Stillwater Medical Center in Oklahoma has ended all in-network contracts with Medicare Advantage plans amid financial challenges at the 117-bed hospital, the Stillwater News Press reported Oct. 14.

Humana and BCBS of Oklahoma were notified that their members will no longer receive in-network coverage after Jan. 1, 2023.

“BCBSOK is willing to work with Stillwater Medical Center in finding solutions that will allow Payne County residents continued local access to Medicare Advantage providers,” a BCBS spokesperson told the newspaper.

The hospital said it made the decision after facing rising operating costs and a high prior authorization burden for the MA plans.

“This was a very tough financial decision for the Stillwater Medical leadership team. Our cost to operate has increased 26 percent over the past 2 years,” Tamie Young, vice president of revenue cycle at SMC, told the News Press. “Financial challenges are increased by a 22 percent denial of service rate from Medicare Advantage plans. This is in comparison to a less than 1 percent denial rate from traditional Medicare.”

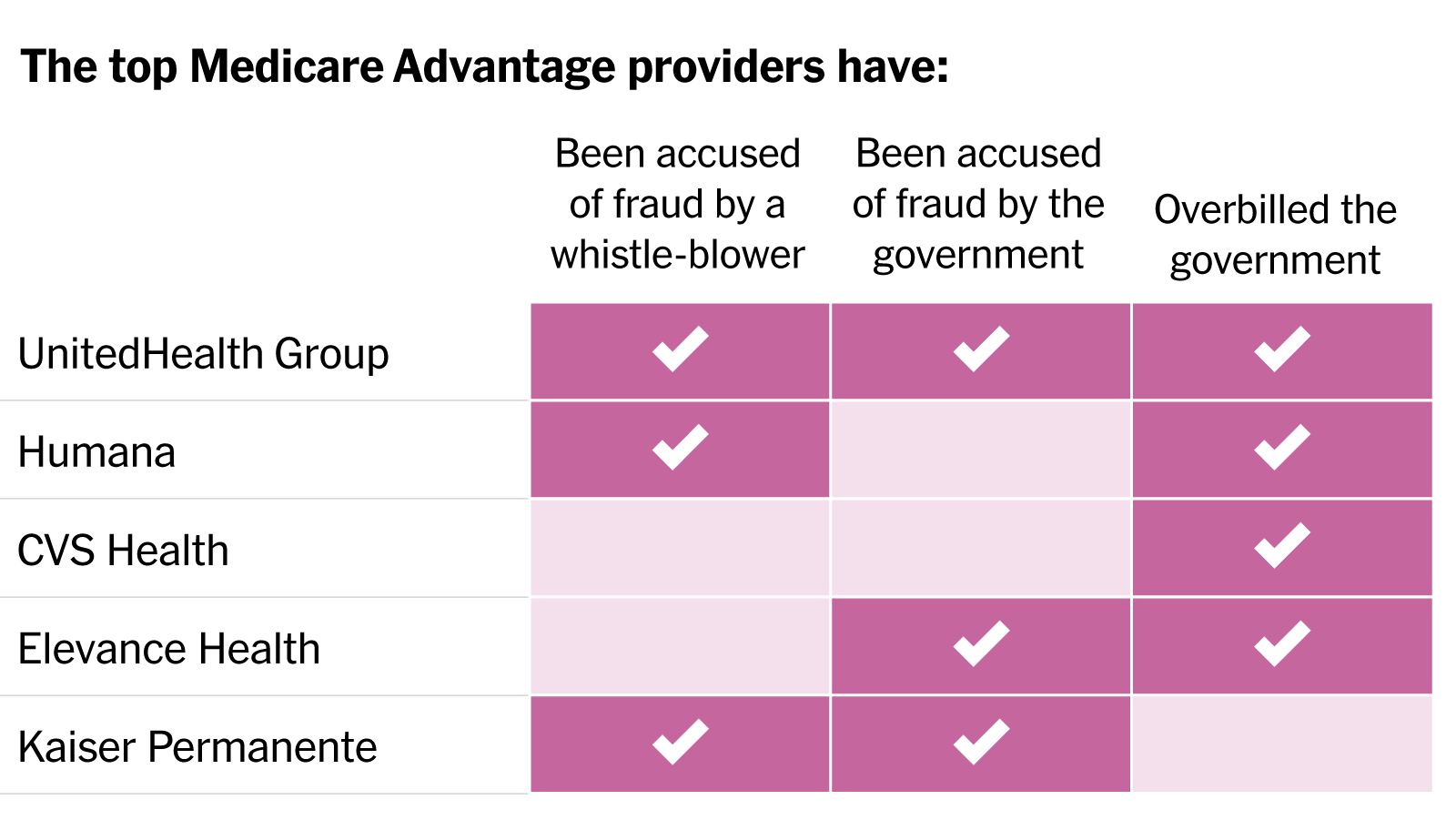

In a blistering article published in the New York Times, reporters Reed Abelson and Margot Sanger-Katz detail widespread fraud allegations involving the nation’s largest MA insurers. Nine of the ten largest plans have been accused by the government of fraud or overbilling, generally for upcoding practices that exaggerate the disease burden among their beneficiaries, without providing them more care. Insurers have disputed most allegations, and regulators have been slow to punish known infractions. As a growing steam of seniors continue the enter the program, aggressive risk adjustment has significantly increased the government’s costs. The Centers for Medicare and Medicaid Services has yet to reduce payments in response to overbilling, despite having the power to do so.

The Gist: While these practices were well known to many in the healthcare industry, MA’s growth—set to overtake traditional Medicare enrollment next year—has added a spotlight worthy of national attention. While many beneficiaries report being satisfied with their MA benefits, the program was also intended to improve the cost efficiency of senior care.

With payers gaming the system to garner record profits, the government has seen higher per-enrollee spending in MA compared to traditional Medicare. There are some signs that the strings are starting to tighten for insurers, as many of the largest are losing Medicare star bonuses in 2023, impacting both plan revenue and ability to market throughout the year. However, reduced quality bonuses change nothing about the underlying MA payment structure, and could even drive insurers to more profit-seeking behavior.

