiny, but we’re not very big.”

Mr. Johnson has spent 37 years working in healthcare, holding senior leadership positions in hospitals and health systems in rural communities and large cities. It’s difficult to identify many things going well when it comes to provider-payer relationships, but Mr. Johnson told Becker’s that it’s the payer movements beneath the reimbursement rates that are worsening and causing greater pain today.

“The part that’s getting worse is the practices behind and underneath the contracts — the sophistication and implementation of pay practices, information systems, artificial intelligence and computer algorithms that are just denying claims by the thousands every month,” he said.

The reimbursement rates secured in contracts are what you can see above water. Beneath, health insurers are moving faster and kicking harder. Throughout the first three months of 2023, about one-third of inpatient and outpatient claims submitted by providers to commercial payers went unpaid for more than 90 days, according to an analysis from Crowe.

“So many more claims are now surfacing with some kind of a fallout on a denial, a downcoding or a pre-authorization — you know, the proverbial dotting the i’s and crossing the t’s, sometimes. But what is abundantly clear is it is not fundamentally about a clinical difference,” Mr. Johnson said.

Denials were once reserved for a sliver of expensive treatments and have now become common occurrence for mundane, ordinary medical care and treatments such as inhalers or familiar medications for chronic conditions a patient has managed for years. The administrative burden is something close to a requirement to prove residency every month to receive electricity or verifying eligibility to work in the U.S. every week for a paycheck — redundant, time-wasting activity for ordinary, essential things.

“For our business office to keep up with what I frankly think is mischief by the payers in terms of denials, pre-authorization, DRG downcoding and a completely unengaged experience trying to negotiate — or to have our physicians call in and do a peer-to-peer conferences about clinical necessity — it’s demoralizing, frankly,” Mr. Johnson said. “Dealing with denial from our payers is one of the biggest dissatisfiers our physicians face.”

Authors of the 2010 Affordable Care Act worried that provisions to expand health insurance access — such as barring health insurers’ refusal to cover patients with preexisting conditions — could cause them to ratchet up other tactics to make up for the change. With this in mind, the law charged HHS with monitoring health plan denial rates, but oversight has been unfulfilled, leaving denials widespread.

Data and numbers on denial rates are not easy to find, but some examination paints a picture rich with variation. An analysis of 2021 plans on Healthcare.gov conducted by KFF found nearly 17 percent of in-network claims were denied, with rates varying from 2 percent to 49 percent. The reasons for the bulk of denials are unclear. About 14 percent were attributed to an excluded service, 8 percent to lack of pre-authorization or referral and 2 percent to questions of medical necessity. A whopping 77 percent were classified as “all other reasons.”

Adding to the inconsistency is the fact that health plan denial rates fluctuate year over year. In 2020, a gold-level health plan offered by Oscar Insurance in Florida denied 66 percent of payment requests; in 2021 it denied 7 percent.

There is much to learn about the ways AI will shape healthcare, and its potential to further expedite and increase denials is concerning. Cigna faces a class-action lawsuit alleging it bypassed requirements for claim review before denial by having an algorithm — dubbed “PXDX” — complete review before having physicians sign off on batches of denied claims. The lawsuit followed a ProPublica report on the practice, which said Cigna physicians denied more than 300,000 claims over two months in 2022 through the system, which equated to 1.2 seconds of review per claim on average.

AI is often touted as a potential, looming replacement to hardworking healthcare professionals, but in the day to day it exacerbates the administrative burdens that already bring them down.

“Nobody becomes a physician because they hope to feel like a cog in a factory,” Michael Ivy, MD, deputy chief medical officer of Yale New Haven (Conn.) Health, told Becker’s. “However, between meeting the demands of payers for referrals, denials of payment and increased documentation requirements in order to assure proper reimbursement and risk adjustment, as well as an increasing number of production metrics, it can be difficult not to feel like a cog.”

On Tuesday, the White House issued a proposal to enhance the 2008 Mental Health Parity and Addiction Equity Act, which requires insurers to cover mental healthcare at the same level as physical care.

Health plans would be required to evaluate mental health coverage policies, including network size, prior authorization rules, and out-of-network payment policies.

The proposal also includes closing a loophole in the original law that excludes non-federal government health plans from these parity standards.

The Gist: Fewer than half of the one in five US adults experiencing mental illness in 2020 received care for their illness, and fewer than one in 10 received treatment for a substance abuse disorder.

But while insurance companies’ failure to establish adequate mental health networks is part of the problem, there are other, larger access issues at play, including the nationwide shortage of mental health clinicians, many of whom don’t accept insurance.

