UnitedHealth Group and the other insurance giants running the Medicare Advantage (MA) program might want to start paying attention to something they haven’t worried much about before: growing skepticism from Republicans.

Until recently, efforts to reform MA — a privatized version of Medicare now covering more than half of all beneficiaries — came mostly from Democrats and independent policy experts.

No longer. The latest skepticism is not coming from a liberal think tank or a progressive PAC. It’s coming from two Republican doctors who have spent decades treating patients and sit on powerful House committees overseeing health care. It’s coming from a former Republican congressman who was an author of the law that established Medicare Advantage two decades ago. And it’s coming from right-leaning organizations and policy experts who are now demanding major changes to MA. Their position marks a dramatic and important shift that could lead to meaningful reforms being enacted in a Congress controlled by Republicans.

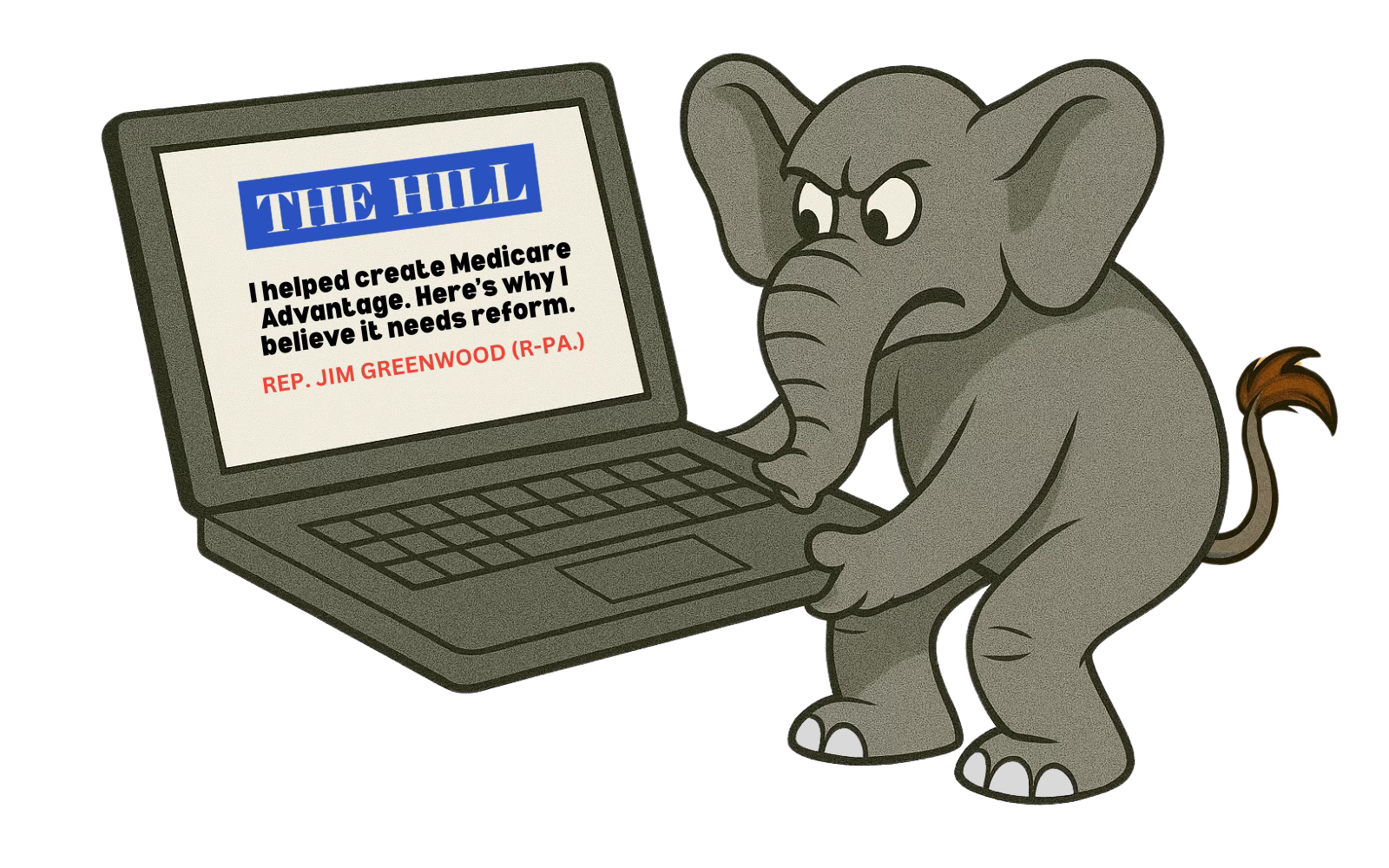

An Architect of MA Speaks Out

In an op-ed published by The HillSunday, former Republican Rep. Jim Greenwood of Pennsylvania — who helped write the Medicare Modernization Act that created Medicare Advantage — said plainly: “The program no longer lives up to [its] promise.”

Greenwood wrote that he had once believed private competition would drive innovation and efficiency. But today, he says, MA has been overtaken by “a handful of massive insurers who are gaming the rules for profit.” Overpayments, cherry-picking, and risk-score manipulation, he said, are now “endemic.”

“It pains me to say this, but the system we helped create is being abused. And it’s not just hurting taxpayers. It’s hurting patients.”

“Seniors… are too often finding out — at the worst possible time — that their plan won’t cover what they need.”

While Greenwood still believes there is a place for private-sector involvement in Medicare, he now calls for rigorous oversight, transparency, and enforcement. He also warns against insurers’ predictable scare tactics whenever reform is on the table.

“I never imagined that Medicare Advantage would become a vehicle for such waste and abuse,” Greenwood concluded. “It’s time to fix it.”

