Peoria, Ill.-based OSF HealthCare has seen drastic improvements to its financial performance over the last two years, a performance that has allowed the health system to see revenue growth and expand its M&A footprint.

OSF was able to turn around a $43.2 million operating loss (-4.5% margin) in the first quarter ended Dec. 31, 2022, to a $0.9 million gain over the same period in 2023.

But the health system didn’t stop there and, in the first six months ended March 31, 2023, transformed a $60.9 million operating loss to an $8.9 million gain for the same period in 2024.

OSF HealthCare CFO Michael Allen connected with Becker’s to discuss the strategies that helped OSF get to a more steady financial place and some of their plans for the future.

Question: What strategies has OSF HealthCare implemented to help it turn the corner financially?

Michael Allen: OSF Healthcare has improved operating results by more than $70 million compared to FY2023, after seeing an even larger improvement from FY2022 to FY2023. After a very difficult FY2022, from a financial perspective, the organization launched a series of initiatives to return to positive margins.

There has been a focus on reducing the reliance on contract labor, nursing and other key clinical positions, with better recruiting and retaining initiatives. The organization is actively implementing automation for repeatable tasks in hard-to-recruit administrative functions and is actively managing supply and pharmaceutical costs against inflationary pressures.

OSF has also seen revenue growth from patient demand, expanding markets, capacity management and improved payment levels from government and commercial payers.

Q: KSB Hospital and OSF HealthCare recently entered into merger negotiations. How do you expect hospital consolidation to evolve in your market as many small, independent providers continue to face financial challenges and struggle to improve their bottom lines?

MA: The economics of the healthcare delivery system model is challenging in most markets, but particularly difficult for small and independent hospitals and clinics. Given the structure of the payment system and the rising operating costs, I don’t see this pressure easing any time soon.

OSF is looking forward to our opportunity to extend our healthcare ministry to KSB and the greater Dixon area and continue their great legacy of patient care.

Q: What advice would you have for other health system financial leaders looking to get their margins up this year?

MA:There are no silver bullets to improving margins. It’s the daily work of using our costs wisely and executing on important strategies that will win the day. Automation, elimination of non-value-added costs and continuously looking for opportunities to get the best care, patient engagement and workforce engagement is where OSF and other health systems will continue to focus.

Q: An increasing number of hospitals and health systems across the U.S. are dropping some or all of their commercial Medicare Advantage contracts. Where do you see the biggest challenges and opportunities for health systems navigating MA?

MA: As more and more patients and payers are entering Medicare Advantage, we continue to watch our metrics on payment levels to ensure we are being paid fairly and within contract terms for our payer partners.

There does appear to be a trend of increasing denials that often aren’t justified or are not within our contract terms, and we will continuously work to rectify those issues with our payers to ensure our patients receive the appropriate care and OSF is paid fairly for services provided.