The nation’s largest retailer and its largest insurer announced a 10-year partnership to bring together the collective expertise of both companies to provide affordable healthcare to potentially millions of Americans. Set to start next year with 15 Walmart Health locations in Georgia and Florida, the collaboration will initially focus on seniors and Medicare Advantage (MA) beneficiaries, and will include a co-branded MA plan in Georgia. Walmart Health Virtual Care will also be in-network for some UnitedHealthcare beneficiaries. Plans for future years involve expanding the collaboration across commercial and Medicaid plans, as well as including pharmacy, dental, and vision services.

The Gist: We have long wondered if this powerhouse pairing was in the works, as this kind of partnership makes a lot of sense for both parties. While Walmart has reportedly been considering an insurance company acquisition for years, and more recently been dabbling in its own insurance efforts, partnering with UHG provides the retailer with a share of the upside potential of getting into the insurance market without having to fully commit to entering that complex business. And given that 90 percent of Americans live within 10 miles of a Walmart store, and more than half of Americans visit a store every week, Walmart provides UHG with low-cost healthcare access points all over the country, especially important in markets where United’s own Optum physician network is not (yet) present.

Before 2011, Medicare Advantage health plans absorbed a greater share of Medicare enrollment because traditional Medicare enrollees were transitioning to Medicare Advantage plans. From 2011 to 2019, Medicare Advantage enrollment continued to increase but the source changed.

The researchers used the Master Beneficiary Summary File from 2011 to 2019 to inform their study of the source of Medicare Advantage enrollment during that timeframe. These files provided over 524.4 million person-years.

Medicare Advantage still drew enrollees from traditional Medicare from 2012 to 2019, with the share of those who came from Medicare Advantage growing from 65.9 percent to 71.1 percent.

The number of enrollees that were new to Medicare who chose Medicare Advantage coverage also grew. A little over 18 percent of enrollees who did not have Medicare coverage previously transitioned into Medicare Advantage in 2012. But by 2019, that share had swelled to 24.7 percent.