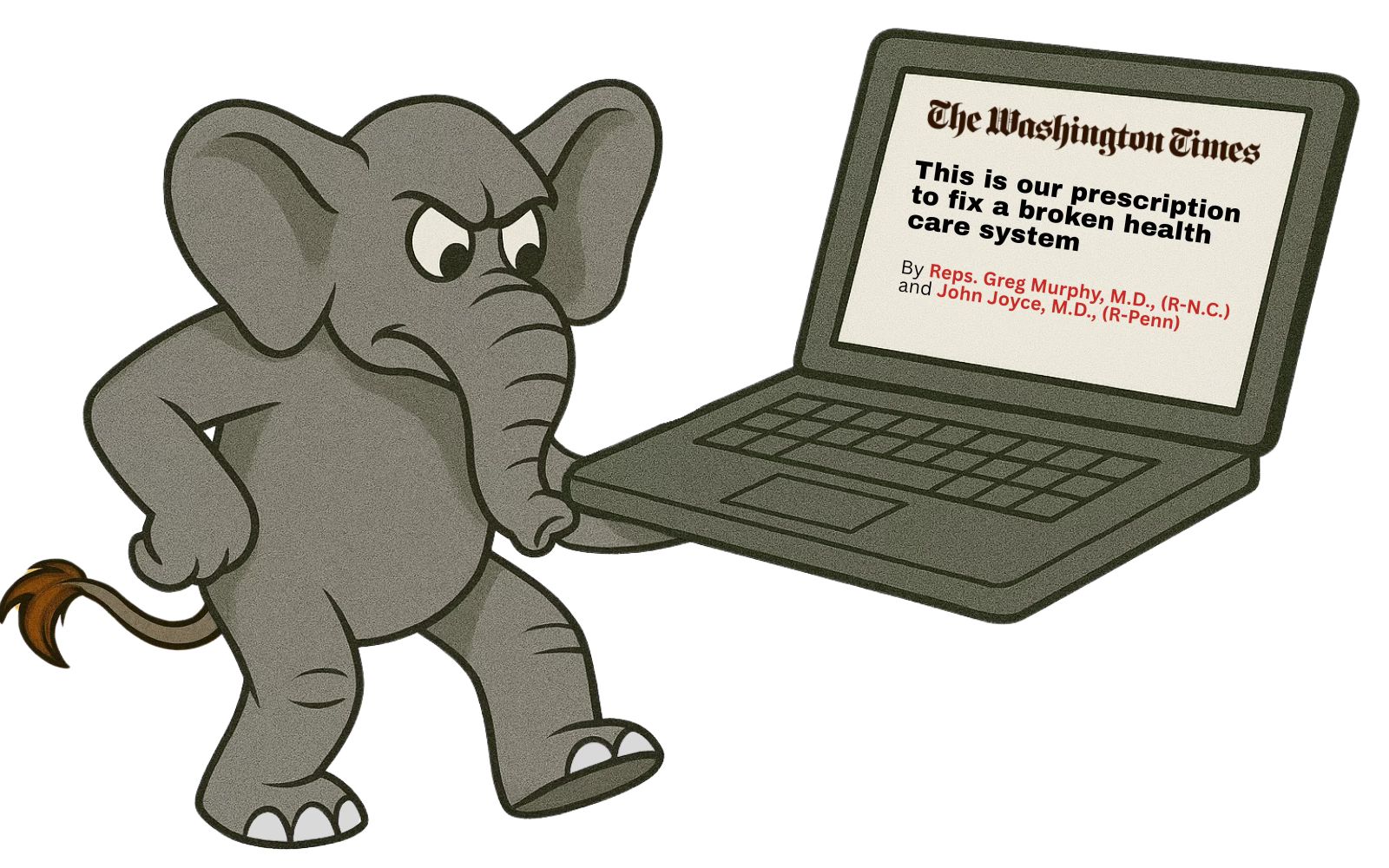

Republican Congressional Docs Say Medicare Advantage Is Broken

Another recent op-ed, written for The Washington Times by two conservative Republicans, Rep. Greg Murphy of North Carolina and Rep. John Joyce of Pennsylvania – both physicians and co-chairs of the GOP Doctors’ Caucus — draws the same conclusion: Medicare Advantage veered too far off course, and it’s time to rein it in. They wrote:

“Profit-driven insurance companies have destroyed [Medicare Advantage’s] model.”

“These plans must stop seeing rewards for delaying or altogether denying care to beneficiaries that need it.”

They called out insurers for “upcoding” — the practice of exaggerating how sick patients are to collect more taxpayer dollars — and for using prior authorization as a weapon to delay or deny necessary care to America’s seniors.

These aren’t unsubstantiated complaints. Recent media investigations found that MA plans regularly reject claims that would be approved under traditional Medicare. The Department of Health and Human Services Inspector General has raised alarms, and the U.S. Justice Department has set its sights on UnitedHealth Group’s Medicare business in particular.

And according to the Medicare Payment Advisory Commission (MedPAC), MA is now costing taxpayers 22% more per beneficiary than traditional Medicare — a difference that translates to $83 billion in overpayments to private health insurers last year alone.

Now, Republicans like Murphy and Joyce are saying the quiet part out loud: MA is making insurance company executives and investors rich at the expense of seniors, people with disabilities and taxpayers.

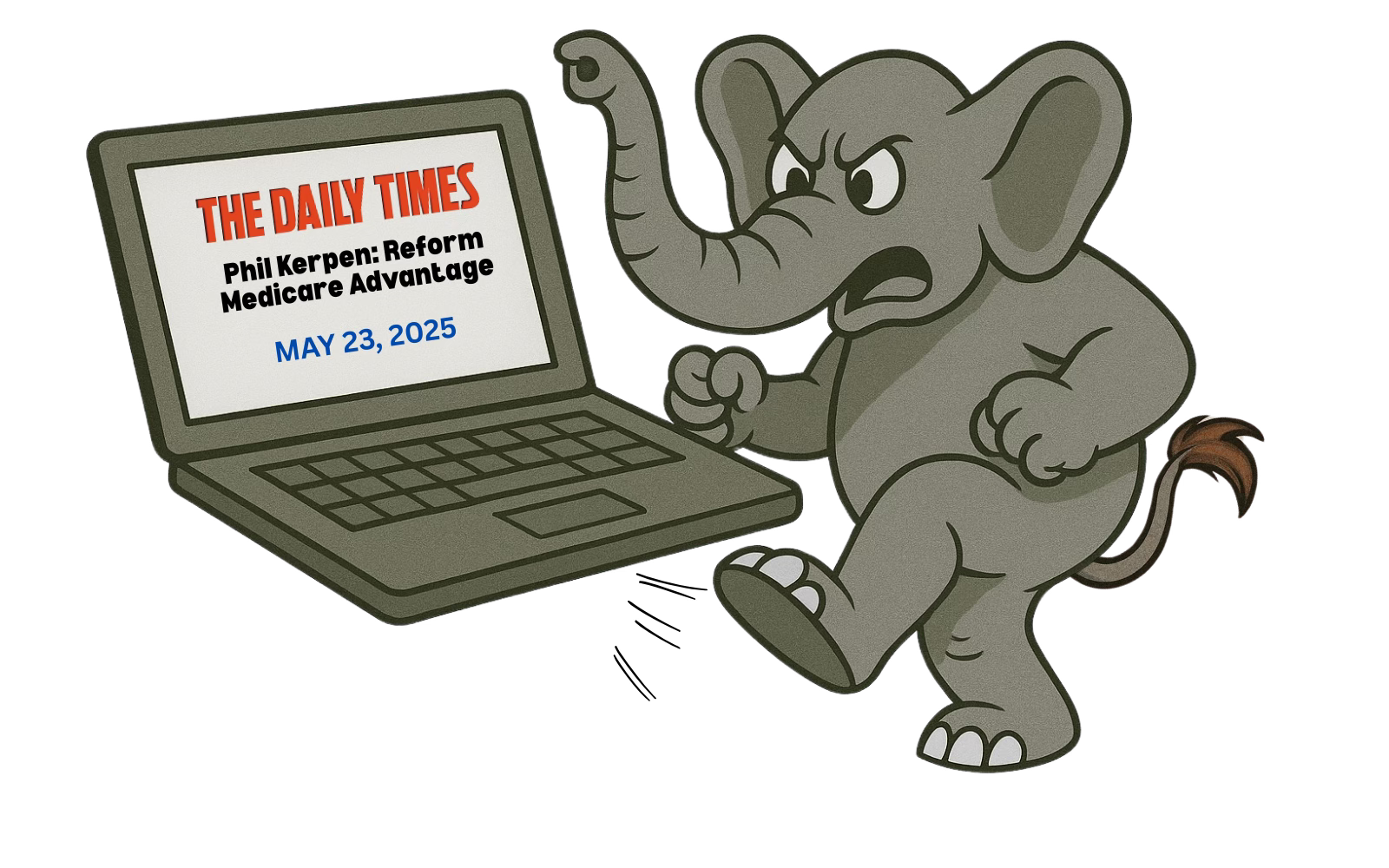

Conservative Advocacy Voices Are Speaking Up, Too

Phil Kerpen, president of the conservative group American Commitment, warned in an op-ed for the Daily Times that Medicare Advantage — which he said was once a “highly innovative and successful” option — is now “becoming increasingly costly and unstable.”

Kerpen pointed to the Department of Justice’s criminal investigation into UnitedHealth as a wake-up call and criticized the monopolistic consolidation of insurers buying up doctors, hospitals, and pharmacies. He called out opaque billing practices, delays in care, and an “unfair burden on taxpayers.”

“If ever there were a government program in need of DOGE-like accountability, competition, and transparency, Medicare Advantage is it.”

He called for reforms many — including myself — have long demanded: stronger disclosure rules, better tools for plan comparison, and serious action on prior authorization abuse. To save the program, he said, President Trump and Congress must be willing to “take on the big insurers and reform it. And quickly.”

Cracks in the Wall of Insurance Influence

There was even a last-minute push, led by Senate HELP Committee Chair Bill Cassidy (R-Louisiana), a doctor, to include MA reforms in Trump’s “One Big Beautiful Bill.” While that effort reportedly failed, Republican critics of the program are vowing to work on a bipartisan basis to enact changes the insurance lobby has fought for years. Upgrade to paid

I spent years in the executive suites of Cigna and Humana — historically big players in Medicare Advantage — and I can tell you this: Republican lawmakers and conservative thought leaders demanding reforms to MA is no small thing. Private insurance corporations have long counted on bipartisan cover to operate with minimal oversight. If they start losing support from Republicans and conservative media, that protective wall begins to crack.

For years, industry lobbyists succeeded in casting Medicare Advantage as politically untouchable — “too complicated,” “too entrenched,” or “too popular to fix.” But as more members of Congress hear from their constituents about denied care, inadequate provider networks, rising out-of-pocket costs, and profiteering by insurance corporations, that illusion is dissipating.

With GOP leaders like Murphy, Joyce, Kerpen — and now Greenwood — stepping forward, it’s clear the tide is turning. Medicare Advantage reform is no longer a partisan issue — it’s an American issue. And for the sake of patients, taxpayers, and the solvency of the Medicare Trust Fund, it’s time Washington acts like it.

The House of Representatives’ reconciliation bill, passed by the powerful Energy and Commerce Committee today, cuts just about everything when it comes to health care – except the actual waste, fraud and abuse. Now the bill heads to the floor for a vote of the full House of Representatives before it must also be passed by the Senate to become law.

