Last week, the nation’s two largest Medicare Advantage insurers revealed that second quarter outpatient volumes were higher than anticipated, prompting a selloff of insurance stocks.

Minnetonka, MN-based UnitedHealth Group (UHG) executives said at a Goldman Sachs investor conference that increased outpatient utilization was driving up its medical loss ratio (MLR) to the high end of its annual target, surmising that a new wave of seniors were finally accessing elective procedures like joint replacements postponed throughout COVID.

Then, in an investor filling, Louisville, KY-based Humana noted that both outpatient and inpatient utilization levels were elevated, though it did not point to any specific causes. But not all insurers have experienced higher-than-expected utilization: Indianapolis, IN-based Elevance Health reported that its medical spending this year so far was in line with expectations, and it did not expect a surge in procedure demand.

The Gist: Health systems will find this news, especially Humana’s reports of elevated inpatient and emergency department volumes, as encouraging as the insurers consider it alarming. But the bulk of this outpatient volume isn’t necessarily returning to health systems, as the proliferation of insurer- and investor-backed ambulatory surgery centers has resulted in not only more, but also lower-cost, competition.

Health systems with significant ambulatory surgery center footprints, including Tenet and HCA, should be well-positioned to capture the volume return.

A majority of Americans with health insurance said they had encountered obstacles to coverage, including denied medical care, higher bills and a dearth of doctors in their plans, according to a new survey from KFF, a nonprofit health research group. As a result, some people delayed or skipped treatment.

Those who were most likely to need medical care — people who described themselves as in fair or poor health — reported more trouble; three-fourths of those receiving mental health treatment experienced problems.

“The consequences of care delayed and missed altogether because of the sheer complexity of the system are significant, especially for people who are sick,” said Drew Altman, the CEO of KFF, formerly known as the Kaiser Family Foundation.

The survey also underscored the persistent problem of affordability as people struggled to pay their share of health care costs. About 40% of those surveyed said they had delayed or gone without care in the last year because of the expense. People in fair or poor health were more than twice as likely to report problems with paying medical bills than those in better health, and Black adults were more likely than white adults to indicate they had trouble.

Why It Matters: Delayed care can endanger health.

Nearly half of those who encountered a problem with their insurance said they could not satisfactorily resolve it. Some could not obtain the care they had sought, while others said they paid more than expected. Among the nearly 60% who reported difficulty with their insurance coverage, 15% said their health had declined.

“This survey shows it’s not enough to just get a card in your pocket — the insurance has to work or it’s not exactly coverage,” said Karen Pollitz, the co-director for KFF’s patient and consumer protections program.

People have a hard time understanding their coverage and benefits, with 30% or more reporting difficulty figuring out what they will be required to pay for care or what exactly their insurance will cover.

“Insurances are way more complicated than they should be,” said Amanda Parente, a 19-year-old college student in Nashville, Tennessee, who is covered under her mother’s employer plan. She was surprised to find that her out-of-pocket costs spiked recently when she sought treatment for strep throat. While she realized her copayments would be higher, “I guess we didn’t know how drastic it was going to be,” she said.

Background: Insurance coverage is confusing to everyone.

Navigating the intricacies of coverage and benefits were similar regardless of what kind of insurance people had. At least half of those surveyed with private coverage, through an employer, those with an “Obamacare” plan, or a government program like Medicare or Medicaid, said they experienced difficulties.

People might be unhappy with their coverage because they were already concerned about higher inflation and potential layoffs, said Christopher Lis, the managing director of global health care intelligence at J.D. Power, which found that consumer satisfaction with insurers had declined in a recent study. “We’ve got economic conditions that set the stage for concern around coverage and benefits,” he said.

Insurers say people generally report being happy with their plan, and 81% of those surveyed by KFF gave their insurance high ratings. “Health insurance providers are committed to improving access, affordability and convenience for all Americans and will continue to find innovative solutions to work toward this common goal,” said David Allen, a spokesperson for AHIP, a trade group that represents insurers.

What’s Next: How to haggle with insurers or appeal?

Also striking among the survey’s findings was how unaware people were about pursuing appeals of denied coverage and how to go about doing so.

“Most people don’t know who to call,” Pollitz said. Sixty percent of insured adults surveyed did not know they had a legal right to appeal, and about three-fourths said they did not know which government agency to contact for help, particularly respondents with private insurance.

