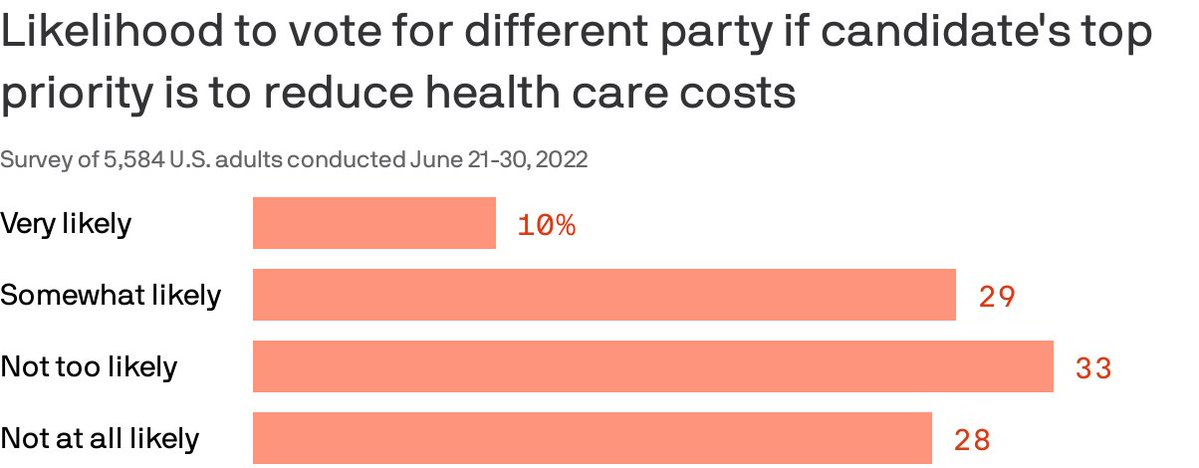

Almost 40% of Americans are willing to split their ticket and vote for a candidate from the opposing party who made a top priority of lowering health costs, according to a Gallup/West Health poll published Thursday.

Why it matters: Though candidates haven’t been talking much about medical costs in the run-up to the midterms, the issue remains enough of a priority that it could erode straight party-line voting.

By the numbers: 87% of Americans polled said a candidate’s plan to reduce the cost of health care services was very or somewhat important in casting a vote.

The issue cut across partisan lines, with 96% of Democrats and 77% of Republican respondents saying a candidate with a health care costs plan was an important factor.

86% also said a plan to lower prescription drug prices is very or somewhat important. That’s especially true for seniors.

Of note: Democratic voters were more likely than Republicans to say they would cross party lines because health costs are a top priority. Four in 10 Democrats said they were likely to do so compared to about 1 in 5 Republicans.

Before 2011, Medicare Advantage health plans absorbed a greater share of Medicare enrollment because traditional Medicare enrollees were transitioning to Medicare Advantage plans. From 2011 to 2019, Medicare Advantage enrollment continued to increase but the source changed.

The researchers used the Master Beneficiary Summary File from 2011 to 2019 to inform their study of the source of Medicare Advantage enrollment during that timeframe. These files provided over 524.4 million person-years.

Medicare Advantage still drew enrollees from traditional Medicare from 2012 to 2019, with the share of those who came from Medicare Advantage growing from 65.9 percent to 71.1 percent.

The number of enrollees that were new to Medicare who chose Medicare Advantage coverage also grew. A little over 18 percent of enrollees who did not have Medicare coverage previously transitioned into Medicare Advantage in 2012. But by 2019, that share had swelled to 24.7 percent.

Beneficiaries who switched to Medicare Advantage from traditional Medicare tended to be older. Fewer of them identified as Hispanic individuals but more of them identified as Black individuals. Additionally, they were more likely to be dually eligible and more likely to have a disability. Finally, they were more likely to die within two years of enrolling in Medicare Advantage.

“Our study is limited in that it was not designed to examine these mechanisms,” the researchers acknowledged. “As MA continues to grow, understanding the reasons for switching from TM to MA will become more important.”

Although the study did not explicitly explore the causes behind these enrollment shifts, the researchers cited three factors that might contribute to the growth and diversity of the Medicare Advantage population.

First, they noted that Medicare Advantage plans offer supplemental benefits and dental and vision coverage, which traditional Medicare does not cover.