I know what you’re thinking: not another story about Medicaid. With the flood of articles detailing the devastating Medicaid cuts proposed by House Republicans —cuts that could strip 8.7 million people of their health coverage — there’s an important fact being overlooked: Members of Congress chose to sidestep policies aimed at reining in Big Insurance abuses and, instead, opted to cut Medicaid.

And the real irony of it all is they could have saved a ton of money if they would just address the elephant in the room.

Abuses by Big Insurance companies have been going on for decades but have only recently come under scrutiny. Insurance companies figured out how to take advantage of the structure of the Medicare Advantage program to receive higher payments from the government.

They do this in two ways:

They make their enrollees seem sicker than they are through a strategy called “upcoding” and;

They use care obstacles such as prior authorization and inadequate provider networks that eventually drive sicker people to drop their plans and leave them with healthier enrollees, referred to as “favorable selection.”

According to the Medicare Payment Advisory Commission (MedPAC) these tactics lead the government to overpay insurance corporations running MA plans by $84 billion a year. This number is expected to grow, and estimates show that overpayments will cost the government more than a $1 trillion from 2025-2034. That is $1 trillion dollars in potential savings Republicans could have included in their bill instead of cutting Medicaid spending that provides care for vulnerable communities.

These overpayments do not lead to better care in MA plans; in fact, research has shown that care quality and outcomes are often worse in MA compared to traditional Medicare. Even worse, these overpayments are tax dollars meant for health care that end up in the pockets of shareholders of big insurance corporations, which spend billions of taxpayer dollars on things like stock buybacks and executive bonuses.

One of the most frustrating parts of the lawmaker’s choice to target Medicaid rather than Big Insurance abuses is that there are multiple policies supported by both Republicans and Democrats to stop these abuses. Sen. Bill Cassidy (R-Louisiana), along with Sen. Jeff Merkley (D-Oregon), have introduced the NO UPCODE Act, which would cut down on the practice of upcoding explained above. President Trump’s Administrator of the Centers for Medicare and Medicaid Services, Dr. Mehmet Oz, said during his confirmation hearing that he supports efforts to crack down on practices used by insurers to upcode. And Rep. Mark Green (R-Tennessee) introduced a bipartisan bill to decrease improper prior authorization denials in MA.

In a somewhat cruel twist, the only mention of Medicare fraud in the Republican reconciliation bill proposals is a section claiming to crack down on improper payments in Medicare Parts A and B (which make up traditional Medicare) by using artificial intelligence.

The total improper payments in TM represent just over one-third of the overpayments going to MA plans each year, and many of the payments flagged as improper in TM are flagged due to missing documentation rather than questionable tactics that MA insurers use.

In reflecting on why Republicans in Congress ignored potential savings from Big Insurance reforms and instead pursued cuts to care for people depending on Medicaid, which do not save as much, my biggest question was, why?

Why would lawmakers swerve around a populist policy right in front of them to stop Big Insurance from profiting off of the federal government to instead propose a regressive policy that targets millions of working Americans and leaves health insurance corporations that make billions in profits each year untouched?

Unfortunately, the answer likely lies in money. Although people enrolled in Medicaid and the Children’s Health Insurance Program (CHIP) make up roughly one-third of the U.S. population, they account for just 0.5% of all political campaign contributions — about $60 million annually. This disparity is likely driven by financial constraints: Many of these individuals are rightly focused on covering basic needs such as housing, food, and childcare, especially as wages have not kept pace with the rising cost of living.

In contrast, the health care sector — which includes major players like big insurance, pharmaceutical and hospital companies—contributed $357 million during the 2020 election cycle, including $97 million to outside groups such as Super PACs. These outside spending groups are largely funded by corporations and wealthy individuals, who represent less than 1% of the population but wield significant political influence.

Super PACs spent more than $2 billion during the 2020 election cycle, amplifying the voices of industry-aligned donors. This stark imbalance in political spending may help explain why congressional proposals targeted Medicaid recipients while leaving the powerful health insurance industry largely untouched.

It is not only Republicans who have failed to stop Big Insurance from taking advantage of federal health programs, Democrats declined to take action when negotiating their health care legislation during President Biden’s term. Rather, it seems to be a failure of policymakers of both parties to pass legislation that makes it clear to Big Insurance that our health care is not an investment opportunity for Wall Street, and the dollars we pay in taxes to support Medicare are not pocket change for executives to use for stock buybacks.

The failure to include MA reform represents a missed opportunity to prioritize patient care over corporate profits. However, the growing strength and voices of patients across the nation will ultimately make it impossible for lawmakers to ignore this issue much longer. With continued momentum, the fight to put patients over Big Insurance profits will succeed.

Democrat lawmakers are urging Republicans debating cuts to Medicaid to focus instead on fraud, waste and abuse in another federal healthcare program: Medicare Advantage.

Curbing upcoding in the privatized Medicare plans, wherein insurers exaggerate the health needs of their members to inflate government reimbursement, is a better avenue for saving federal dollars than restricting benefits or cutting eligibility in Medicaid, the 36 Democrats wrote in a letter to GOP leadership on Wednesday.

The letter was addressed to Senate Majority Leader John Thune, R-S.D, and House Speaker Mike Johnson, R-La., and comes as Republicans debate different policies to reach savings targets.

Dive Insight:

Republicans in Congress are aiming to extend tax cuts from President Donald Trump’s first term. Their budget directs the House Energy and Commerce Committee to cut $880 billion in spending — a goal that’s impossible to reach without touching Medicaid, which (along with its sister program for children) provides safety-net insurance to some 80 million Americans.

Now, Democrats in both chambers are urging Republicans to redirect their attention from Medicaid to MA, privatized plans for Medicare seniors that can provide additional benefits but also restrict care in a way traditional Medicare is not allowed to do. Still, the plans have steadily grown in popularity and now cover more than half of the 68 million Americans in Medicare.

“Your directive to cut federal health care spending should come from reducing waste, fraud, and abuse like upcoding by for-profit insurance companies, not by cutting health care benefits for American families who rely on Medicaid to make ends meet,” the Democrats’ letter reads.

The letter cites a Wall Street Journal investigation into upcoding published last year that found MA insurers frequently added diagnoses for their members for which their members never received treatment or that went against doctors’ observations. The practice drove a total of $50 billion in additional payments to the private insurers over three years, according to the investigation.

Similarly, influential congressional advisory group MedPAC found CMS paid MA insurers $84 billion more in 2024 than the government would have if those members had been in traditional Medicare. Upcoding was responsible for almost half of those overpayments.

Traditionally, Republicans broadly support MA, which was created on the premise that private insurers could help the government manage Medicare more economically. However, there’s been rising bipartisan support for reforming the program in light of growing evidence of practices like upcoding that inflate government reimbursement to plans without helping enrollees.

In his confirmation hearing, Dr. Mehmet Oz, the surgeon and television personality tapped by Trump as the administrator of the CMS, agreed that tackling fraud, waste and abuse in MA was a “rational” way of lowering federal healthcare spending.

“We’re actually apparently paying more for Medicare Advantage than we’re paying for regular Medicare. So it’s upside down,” Oz said in front of the Senate Finance Committee in March.

Republicans in the House are currently trying to figure out how to achieve desired savings without slashing Medicaid, given the program’s political popularity, including among Republican voters.

GOP leadership recently appeared to rule out two Medicaid policies that would cause significant upheaval for enrollees in the program: lowering the portion of Medicaid costs borne by the federal government for the Medicaid expansion population, and per-capita caps on benefits for beneficiaries in expansion states.

“Moving forward with this dangerous plan to rip health care away from low- and middle-income Americans would be a man-made disaster for the health of the nation and the economy,” the Democrats’ letter reads. “We urge you instead to listen to Administrator Oz and tackle real fraud, waste, and abuse by private, for-profit health insurers in MA.”

House E&C is expected to hold its reconciliation markup next week.

On October 15, the open enrollment period for Medicare begins running through December 7 for coverage starting in January 2025. In this period, 67 million Medicare eligible seniors can review features of Medicare plans offered in their area, switch from traditional Medicare to a Medicare Advantage (MA) plan (or vice versa), change their MA selection and add/change their Medicare Part D prescription drug plans.

In 2024, Medicare Advantage plans enrolled 33 million seniors and Medicare paid private insurers $462 billion to pay for their care.

But conditions for Medicare Advantage have changed in recent years prompting many to ask ‘what is the Medicare Advantage?’

