Cartoon – Modern Emergency Coverage

The Affordable Care Act (ACA) made historic strides in expanding access to health insurance coverage by covering an additional 20 million Americans. President Joe Biden ran on a platform of building upon the ACA and filling in its gaps. With Democratic majority in the Senate, aspects of his health care plan could move from idea into reality.

The administration’s main focus is on uninsurance, which President Biden proposes to tackle in three main ways: providing an accessible and affordable public option, increasing tax credits to help lower monthly premiums, and indexing marketplace tax credits to gold rather than silver plans.

However, underinsurance remains a problem. Besides the nearly 29 million remaining uninsured Americans, over 40% of working age adults are underinsured, meaning their out-of-pocket cost-sharing, excluding premiums, are 5-10% of household income or more, depending on income level.

High cost-sharing obligations—especially high deductibles—means insurance might provide little financial protection against medical costs beneath the deductible. Bills for several thousand dollars could financially devastate a family, with the insurer owing nothing at all. Recent trends in health insurance enrollment suggest that uninsurance should not be the only issue to address.

A high demand for low premiums

Enrollment in high deductible health plans (HDHP) has been on a meteoric rise over the past 15 years, from approximately 4% of people with employer-sponsored insurance in 2006 to nearly 30% in 2019, leading to growing concern about underinsurance. “Qualified” HDHPs, which come with additional tax benefits, generally have lower monthly premiums, but high minimum deductibles. As of 2020, the Internal Revenue Service defines HDHPs as plans with minimum deductibles of at least $1,400 for an individual ($2,800 for families), although average annual deductibles are $2,583 for an individual ($5,335 for families).

HDHPs are associated with delays in both unnecessary and necessary care, including cancer screenings and treatment, or skipped prescription fills. There is evidence that Black patients disproportionately experience these effects, which may further widen racial health inequities.

A common prescription has been to expand access to Health Savings Accounts (HSAs), with employer and individual contributions offsetting higher upfront cost-sharing. Employers often contribute on behalf of their employees to HSAs, but for individuals in lower wage jobs without such benefits or without extra income to contribute themselves, the account itself may sit empty, rendering it useless.

A recent article in Health Affairs found that HDHP enrollment increased from 2007 to 2018 across all racial, ethnic, and income groups, but also revealed that low-income, Black, and Hispanic enrollees were significantly less likely to have an HSA, with disparities growing over time. For instance, by 2018, they found that among HDHP enrollees under 200% of the federal poverty level (FPL), only 21% had an HSA, while 52% of those over 400% FPL had an HSA. In short, the people who could most likely benefit from an HSA were also least likely to have one.

If trends in HDHP enrollment and HSA access continue, it could result in even more Americans who are covered on paper, yet potentially unable to afford care.

Addressing uninsurance could also begin to address underinsurance

President Biden’s health care proposal primarily addresses uninsurance by making it more affordable and accessible. This can also tangentially tackle underinsurance.

To make individual market insurance more affordable, Biden proposes expanding the tax credits established under the ACA. His plan calls for removing the 400% FPL cap on financial assistance in the marketplaces and lowering the limit on health insurance premiums to 8.5% of income. Americans would now be able to opt out of their employer plan if there is a better deal on HealthCare.gov or their state Marketplace. Previously, most individuals who had an offer of employer coverage were ineligible for premium subsidies—important for individuals whose only option might have been an employer-sponsored HDHP.

Biden also proposes to index the tax credits that subsidize premiums to gold plans, rather than silver plans as currently done. This would increase the size of these tax credits, making it easier for Americans to afford more generous plans with lower deductibles and out-of-pocket costs, substantially reducing underinsurance.

The most ambitious of Biden’s proposed health policies is a public option, which would create a Medicare-esque offering on marketplaces, available to anyone. As conceived in Biden’s proposal, such a plan would eliminate premiums and having minimal-to-no cost-sharing for low-income enrollees; especially meaningful for under- and uninsured people in states yet to expand Medicaid.