State insurance regulators oversee fully insured policies sold to individuals and small businesses, and the federal Department of Labor has jurisdiction over employer-sponsored insurance.

Many of the problems people have with their insurance could be solved by enforcing existing rules, like federal regulations requiring private insurers to issue understandable explanations of benefits and to maintain accurate, current lists of doctors and hospitals within their networks.

Pent-up demand for delayed healthcare during the COVID-19 pandemic is pressuring medical costs for health insurers that had a financial windfall during the pandemic amid low utilization.

UnitedHealth, the parent company of the largest private payer in the U.S., expects its medical loss ratio — the share of premiums spent on member’s healthcare costs — to be higher than previously expected in the second quarter of 2023, due to a surge in outpatient care utilization among seniors, CFO John Rex said Tuesday during Goldman Sachs’ investor conference.

The news sent UnitedHealth’s stock down 7% in morning trade Wednesday, and affected other Medicare-focused health insurers as well. Humana, CVS and Centene — the three largest MA insurers by enrollee after UnitedHealth — dropped 13%, 6% and 8%, respectively.

Dive Insight:

The early days of COVID saw widespread halts in nonessential services, causing visits to plunge with an estimated one-third of U.S. adults delaying or foregoing medical care in the pandemic’s first year. By 2022, the sizable rebound in deferred care that many predicted had yet to materialize.

Now, early signs suggest utilization may again be increasing, with the cost of rebounding care coming around to hit payers. UnitedHealth now expects its MLR for the second quarter to reach or exceed its full-year target of 82.1% to 83.1%.

“As you look at a Q2, you would expect Q2 medical care ratio to be somewhere in the zone of probably the upper bound or moderately above the upper bound of our full-year outlook,” Rex said. “I would expect at this distance that the full year would probably settle in in the upper half of the existing range we set up.”

In comparison, the insurer reported an MLR of 82.2% in the first quarter of 2023. UnitedHealth’s MLR was 82% in 2022.

UnitedHealth said the MLR increase is because medical activity is normalizing after COVID kept seniors away from non-essential care.

“We’re seeing as behaviors kind of normalize across the country in a lot of different ways and mask mandates are dropped, especially in physician offices, we’re seeing that more seniors are just more comfortable accessing services for things that they might have pushed off a bit like knees and hips,” said Tim Noel, UnitedHealth’s chief executive for Medicare and retirement.

The Minnetonka, Minnesota-based insurer has seen strong outpatient demand through April, May and June, particularly in hips and knees with high volumes at its owned ambulatory surgical centers and within its Medicare business, executives said.

Inpatient volumes have remained consistent, and while outpatient utilization has increased, patient acuity has remained the same. Optum Health’s behavioral businesses are also seeing higher utilization in the second quarter, said Patrick Conway, CEO of Care Solutions at Optum, UnitedHealth’s health services division.

UnitedHealth doesn’t expect this higher activity to let up anytime soon. As a result, the payer incorporated higher outpatient utilization into its Medicare Advantage plan bids for 2024, which were placed in early June. The move attests to the longer duration of the trend, SVB Securities analyst Whit Mayo wrote in a note.

“Assuming it is going to end quickly wouldn’t be prudent on our part,” Rex said. “We’ll see how this progresses here.”

On Monday, Minnetonka, MN-based UHG’s Optum division made a $3.3B all-cash offer to acquire Baton Rouge, LA-based Amedisys, one of the country’s largest home health companies.

Optum’s bid came several weeks after Bannockburn, IL-based Option Care Health, a home health company specialized in drug and infusion services, offered to purchase Amedisys in an all-stock transaction valued at $3.6B. Amedisys itself acquired hospital-at-home company Contessa Health for $250M in 2021. While its Board of Directors is now evaluating whether UHG has made a “Superior Proposal”, a UHG acquisition of Amedisys would likely be subject to significant regulatory oversight, as the payer recently closed on its purchase of home health company and Amedisys-competitor LHC Group in a deal that was heavily scrutinized by the Federal Trade Commission.

The Gist: UHG, the nation’s largest health insurer, is on a tear to bring the country’s largest home health providers under its Optum umbrella—and it has the deep pockets to outbid nearly anyone else trying to do the same.

While some questioned the value of an Option Care-Amedisys combination, UHG would get to plug another asset into its scaled continuum of home-based care, allowing it to steer beneficiaries away from high-cost post acute care and continue to increase profitable intercompany eliminations.