Background:

Medicare began July 30, 1965 as a key element in President Lyndon Baines Johnson’s Great Society program offering federal-government-paid insurance coverage for seniors at the age of 65. “Original Medicare” had two parts: Part A to cover hospitals and Part B to cover physicians and outpatient services. In 1972, coverage for adults with disabilities was added, and in 2003, coverage for prescription drugs (Part D) was added.

Its funding comes from payroll taxes paid by employers and their employees, and those who are self-employed PLUS income taxes paid on Social Security benefits, interest earned on the Medicare trust fund’s investments and Part A premiums from people who aren’t eligible for premium-free Part A.

Along the way, Congress authorized seniors the option of accessing Medicare through private insurers aka Part C (Balanced Budget Act of 1997), expanded its scope (Medicare Modernization Act of 2003) and supplemented its funding differential above Original Medicare (Patient Protection and Affordable Care Act 2010) to stimulate enrollment growth. The rationale for MA was straightforward: it offered federal regulators a lab to test care management for seniors with the dual aims of lowering their health costs and improving their health. Private insurers responded. By design, funding for MA was set above Original Medicare rates to encourage private insurer participation.

It worked. This year, the average MA enrollee had 43 plans from which to choose. By three measures, Medicare Part C has been successful:

Enrollment growth: Enrollment in MA plans has increased from 31% of Medicare eligible adults in 2014 to 51% in 2024 and is projected to increase in 2025. Notably, enrollment in special needs and employer-sponsored MA plans has increased faster than the individual MA market which is subject to open enrollment periods. Satisfaction appears high (69% of members do not shop for another plan during open enrollment periods) and member churn is low.

Medicare has saved money: Per the 2024 Medicare Trustees’ Report, MA has contributed to slower growth in Medicare spending than forecast. “The Social Security and Medicare programs both continue to face significant financing issues…The Hospital Insurance (HI) Trust Fund will be able to pay 100% of total scheduled benefits until 2036, 5 years later than reported last year. At that point, that fund’s reserves will become depleted and continuing program income will be sufficient to pay 89% of total scheduled benefits.”

Private insurer participation has been strong: For health insurers, Medicare Advantage is profitable: PMPM contribution margins are 50-100% higher than individual and group lines of business. And, as CMS payments to MA have tightened, the MA insurer market consolidated with 3 (UnitedHealth, Humana, CVS-Aetna) taking advantage of operating pressures on small players to increase their share to 58% of total enrollment. Advantage: Seniors, Medicare and Corporate Insurance.

But conditions going forward suggest the MA advantage might not be as strong. The market signals are clear:

Insurer belt tightening: Since 2023, seniors’ use of hospitals, specialty care and prescription drugs has returned to pre-pandemic normalcy cutting into insurer margins. In its CY 2025 Rate Announcement September 27, CMS announced “The average monthly plan premium for all MA plans, which includes MA plans that provide prescription drug coverage and MA Special Needs Plans (SNPs), is projected to decrease from $18.23 in 2024 to $17.00 in 2025. Benefit options will remain stable, including MA supplemental benefit offerings such as hearing, dental, and vision. The amount of rebate dollars, which can be used for supplemental benefits, will remain stable, with a slight increase, from 2024 to 2025. Enrollment in MA is projected to be 35.7 million in 2025, an increase from 2024, with MA enrollment representing approximately 51% of all people enrolled in Medicare.” This translates to lower margins for MA plans, fewer supplemental benefits for enrollees and lower payments to hospitals and physicians.

Increased regulatory scrutiny: The Medicare Payment Advisory Commission (MedPAC) concluded that MA plans receive payments from CMS that are 122%of spending for similar beneficiaries in traditional Medicare, on average, translating to an estimated $83 billion in overpayments in 2024. Congress is investigating. In 2023, CMS adopted tougher audit standards specific to diagnosis codes used by private MA plans to bill Medicare on behalf of their enrollees. Audits conducted by the U.S. Department of Human Services’ Office of Inspector General (OIG) applying the new standards found the majority of private MA plans guilty of upcoding and thereby overpaid by Medicare. In 2025, cut points used by CMS to award star ratings have been modified resulting in fewer plans getting 4-star ratings that enable their participation in 5% bonus payments—a major reason recent stock declines for UHG, HUM, CVS and others. Regulatory scrutiny of MA plan marketing practices, coding, denials and prior authorization procedures will intensify reflecting bipartisan intent to constrain MA profits.

Understandably, tension between MA insurers and providers has intensified as insurers seek to protect their margins. The Change Healthcare (CH) cyber-attack (February 21, 2024) that disabled insurer payments to hospitals and physicians stoked animosity since CH is a subsidiary of UnitedHealth Group–the largest sponsor of MA plans and the healthcare juggernaut. Though operating margins for half of U.S. hospitals have recovered, insurer cuts coupled with labor and prescription drug costs have decimated care delivery in almost every community. Participation in MA plan provider networks, once SOP is now a tough call for hospitals, medical groups and other providers.

My take:

What is the Medicare Advantage?

As a lab for innovation in care management for seniors, it’s promising.

As an engine to drive lower costs for senior health and extended solvency to the Medicare program, it’s unclear.

As a platform to shift incentives from fee-for-service to value across the system, it’s helpful.

But until and unless hospitals, physicians, insurers, business leaders and regulators commit to implement a transformed system of health that’s comprehensive, affordable, efficient and accountable, the Medicare Advantage will be marginalized.

In many ways, the headwinds facing MA are part of the larger narrative facing healthcare:

public sentiment against consolidation and corporatization has eroded its cherished trust and confidence. It’s true for insurance, hospitals, prescription drug companies and PBMs. The blame is shared: no one of these owns the moral high ground (though a few organizations in their ranks aspire).

Last Monday, CMS announced the base payment rate it will pay Medicare Advantage plans in 2025: plans will see an average 3.7%, or $16 billion, increase in payments once risk scores are factored in but a cut to base payments of 0.16% since 2025 risk scores were expected to be 3.86%. That’s the math.

It came as a surprise to insurers and investors who had imagined CMS would modify its November proposed rule to increase payments as has been the precedent in prior years. Per Bloomberg:

Then on Wednesday, CMS released a 1327-page final rule with sweeping directives about how Medicare Advantage plans should operate starting next year:

“This final rule will revise the Medicare Advantage (Part C), Medicare Prescription Drug Benefit (Part D), Medicare cost plan, and Programs of All-Inclusive Care for the Elderly (PACE) regulations to implement changes related to Star Ratings, marketing and communications, agent/broker compensation, health equity, dual eligible special needs plans (D-SNPs), utilization management, network adequacy, and other programmatic areas. This final rule also codifies existing sub-regulatory guidance in the Part C and Part D programs.”

When first proposed in November, insurers pushed back. In response, most of the 3463 comment letters received by CMS said they needed more time to modify their plans. CMS replied: “We appreciate the commenter’s concern regarding the plans having enough time to understand the impact of finalized regulations. We will take their recommendation into consideration for future rulemaking.” P20). Accordingly, all MA plans must get approvals from CMS reflecting these changes on or before June 3, 2024.

Arguably, CMS took this hardline approach because bona fide studies by MedPAC, USC Shaeffer and others found widespread risk-score upcoding by Medicare Advantage plans that resulted in 6%-20% annual overpayments by Medicare.

Recent high-profile missteps by two of the biggest and most profitable MA players no doubt reinforced CMS’ get tougher posture: UnitedHealth Group’s Change Healthcare cybersecurity breech and Cigna’s $172 million Fraud and Abuse penalty for inflating its MA risk coding.

So, the transition from Medicare Advantage circa 2024 to Medicare Advantage 2025 will be its most significant since Medicare Choice was included in the Balanced Budget Act of 1997. In 2024, Medicare Advantage experienced enrollment growth and profitability to which its players were accustomed despite a late-year spike in utilization:

33.8 million Medicare enrollees (or 51% of total Medicare enrollment) get their coverage from Medicare Advantage plans—up 6.4% from 2023.

The average Medicare beneficiary has access to 43 Medicare Advantage plans in 2024, the same as in 2023, but more than double the number of plans offered in 2018. The majority of options do not require an extra payment above what Medicare pays private issuers on their behalf and the majority offer supplemental benefits including dental, eyecare, wellness et al.

And Medicare Advantage insurers entered the year on solid financial footing: the biggest issuers posted strong profits in 2023 i.e. UnitedHealth Group: $22.4 billion, CVS (Aetna) Health: $8.3 billion, Elevance Health: $6 billion, Cigna Group: $5.2 billion, Centene: $2.7 billion, Humana: $2.5 billion

In 4Q 2023, pent-up demand for services by Medicare Advantage enrollees pushed utilization of doctors, hospitals and other providers up 8.1% above prior year levels including 4Q 2023 increases for outpatient surgery 14.4%, outpatient visits excluding ER and surgery 8.7%, physician visits 6.0%, inpatient adult care 5.3%, Part B drugs 5% and ER visits 4%.