Moving forward: A need to directly address underinsurance

More extensive efforts are necessary to meaningfully address underinsurance and related inequities. For instance, the majority of persons with HDHPs receive coverage through an employer, where the employer shares in paying premiums, yet cost-sharing does not adjust with income as it can in the marketplace. Possible solutions range from employer incentives to expanding the scope of deductible-exempt services, which could also address some of the underlying disparities that affect access to and use of health care.

The burden of high cost-sharing often falls on those who cannot afford it, while benefiting employers, healthy employees, or those who can afford large deductibles. Instead of encouraging HSAs, offering greater pre-tax incentives that encourage employers to reabsorb some of the costs that they have shifted on their lower-income employees could prevent the income inequity gap from widening further.

Under the ACA, most health insurance plans are required to cover certain preventative services without patient cost-sharing. Many health plans also exempt other types of services from the deductible – from generic drugs to certain types of specialist visits – although these exemptions vary widely across plans. Expanding deductible-exempt services to include follow-up care or other high-value services could improve access to important services or even medication adherence without high patient cost burden. Better educating employees about what services are exempt would make sure that patients aren’t forgoing care that should be fully covered.

Health insurance is complicated. Choosing a plan is only the start. More affordable choices are helpful only if these choices are fully understood, e.g., the tradeoff between an HDHP’s lower monthly premium and the large upfront out-of-pocket cost when using care. Investing in well-trained, diverse navigators to help people understand how their options work with their budget and health care needs can make a big difference, given that low health insurance literacy is related to higher avoidance of care.

The ACA helped expand coverage, but now it’s time to make sure the coverage provided is more than an unused insurance card. The Biden administration has the opportunity and responsibility to make progress not only on reducing the uninsured rate, but also in reducing disparities in access and patient affordability.