If UHG’s bid for Amedisys is accepted, it would also gain its first hospital-at-home asset in Contessa, providing it with the opportunity to fully redirect—and reduce—its inpatient care spend.

The news of Optum’s bid to acquire Amedisys came as a surprise — but it fits a larger theme of payers, particularly Medicare Advantage plans, looking to acquire assets to build out a home ecosystem.

In recent years, we’ve seen this play out in a number of ways, with some buyers finding success in their endeavors and others selling off the asset shortly after acquisition. While some buyers, including payers and other providers, have been able to capitalize on owning home health assets, others have struggled to benefit financially.

The drivers

When acquiring a home health agency, payers’ objectives are largely centered around operating costs and the ability to refer as many of their patients to these organizations as possible. If the agency is not delivering a return on investment or is unable to refer enough patients, payers are not afraid to divest and reevaluate structure.

Despite these varying outcomes, the race is on to acquire home-based care assets. We suspect there are two main reasons:

1. Home-based care is a cost-effective alternative

Payers want to direct their members from acute care back to the home without a skilled nursing stay. Especially for Medicare Advantage patients, there is a financial incentive to avoid sending patients to a skilled nursing facility (SNF).

Amid the push to improve patient quality, SNFs are often seen as a cost center that payers are eager to cut out — leading many to invest in home health agencies and services.

2. Home-based care operators need to grow their workforce

All home-based care operators, whether part of a payer organization or not, need to grow their workforce. According to our research, this was the number one factor hindering the expansion of home-based care.

By adding Amedisys’s workforce to their own existing home-based care workforce, Optum could help overcome this challenge.

Optum’s interest in Amedisys is also notable because of the diversity of services that Amedisys offers. Not only do they support home health, but they also offer hospital at home services through Contessa as well as home-based palliative and hospice care. That’s an attractive suite of services for a Medicare Advantage payer interested in offering more care in the home.

What we’ll be watching

It’s still unclear what will happen with Optum’s offer for Amedisys. Even if Amedisys agrees to the acquisition, the deal is likely to face FTC scrutiny. If that does happen, we’ll be watching to see whether Optum has to divest from any of Amedisys’ assets as part of an eventual deal.

With the continued rise in seniors who require skilled care — most of whom would prefer to age in the home — investments and divestments in the home health space will continue to make headlines.

Moving forward, we’ll be paying close attention to the outcomes of larger home health acquisitions by payer organizations.

Specifically, we’ll be watching to see if they’re able to successfully move their members away from facility-based care and into the home, both in terms of quality and the bottom line.

In the mid-1980’s, managed care advocate Dr. Paul Ellwood predicted that eventually, US healthcare would be dominated by perhaps a dozen vast national firms he called SuperMeds that would combine managed care based health insurance with care delivery systems. Ellwood was a leader of the “managed competition” movement which advocated for a private sector alternative to a federal government-run National Health Insurance system. Ellwood and colleagues believed that Kaiser Foundation Health Plans and other HMOs would be able to stabilize health costs and thus affordably extend care to the uninsured.

The US political system and market dynamics would not co-operate with Ellwood and his Jackson Hole Group’s vision. In the ensuing thirty-five years, healthcare has remained both highly fragmented and regional in focus. However, unbeknownst to most, during the past decade, as a result of a major merger and relentless smaller acquisitions, two SuperMeds were born- CVS/Aetna and UnitedHealth Group, that whose combined revenues comprise 14% of total US health spending.

CVS/Aetna is slightly larger than United, by dint of grocery sales in its drugstores and its vast Caremark pharmacy benefits management business. However, CVS’s Aetna health insurance arm is one third the size of United’s, and though CVS is rapidly scaling up its care delivery apparatus through its in-store Health Hubs, it remains is a tiny fraction of United’s care footprint. Despite being slightly smaller at the top line, United’s market capitalization is more than 3.5 times that of CVS.

United’s vast scope is difficult to comprehend because much of it is not visible to the naked eye, and the most rapidly growing businesses are partly nested inside United’s health insurance business.

United employs over 300 thousand people. At $287.6 billion total revenues in 2021, United exceeded 7% of total US health spending (though $8.3 billion are from overseas operations).