Beneficiaries who switched to Medicare Advantage from traditional Medicare tended to be older. Fewer of them identified as Hispanic individuals but more of them identified as Black individuals. Additionally, they were more likely to be dually eligible and more likely to have a disability. Finally, they were more likely to die within two years of enrolling in Medicare Advantage.

“Our study is limited in that it was not designed to examine these mechanisms,” the researchers acknowledged. “As MA continues to grow, understanding the reasons for switching from TM to MA will become more important.”

Although the study did not explicitly explore the causes behind these enrollment shifts, the researchers cited three factors that might contribute to the growth and diversity of the Medicare Advantage population.

First, they noted that Medicare Advantage plans offer supplemental benefits and dental and vision coverage, which traditional Medicare does not cover.

In 2022, more Medicare Advantage plans offered more supplemental benefits, including special supplemental benefits for the chronically ill (SSBCI), expanded supplemental benefits, and traditional supplemental benefits, according to a Better Medicare Alliance brief.

Second, Medicare Advantage plans offer lower out-of-pocket healthcare spending compared to traditional Medicare.

Finally, Medicare Advantage might be more attractive due to the lower premiums.

In 2022, costs were particularly low since Medicare Advantage premiums dropped to the lowest level in 15 years, 10 percent lower than in 2021, the Better Medicare Alliance report shared.

The results corroborate separate studies that show that the Medicare Advantage population is growing and becoming more diverse.

In more than 100 congressional districts, Medicare Advantage coverage represents half or more of enrollment, according to Better Medicare Alliance research. Medicare Advantage coverage is particularly strong in Alabama, Michigan, and Florida.

Medicare Advantage plans grew 60 percent from 2013 to 2020. By 2020, Medicare Advantage plans served 25 million seniors, of which six out of ten were women. Also, more than half of all Hispanic American seniors (52 percent), 49 percent of African American seniors, and 35 percent of Asian Americans selected Medicare Advantage plans for their coverage.

A recent piece in the Harvard Business Review demonstrates how SCAN Health Plan, a not-for-profit, California-based Medicare Advantage plan with over 270,000 members, was able to increase medication adherence among Black and Hispanic beneficiaries. Dr. Sachin Jain, CEO of SCAN, and his colleagues describe how identifying the specific causes of disparities in medication adherence, establishing clear financial incentives for senior leaders, and targeting investments enabled the insurer to reduce disparities by 35 percent within eighteen months.

The Gist: Addressing complex and longstanding racial health disparities is an incredibly difficult but vital task. While there’s been plenty of discussion about the problem, there’s been a lack of effective solutions for healthcare organizations to deploy.

SCAN’s progress demonstrates how narrowing the focus down to a more specific issue can yield faster results. Jain and his colleagues write that SCAN’s next areas of focus are reducing disparities in diabetes control and flu vaccinations. We’re looking forward to learning about other innovative ways healthcare organizations are tackling long overdue gaps in care.

With a closely divided Congress, President Biden has leaned heavily on regulatory actions to advance his healthcare priorities. With the midterm elections fast approaching, the graphic above assesses the impact of those actions, and outlines which legislative components Democrats may still try to pass before November.

From the start, the administration has signaled the importance of promoting competition in healthcare markets, and has devoted more scrutiny to hospital mergers—while leaving most attempts at vertical integration unchallenged. Through Medicaid waivers, it has worked to expand insurance coverage, rolling back Trump-era work requirements, expanding postpartum coverage, and encouraging states to experiment with public option plans on the Affordable Care Act (ACA) exchanges.

The Centers for Medicare and Medicaid Services (CMS) has continued the steady march toward value programs, revising the Direct Contracting model to factor in health equity. Despite these incremental moves, Medicare Advantage (MA) remains the focus of long-term efforts to control Medicare spending, and MA programs have seen payments boosts year-over-year.

Meanwhile, the fate of President Biden’s signature healthcare campaign promises remains in the hands of an intransigent Congress. Senate Democrats are currently trying to negotiate a deal on a bill allowing Medicare drug negotiations and extending ACA subsidies, an important provision to protect millions from receiving premium hike notices just weeks before Election Day.