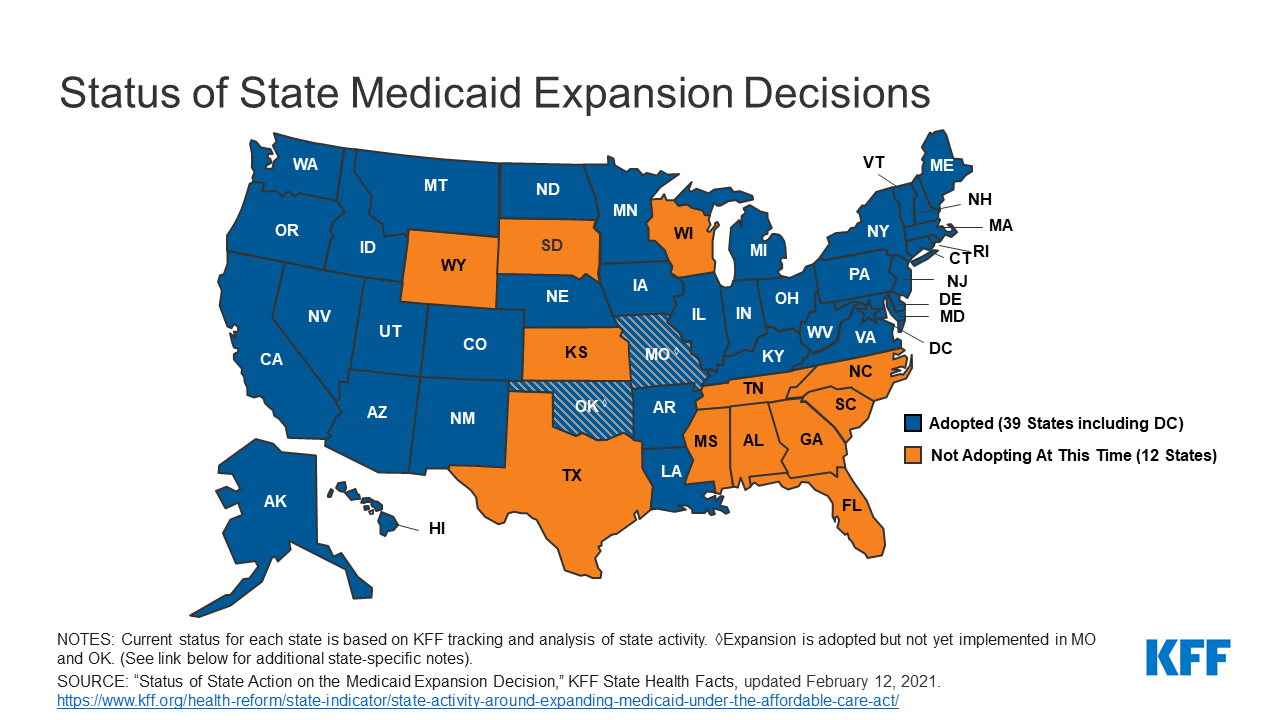

President Joe Biden has an unexpected opening to cut deals with red states to expand Medicaid, raising the prospect that the new administration could extend health protections to millions of uninsured Americans and reach a goal that has eluded Democrats for a decade.

The opportunity emerges as the covid-19 pandemic saps state budgets and strains safety nets. That may help break the Medicaid deadlock in some of the 12 states that have rejected federal funding made available by the Affordable Care Act, health officials, patient advocates and political observers say.

Any breakthrough will require a delicate political balancing act. New Medicaid compromises could leave some states with safety-net programs that, while covering more people, don’t insure as many as Democrats would like. Any expansion deals would also need to allow Republican state officials to tell their constituents they didn’t simply accept the 2010 health law, often called Obamacare.

“Getting all the remaining states to embrace the Medicaid expansion is not going to happen overnight,” said Matt Salo, executive director of the nonpartisan National Association of Medicaid Directors. “But there are significant opportunities for the Biden administration to meet many of them halfway.”

Key to these potential compromises will likely be federal signoff on conservative versions of Medicaid expansion, such as limits on who qualifies for the program or more federal funding, which congressional Democrats have proposed in the latest covid relief bill.

But any deals would bring the country closer to fulfilling the promise of the 2010 law, a pillar of Biden’s agenda, and begin to reverse Trump administration efforts to weaken public programs, which swelled the ranks of the uninsured.

“A new administration with a focus on coverage can make a difference in how these states proceed,” said Cindy Mann, who oversaw Medicaid in the Obama administration and now consults extensively with states at the law firm Manatt, Phelps & Phillips.

Medicaid, the half-century-old health insurance program for the poor and people with disabilities, and the related Children’s Health Insurance Program cover more than 70 million Americans, including nearly half the nation’s children.

Enrollment surged following enactment of the health law, which provides hundreds of billions of dollars to states to expand eligibility to low-income, working-age adults.

However, enlarging the government safety net has long been anathema to most Republicans, many of whom fear that federal programs will inevitably impose higher costs on states.

And although the GOP’s decade-long campaign to “repeal and replace” the health law has largely collapsed, hostility toward it remains high among Republican voters.

That makes it perilous for politicians to embrace any part of it, said Republican pollster Bill McInturff, a partner at Public Opinion Strategies. “A lot of Republican state legislators are sitting in core red districts, looking over their shoulders at a primary challenge,” he said.

Many conservatives have called instead for federal Medicaid block grants that cap how much federal money goes to states in exchange for giving states more leeway to decide whom they cover and what benefits their programs offer.

Many Democrats and patient advocates fear block grants will restrict access to care. But just before leaving office, the Trump administration gave Tennessee permission to experiment with such an approach.

“It’s a frustrating place to be,” said Tom Banning, the longtime head of the Texas Academy of Family Physicians, which has labored to persuade the state’s Republican leaders to drop their opposition to expanding Medicaid. “Despite covid and despite all the attention on health and disparities, we see almost no movement on this issue.”

Some 1.5 million low-income Texans are shut out of Medicaid because the state has resisted expansion, according to estimates by KFF. (KHN is an editorially independent program of KFF.)

An additional 800,000 people are locked out in Florida, which has also blocked expansion.

Two million more are caught in the 10 remaining holdouts: Alabama, Georgia, Kansas, Mississippi, North Carolina, South Carolina, South Dakota, Tennessee, Wisconsin and Wyoming.

Advocates of Medicaid expansion, which is broadly popular with voters, believe they may be able to break through in a handful of these states that allow ballot initiatives, including Mississippi and South Dakota.