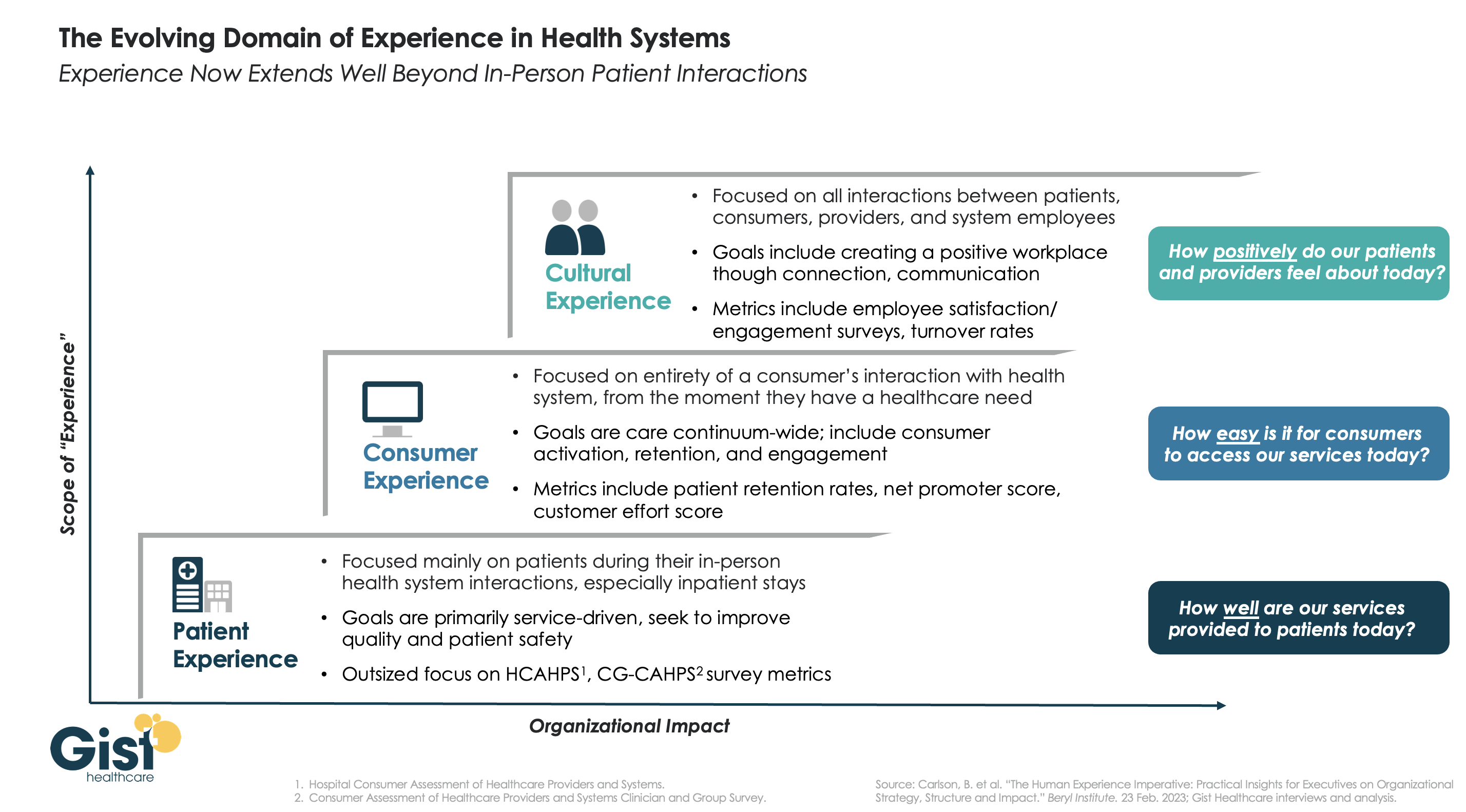

In this week’s graphic, we highlight the importance of broadening the domain of health system experience initiatives beyond patients to include consumers and even employees.

While reimbursements tied to HCAHPS (Hospital Consumer Assessment of Healthcare Providers and Systems) and CG-CAHPS (Clinician and Group Consumer Assessment of Healthcare Providers and Systems) scores have made patient experience a main focus for years, an increasingly consumer-driven healthcare industry means that health systems must consider the experience of all consumers in their markets, with the hopes of meeting their needs and eventually welcoming them as new—or retuning—patients.

Embracing this mindset requires focusing on the entirety of a consumer’s interactions with the health system and the tracking of non-traditional metrics that measure the strength and value of their relationship to the system. Some systems are expanding their experience purview even further by also focusing on the working conditions and morale of their providers and other staff, as a healthy workplace environment serves to better both the patient and consumer experience. Easily accessible services and positive interactions with providers and other staff can determine a consumer’s view of their experience before any care is actually delivered.

Cultural and strategic shifts that integrate experience from the top down into all operational facets of the health system will ultimately strengthen consumer loyalty, employee retention, and the financial health of the system.

On January 1st, 2024 #AB1076 and #SB699, two draconian noncompete laws go into effect. It could put many #employedphysicians in a new position to walk away from #employeeremorse.

AB1076 voids non-compete contracts and require the employer to give written notice by February 14th, 2024 that their contract is void.

Is this a good or bad thing? It depends.

If the contract offers more protections and less risk to the employed physician, and the contract is void – does that mean the whole contract is void? Or is the non-compete voidable?

But for the hospital administrator or practice administrator, we’re about to witness the golden handcuffs come off and administrators will have to compete to retain talent that could be lured away more easily than in the past. But the effect of the non-compete is far more worrisome for an administrator because of the following:

The physicians many freely and fairly compete against the former employer by calling upon, soliciting, accepting, engaging in, servicing or performing business with former patients, business connections, and prospective patients of their former employer.

It could also give rise to tumult in executive positions and management and high value employees like managed care and revenue cycle experts who may have signed noncompete contracts.

If the employer does not follow through with the written notice by February 14th, the action or failure to notify will be “deemed by the statute to be an act of unfair competition that could give rise to other private litigation that is provided for in SB699.

The second law, SB699, provides a right of private action, permitting the former employees subject to SB699 the right to sue for injunctive relief, recovery of actual damages, and attorneys fees. It also makes it a civil violation to enter into or enforce a noncompete agreement. It further applies to employees who were hired outside California but now work in or through a California office.

What else goes away?

Employed physicians can immediately go to work for a competitor and any notice requirement or waiting period (time and distance provisions) are eliminated by the laws. So an administrator could be receiving “adios” messages on January 2nd, and watch market share slip through their fingers like a sieve starting January 3rd.