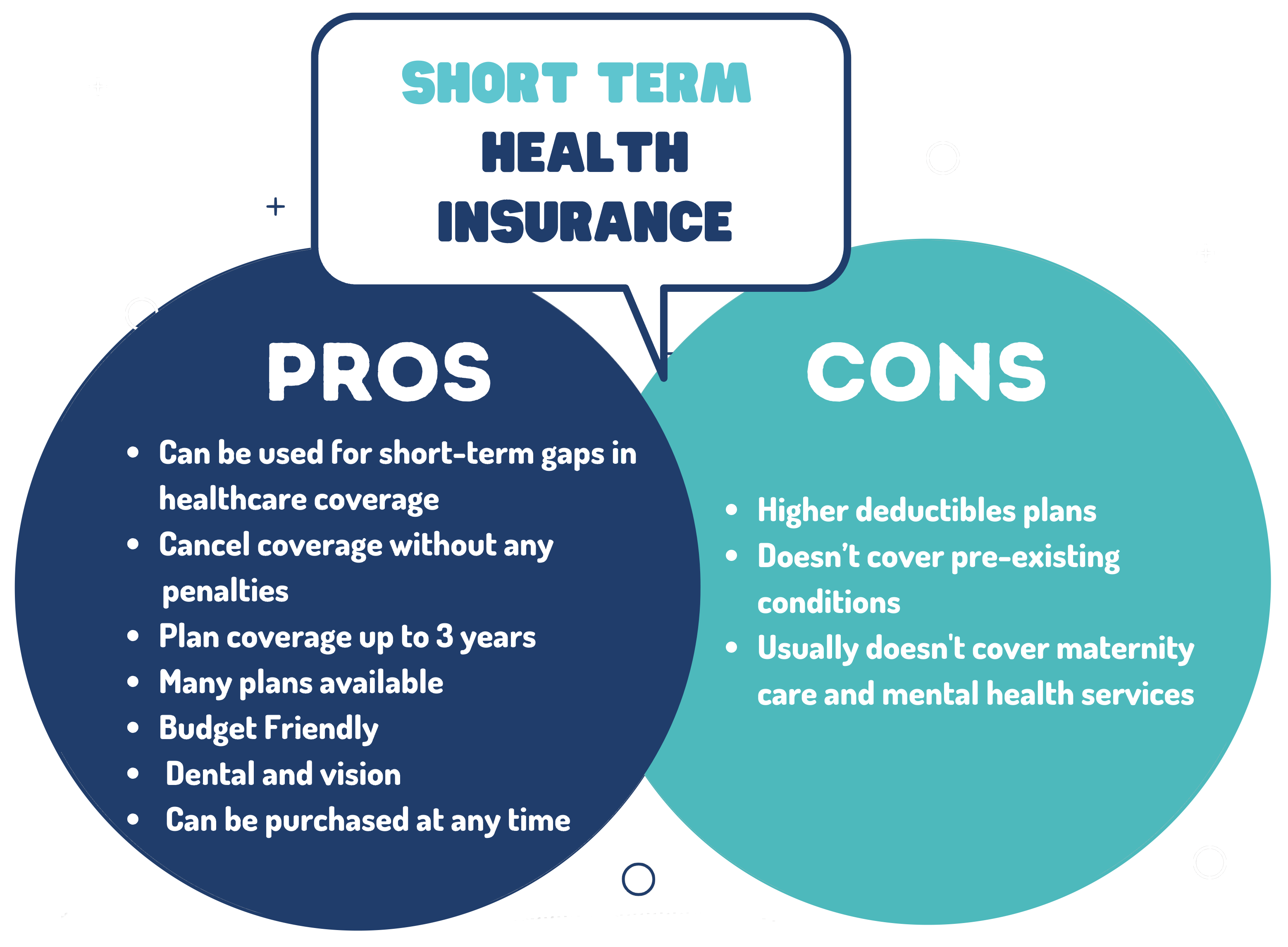

Last Friday, the Department of Health and Human Services, the Treasury Department, and the Department of Labor jointly issued several proposed rules to shore up consumer healthcare protections, including reversal of a Trump administration policy that allowed consumers to enroll in short-term health plans, which were intended to serve as limited coverage options during transitional periods, for up to three years. Approximately 3M people were enrolled in these plans in 2019.

A new rule would limit consumer access to these plans to just three months, with an optional one-month extension, while also requiring payers to disclose clearly how their plans fall short of comprehensive health insurance.

The Gist: In an expected move, theBiden administration continues its unwinding of the Trump-era policies it sees as undermining the Affordable Care Act’s (ACA’s) mission of guaranteeing robust, accessible insurance for all.

Short-term plans, which were granted an exemption from the ACA requirement that health plans cover ten essential health benefits, have been found to discriminate against people with pre-existing conditions, revoke coverage for enrollees retroactively, and generate excess surprise bills due to their limited networks.