In 2021, United was $100 billion larger than the British National Health Service. It is more than three times the size of Kaiser Permanente, and five times the size of HCA, the nation’s largest hospital chain. United is both larger and richer than energy giant Exxon Mobil. United has over $70 billion in cash and investments, and is generating about $2 billion a month in operating cash flow.

Its highly regulated health insurance business is the visible tip of a rapidly growing iceberg. Revenue from United’s core health insurance business grew at 11% in 2021, compared to 14% growth in United’s diversified Optum subsidiary. Optum generated $155.6 billion in 2021 (of which 60% were from INSIDE United’s health insurance business). You can see the relationship of Optum’s three major businesses to United’s health insurance operations in Exhibit I.

Optum is the Key to United’s Growth

Understanding the role of Optum is key to understanding United’s business. It is remarkable how few of my veteran health care colleagues have any idea what Optum is or what it does. Optum was once a sort of dumping ground for assorted United acquisitions without a seeming core purpose. A private equity colleague once derided Optum as “The Island of Lost Toys”. Now, however, Optum is driving United’s growth, and generates billions of dollars in unregulated profits both from inside the highly regulated core health insurance business and from external customers.

Optum consists of three parts:Optum Health, its care delivery enterprise ($54 billion revenues in 2021), Optum Rx, its pharmacy benefits management enterprise ($91 billion revenues in 2021) and Optum Insight, a diversified business services enterprise ($12.2 billion in 2021). Virtually all of United’s acquisitions join one of these three businesses.

Optum Health: The Third Largest Care Delivery Enterprise in the US

By itself, Optum Health is almost the size of HCA ($54 billion in 2021 vs HCA’s $58.7 billion) and consists of a vast national portfolio of care delivery entities: large physician groups, urgent care centers, surgicenters, imaging centers, and now by dint of the recently announced $5.7 billion acquisition of LHC, home health agencies. Optum Health has studiously avoided acquiring beds of any kind: hospitals, nursing homes, etc. and likely will continue to do so. Optum Health’s physician groups not only generate profits on their own, but also provide powerful leverage for United to control health costs for its own subscribers, pushing down United’s highly visible and regulated Medical Loss Ratio (MLR), and increasing health plan profits.

Optum Health began in 2007 when United acquired Nevada-based Sierra Health, and thus became the new owner of a small multispecialty physician group which Sierra owned. The group did not belong in United’s health insurance business and came to rest over in Optum. Over the past twelve years, Optum Health has acquired an impressive percentage of the major capitated medical groups in the US- Texas’ WellMed, California’s HealthCare Partners (from DaVita), as well as Monarch, AppleCare and North American Medical Management, Massachusetts’ Reliant (formerly Fallon Clinic) and Atrius in Massachusetts (pending) , Kelsey Seybold Clinic (also pending) in Houston, TX and Everett Clinic and PolyClinic in Seattle.

Optum Health claims over 60 thousand physicians, though many of these are actually independent physicians participating in “wrap around” risk contracting networks. By comparison, Kaiser Permanente’s Medical Groups employ about 23 thousand physicians. United’s management claims that Optum Health provides continuing care to about 20 million patients, of whom 3 million are covered by some form of so-called “value based” contracts. Perhaps half of this smaller number are covered by capitated (percentage of premium-PMPM) contracts.

Optum Health straddles fierce competitive relationships between United’s health insurance business and competing health plans in well more than a dozen metropolitan areas. Almost half (44%) of Optum Health’s revenues come from providing care for health plans other than United.

When Optum acquires a large physician group, it acquires those groups’ contracts with United’s health insurance competitors, some of which contracts have been in place for decades. Premium revenues from other health plans, presumably capitation or per member per month (PMPM) revenues, are one-quarter of Optum Health’s $54 billion total revenues. These “external” premium revenues have quadrupled since 2018, largely for Medicare Advantage subscribers. Optum Health contributes about $4.5 billion in operating profit to United. It is impossible to determine from United’s disclosures how much of this profit comes from Optum Health’s services provided to United’s insured lives and how much from its medical groups’ extensive contracts with competing health plans.

Optum Health’s surgicenters and urgent care centers provide affordable alternatives to using expensive hospital outpatient services and emergency departments, potentially further reducing United medical expense. This creates obvious tensions with United’s hospital networks, since Optum Health can use its large medical practices and virtual care offerings to divert patients from hospitals to its own services, or else render those services unnecessary.