Since 2018, voters in Idaho, Nebraska, Utah, Oklahoma and Missouri have backed initiatives to expand Medicaid eligibility, effectively circumventing Republican political leaders.

“The work that we’ve done around the country shows that no matter where people live — red state or blue state — there is overwhelming support for expanding access to health care,” said Kelly Hall, policy director of the Fairness Project, a nonprofit advocacy group that has helped organize the Medicaid measures.

But most of the holdout states, including Texas, don’t allow citizens to put initiatives on the ballot without legislative approval.

And although Florida has an initiative process, mounting a ballot campaign there is challenging, as political advertising is expensive. Unlike in many states, Florida’s leading hospital association hasn’t backed expansion.

Another route for expansion: compromises that could win over skeptical Republican state leaders and still get the green light from the Biden administration.

The Obama administration approved conservative Medicaid expansion in Arkansas, which funneled enrollees into the commercial insurance market, and in Indiana, which forced enrollees to pay more for their medical care.

Money is a major focus of current talks in several states, according to health officials, advocates and others involved in efforts across the country.

The health law at first fully funded Medicaid expansion with federal money, but after the first three years, states had to begin paying part of the tab. Now, states must come up with 10% of the cost of expansion.

Even that small share is a challenge for states, many of which are reeling from the economic downturn caused by the pandemic, said David Becker, a health economist at the University of Alabama-Birmingham who has assisted efforts to expand Medicaid in that state.

“The question is: Where do we get the money?” Becker said, noting that some Republicans may be open to expanding Medicaid if the federal government pays the full cost of the expansion, at least for a year or two.

Other efforts to find ways to offset state costs are underway in Kansas and North Carolina, which have Democratic governors whose expansion plans have been blocked by Republican state legislators. Kansas Gov. Laura Kelly this month proposed using money from the sale and taxation of medical marijuana.

Some Democrats in Congress are pushing to revise the health law to provide full federal funding to states that expand Medicaid now. Separately, in the stimulus bill unveiled last week, House Democrats proposed an additional boost in total Medicaid aid to states that expand.

Other Republicans have signaled interest in partly expanding Medicaid, opening the program to people making up to 100% of the federal poverty level, or about $12,900, rather than 138%, or $17,800, as the law stipulated.

The Obama administration rejected this approach, but the idea has gained traction in several states, including Georgia.

It’s unclear what kind of compromises the new administration may consider, as Biden has yet to even nominate someone to oversee the Medicaid program.

Some Democrats say it’s time to give up the search for middle ground with Republicans on Medicaid.

A better strategy, they say, is a new government insurance plan, or public option, for people in non-expansion states, a strategy Biden endorsed on the campaign trail.

“Democrats can no longer countenance millions of Americans living in poverty without insurance,” said Chris Jennings, a Democratic health care strategist who worked in the White House under Presidents Bill Clinton and Barack Obama and served on Biden’s transition team.

“This is why the Biden public option or other new ways to secure affordable, meaningful care should become the order of the day for people living in states like Florida and Texas.”

Young adults were among the most likely to be uninsured prior to the Affordable Care Act, but the law’s Medicaid expansion had a significant impact on those rates, according to a new study.

Research published by Urban Institute, this week shows the uninsured rate for people aged 19 to 25 declined from 30% to 16% between 2011 and 2018, while Medicaid enrollment for this population increased from 11% to 15% in that window.

The coverage increases were felt most keenly between 2013 and 2016, when many of the ACA’s key tenets were carried out, including Medicaid expansion and the launch of the exchanges, according to the study.

“Before the ACA, adolescents in low-income households often aged out of eligibility for public health insurance coverage through Medicaid or the Children’s Health Insurance Program as they entered adulthood,” the researchers wrote. “Further, young adults’ employment patterns made them less likely than older adults to have an offer of employer-sponsored insurance coverage.”

States that expanded Medicaid saw greater declines in the number of young people without insurance, the study found.

On average, the uninsured rates among young people declined from nearly 28% in 2011 to 11% in 2018, according to the analysis. In non-expansion states, however, the uninsured rate decreased from about 33% to nearly 21%.