In 2022, more Medicare Advantage plans offered more supplemental benefits, including special supplemental benefits for the chronically ill (SSBCI), expanded supplemental benefits, and traditional supplemental benefits, according to a Better Medicare Alliance brief.

Second, Medicare Advantage plans offer lower out-of-pocket healthcare spending compared to traditional Medicare.

Finally, Medicare Advantage might be more attractive due to the lower premiums.

In 2022, costs were particularly low since Medicare Advantage premiums dropped to the lowest level in 15 years, 10 percent lower than in 2021, the Better Medicare Alliance report shared.

The results corroborate separate studies that show that the Medicare Advantage population is growing and becoming more diverse.

In more than 100 congressional districts, Medicare Advantage coverage represents half or more of enrollment, according to Better Medicare Alliance research. Medicare Advantage coverage is particularly strong in Alabama, Michigan, and Florida.

Medicare Advantage plans grew 60 percent from 2013 to 2020. By 2020, Medicare Advantage plans served 25 million seniors, of which six out of ten were women. Also, more than half of all Hispanic American seniors (52 percent), 49 percent of African American seniors, and 35 percent of Asian Americans selected Medicare Advantage plans for their coverage.

Despite the hype, accountable care organizations (ACOs) and other Medicare-driven payment reform programs intended to improve quality and lower healthcare spending haven’t bent the cost curve to the extent many had hoped.

A recent and provocative opinion piece in STAT News, from health policy researcher Kip Sullivan and two single-payer healthcare advocates, calls for pressing pause on value-based payment experimentation. The authors argue that current attempts to pay for value have ill-defined goals and hard-to-measure quality metrics that incentivize reducing care and upcoding, rather than improving outcomes.

The Gist: We agree with the authors that current value-based care experiments have been disappointing.

The intention is good, but the execution has been bogged down by entrenched industry dynamics and slow-to-move incumbents. One fair criticism: ACOs and other “total cost management” reforms largely focus on the wrong problem. They address utilization, rather than excessive price.

But we’re having a price problem in the US, not a utilization problem.Europeans, for example, have more physician visits each year than Americans, yet spend less per-person on healthcare. It’s our high prices—for everything from physician visits to hospital stays to prescription drugs—that drive high healthcare spending.

The root cause: our third-party payer structure actively discourages real efforts to lower price—every player in the value chain, including providers, brokers, and insurers, does better economically as prices increase. That’s why price control measures like reference pricing or price caps have been nonstarters among industry participants.

Recent reforms that increase price transparency, while not the entire solution, at least shine a light on the real challenges our healthcare system faces.