But 2025 will be different. The 4Q spike in utilization and impact of the new rules will have profound impact on Medicare Advantage: the biggest players like United and Humana will adapt and be OK, but others downstream will be disrupted or impaired:

Smaller MA plan sponsors and their lobbyists: AHIP, ACHP, BCBSA, Better Medicare Alliance and the army of lobbyists deployed to defeat these rules took a hit. Members pay dues for results. These rules were disappointing (though it could have been worse).

MA brokers, agents and marketing organizations: The limits on compensation, constraints on MA marketing tactics and enrollee protections around transparency may reduce revenues for many third-party marketing organizations that sell their services to the plans. A shakeout is likely.

Supplemental services providers: lower payments by CMS will force some to reduce/eliminate supplemental benefits that are valued less by enrollees. Dental and prescription drug benefits appear safe but others (i.e. fitness programs) might be cut by some.

Hospitals and physicians: Cuts by CMS to MA plans will trickle-down as reimbursement cuts to direct providers of care. Hardest hit will be smaller and rural providers in communities with large MA enrollment.

MA enrollees: Though the rule adds behavioral health benefits, data privacy protections and equity considerations in utilization management decisions by the plans, the likely impact of the rate cut is fewer plan options for enrollees and higher premiums. Margin compression for MA plans will hurt bigger plans who will adapt but incapacitate smaller plans unable to survive.

The Presidential campaigns: MA sponsors must submit their proposed 2025 plans to CMS on or before June 3, 2024—in the midst of Campaign 2024. And open enrollment will begin in October as MA plans launch marketing for their newly-revised offerings. No doubt, the Campaigns will opine to Medicare security in their closing rhetoric recognizing MA covers more than half its enrollees.

My take:

These rules are a big deal. CMS appears poised to challenge the industry’s formidable strengths and force changes.

Together, these rules will disrupt day to day operations in every MA plan, intensify friction with providers over network design, coverage and reimbursement negotiations and confuse enrollees who might have to pay more or change plans.

Medicare Advantage remains a work-in-process. Stay tuned.

Over the past seven years, Medicare Advantage’s (MA’s) enrollment has almost doubled, adding 10 percent to its market share , now at 49 percent. Rebates, the additional dollars paid by CMS to MA plans that bid beneath their “benchmark,” have doubled in that time from $80 per beneficiary per month (PBPM) to $164. (Benchmarks are intended to represent the average per-beneficiary spending in traditional Medicare (TM) in a given service area.)

The Medicare Advantage industry’s explanation of its success is grounded in claims about MA’s ability to deliver Medicare Part A and B benefits for much less than TM. These savings are, in theory, the basis for the rebates, the incremental revenue CMS pays to plans that fund the improved benefits and lower premiums as compared to TM, which in turn help attract members to MA plans. Indeed, the Medicare Payment Advisory Commission (MedPAC) reports that MA bids average 85 percent of the FFS cost. Because these bids include approximately 15 percent for administrative costs and profits, they imply that Plan medical cost savings must be in the range of 25 to 30 percent versus the Medicare FFS cost benchmark bidding target.

However, a close examination of the bid process reveals that most of these savings are artifacts of the process and not due to better or more efficient care. They result from including “induced utilization costs” from Medicare supplemental insurance, legislated increases in the benchmarks, and risk score gaming. The inflation of benchmarks and risk score gaming, not better care, finance the rebates that drive MA market success.

CMS pays MA Plans a per-person revenue amount that is determined by the Plan’s bid to provide Part A (hospital) and Part B (all other medical services) to enrollees. Plans bid against a benchmark, which as noted is intended to capture the amount that Medicare would spend on TM benefits for an average TM beneficiary. If the bid is less than the benchmark, CMS keeps about one-third of the difference and pays two-thirds to the Plan as a rebate. This rebate can be used to improve benefits or reduce costs for the members. If the bid is above the benchmark, there is no rebate, and the Plan must charge the member premiums to make up the difference.

Bids include the cost of medical services as well as plan administrative costs and profits. Most plans bid sufficiently below the benchmark to offer members a “zero premium” product, often including Part D drug coverage. Conceptually, the difference between the benchmark and the bid represents “savings” that the plan generates that decrease CMS costs.

Real Vs. Apparent Savings

The difference between bids and benchmarks, i.e., the savings vs. FFS, and rebates have doubled over the past seven years, leading to improved benefits, lower premiums for members, higher profits and more rapid growth. In 2022, rebates were $164 PBPM and 66 percent of beneficiaries were in zero-premium products.

This suggests that savings for CMS have increased; however, the reality is that most of these are just “apparent savings”—not real savings—that increase costs for CMS, beneficiaries and taxpayers.

Here is how that happened.

Benchmarks Are Significantly Inflated By Including The Costs Of ‘Induced Utilization’

The total cost of care is a function of the price paid per service and the number of services patients receive. Because MA Plans are given the right to use CMS’s Medicare pricing schedule for all Medicare participating providers, the MA average price per service tends to be about the same as Medicare’s. Most savings in MA then must be due to changes in utilization of services. Is the 25-30 percent implied savings of MA really due to 25-30 percent lower utilization across the full set of health care services, or is something else leading to “apparent savings”?

The ‘Induced Utilization Effect’ Of Medicare Supplemental Insurance Leads To Higher Utilization And Costs In The TM Population

Health insurance benefits programs vary by the percentage of costs paid by the covered individual. First-dollar coverage (FDC) means that the insurer pays most of the cost of services. Non-first dollar coverage (NFDC) with deductibles, coinsurance, and copays creates financial hurdles for patients as they pay more of the cost. Actuaries have shown that populations with FDC use more services and have higher total costs. We use the term “induced utilization” to denote the additional services associated with FDC. If one assumes that the additional services are necessary and contribute to better health, this difference is better framed as “forgone services” by the population with NFDC.

TM’s population provides an ideal context to study this phenomenon. TM’s fee-for-service benefits cover about 84 percent of medical costs but the vast majority of TM beneficiaries (84 percent) have supplemental insurance coverage that covers the other 16 percent of costs, effectively giving them FDC. MedPAC commissioned two studies to examine the difference in utilization between beneficiaries with and without supplemental coverage. MedPAC cited the first study in their June 2012 report on reforming Medicare’s benefit design, concluding:

The study estimated that total Medicare spending was 33 percent higher for beneficiaries with medigap policies . . . Beneficiaries with employer sponsored coverage had 17 percent higher Medicare spending

The authors of this study updated it in 2014, using three years of additional data, through 2008. Their conclusions at that time estimated that Medicare spending was 25 percent higher for beneficiaries with Medigap policies and 14 percent higher for those with employer-sponsored coverage. Another 2019 study on induced utilization showed that Medigap increased utilization by more than 20 percent.

The way the costs from induced utilization inflate the MA benchmark calculation has major implications for the calculation of MA Plan rebates. As we shall see below, the current approach gives MA plans a massive head start on financial success, no matter how well or poorly they manage care or costs.

Effects Of Induced Utilization On TM Spending Flow Through To MA Benchmarks

At a high level, the MA benchmark is based on the average total cost for all TM beneficiaries. The 2022 TM average cost of $1,086 per beneficiary per month (PBPM) is the average of the total medical costs for two Medicare populations: those with additional coverage (TM + Coverage) and those with Medicare only (TM only). Exhibit 1, using the differences in spending cited by Hogan et al in 2014 above, demonstrates the underlying average costs for individuals with and without additional coverage. The TM-only population costs CMS $920 while the TM+ Coverage population costs $1,169. The overall weighted average cost of $1,086 is inflated above the TM-only cost by $166, or 18 percent.

The Expected Cost Plans Use In Their Bids, Based On TM-Only Benefits, Are Far Below The Inflated MA Benchmark And Result In Large “Apparent Savings” And Rebates

The MA bid process instructs plans to bid their expected cost using the standard Medicare package of services and benefits. Any improved benefits and resulting costs are part of the supplemental benefit information that explains how they will use the rebates. The intent is for the plans to demonstrate their ability to drive significant savings versus CMS’s cost. One would think that this should be a comparison of the bid with the TM-only population’s cost. But the MA benchmark used in the comparison is based on the overall average of costs for the TM +Coverage and the TM-only populations, thereby including the induced utilization costs. When the lower expected cost is subtracted from the inflated benchmark it automatically creates “apparent savings” of $166 PBPM, or 18 percent.