Though some observers have termed Optum/United’s business model “vertical integration”-ownership of the suppliers to and distributors of a firm’s product– Optum Health has actually grown less vertical since 2018, with revenues from competing health plans growing from 36% of total revenues in 2018 to 44% in 2021. A 2018 analysis by ReCon Strategy found at best a sketchy matchup between United’s health plan enrollment by market and its Optum Health assets (https://reconstrategy.com/2018/04/uniteds-medicare-advantage-footprint-and-optumcare-network-do-not-overlap-much-so-far/.

Optum Rx: The Nation’s Third Largest Pharmacy Benefits Management Business

Optum’s largest business in revenues is its Optum Rx pharmaceutical benefits management (PBM) business, which generates $91 billion in revenues, and processes over a billion pharmacy claims not only for United but also many competing insurers and employer groups. Pharmaceutical costs are a rapidly growing piece of total medical expenses, and controlling them is yet another source of largely unregulated profits for United; Optum Rx generated over $4.1 billion of operating profit in 2021.

Optum Rx is the nation’s third largest PBM business after Caremark, owned by CVS/Aetna and Express Scripts, owned by CIGNA, and processes about 21% of all scripts written in the US. Pharmacy benefits management firms developed more than two decades ago to speed the conversion of patients from expensive branded drugs to generics on behalf of insurers and self-funded employers. They were given a big boost by George Bush’s 2004 Medicare Part D Prescription Drug benefit, as a “pro-competitive” private sector alternative to Medicare directly negotiating prices with pharmaceutical firms.

Reducing drug spending is one key to United’s profitability. Since generics represent almost 90% of all prescriptions written, Optum Rx now relies on fees generated by processing prescriptions and on rebates from pharmaceutical firms to promote their costly branded drugs as preferred drugs on Optum Rx’s formularies. These rebates are determined based on “list” prices for those drugs vs. the contracted price for the PBMs, and are actual cash payments from manufacturers to PBMs.

Drug rebates represent a significant fraction of operating profits for health insurers that own PBMs, particularly for their older Medicare Advantage patients that use a lot of expensive drugs. Unfortunately, PBMs have incentives to inflate the list price, because rebates are caculated based on the spread between list prices and the contract pricel Unfortunately, this increases subscribers’ cash outlays, because patient cost shares are based on list prices.

Optum Rx generates about 39% of its revenues (and an undeterminable percentage of its profits) serving other health insurers and self-funded employers. Many of those self-funded employers demand that Optum pass through the rebates directly to them (even if it means being charged higher administrative fees!).

Unlike the situation with Optum Health, the “verticality” of Optum’s PBM business-the percentage of Optum revenues derived from serving United subscribers- has increased in the last seven years, to more than 60% of Optum Rx’s total business. What happens to the billions of dollars in rebates generated by Optum Rx is impossible to determine from United’s disclosures. However, our best guess is that pharmaceutical rebates represent as much as a quarter of United’s total corporate profits.

Optum Insight: “Intelligent” Business Solutions

The fastest growing and by far the most profitable Optum business is its business intelligence/business services/consulting subsidiary. Optum Insight was generated $12.2 billion in revenues in 2021, but a 27.9% operating margin, five times that of United’s health insurance business. Optum Insight is strategically vital to enhancing the profitability of United’s health insurance activities, but also generates outside revenues selling services to United’s health insurance competitors and hospital networks.

The core of Optum Insight is a business intelligence enterprise formerly known as Ingenix, which provided “big data” to United and other insurers about hospital and pricing behavior and utilization-crucial both for benefits design and administration. In 2009, Ingenix was accused by New York State of under reporting prices for out of network health services for itself and its clients, which had the effect of reducing its own medical reimbursements, and increasing patient cost shares. United signed a consent decree to alter Ingenix business practices and settled a raft of lawsuits filed on behalf of patients, physicians and employers. Its name was subsequently changed to Optum Insight.

By dint of aggressive acquisitions, Optum Insight has dramatically increased its medical claims management business, consulting services and business process outsourcing activities. . Most of United’s investment in artificial intelligence can be found inside Optum Insight. Big data plays a crucial role in United’s overall strategy. Optum Insight’s claims management software uses vast medical claims data bases and artificial intelligence/machine learning software to spot and deny medical claims for which documentation is inadequate or where services are either “inappropriate” or else not covered by an individual’s health plan. Providers also claim that the same software rejects as many as 20% of their claims, often for problems as tiny as a mis-spelled word or a missing data field.