And what about the appointment book? Typically, appointments are set months in advance, especially for surgeons – along with surgery bookings, surgery block times, and follow up visits.

Hospitals may be forced to reckon with ASCs where the surgeons could not book cases under their non-compete terms and conditions. They could up and move their cases as quickly as they can be credentialed and privileged and their PECOS and NPPES files updated and a new 855R acknowledged as received.

Will your key physicians, surgeons and APPs leave on short notice?

APPs such as PAs and NPs could also walk off and bottleneck appointment schedules, surgical assists, and many office-based procedures that were assigned to them. They could also walk to a new practice or a different hospitals and also freely and fairly compete against the former employer by calling upon, soliciting, accepting, engaging in, servicing or performing business with former patients, business connections, and prospective patients of their former employer.

Next, let’s talk about nurses and CRNAs. If they walk off and are lured away to a nearby ASC or hospital, or home health agency, that will disrupt many touchpoints of the current employer.

Consultants’ contracts are another matter to be reckoned with. In all my California (and other) contracts, contained within them are anti-poaching provisions that state that I may not offer employment to one of their managed care, revenue cycle, credentialing, or business development superstars. Poof! Gone!

The time to conduct a risk assessment is right now! But many of the people who would be assigned this assessment are on holiday vacation and won’t be back until after January 1st. But then again, they too could be lured away or poached.

What else will be affected?

Credentialing and privileging experts should be ready for an onslaught of applications that have to be processed right away. They will not only be hit with new applications, but also verification of past employment for the departing medical staff.

Billing and Collections staff will need to mount appeals and defenses of denied claims without easy access they formerly had with departing employed physicians.

Medical Records staff will need to get all signature and missing documentation cleared up without easy access they formerly had with departing employed physicians.

Managed Care Network Development experts at health plans and PPOs and TPAs will be recredentialing and amending Tax IDs on profiles of former employed physicians who stand up their own practice or become employed or affiliated with another hospital or group practice. This comes at an already hectic time where federal regulations require accurate network provider directories.

The health plans will need to act swiftly on these modifications because NCQA-accredited health plans must offer network adequacy and formerly employed physicians who depart one group but cannot bill for patient visits and surgeries until the contracting mess is cleared up does not fall under “force majeure” exceptions. If patients can’t get appointments within the stated NCQA time frames, the health plan is liable for network inadequacy. I see that as “leverage” because the physician leaving and going “someplace else” (on their own, to a new group or hospital) can push negotiations on a “who needs whom the most?” basis. Raising a fee schedule a few notches is a paltry concern when weight against loss of NCQA accreditation (the Holy Grail of employer requirements when purchasing health plan benefits from a HMO) and state regulator-imposed fines. All it takes to attract the attention of regulators and NCQA are a few plan member complaints that they could not get appointments timely.

Health plans who operate staff model and network model plans that employ physicians, PAs and NPs (e.g., Kaiser and others who employ the participating practitioners and own the brick and mortar clinics where they work) are in for risk of losing the medical staff to “other opportunities.” These employment arrangements are at a huge risk of disruption across the state.

Workers Compensation Clinics that dot the state of California and already have wait times measured in hours as well as Freestanding ERs and Freestanding Urgent Care Clinics could witness a mass exodus of practitioners that disrupt operations and make their walk in model inoperative and unsustainable in a matter of a week.

FQHCs that employ physicians, psychotherapists, nurse practitioners and physician assistants could find themselves inadequately staffed to continue their mission and operations. Could this lead to claims of patient abandonment? Failed Duty of Care? Who would be liable? The departing physician or their employer?

And then, there are people like me – consultants who help stand up new independent and group practices, build new brands, rebrand the physicians under their own professional brands, launch new service lines like regenerative medicine and robotics, cardiac and vascular service lines, analyze managed care agreements, physician, CRNA, psychotherapist, and APP employment agreements. There aren’t many consultants with expertise in these niches. There are even fewer who are trained as paralegals, and have practical experience as advisors or former hospital and group practice administrators (I’ve done both) who are freelancers. I expect I will become very much in demand because of the scarcity and the experience. I am one of very few experts who are internationally-published and peer-reviewed on employment contracts for physicians.