In expansion states, Medicaid enrollment for people aged 19 to 25 rose from 12% in 2011 to close to 21%, according to the study, while enrollment in non-expansion states remained flat.

Urban’s researchers estimate that Medicaid expansion is linked to a 3.6 percent point decline in uninsurance among young people overall, and had the highest impact on young Hispanic people. Uninsurance decreased by 6 percentage points among Hispanic young people, the study found, and that population had the largest uninsured rate prior to the ACA.

“The effects of Medicaid expansion on young adults’ health insurance coverage and health care access provide evidence of the initial pathways through which Medicaid expansions could improve young adults’ overall health and trajectories of health throughout adulthood,” the researchers wrote.

“Beyond coverage and access to preventive care, Medicaid expansion may affect young adults’ health care use in ways not examined in our report. Thus, ensuring young adults have health insurance coverage and access to affordable care is a critical first step toward long-term health,” they wrote.

https://mailchi.mp/41540f595c92/the-weekly-gist-february-12-2021?e=d1e747d2d8

Starting next week, millions of uninsured Americans will have the opportunity to sign up for coverage on the federal insurance marketplace, the result of President Biden’s executive order to create a 90-day special enrollment period. The graphic above highlights the potential impact of this enrollment period on the uninsured population.

According to a Kaiser Family Foundation analysis, of the nearly 15M uninsured who are marketplace-eligible, nearly 9M qualify for free or subsidized coverage. Enrollment of these individuals will come with added challenges, as they tend to be less educated, younger, more rural, and less likely to speak English, as compared to the general population. An Urban Institute survey found almost half of uninsured individuals are unfamiliar with marketplace coverage options, and nearly two-thirds lack an understanding of available financial assistance.

The federal government is dedicating $50M to advertise the special enrollment period, to assist with outreach and education. Given the population most likely to have lost insurance due to the COVID pandemic, this funding will be critical to making sure eligible people take advantage or free or low-cost coverage.

https://mailchi.mp/41540f595c92/the-weekly-gist-february-12-2021?e=d1e747d2d8

Ahead of a Supreme Court hearing in March to consider the legality of imposing work requirements as a condition of gaining Medicaid coverage, the Centers for Medicare and Medicaid Services (CMS) were expected to inform states on Friday of plans to rescind the controversial Trump administration policy.

Under the previous administration, ten states had applied for and were approved to use waiver authority to impose work requirements on Medicaid enrollees, and several other states were in the process of submitting applications. Critics (including us) have long held that such requirements, while nominally intended to introduce an element of “personal responsibility” to the safety-net coverage program for low-income Americans, actually serve to hinder access to care, and jeopardize the health status of already vulnerable populations; in addition, the added expense of program infrastructure often exceeds anticipated cost savings.

The policy was a favored project of former CMS administrator Seema Verma, who helped craft a similar program for the state of Indiana before joining the Trump administration. Among states granted waiver authority to impose work requirements, only Arkansas ever fully implemented the policy, before the legality of the waivers was challenged successfully in lower courts.

The Biden administration’s recision of work requirements is part of a broader reversal of Trump-era healthcare policies. This week the Justice Department notified the Supreme Court that it was switching sides in the closely watched case questioning the constitutionality of the Affordable Care Act (ACA), although the court has already heard the case and is expected to rule this spring. Starting Monday, the Biden team will also reopen the federal insurance marketplace for a special enrollment period, bolstering funding for outreach to ensure those eligible are aware of coverage options. And as part of its proposed COVID relief legislation, the administration plans to increase subsidies to help individuals buy coverage on the exchanges, and to increase funding to support state Medicaid programs—policies that got a boost this week from a broad coalition of healthcare industry groups, including health plans, doctors, and hospitals.

As the administration rounds out its health policy team, we’d expect a continued focus on strengthening the core pillars of the ACA, along with a greater focus on ensuring health equity and addressing disparities. Meanwhile, two key positions remain unfilled: CMS administrator and commissioner of the Food and Drug Administration (FDA). These slots will likely remain open until the looming confirmation battle over Biden’s nominee for Secretary of Health and Human Services (HHS), California Attorney General Xavier Becerra, has been settled.