Optum Insight software plays a crucial role in helping United’s health insurance plans manage their medical expense. Traditional health plan profitability is generated by reducing medical expense relative to collected premiums to increase underwriting profit. These profits are regulated, with highly variable degrees of rigor by state health insurance commissioners, and also by provisions of ObamaCare enacted in 2010.

Though its acquisition of Equian in 2019 and the proposed $13 billion acquisition of health information technology conglomerate Change Healthcare in 2021, United came within an eyelash of a near monopoly on “intelligent” medical claims processing software. The Justice Department challenged this latter acquisition and United may agree to divest Change’s claims processing software business as a condition of closing the deal. Even without the Change acquisition, Optum Insight processes hundreds of millions of medical claims annually not only for United’s health insurance business but for many of United’s competitors.

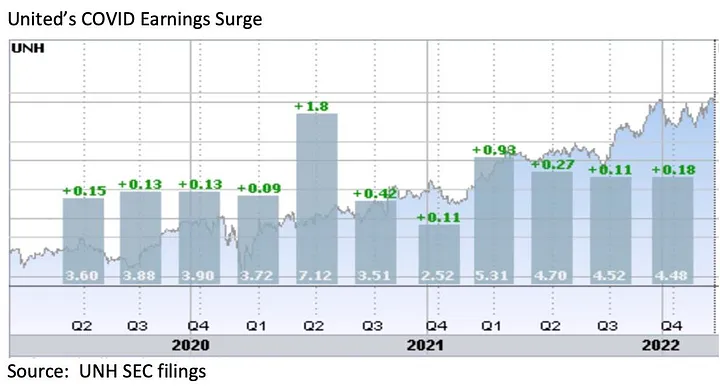

However, Optum Insight’s claims management system can also be used to increase MLR if medical expense unexpectedly declines, exposing the firm to federal requirement that it rebate excessive ‘savings’ to subscribers. This happened in 2020, when the COVID pandemic dramatically and unexpectedly added billions to United’s earnings due to hospitals suspending elective care. The chart below shows United’s 2Q2020 earnings per share almost doubling due to the precipitous drop in its medical claims expenses!

Hospital finance colleagues reported an immediate and substantial drop in medical claims denials from United and other carriers in the summer and fall of 2020. United’s quarterly profits dutifully and steeply declined in the subsequent two quarters, because its medical expenses sharply rebounded. The rise in

United’s medical expenses helped the firm avoid premium rebates to patients required by provisions of the ObamaCare legislation passed in 2010. The firm did voluntarily rebate about $1.5 billion to many of its customers in June, 2020.

However the most rapidly growing part of Optum Insight is its Optum 360 business process outsourcing business, which helps hospitals manage their billing and collections revenue cycle, as well as information technology operations, supply chain (purchasing and materials management) and other services. Through Optum 360, Optum Insight has signed five long term master contracts in the past two years’ worth many billions of dollars with care providers in California, Missouri and other states to provide a broad range of business services.

With all these different businesses, it is theoretically possible for one piece of Optum to be reducing a hospital’s cash flow by denying medical claims for United subscribers, while United’s health insurance network managers bargain aggressively to reduce the hospital’s reimbursement rates while yet another piece of Optum runs the billing and collection services for the same hospital and its employed physicians, while yet another piece of Optum competes with the hospital’s physicians and ambulatory services, diverting patients from its ERs and clinics, reducing the hospital’s revenues.

It is not difficult to imagine a future in which Optum/United offers hospital systems an Optum 360 outsourcing contract that run most of the business operations of a hospital system in exchange for preferred United health plan rates, an AI-enabled EZ pass on its medical claims denials and inpatient referrals from Optum physician groups and urgent care centers, at the expense of competing hospitals.

Managing these potential conflicts will be an increasing challenge as these various businesses grow, placing intense pressure on United’s leadership to get the various pieces of United to work together. To many anxious hospital executives, United resembles nothing so much as the Kraken, rising up out of the sea, surrounding and engulfing them- a powerful friend perhaps or a fearsome foe. As you might expect, United’s growing market power and growth has generated a fierce backlash in the hospital management community.

What Business is United Healthcare In?

United Healthcare is the most successful business in the history of American healthcare. The rapid growth of Optum and continued health insurance enrollment growth from government programs like Medicaid and Medicare has created a cash engine which generates nearly $2 billion a month in free cash flow. Optum’s portfolio has given United an impressive array of tools, unequalled in the industry, to improve its profitability and to reach into every corner of the US health system. United Healthcare is managed care on steroids.