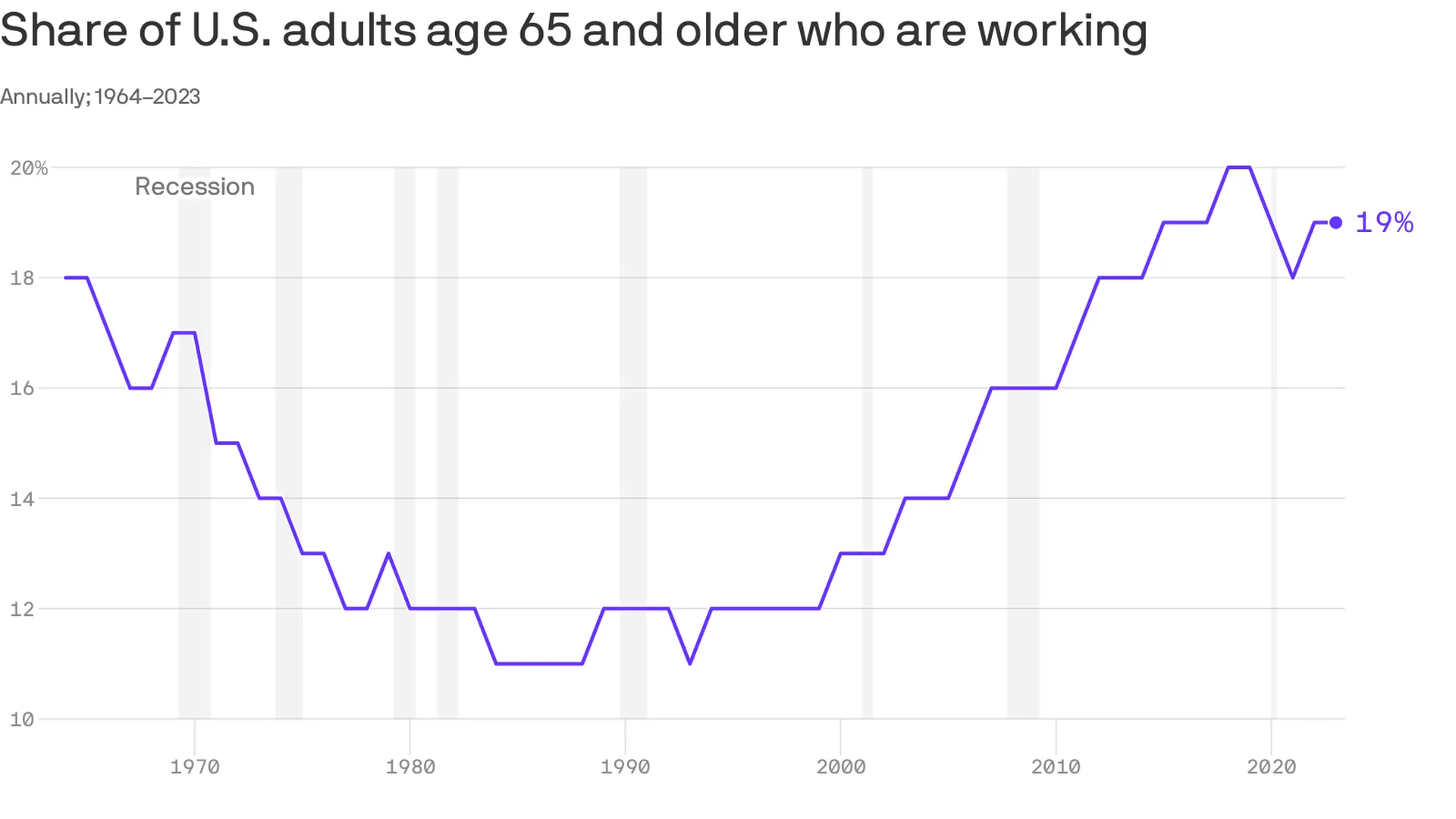

An increasing number of Americans age 65 and older are working — and earning higher wages, per a study from the Pew Research Center out Thursday.

Why it matters:

This is good for the economy, especially as the U.S. population ages — but whether or not it’s good for older Americans is a bit more subjective.

Zoom in:

The share of older adults working has been steadily increasing since the late 1980s, with a detour during the pandemic as older folks retired in greater numbers. Several forces are driving the shift:

Older workers are increasingly likely to have a four-year degree, and typically workers with more education are more likely to be employed.

Technology has made many jobs less physically taxing, so older workers are more likely to take them.

Meanwhile, changes in the Social Security law pushed many to continue working past 65 to get their full retirement benefits.

At the same time, there’s been a shift away from pension plans, which typically force people out of a job at a certain age, into 401(k) style plans that are less restrictive (and less generous, critics say).

By the numbers:

Last year, the typical 65+ worker earned $22 an hour, up from $13 (in 2022 dollars)in 1987. That’s about $3 less than the average for those age 25-64, and the number includes wages of full- and part-time workers.

Be smart:

Before Social Security existed, older people worked — a lot. In the 1880s, about three-fourths of older men were employed, said Richard Fry, senior researcher at Pew. They also didn’t live as long.

Meanwhile, the 65+ age group is a fast-growing one — by 2032 all the baby boomers will be in this category, per the BLS’s projections, and their increased workforce participation is good for an economy that is struggling with long-term labor shortages.