Exhibit 2 illustrates how these “apparent savings” roll through the MA bid to create rebates for the plans. Our model in exhibit 2 is based on MedPAC’s analysis of the industry-wide 2022 MA bids, which showed an average rebate of $164 PBPM. That analysis, combined with the Medicare 2022 average TM cost of $1,086, implies that the expected medical costs used in the bids averaged approximately $790, an actual medical cost savings of $130 PBPM (14 percent) compared to the $920 TM-only cost.

Column 1 shows what would happen if the benchmark were set at the TM-Only cost of $920 with an average risk population. With assumed administrative costs of $80 PBPM (8 percent) and profits of $50 (5 percent) the resulting bid would be $920. Because the bid and the benchmark would be both $920, plans would show no savings and receive no rebate. The total savings in the Bid are just the medical cost savings of $130, which fund the plan administrative costs and profits. With no rebate they would have to charge members for any improved or supplemental benefits. This would not be a formula for success in MA.

Column 2 uses the inflated benchmark of $1,086 that includes the $166 induced utilization effect. Medical costs do not change, the bid remains the same, and the $166 becomes the difference between the benchmark and the bid; two-thirds of the $166 becomes the rebate of $108. The total savings implied in the bid increase to $296, but 56 percent is due to “apparent savings,” which account for 100 percent of the rebate.

But this is still well below the reported 2022 $164 average rebate. Is more of this driven by plan medical cost savings?

Legislated Payments Above FFS Cost Further Inflate Benchmarks And Contribute To Apparent Savings And Rebates

The MA average national benchmark of $1,086 is based on Medicare’s national average cost for TM in 2022, as reported by CMS. This is what Medicare pays for all Part A and B services for an average beneficiary across the country. Actual MA rates are set at the county level and are adjusted from 95 percent to 115 percent of FFS Medicare expenses depending on whether a county has high or low costs relative to the national average. Approximately 80 percent of MA enrollees are also in plans that receive quality bonuses.

County bonuses and quality bonuses are added to benchmarks. According to MedPAC, in 2022 these bonuses accounted for an additional 8 percent increase in payments above the FFS cost, and 90 percent of MA members were in Plans receiving quality bonuses.MedPAC again reiterated at its January 2023 meeting that the “quality bonus program is not a good way of judging quality for the 49 percent of beneficiaries in MA.” Column 3 starts with a benchmark that is inflated $87 (8 percent) more to account for these bonuses. The bid is unchanged, increasing the difference to $253 and the rebate to the $164 reported by MedPAC. Of the savings implied in the bid, 66 percent is from benchmark inflation, as is 100 percent of the rebate.

Risk Score Gaming Acts As A Multiplier Of This Benchmark Inflation

As described in our prior article, MA Money Machine Part 1, plans systematically increase their risk scores to improve payments from CMS. Column 4 in exhibit 2 illustrates the results for a plan that increases its risk score from 1 to 1.1. In the bid process, the benchmark-bid difference is computed by comparing the actual bid to the risk-adjusted benchmark. Our prior examples had an average risk score of 1, so the risk-adjusted benchmark is the same as the benchmark. In Column 4 the benchmark is risk adjusted by multiplying the $1,173 from Column 3 by the 1.1 risk score, resulting in an increase of $117.

While the higher risk score might suggest that the population is sicker, that is an illusion created by the risk score game. The medical costs do not change.The reality is the population is the same; the plan has just collected more codes that make the population look sicker. We recently presented an example of this using data from a United Health Group (UHG)/Optum Team Study that included a comparison of HCC coding rates for FFS and MA populations.

The bid therefore remains the same. The difference has increased to $370, resulting in a rebate of $241. The savings implied in the bid increase to $500, but 74 percent of these and 100 percent of the rebate are apparent savings from benchmark and risk score driven inflation.

The MA Bid Process Allows Plans With Zero Cost Savings To Offer Zero Premium Products

Column 5 of exhibit 2 shows that even if the plan has no actual medical cost savings, and no increase in the risk score, the benchmark inflation from induced utilization and bonuses allows the plan to have a rebate of $100.

MedPAC has reported that rebates vary widely, suggesting that there are indeed real MA plans today that are delivering no improvement in medical costs vs. FFS but still are receiving rebates and offering zero premium products.

Even Plan Medical Cost Savings Are Uncertain

Most of our examples assume that MA beneficiaries have a risk score of 1, that is they have the same health burden as an average Medicare population. Multiple studies have shown that this is not the case. Jacobson et al demonstrated that beneficiaries who enrolled in MA in 2016 were 16 percent less costly than individuals who stayed in TM. Other researchers have used mortality rates as evidence that individuals choosing MA are healthier than those in TM. If MA beneficiaries are actually healthier and have lower medical costs, the 14 percent “real” cost savings we use in exhibit 2 would be overstated.

ACOs Do Not Benefit From Any of These Subsidies

In an earlier paper, Joe Antos and Jim Capretta asserted that “There is little question the MA plans have the capacity to deliver Medicare benefits at far less cost than unmanaged fee-for-service” and further that accountable care organizations (ACOs) deliver “far less that the savings that could be achieved by MA plans based on their bids.” While we disagree with both statements, we agree on one point: the savings implied in MA bids seem large. But they are mostly apparent not real savings.

ACOs have a very different starting point from MA plans. They don’t start with the 18 percent advantage demonstrated above, they don’t get county and quality bonuses and they are not able to benefit much from risk coding. The costs of induced utilization are in their benchmarks, but their aligned beneficiaries are representative of the TM mix of people with FDC and non-FDC. The benefits and the resulting costs match, unlike the MA bid comparison of average costs and lower plan expected costs. Any comparison of savings by the two programs needs to account for this reality. We believe that most of the differences in the “real savings” of the two programs is accounted for by claims denials and some instances of lower prices in MA vs. FFS.

Conclusion

MA is growing rapidly because of plans offering lower premiums and improved, supplemental benefits.

Claims by the MA industry that they are successful because they deliver more efficient care are flawed because they compare MA costs to inflated benchmarks that are much higher than the actual CMS costs to provide benefits.

Even if one assumes that MA does decrease medical costs, these savings as reflected in MA bids are not the drivers of the rebates or MA success. Indeed, 100 percent of rebates result from inflated benchmarks and risk score gaming. The resulting payments, which are in excess of TM costs, generate the additional funding for “free-to-the-member” improved benefits. While there is large variation, and some plans improve care and decrease utilization, MA industry success is a function of corporate subsidies.

The bottom line: we are systematically driving people out of TM by subsidizing the more expensive MA.

Inflated benchmarks from these three sources start MA plans “on third base” and risk score gaming gives them a free walk home. For MA plan owners it feels like they hit a home run. For taxpayers and Medicare beneficiaries footing the bill it feels like a series of major errors. CMS in its 2024 Medicare Advantage Advance Notice has proposed significant changes to the Risk Adjustment system. We believe this would be an important step forward towards addressing the vast overpayments to MA plans and deserves our support.

Hard-pressed to come up with significant savings to reduce the deficit, some Senate Republicans are taking a closer look at reforms to Medicare Advantage in light of reports that insurance companies are collecting billions of dollars in extra profits by over-diagnosing older patients.

But the idea of cracking down on Medicare Advantage overpayments to insurance companies divides Republicans, who have traditionally championed the program.

Proponents of Medicare Advantage reform anticipated it will face strong opposition from the insurance industry, one of the most powerful special interest groups in Washington.

Sen. Bill Cassidy (La.), the top-ranking Republican on the Senate Health, Education, Labor and Pensions Committee, is leading the push to reduce Medicare overpayments.

“Medicare is going insolvent. If we don’t do anything, it’s going to go insolvent. We have a whole package of things, all of them bipartisan, and we’re doing it essentially to have something out there so that if somebody decides to do something, there will be things that are examined, considered and bipartisan” to vote on, he said.

“I come up with lots of stuff. We thought it through policy and think it’s policy that can make it all the way through,” he said.

Cassidy’s office says his bill could extend the solvency of Medicare by saving as much as $80 billion in federal funds over the next decade without cutting benefits.

He emphasizes that it would not cut Medicare Advantage benefits, but critics of the legislation are sure to challenge that claim.

“We’re not undermining Medicare Advantage,” he said.

“In fact, I would say this is a better alternative than what CMS is doing by rule,” he added, referring to a new rule-making action by the Biden administration to recover overpayments in Medicare Advantage through the Centers for Medicare & Medicaid Services.

The Medicare Payment Advisory Panel estimates that Medicare Advantage plans collected $124 billion in overpayments from 2008 to 2023. They collected an estimated $44 billion overpayments in 2022 and 2023 alone, according to MedPAC.