United’s diversified portfolio of businesses gives the firm what a finance-savvy colleague termed “optionality”- the ability to redirect capital and management attention to areas of growth and away from areas that have ceased to grow, in the US or overseas. With its substantial investable capital, it will have the pick of the litter of the 11 thousand digital health companies as the overextended digital health market consolidates. United will be able to use its vast resources to build state-of-the-art digital infrastructure to reach and retain patients and manage their care.

United’s main short term business risks seem to be running out of accretive transactions effectively to deploy its growing horde of capital and managing the firm’s rising political exposure. United has had tremendous business discipline and has shied away from speculative acquisitions that are not immediately accretive to earnings. If its earnings growth falters, however, it will also encounter pressure from the investment community to increase dividends (presently about 1.2%) or share buybacks to bolster its share price, or else divest some or all of Optum in order to “maximize shareholder value”.

Answering the question, “What Business is United In” is simple: just about everything in health but hospitals and nursing homes.

Answering the questions- who are its customers and what do they want? — is a great deal harder. The customers United serves are in a sort of cold war with one another. United’s original business was protecting employers from health cost growth , and tempering the influence of hospitals and doctors by reducing their rates and utilization. By fostering so-called Consumer Directed Health Plans that expose many of their subscribers to very high front-end copayments, United and its health insurance brethren, have also increased their out-of-pocket costs, whether they have the savings to pay them or not.

There are also some ironies in United’s development. Optum Insight’s suite of hospital business services are designed to reduce administrative costs created in major part by United and other insurers’ medical claims data requirements. Its PBM business, originally intended to reduce drug spending by bargaining aggressively with pharmaceutical manufacturers has ended up pushing up drug list prices and consumer cost shares.

While presumably everybody benefits if United can somehow help patients become and remain healthy, it is still far from obvious how to do this. Managing all these markedly divergent customer needs will be a tremendous management challenge for whoever succeeds United’s reclusive (and very effective) 70 year old Chairman Stephen Hemsley.

What Does Society Get from this Vast Enterprise?

However, as Peter Drucker told a different generation of business giants, businesses are not entities unto themselves, accountable only to shareholders and customers. They are organs of society, and are expected to create social value. Americans are suspicious of vast enterprises, as businesses from Standard Oil, US Steel and ATT to Microsoft and Facebook have learned. As businesses grow and become more successful, public suspicion grows.

Private health insurers already face strident opposition from progressive Democrats, who believe that health coverage ought to be a public good, a right of citizenship provided publicly; in other words, that private health insurers have no business being in business. And large insurers like United also face intense opposition from hospitals and many physicians because they reduce their incomes and impose major administrative burdens upon them.

In the age of Twitter and TikTok, United is highly vulnerable to “event risks” that confirm the hostile narratives of the firm’s detractors that United is mainly about maximizing its own profits, not about improving the health of its subscribers or the communities it serves. It is not clear how many the tens of millions of United subscribers have warm and fuzzy feelings about their giant health insurer. Memories of the HMO backlash of the 1990’s reside in the firm’s corporate memory.

United has grown to its present immense scale largely without public knowledge. United has within its reach the capability of constraining overall health cost growth across dozens of metropolitan areas and regions, not merely cost growth for its own beneficiaries (roughly one in seven US citizens already get their health insurance through United). With its expanding digital health operations, it can deploy state of the art tools for helping United’s 50 million subscribers avoid illness and live healthier lives.

United also has the ability to damage the financial operations of beloved local hospitals and deny coverage to families, raising their out of pocket expenses. How United frames and defends its social mission and how it manages all the delicate and increasingly fraught customer relationships will determine its future, and in important ways, ours as well.

Starting June 1, UnitedHealthcare will require physicians to submit prior authorization requests for certain types of colonoscopies. While routine screening colonoscopies will remain exempt, United beneficiaries requiring surveillance or diagnostic colonoscopies—which are performed on patients at greater risk of developing colon cancer or those already exhibiting worrisome symptoms—will need advance approval for the procedures to be covered by the payer. A UnitedHealthcare spokesperson said that this policy change is due to concerns that colonoscopy overutilization generates unnecessary medical risks and higher healthcare spending for patients.