Concierge primary care company One Medical is reportedly considering a sale after receiving interest from CVS Health, according to Bloomberg. While talks with CVS are no longer active, sources familiar with the situation say the company is weighing offers from other suitors. Also this week, there were rumors that Humana is interested in acquiring Florida-based Cano Health, which provides comprehensive care to over 200K seniors enrolled in Medicare Advantage plans across six states.

The Gist: We’ve long thought that the ultimate buyer for these primary care startups would be large, vertically integrated insurers, as many have struggled to achieve profitability while maintaining strong enrollment growth.

Competition among insurers to acquire care delivery assets has intensified, as payers look to Medicare Advantage as their primary growth vehicle, and aim to amass primary care networks capable of managing their growing senior care businesses.

As part of the 2023 Physician Fee Schedule proposed rule, the Centers for Medicare & Medicaid Services (CMS) outlined major changes to the Medicare Shared Savings Program (MSSP), with the goals of increasing participation in the program and improving health equity.

The agency hopes their revisions to the benchmarking methodology, which will advantage smaller accountable care organizations (ACOs) and those enrolling large numbers of underserved beneficiaries, will change the trajectory of the program.

With participation among providers stagnating in recent years, the new rules represent a recognition from CMS that MSSP, in its current form, is likely to increase spending rather than generate significant savings. The rule also includes a 3.9 percent decrease in the “conversion factor” for physician payment, which has already drawn outrage from the American Medical Association and other physician groups.

The Gist:There is little reason to expect that these modifications—as significant as they are—will be meaningful to beneficiaries or to the Medicare program’s overall sustainability. Although it is heartening to see CMS admit that ACOs are on course to violate the statutory requirement that the program not increase spending, the proposed changes would net only $14.8B in savings over a twelve-year period—a rounding error for a program that spent $830B in 2020 alone. Meanwhile the 11M beneficiaries attributed to MSSP ACOs are dwarfed by the 28M enrolled in MA.

For many health systems and physician groups—particularly those who are most progressive in managing risk—MSSP is now a sideshow to their Medicare Advantage (MA) strategies. The federal government has made two “bets” on how to lower health spending for seniors, and the dollars spent on enticing insurers to grow their MA businesses (in the form of subsidies) far outweigh the effort to encourage provider participation in ACOs—a clear sign of Medicare’s priorities.

But with MA currently not generating savings compared to fee-for-service Medicare, cuts in per-beneficiary spending in MA will be necessary to achieve savings in the long term.

Political will seems to be growing to reshape the increasingly popular Medicare Advantage program.

At a House Energy and Commerce committee hearing on Tuesday, lawmakers on both sides of the aisle called for more oversight of MA following watchdog reports that found impediments to receiving covered care, including improper denials of prior authorization requests, and plans gaming the system in exchange for more funding from Medicare.

“Medicare Advantage is an important tool for helping seniors and we want it to succeed. We’re going to continue to conduct the oversight necessary,” said Oversight and Investigations Subcommittee Chair Diana DeGette, D-Colo.

Witnesses at the hearing — officials from the Government Accountability Office, HHS Office of Inspector General and congressional advisory board MedPAC — also pointed to higher rates of beneficiary disenrollment in their last year of life and opaque plan data, which can complicate oversight efforts.

Surveys have shown MA remains extremely popular with beneficiaries, attracted by lower co-pays and supplemental benefits like vision coverage and telehealth. In the program, Medicare pays private plans a capitated monthly rate to provide care for their beneficiaries based on the severity of their beneficiaries’ needs.

The hearing comes amid inflamed industry debate over the future of MA.

For-profit hospital lobby Federation of American Hospitals submitted a letter for the record sharing concerns over some MA plans denying patient care and having inadequate care networks.

Meanwhile, MA trade group Better Medicare Alliance sent a letter to the CMS on Monday urging the agency to safeguard the program as Congress mulls changes to Medicare.

But as Medicare’s hospital benefit — part of which funds MA — limps towards insolvency, lawmakers appear poised to target the growing MA program in a bid to crack down on improper payments and care denials.