Unlike traditional fee-for-service Medicare, Medicare Advantage plans are offered by private companies. Both are funded by taxpayers through general revenues, payroll taxes and beneficiaries’ premiums.

Cassidy is also leading a bipartisan working group to reform Social Security to extend its solvency. Members include Sens. Angus King (I-Maine) and Mitt Romney (R-Utah).

“To have a significant impact on fiscal policy, you’d have to look at entitlements,” said Romney, who called Medicare Advantage “an area we’re going to be looking at very shortly — the committee will be looking at Medicare Advantage,

the cost of Medicare Advantage …. It’s become more expensive than the old fee-for-service Medicare.”

In a follow-up interview Thursday, Romney said senators are also looking at reforms to Pharmacy Benefit Managers, the companies that serve as middle-men between drug manufacturers, insurance companies and pharmacies.

Romney said, “in the past, Medicare Advantage has been a lower-cost way of providing Medicare than fee-for-service Medicare.”

“If that’s changing, I’d like to understand why and make sure we don’t create impediments to the lower-cost Medicare Advantage,” he said.

Sen. Mike Braun (R-Ind.) said Medicare Advantage overpayment “definitely” is a “reform issue.”

“I’ve been the loudest voice on reforming health care and that’s a commonsense idea,” he said. “Whatever it takes to bring down health care costs.

“I’m one of the most free-market people here, but the health care industry is not a free market. It’s like an unregulated utility,” he said. “There’s so much opaqueness.”

But some Republicans are already trying to paint efforts to reduce overpayments as cuts to Medicare Advantage.

“The problem with Medicare Advantage is President Biden is cutting $540 per member per year. That’s the problem. Medicare Advantage has been very successful,” said Sen. Roger Marshall (R-Kan.), an OB/GYN who practiced medicine for more than 25 years.

National Republican Senatorial Committee Chairman Steve Daines (R-Mont.) accused Biden of “proposing Medicare Advantage cuts” when the president accused some Republicans of wanting to sunset Medicare at his Feb. 7 State of the Union address.

Medicare Advantage is getting more popular among Democrats as well as the number of blue state enrollees in the program soars. The number of Americans enrolled in Medicare Advantage has nearly doubled over the last 12 years, according to the Kaiser Family Foundation.

Cassidy’s proposal, which he introduced with progressive Sen. Jeff Merkley (D-Ore.) on Monday, could draw broader interest from Republicans.

Sen. John Cornyn (R-Texas), an adviser to the Senate GOP leadership, called Medicare Advantage a “success.”

“That doesn’t mean that it should be immune from oversight, so I’ll be interested to see what they have to say,” he said.

Cassidy and Merkley say that Medicare Advantage plans have a financial incentive to make beneficiaries appear sicker than they are because they are paid a standard rate based on the health of individual patients. Their bill, the No Unreasonable Payment, Coding or Diagnoses for Elderly (No Upcode Act) would require risk models based on more extensive diagnostic data over a period of two years.

The goal is to narrow the disparity in how patients are assessed by traditional Medicare and Medicare Advantage.

Studies and audits conducted by CMS and the Department of Health and Human Services’ inspector general found that insurance companies collected billion of dollars in overpayments because of diagnoses that were not later supported by enrollees’ medical records.

The Kaiser Family Foundation reported in August that more than 28 million people — or about 48 percent of the eligible Medicare population — were enrolled in Medicare Advantage plans in 2022. They accounted for $427 billion or 55 percent of total federal Medicare spending.

The AHA has previously noted the third party observers who demonstrate a tenuous grasp of the data and rules regarding federal hospital transparency requirements. Now, some of those same entities with deep pockets and an apparent vendetta against hospitals and health systems have turned their attention toward the broader financial challenges facing the field. The results, as described in a recent Health Affairs blog, are as expected — a complete misunderstanding of current economic realities.

The three most egregious suggestions in this piece are that hospitals are seeking some kind of bailout from the federal government, employers and patients; that investment losses are the most problematic aspect of hospital financing; and that hospitals’ analyses of their financial situation are dishonest.

We debunk these in turn.

Hospitals are seeking fair compensation, not a government bailout. The authors state that hospitals are asking “constituents to foot the bill for hospitals’ investment losses.” This is patently false. Indeed, if you read the request we made to Congress cited in their blog, hospitals and health systems are simply asking to get paid for the care they deliver or to lower unnecessary administrative costs. This includes asking Medicare to pay for the days hospitals care for patients who are otherwise ready for discharge. Increasingly, this has occurred because there is no space in the next site of care or the patient’s insurer has delayed the authorization for that care. Keeping someone in a hospital bed for days, if not weeks, requires skilled labor, supplies and basic infrastructure costs. This doesn’t even account for the impact on a patient’s health for not being in the most appropriate care setting. Today, hospitals are not paid for these days. Asking for fair compensation is not a bailout; it is a basic responsibility of any purchaser.

While investment income may be down, hospitals and health systems have faced massive expense increases in the last year. The authors note that patient care revenue was up “by just below 1 percent in relative terms from 2021 to 2022,” suggesting that implies a positive financial trend. However, hospital total expenses were up 7% in 2022 over 2021, and were up by even more, 20%, when compared to pre-pandemic levels, according to Kaufman Hall. And it’s not just the AHA and Kaufman Hall saying this either: in its 2023 outlook, credit rating agency Moody’s noted that “margins will remain constrained by high expenses.” Hospitals should not need to rely on investment income for operations. However, many have been forced into this situation by substantial underpayments from their largest payers (Medicare and Medicaid), which even the Medicare Payment Advisory Commission (MedPAC), an independent advisor to Congress, has acknowledged. MedPAC’s most recent report showed a negative 8.3% Medicare operating margin. Hospitals and health systems are experiencing run-away increases in the supplies, labor and technology needed to care for patients. At the same time, commercial insurance companies are increasing their use of policies that can cause dangerous delays in care for patients, result in undue burden on health care providers and add billions of dollars in unnecessary costs to the health care system.

Hospitals and health systems are committed to an honest examination of the facts. The authors imply that the studies documenting hospitals’ financial distress are biased. They note that certain studies conducted by Kaufman Hall are based on proprietary data and therefore “challenging to draw general inferences.” They then go on to cherry-pick metrics from specific non-profit health care systems voluntarily released financial disclosures to make general claims about “the primary driver of hospitals’ financial strain.” The authors and their financial backers clearly seem to have a preconceived narrative, and ignore all the other realities that hospital and health system leaders are confronting every day to ensure access to care and programs for the patients and communities they serve.

It is imperative to acknowledge financial challenges facing hospitals and health systems today. Too much is at stake for the patients and communities that depend upon hospitals and health systems to be there, ready to care.

MedPAC’s recommendation that acute care hospitals don’t need a significant increase in 2024 Medicare rates is “totally insufficient and out of touch with reality,” according to the American Hospital Association.

“This view is one-sided, inaccurate and misleading,” Ashley Thompson, AHA’s senior vice president of public policy analysis and development, wrote in a March 23 blog post. “After years of once-in-a-lifetime events in the form of a global pandemic and record inflation, hospitals across the country are struggling to continue to fulfill their mission to care for their patients and communities.”

In its annual March report to Congress, MedPAC recommended an update to hospital payment rates of “current law plus 1 percent,” which the AHA says is not enough for many hospitals to keep their doors open.

The commission found that most indicators of sufficient Medicare rates for providers were positive or improved in 2021, though it acknowledged that hospitals saw more volatile cost increases in 2022 compared to years prior. Hospital margins were also lower last year than in 2021, according to preliminary data, driven in part by providers facing higher than expected costs and capacity and staffing challenges.

The report also said that its 2024 payment recommendations “may not be sufficient” to sustain some safety-net hospitals with a low number of commercially insured patients, and proposed $2 billion in add-on payments.

Across the U.S., a total of 631 rural hospitals — or about 30 percent of all rural hospitals — are at risk of closing in the immediate or near future.

MedPAC’s recommendations for 2024 differ from how some health economists have recently described hospitals’ finances. In January, hospitals had a median operating margin of -1 percent according to Kaufman Hall, a finding that arrived on the heels of 2022 being named the worst financial year for hospitals since the start of the COVID-19 pandemic.

“It is also important to realize that MedPAC’s report and data has limitations,” Ms. Thompson wrote, referring to a misalignment in the calendar year MedPAC chose to analyze and how hospitals can differ in how they report their individual financial earnings.

MedPAC said its report reflects 2021 data, preliminary data from 2022, and projections for 2023, along with recent inflation rates.