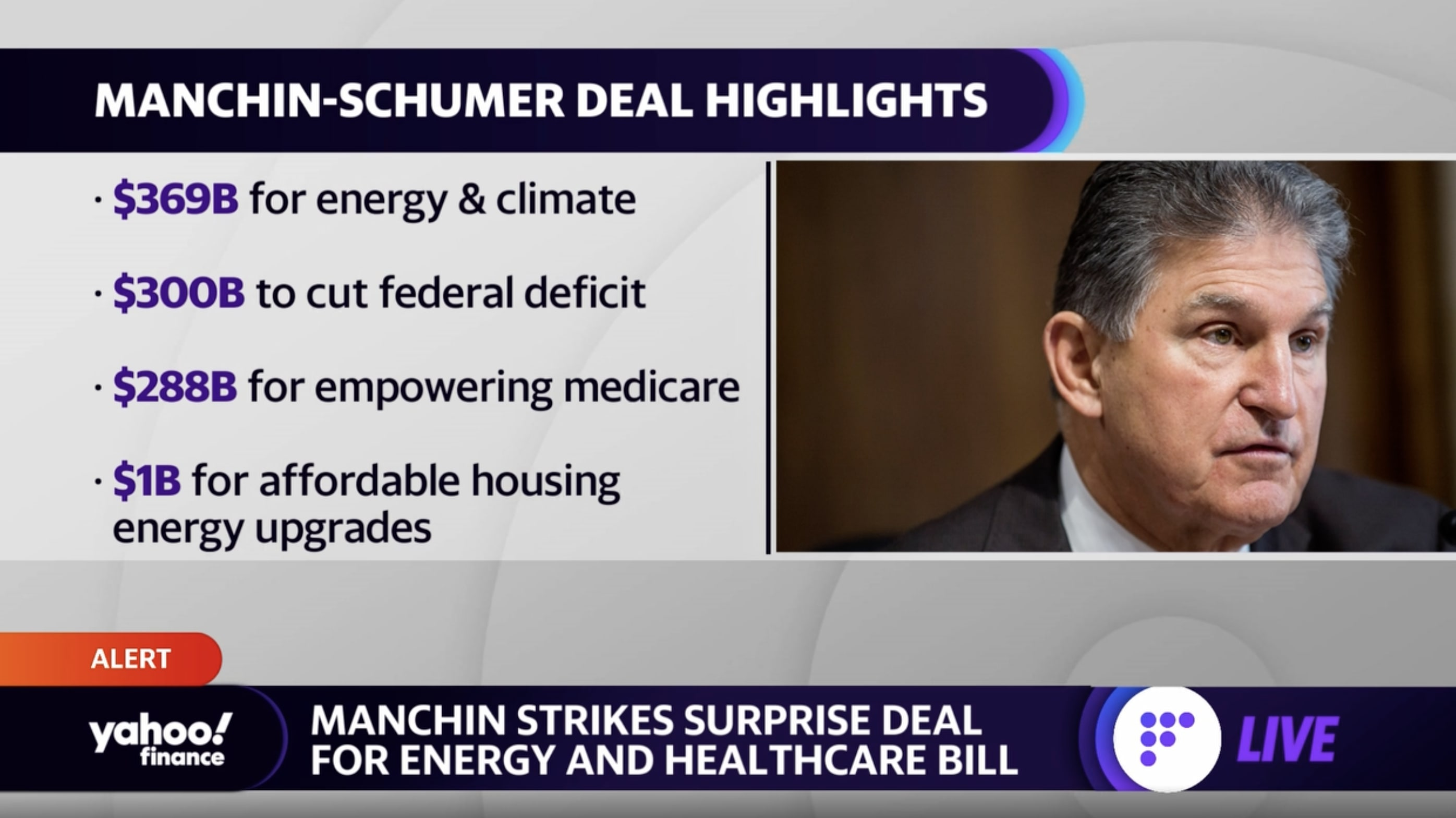

Senate Majority Leader Chuck Schumer (D-NY) and Senator Joe Manchin (D-WV) surprised everyone Wednesday night by announcing they reached a deal on a legislation package called the Inflation Reduction Act of 2022. The deal is a revival of portions of President Biden’s “Build Back Better” plan, more narrowly scoped to meet the demands of Sen. Manchin.

On the healthcare front, the bill would allow Medicare to negotiate prices for certain prescription drugs starting in 2026, and limit seniors’ annual out-of-pocket spending on Part D prescriptions to $2,000. It also includes $64B to extend the enhanced tax credits for Affordable Care Act exchange plans through 2025, avoiding health plan rate increases for millions of Americans.

The Gist: While several Senate Democrats have announced support for the legislation, the party can’t afford any holdouts given its razor-thin majority. If all Democrats get on board, this legislation will fulfill the party’s longtime promise to lower prescription drug prices. But it stops well short of other major healthcare measures being discussed last year, including expanding Medicare coverage to include dental, vision, and hearing coverage, and closing the so-called Medicaid coverage gap.

After a few years of relatively unchanged monthly premiums, a Kaiser Family Foundation analysis of 72 rate filings for 2023 finds a median 10 percent increase. Insurers say the biggest driver is rising medical costs, driven by higher rates for provider services and pharmaceuticals, as well as a return to pre-pandemic utilization levels. Insurers aren’t expecting COVID-19 or federal policy changes—including a potential extension of enhanced subsidies—to have much of an impact on rates.

The Gist:High inflation and the growing wage-price spiral have left providers with much higher costs, which is sure to drive up the overall cost of healthcare. Where provider systems have the leverage to demand higher rates from insurers, this will inevitably drive up premiums—an effect that is already starting to show up in the individual insurance market.

If Congressional Democrats are able to extend ACA subsidies, most ACA enrollees won’t actually feel these premium increases, but as contracts in the group market come up for renewal, we’d expect inflation in employer-sponsored premiums as well. Given the cost-sharing now built into most benefit plans, individual consumers will likely see healthcare join gas, food, and housing as household costs that are experiencing unsustainable inflationary increases.