“This is something that I think is very much bipartisan,” said Rep. Gary Palmer, R-Ala.

Coverage delays and denials

It’s not the first time lawmakers have zeroed in on MA oversight as a strategy to save Medicare money: In a Senate hearing on Medicare insolvency in February, Sen. Elizabeth Warren, D-Mass., said “the Medicare system is hemorrhaging money on scams and frauds” due to insurers taking advantage of the program’s rules to increase profits.

Even amid rising congressional criticism of MA, lawmakers on Tuesday reiterated their support for the program overall, which covered roughly 27 million Americans in 2021.

That’s more than a third of all Medicare beneficiaries, though MA is expected to swell to cover half of all Medicare members by 2030.

But lawmakers said they are increasingly concerned about disparities in the quality of coverage offered by Medicare Advantage plans compared to traditional Medicare plans, along with unscrupulous practices in the program resulting in higher reimbursement for MA organizations.

A GAO report found MA beneficiaries in their last year of life disenroll from MA in favor of traditional Medicare at a rate two times higher than other MA members, suggesting the plans may not support high-cost and specialized care, testified Leslie Gordon, GAO’s acting director for healthcare.

Gordon called it a “red flag” for the program that requires more scrutiny from CMS.

In addition, an HHS OIG report published April found MA organizationswrongly denied members care, with plans turning down 18% of payment requests that should have been approved.

Erin Bliss, OIG assistant inspector general in the Office of Evaluation and Inspection, testified plans sometimes use internal critical criteria that are not required by Medicare. In one example, an MA plan denied a medically necessary CT scan to diagnose a serious disease, citing that the patient hadn’t yet received an x-ray, Bliss said.

When appealed, plan denials were reversed 75% of time, a rate DeGette called “alarmingly high.”

“We are concerned that patients are receiving the timely care they need in those situations,” Bliss said.

OIG also found plans denied 13% of prior authorization requests that would have been approved under traditional Medicare.

Rep. Michael Burgess, R-Texas, suggested policymakers consider requiring insurers to forego prior authorization for doctors with a consistent track record of submitting accurate data. That strategy, called “gold carding,” is already used in some states, including Texas and West Virginia, to pare back on prior authorization delays.

MA payment reform

Along with coverage restrictions, lawmakers at Tuesday’s hearing asked witnesses about the scope and severity of improper MA payments in a bid to zero in on specific solutions Congress and the CMS can enact.

Though MA has potential to save the Medicare program money, “the current incentives for MA plans are not adequately aligned with the Medicare program,” said James Mathews, MedPAC executive director.

“Substantial reforms are urgently needed,” especially in light of Medicare’s “profound” financial problems, Mathews said.

In 2022, the average MA plan bid was 85% of fee-for-service spending, Mathews said. However, Medicare pays plans 104% of fee-for-service costs.

That imbalance is partially due to plans making patients appear sicker than they are to get extra payments from the government, witnesses said. The practice, called “coding intensity,”resulted in an estimated $12 billion in excess Medicare spending in 2020, according to MedPAC data.

Methods include chart reviews, where plans identify and add patient diagnoses that aren’t included in the service record, and health risk assessments, where plans contract with vendors to visit beneficiaries homes and conduct assessments, finding new diagnoses that often aren’t backed up by other records, according to Bliss.

GAO estimates that roughly a tenth of Medicare payments to MA plans in 2021 were improper, Gordon said.

To try to tamp down on coding intensity, the CMS should conduct targeted oversight of MA plans that routinely use these tools, and reassess whether chart reviews and in-home assessments are allowed to be sole sources of diagnoses for payment purposes, witnesses said. In addition, MA should improve care coordination for enrollees who receive health risk assessments.

The CMS should also consider replacing the quality bonus program and change its approach to calculating MA benchmarks, Mathews said.

In addition, the agency should require and validate data for completeness and accuracy before risk-adjusting payments through methods like medical record reviews, Gordon said.

Gordon also suggested the agency conduct more timely audits, as the CMS is currently missing out on recouping hundreds of millions of dollars in improper payments.