The big picture:

“If people are working longer because they find purpose in their jobs and want to stay engaged, that’s good for them individually,” said Nick Bunker, head of economic research at Indeed Hiring Lab.

It’s also good for the productive capacity of the economy, and the firms where they work. “Older folks have lots of experience and knowledge to pass down,” he said.

Yes, but: If there are people who want to retire, but can’t because of financial constraints, “that’s bad,” he added.

What to watch:

The share of older adults working peaked before the pandemic — will it surpass those levels?

The number hasn’t bounced back as much as anticipated partly because older Americans benefited hugely from the stock market surge and real estate gains of the past few years — and didn’t need to work anymore.

Nurses who work for staffing agencies are much more satisfied than their counterparts who serve hospitals, health systems, home healthcare providers and senior living facilities, according to an Oct. 18 report from MIT Sloan Management Review.

Researchers identified 200 of the largest healthcare employers in the U.S., and calculated how highly nurses rate the organization and senior leadership on Glassdoor from the beginning of COVID-19 through June 2023 (view their ranking here).

The five highest-ranked employers in the sample were staffing agencies, according to the report — and higher compensation only accounts for part of nurses’ satisfaction. Researchers analyzed the free text on Glassdoor to determine how positively nurses spoke about 200 topics, and found that nurses spoke more highly of staffing agencies on issues other than pay.

Overall, 75% of nurses’ comments about staffing agencies were positive, compared with 23% of nurses’ comments about health systems.

Staffing agencies have other healthcare employers beat in problem resolution, the researchers found. Seventy-three percent of nurses said staffing agencies resolved problems efficiently, compared to 31% of nurses employed by hospitals and health systems. The difference was even greater when it came to resolving problems effectively — 55% of nurses say staffing agencies do this, compared to 9% of nurses at hospitals and health systems.

Nurses also rated staffing agencies more highly on several measures related to honesty, according to the report. Three-quarters of nurses employed by staffing agencies spoke highly of their organizations’ speed in replying to inquiries; less than one-quarter of nurses employed by hospitals and health systems praised their organization on timely replies. Staffing agencies scored 41 percentage points higher on transparency, 36 points higher on trust and 46 points higher on honesty than their hospital and health system counterparts.

Although nurses employed by staffing agencies also ranked their compensation and work-related stress levels significantly better than nurses employed by hospitals and health systems, the latter took the lead in some metrics. Nurses prefer hospitals and health systems for health and retirement benefits, learning and development opportunities, and connection with colleagues: all “important aspects of organizational life,” according to the report.

“Healthcare systems can learn from staffing agencies, but they can also leverage their own distinctive advantages to attract and retain nurses,” the report says. “Healthcare systems should invest in their comparative advantages and emphasize them when communicating their value proposition to potential and current employees.”

Hospitals and health systems are seeing some signs of stabilization in 2023 following an extremely difficult year in 2022. Workforce-related challenges persist, however, keeping costs high and contributing to issues with patient access to care. The percentage of respondents who report that they have run at less than full capacity at some time over the past year because of staffing shortages, for example, remains at 66%, unchanged from last year’s State of Healthcare Performance Improvement report. A solid majority of respondents (63%) are struggling to meet demand within their physician enterprise, with patient concerns or complaints about access to physician clinics increasing at approximately one-third (32%) of respondent organizations.

Most organizations are pursuing multiple strategies to recruit and retain staff. They recognize, however, that this is an issue that will take years to resolve—especially with respect to nursing staff—as an older generation of talent moves toward retirement and current educational pipelines fail to generate an adequate flow of new talent. One bright spot is utilization of contract labor, which is decreasing at almost two-thirds (60%) of respondent organizations.

Many of the organizations we interviewed have recovered from a year of negative or breakeven operating margins. But most foresee a slow climb back to the 3% to 4% operating margins that help ensure long-term sustainability, with adequate resources to make needed investments for the future. Difficulties with financial performance are reflected in the relatively high percentage of respondents (24%) who report that their organization has faced challenges with respect to debt covenants over the past year, and the even higher percentage (34%) who foresee challenges over the coming year. Interviews confirmed that some of these challenges were “near misses,” not an actual breach of covenants, but hitting key metrics such as days cash on hand and debt service coverage ratios remains a concern.

As in last year’s survey, an increased rate of claims denials has had the most significant impact on revenue cycle over the past year. Interviewees confirm that this is an issue across health plans, but it seems particularly acute in markets with a higher penetration of Medicare Advantage plans. A significant percentage of respondents also report a lower percentage of commercially insured patients (52%), an increase in bad debt and uncompensated care (50%), and a higher percentage of Medicaid patients (47%).