The American College of Gastroenterology released a statement criticizing the new policy on the grounds that prior authorization requirements create harmful delays for patients and are a significant source of provider burnout.

The Gist: So much for the planned rollback of prior authorizations that UnitedHealthcare recently touted.

While the insurer is not wrong in saying that some studies have documented overutilization of colonoscopies,

prior authorization is a blunt tool that takes care decision making out of practicing providers’ hands, redirecting that power (along with more profit) to the payer.

To process prior authorization requests in a timely manner, insurers now commonly rely on AI algorithms, which are an imperfect solution. For patients exhibiting signs of colon cancer,improper denials and delayed approvals for colonoscopies could have life-threatening implications.

The Cigna Group beat investor expectations and reported a 10 percent growth in membership year over year, according to the company’s first quarter earnings published May 5.

“Our strong results in the first quarter demonstrate how our company continues to execute well, while also introducing innovative, market-leading solutions that improve clinical outcomes, affordability and transparency for the benefit of those we serve,” Chair and CEO David Cordani said.

Total revenues in the first quarter were $46.5 billion, up 6 percent year over year.

Evernorth revenues rose 8 percent year over year to $36.2 billion. The insurance side of the business, Cigna Healthcare, reported first-quarter revenues of $12.8 billion, up 13 percent from the previous year.

In the first quarter, net income was $1.3 billion, up 6 percent year over year.

The company’s medical loss ratio was 81.3 percent in the first quarter, compared to 81.5 percent during the same period last year.

As of March 31, Cigna had 19.5 million total medical members, up 10 percent year over year.

For 2023, the company projects revenues of at least $188 billion. Full-year adjusted income from operations is projected to be at least $7.36 billion, or at least $24.70 per share.

American Medical Association President Jack Resneck Jr., MD, detailed in a post on the medical group’s website the “Kafkaesque” prior authorization process that an unnamed insurance company allegedly put one of his patients through.

Dr. Resneck, a San Francisco-based dermatologist, was treating a patient with severe head-to-toe eczema, who was unable to sleep because of the condition, according to the post. Dr. Resneck found a medication that allowed the patient to sleep and return to work.

Several months later, however, the patient was unable to get the prescription refilled at the pharmacy, according to the report. Dr. Resneck completed the paperwork describing how well the patient had responded to the medication, as required by the insurance company, and faxed it over. The prior authorization request for the prescription refill was rejected.

Dr. Resneck said the insurance company rejected the refill on the grounds that the patient no longer met the severity criteria because not enough of his body was covered and he was not missing enough sleep.

The insurance company allegedly wanted to take the patient off the medication for several weeks to let his eczema flare up again, according to the post. It took more than 20 additional telephone calls until the patient’s prescription was refilled.

Embattled insurtech Bright Health will fully ax its insurance business as a potential bankruptcy looms, the company announced Friday.

The company secured an extension to its credit facility through June 30, giving it a few extra months to avoid going belly-up. To ensure it qualifies for the extension, the company must find a buyer for its California-based Medicare Advantage (MA) business by the end of May, according to a filing with the Securities and Exchange Commission.

Bright Health revealed March 1 that it had overdrawn its credit and would need to secure $300 million by the end of April to stay afloat.

The MA business includes nearly 125,000 California seniors across its Brand New Day and Central Health Plan brands. In the announcement, Bright said the sale would “substantially bolster” its finances.

“Since our founding, Bright Health has worked to make healthcare simpler, more personal and affordable for consumers,” CEO Mike Mikan said in the announcement. “As our markets evolve, we are taking steps to adapt and ensure our businesses are best positioned for long-term success.”

Manny Kadre, lead independent director of Bright Health’s board of directors, said in the announcement that the company has “received inbound interest” about the California MA business as it explores its options.

With the full divestiture of its insurance business, that means Bright Health will be all-in on its NeueHealth care delivery services. Mikan said in the announcement that the segment performed well in the first quarter and has grown to serve about 375,000 value-based care customers.

As Bright shops for a buyer for its MA plans, it’s also continuing to unwind the ACA business, a process that hit a snag as it was hit with a lawsuit from Oklahoma-based health system SSM Health, which alleged that the insurer owed it more than $13 million in unpaid claims.

Bright Health is also under the gun to boost its stock price, as the New York Stock Exchange has threatened to delist its shares. Shares in the company were trading at 17 cents on Friday afternoon.