Policymakers appeared open witnesses’ suggestions to ensure MA is running as smoothly as possible, with Rep. Frank Pallone, D-N.J., calling for an additional hearing on the matter.

“This is bipartisan … You can be assured that we’re going to be following up,” DeGette said.

Social factors impact a person’s health and their potential health outcomes. While this has long been discussed (especially by folks of color, individuals with lived experiences, and those in public health), it is finally now getting deserved mainstream attention, including by health insurers.

Medicare Advantage (MA) — a program that offers private plan alternatives to traditional Medicare — is one key player looking at social determinants of health. It’s a good thing, too; an estimated 42% of the Medicare population are enrolled in MA plans, and that share grows each year. MA plans have more flexibility in offering supplemental benefits and services, some of which can address social determinants of health.

In 2018, the Creating High-Quality Results and Outcomes Necessary to Improve Chronic (CHRONIC) Care Act passed with bipartisan support and marked a substantial shift in MA policy by including acknowledgment of the role of social determinants of health. It allows even greater flexibility for MA plans to help with the very conditions that impact how a person lives, such as providing financial assistance for nutritional needs, transportation to appointments, caregiver support, and even home construction projects. Interestingly, it does not mandate coverage, so it is still dependent on what plans an individual has access to and how health plans are choosing to move forward with this freedom.

The problem is, however, that most individuals aren’t eligible for Medicare until age 65 (there are some exceptions). If we wait until Medicare eligibility to act on social determinants of health, are we waiting too long?

The short answer is yes. Although addressing social determinants of health in the Medicare-eligible population is important, what we know suggests that more could be done earlier.

Why are social determinants important in Medicare Advantage?

Chronic disease is a significant issue among Medicare-eligible individuals, and one that’s exacerbated by social determinants of health. There are substantial implications for both beneficiaries and MA plans. For beneficiaries, chronic disease affects not only their quality of life, but also their wallet. From the plans’ perspectives, the presence of comorbid chronic diseases is a significant differentiator between so called “high cost” beneficiaries and those who are not.

Current MA enrollment trends also point to the need to sharpen the focus on social determinants of health. Although they make up a minority of MA enrollees, persons of color are enrolling in MA plans at a breakneck pace: especially among Black people, dual enrollees, and people living in disadvantaged neighborhoods.

Historically, these are folks most negatively impacted by social determinants of health, and the likelihood of poor health outcomes is only compounded when enrollees reside in disadvantaged neighborhoods. These are neighborhoods commonly characterized by high concentrations of poverty, crime, and harmful environmental exposures compounded by limited resources to support economic and social well-being, and research has consistently found strong associations between neighborhood disadvantage and health risks and outcomes.

Health systems must do more about social determinants earlier in life

Social determinants of health affect us all — regardless of age. Until recently, they have received relatively little attention from insurers.

It is difficult though to discern the extent that these actions are altruistic or opportunistic, especially when they can technically be both. While that might not be the worst thing, it does matter if it leaves out the very people it should be helping.

Let’s consider internet access, for example. If a patient isn’t connected to the web, they can’t participate in a telehealth visit, leaving in-person care as the only option. In a world where telehealth visits are reimbursed at a fraction of the in-person rate, there are substantial cost savings (read: profit) associated with facilitating and promoting virtual care. Critics have also pointed out that most of these steps can be attributed to insurers’ philanthropic apparatuses as opposed to any substantive change or innovation in member benefits.

What is also becoming readily apparent, is that while telehealth use is increasing, it does not make care accessible for everyone. It could even serve to increase disparities if it is not done properly.

However, administrative hurdles and societal stigma can challenge people’s willingness to participate in these programs no matter how beneficial they might be. We should all be asking what more the health system — providers, payers, and government — should be doing to improve social determinants of health earlier in life.

The CHRONIC Care Act has the potential to mitigate some of these harmful impacts of long-standing structural inequities by providing greater flexibility for plans to cover non-medical needs. The law illustrates that policymakers believe that health insurers should do more to address social determinants of health. Perhaps they should also focus on how plans can address these social factors earlier in the life cycle as well.