Healthcare costs are becoming an increasing source of stress for older Americans, leading to some paring back on treatment, medicines or other spending on food and utilities — or skipping them altogether — to cover medical costs, according to new research conducted by Gallup in partnership with West Health.

The survey of U.S. adults released Wednesday found that almost half of adults aged 50 to 64 and more than a third of adults 65 and older are concerned they won’t be able to pay for needed healthcare services in the next year. That’s nearly 50 million older Americans.

About 80 million adults above age 50 see healthcare costs as a financial burden. Becoming eligible for Medicare seems to assuage those worries slightly, however: 24% of adults aged 50 to 64, who are not yet eligible for the federal health insurance, said health costs were a major burden. That percentage fell to 15% for those aged 65 and above.

Dive Insight:

The West Health-Gallup survey, conducted in September and October of 2021, is the latest vignette of how exorbitant healthcare costs in the U.S. are increasingly impacting the financial stability of Americans, especially those of retirement age who are more likely to have expensive medical needs.

Out-of-pocket healthcare expenses for adults aged 65 and older increased 41% from 2009 to 2019, according to HHS data. That population spends on average almost double their total expenditures on healthcare costs compared with the general population, despite Medicare coverage.

That cost problem is only likely to worsen amid surging inflation raising the cost of groceries, gas and other needed items. Additionally, U.S. demographics shifts are an added stressor. By 2030, the percentage of Americans 65 years and older will outweigh those under the age of 18, a first in the country’s history, according to Census Bureau projections.

“As sizable numbers of Americans 65 and older face tangible tradeoffs to pay for healthcare, many more Americans in the next decade will incur health and financial consequences because of high costs,” researchers wrote in the report.

The West Health-Gallup poll found about one in four adults aged 65 and above cut back on food, utilities, clothing or medication to cover healthcare costs. That’s compared to three in 10 for adults aged 50 to 64.

Older women and Black adults were more likely to forgo basic necessities to pay for healthcare than other demographics.

More than 20 million Americans aged 50 years and above said there was a time within the last three months when they or a family member was sick, but didn’t seek treatment due to cost.

More than 15 million Americans said they or a family member skipped a pill or dose of prescribed medicine in order to save money.

Researchers urged policymakers to act to improve efficiency and reduce the costs of medical care and prescription drugs in the U.S. Congress has yet to take meaningful action to lower medical costs, despite rising support for government intervention and high-profile proposals from the Biden administration.

Part of the reason why medical debt is so high is because many Americans don’t have enough savings to pay their deductibles and other out-of-pocket costs, according to a second KFF analysis.

Driving the news: Health insurance plans’ out-of-pocket limits prevent enrollees from paying limitless sums of money for medical care. But that doesn’t mean they protect people from having to pay several thousands of dollars — which not everyone has lying around.

Deductibles alone, which people must pay before coverage for most services kicks in, are frequently thousands of dollars and can exceed the amount of liquid assets a household has.

By the numbers: Over 40% of multi-person households can’t cover a mid-range employer family plan deductible of $4,000, and 61% don’t have enough to cover a high-range deductible.

The ability to pay out-of-pocket costs varies significantly by income.

Americans owe at least $195 billion of medical debt, despite 90% of the population having some kind of health coverage, according to new research from the Peterson Center on Healthcare and the Kaiser Family Foundation.

Why it matters: People are spending down their savings and skimping on food, clothing and household items to pay their medical bills, Adriel writes.

About16 million people, or 6% of U.S. adults, owe more than $1,000 in medical bills, and 3 million people owe more than $10,000.

The financial burden falls disproportionately on people with disabilities, those in generally poor health, Black Americans and people living in the South or in non-Medicaid expansion states, per the research.

Go deeper: 16% of privately-insured adults say they would need to take on credit card debt to meet an unexpected $400 medical expense, while 7% would borrow money from friends or family, per the research, which focused on adults who reported having more than $250 in unpaid bills as of December 2019.

It’s not yet clear how much the pandemic and the recession factor into the picture, in part because many people delayed or went without care. There also was a small shift from employer-based coverage to Medicaid, which has little or no cost-sharing.

While the new federal ban on surprise billing limits exposure to some unexpected expenses, it only covers a fraction of the large medical bills many Americans face, the researchers say.