Supply chain issues are concentrated largely in distribution delays and raw product and sourcing availability. These issues are sometimes connected when difficulties sourcing raw materials result in distribution delays. The most common measures organizations are taking to mitigate these issues are defining approved vendor product substitutes (82%) and increasing inventory levels (57%). Also, as care delivery continues to migrate to outpatient settings, organizations are working to standardize supplies across their non-acute settings and align acute and non-acute ordering to the extent possible to secure volume discounts.

Survey Highlights

98% of respondents are pursuing one or more recruitment and retention strategies

90%have raised starting salaries or the minimum wage

73%report an increased rate of claims denials

71% are encountering distribution delays in their supply chain

70%are boarding patients in the emergency department or post-anesthesia care unit because of a lack of staffing or bed capacity

66% report that staffing shortages have required their organization to run at less than full capacity at some time over the past year

63% are struggling to meet demand for patient access to their physician enterprise

60% see decreasing utilization of contract labor at their organization

44%report that inpatient volumes remain below pre-pandemic levels

32% say that patients concerns or complaints about access to their physician enterprise are increasing

24%have encountered debt covenant challenges during the past 12 months

None of our respondents believe that their organization has fully optimized its use of the automation technologies in which it has already invested

The hospital workforce is critical to the care process and is most often the largest expense on a hospital or health system’s balance sheet. Even before the pandemic, labor expenses — which include costs associated with recruitment and retention, employee benefits and incentives — accounted for more than 50 percent of hospitals’ total expenses, according to the American Hospital Association.

As a result, a slight increase in labor costs can have a tremendous effect on a hospital or health system’s total expenses and operating margins. Hospitals across the country are focused on managing the premium cost of labor, while recruiting and retaining talent remains a priority, and the cost of supplies and drugs also increases due to inflation.

Here’s how 23 health systems’ labor costs are tracking based on the results of their most recent financial documents.

Note: This is not an exhaustive list. Most of the following health systems’ labor costs are for the three months ending 30, with others for the six months ending June 30 and the 12 months ending June 30 — the most recent periods for which financial data is available. The year-over-year percentage increase/decrease is also included.

21. CommonSpirit Health (Chicago) Salaries and benefits: $18.3 billion (+0.7 percent YOY) *For the 12 months ended June 30 **Merged with Broomfield, Colo. -based SCL Health in April 2022

22. Ascension (St. Louis) Salaries, wages and employee benefits: $14.3 billion (-1.3 percent YOY) *For the 12 months ended June 30

Robert Wood Johnson University Hospital in New Brunswick, N.J., said it plans to temporarily cut off healthcare benefits for striking union workers, effective Sept. 1.

Hospital spokesperson Wendy Gottsegen described the move as unfortunate.

“We have said all along that no one benefits from a strike — least of all our nurses. We hope the union considers the impact a prolonged strike is having on our nurses and their families,” Ms. Gottsegen said in an Aug. 28 news release shared with Becker’s. “As of Sept. 1, RWJUH nurses must pay for their health benefits through COBRA. This hardship, in addition to the loss of wages throughout the strike, is very unfortunate and has been openly communicated to the union and the striking nurses since prior to the walkout on Aug. 4.”

The ongoing strike involves the United Steelworkers Local 4-200, which represents about 1,700 nurses at the facility.

Union members voted to authorize a strike in July. The union and hospital have been negotiating a new agreement for months, with the last bargaining session occurring Aug. 16.

During negotiations, the union has said it seeks a contract that provides safe staffing standards, living wages and quality, affordable healthcare.

Local 4-200 President Judy Danella, RN, said in a previous union release, “Our members remain deeply committed to our patients. However, we must address urgent concerns, like staffing. We need enough nurses on each shift, on each floor, so we can devote more time to each patient and keep ourselves safe on the job.”

Several nurses told TAPinto New Brunswick last week that they began preparing for the current situation ahead of the strike, taking overtime shifts and saving as much money as possible. Others told the publication they are taking part-time jobs or temporary employment elsewhere in the nursing field or adjacent roles.

“I think it’s important that you [remember] you might not get the job you want to do at that moment, but people have to do what they have to do to get it done,” Jessica Newcomb, RN, told TAPinto New Brunswick.

Meanwhile, the hospital has contracted with an agency to hire replacement nurses during the strike.

“As always, our top priority is to our patients. RWJUH is open, fully operational and completely staffed, and we remain steadfast in our commitment to deliver the highest quality and always-safe patient care,” Ms. Gottsegen said.

As of Aug. 28, no further dates for negotiations were scheduled by mediators.