“…cost reports are filed for hospitals’ own specific fiscal years, and because surges, relief payments, and eventual expense increases happened at different times for different hospitals, these calculated margins don’t necessarily provide a fully accurate picture of the financial reality in 2021,” Ms. Thompson wrote.

The AHA stressed that hospitals’ finances in 2023 face much different challenges compared to 2021, when the industry was more supported by strong investment returns and federal pandemic relief.

“The fact that massive numbers of hospitals are not currently closing due to financial pressures should be seen as positive for patients and communities,” Ms. Thompson said. “Instead, some observers seem to be disappointed that more hospitals are not failing financially.”

A detailed response from the AHA to the MedPAC report is available here.

The Medicare Advisory Payment Commission recommends a higher-than-current-law fee-for-service payment update in 2024 for acute care hospitals and positive payment updates for clinicians paid under the physician fee schedule. It recommends reductions in base payment rates for skilled nursing facilities, home health agencies and inpatient rehabilitation facilities.

MedPAC gave Congress recommendations on payment rates in both traditional fee-for-service and Medicare Advantage for 2024, satisfying a legislative mandate comparing per enrollee spending in both programs.

MedPAC estimates that Medicare spends 6% more for MA enrollees than it would spend if those enrollees remained in fee-for-service Medicare.

In their March 2023 Report to the Congress: Medicare Payment Policy, commissioners said they were acutely aware of how providers’ financial status and patterns of Medicare spending varied in 2020 and 2021 due to COVID-19 and were also aware of higher and more volatile cost increases.

However, they’re statutorily charged to evaluate available data to assess whether Medicare payments are sufficient to support the efficient delivery of care and ensure access to care for Medicare’s beneficiaries, commissioners said.

FEE-FOR-SERVICE RATE RECOMMENDATIONS

MedPAC’s payment update recommendations are based on an assessment of payment adequacy, beneficiaries’ access to and use of care, the quality of the care, the supply of providers, and their access to capital, the report said. As well as higher payments for acute care hospitals and clinicians, MedPAC recommends positive rates for outpatient dialysis facilities.

It recommends providing additional resources to acute care hospitals and clinicians who furnish care to Medicare beneficiaries with low incomes. It also recommends a positive payment update in 2024 for hospice providers concurrent with wage adjusting and reducing the hospice aggregate Medicare payment cap by 20%.

It recommends negative updates, which are reductions in base payment rates, for skilled nursing facilities, home health agencies and inpatient rehabilitation facilities.

Acute care

For acute care hospitals paid under the inpatient prospective payment system, commissioners recommend adding $2 billion to current disproportionate share and uncompensated care payments and distributing the entire amount using a commission-developed “Medicare SafetyNet Index” to direct funding to those hospitals that provide care to large shares of low-income Medicare beneficiaries.

This recommendation got pushback from America’s Essential Hospitals.

“We appreciate the Medicare Payment Advisory Commission’s desire to define safety net hospitals for targeted support, but the commission’s Medicare safety net index (MSNI) could have the perverse effect of shifting resources away from hospitals that need support the most,” said SVP of Policy and Advocacy Beth Feldpush. “The MSNI methodology fails to account for all the nation’s safety net hospitals by overlooking uncompensated care and care provided to non-Medicare, low-income patients – especially Medicaid beneficiaries. Any practical definition of a safety net provider must consider the care of Medicaid and uninsured patients, yet the MSNI misses on both counts.”

Feldpush urged policymakers to develop a federal designation of safety net hospitals and to reject the MSNI.

“Further, policymaking for these hospitals should supplement, rather than redistribute, existing Medicare DSH funding, which reflects a congressionally sanctioned, well-established methodology,” she said.

Physicians and clinicians

For clinicians, the commission recommends that Medicare make targeted add-on payments of 15% to primary care clinicians and 5% to all other clinicians for physician fee schedule services provided to low-income Medicare beneficiaries.

The American Medical Association commended MedPAC, but also said that an update tied to just 50% of the Medicare Economic Index would cause physician payment to chronically fall even further behind increases in the cost of providing care. AMA president Dr. Jack Resneck Jr. urged Congress to pass legislation providing for an annual inflation-based payment update.

MedPAC has long championed a physician payment update tied to the Medicare Economic Index, Resneck said. Physicians have faced the cost of inflation, the COVID-19 pandemic and growing expenses to run medical practices, jeopardizing access to care, particularly in rural and underserved areas.

“Not only have Medicare payments failed to respond adequately, but physicians saw a 2% payment reduction for 2023, creating an additional challenge at a perilous moment,” Resneck said. “As one of the only Medicare providers without an inflationary payment update, physicians have waited a long time for this change. When adjusted for inflation, Medicare physician payment has effectively declined 26% from 2001 to 2023. These increasingly thin or negative operating margins disproportionately affect small, independent, and rural physician practices, as well as those treating low-income or other historically minoritized or marginalized patient communities. Our workforce is at risk just when the health of the nation depends on preserving access to care.”

The AMA and 134 other health organizations wrote to congressional leaders urging for a full inflation-based update to the Medicare Physician Fee Schedule.

MGMA’s SVP of Government Affairs Anders Gilberg said, “Today’s MedPAC report recommends Congress provide an inflationary update to the Medicare base payment rate for physician and other health professional services of 50% of the Medicare Economic Index (MEI), an estimated annual increase of 1.45% for 2024. In the best of times such a nominal increase would not cover annual medical practice cost increases. In the current inflationary environment, it is grossly insufficient.”

MGMA urged Congress to pass legislation to provide an annual inflationary update based on the full MEI.

Ambulatory surgical centers and long-term care hospitals

Previously, the commission considered an annual update recommendation for ambulatory surgical centers (ASCs). However, because Medicare does not require ASCs to submit data on the cost of treating beneficiaries, the commissioners said they had no new significant data to inform an ASC update recommendation for 2024.

Commissioners also previously considered an annual update recommendation for long-term care hospitals (LTCHs). But as the number of cases that qualify for payment under Medicare’s prospective payment system for LTCHs has fallen, they said they have become increasingly concerned about small sample sizes in the analyses of this sector.

“As a result, we will no longer provide an annual payment adequacy analysis for LTCHs but will continue to monitor that sector and provide periodic status reports,” they said in the report.

MEDICARE ADVANTAGE

Commissioners said that overall, indicators point to an increasingly robust MA program. In 2022, the MA program included over 5,200 plan options, enrolled about 29 million Medicare beneficiaries (49% of eligible beneficiaries), and paid MA plans $403 billion (not including Part D drug plan payments).

In 2023, the average Medicare beneficiary has a choice of 41 plans offered by an average of eight organizations. Further, the level of rebates that fund extra benefits reached a record high of about $2,350 per enrollee, on average.

Medicare payments for these extra benefits – which are not covered for beneficiaries in FFS – have more than doubled since 2018. For 2023, the average MA plan bid to provide Medicare Part A and Part B benefits was 17% less than FFS Medicare would be projected to spend for those enrollees.

However, the benefits from MA’s lower cost relative to FFS spending are shared exclusively by the companies sponsoring MA plans and MA enrollees (in the form of extra benefits). The taxpayers and FFS Medicare beneficiaries (who help fund the MA program through Part B premiums) do not realize any savings from MA plan efficiencies.

Medicare should not continue to overpay MA plans, MedPAC said. Over the past few years, the commission has made recommendations to address coding intensity, replace the quality bonus program and establish more equitable benchmarks, which are used to set plan payments, the report said. All of these would stem Medicare’s excess payments to MA plans, helping to preserve Medicare’s solvency and sustainability while maintaining beneficiary access to MA plans and the extra benefits they can provide.

PART D

Medicare’s cost-based reinsurance continues to be the largest and fastest growing component of Part D spending, totaling $52.4 billion, or about 55% of the total, according to the report.

As a result, the financial risk that plans bear, as well as their incentives to control costs, has declined markedly. The value of the average basic benefit that is paid to plans through the capitated direct subsidy has plummeted in recent years.

In 2023, direct subsidy payments averaged less than $2 per member per month, compared with payments of nearly $94 per member, per month, for reinsurance. To help address these issues, in 2020 the commission recommended substantial changes to Part D’s benefit design to limit enrollee out-of-pocket spending; realign plan and manufacturer incentives to help restore the role of risk-based, capitated payments; and eliminate features of the current program that distort market incentives.

In 2022, Congress passed the Inflation Reduction Act, which included numerous policies related to prescription drugs. One such provision is a redesign of the Part D benefit with many similarities to the commission’s recommended changes.

The changes adopted in the IRA will be implemented over the next several years, and are likely to alter the drug-pricing landscape, commissioners said.