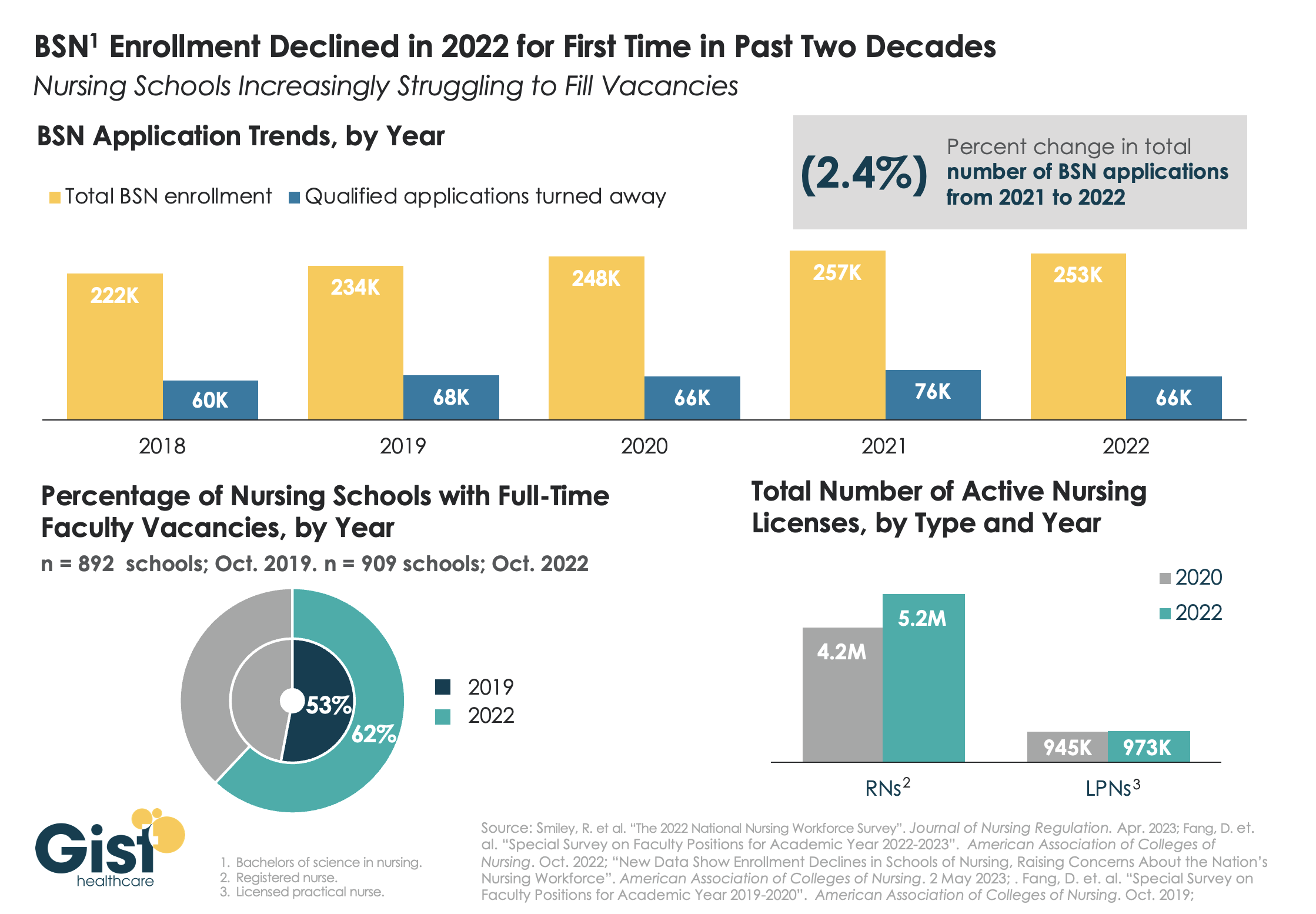

While last week’s graphic looked at how a wave of retirements has hit the nursing workforce, this week we take a look at the pipeline of nurses in training to fill that gap. In recent years, there has been a consistent stream of qualified applicants who want to become BSN nurses, but schools don’t have the capacity to admit them.

One reason: an ongoing shortage of nursing faculty, which recent retirements have exacerbated. The percentage of nursing schools with at least one full-time faculty vacancy grew from53 percent in 2019 to 62 percent in 2022.

Looking at registered nurses (RNs), the number with active licenses has continued to grow at a much higher rate than the supply of licensed practice nurses (LPNs) with active licenses.

The relatively small LPN workforce is especially significant, given rising interest in team-based nursing care, which aims to utilize a higher number of LPNs, supervised by RNs and BSNs.

Expanding training programs with an eye toward the skills and mix needed to deliver team-based care will be critical to ensuring a stable, efficient nursing workforce for future decades.

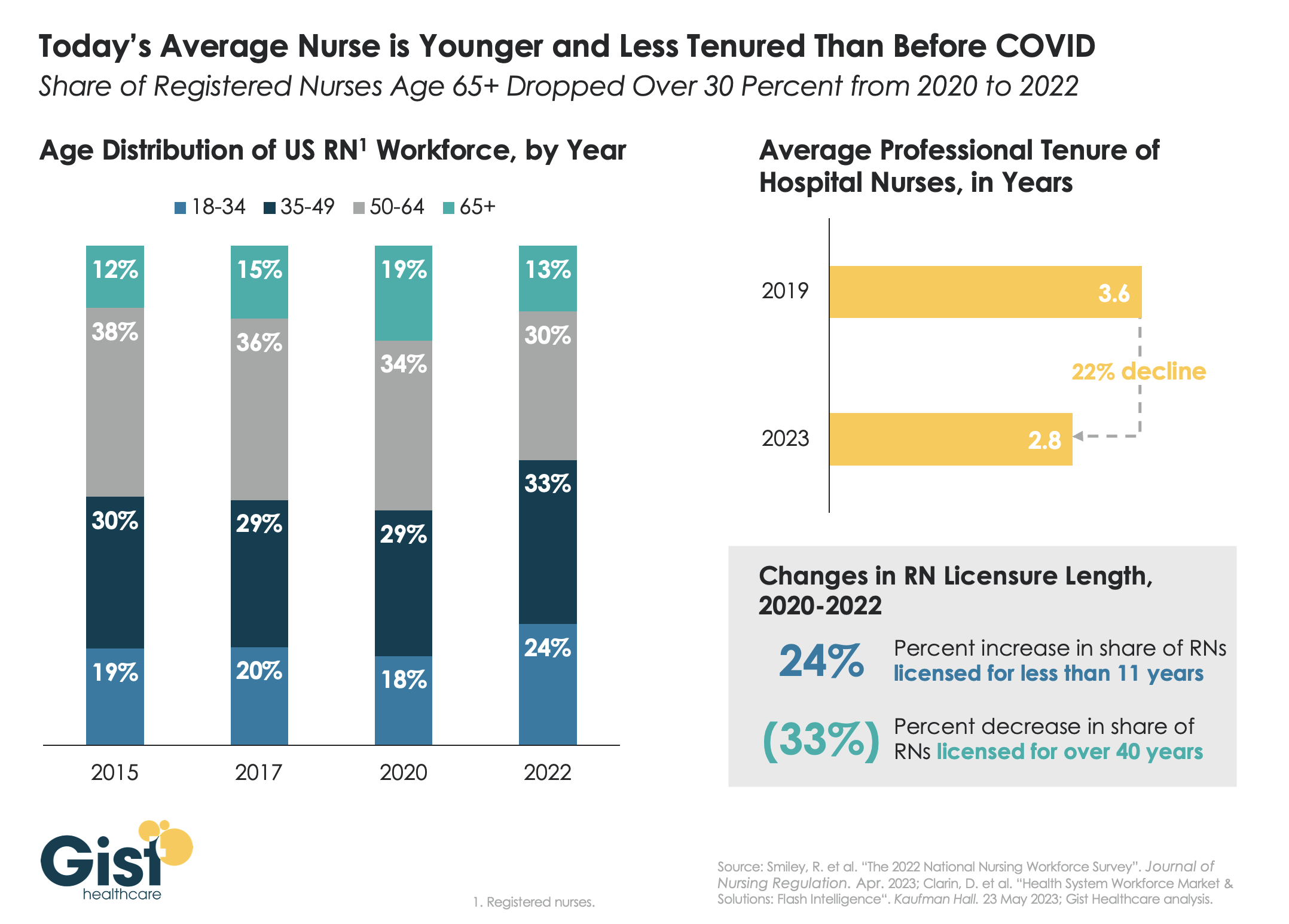

Last week we discussed how hospitals are still struggling to retain talent. This week’s graphic offers one explanation for this trend:

a significant share of older nurses, who continued to work during the height of the pandemic, have now exited the workforce, and health systems are even more reliant on younger nurses.

Between 2020 and 2022, the number of nurses ages 65 and older decreased by 200K, resulting in a reduction of that age cohort from 19 percent to 13 percent of the total nursing workforce. While the total number of nurses in the workforce still increased, the younger nurses filling these roles are both earlier in their nursing careers (thus less experienced), and more likely to change jobs.

Case in point:

From 2019 to 2023, the average tenure of a hospital nurse dropped by 22 percent. The wave of Baby Boomer nurse retirements has also resulted in a 33 percent decrease from 2020 to 2022 in the number of registered nurses who have been licensed for over 40 years.

Given these shifts, hospitals must adjust their current recruitment, retention, training, and mentorship initiatives to match the needs of younger, early-career nurses.