The groups said that Americans “deserve a stable healthcare market that provides access to high-quality care and affordable coverage for all.”

This week, a coalition of healthcare and employer groups called for achieving universal health coverage by expanding financial assistance to consumers, bolstering enrollment and outreach efforts, and taking additional steps to protect those who have lost or are at risk of losing employer-based coverage because of the economic downturn caused by the COVID-19 pandemic.

The Affordable Coverage Coalition encompasses groups representing the nation’s doctors, hospitals, employers and insurers. They include America’s Health Insurance Plans, American Hospital Association, American Medical Association, American Academy of Family Physicians, Blue Cross Blue Shield Association, Federation of American Hospitals and the American Benefits Council.

They have banded together to advocate for achieving universal coverage via expansion of the Affordable Care Act, which is supported by President Biden. Biden also intends to achieve universal coverage through a Medicare-like public option — a government-run health plan that would compete with private insurers.

WHAT’S THE IMPACT

Despite a lot of pre-election talk about universal healthcare coverage from elected officials and those vying for public office, achieving this has remained an elusive goal in the U.S. In a joint statement of principles, the groups said that Americans “deserve a stable healthcare market that provides access to high-quality care and affordable coverage for all.”

“Achieving universal coverage is particularly critical as we strive to contain the COVID-19 pandemic and work to address long-standing inequities in healthcare access and outcomes,” the groups wrote.

The organizations support a number of steps to make health coverage more accessible and affordable, including protecting Americans who have lost or are at risk of losing employer-provided health coverage from becoming uninsured.

They also want to make Affordable Care Act premium tax credits and cost-sharing reductions more generous, and expand eligibility for them, as well as establish an insurance affordability fund to support any unexpected high costs for caring for those with serious health conditions, or to otherwise lower premiums or cost-sharing for ACA marketplace enrollees.

Also on the group’s to-do list: Restoring federal funding for outreach and enrollment programs; automatically enrolling and renewing those eligible for Medicaid and premium-free ACA marketplace plans; and providing incentives for additional states to expand Medicaid in order to close the low-income coverage gap.

THE LARGER TREND

The concept of universal coverage is gaining traction among patients thanks in large part to the COVID-19 pandemic. In fact, A Morning Consult poll taken in the pandemic’s early days showed about 41% of Americans say they’re more likely to support universal healthcare proposals. Twenty-six percent of U.S. adults say they’re “much more likely” to support such policy initiatives, while 15% say they’re somewhat more likely.

As expected, Democrats were the most favorable to the idea, with 59% saying they were either much more likely or somewhat more likely to support a universal healthcare proposal. Just 21% of Republicans said the same. Independents were somewhere in the middle, with 34% warming up to the idea of blanket coverage.

More than 21% of Republicans said they were less likely to support universal care in the wake of the COVID-19 crisis. Seven percent of independents reported the same, while for Democrats the number was statistically insignificant.

During his campaign, President Joe Biden said he supported a public option for healthcare coverage. He also pledged to strengthen the Affordable Care Act. By executive order, Biden opened a new ACA enrollment period for those left uninsured. It begins February 15 and goes through May 15.

Under the Biden Administration, the DOJ says the ACA can stand even though there is no longer a tax penalty for not having health insurance.

The Department of Justice, under the Biden Administration, has told the Supreme Court that it has changed its stance on the Affordable Care Act.

The DOJ previously filed a brief contending that the ACA was unconstitutional because the individual mandate was inseverable from the rest of the law.

Following the change in Administration, the DOJ has reconsidered the government’s position and now takes the position that the ACA can stand, even though there is no longer a mandate for consumers to have health insurance or face a tax penalty, according to a February 10 filing.

WHY THIS MATTERS

Hospitals and health systems support the change in position.

“Without the ACA, millions of Americans will lose protections for pre-existing conditions and the health insurance coverage they have gained through the exchange marketplaces and Medicaid. We should be working to achieve universal coverage and preserve the progress we have made, not take coverage and consumer protections away,” said American Hospital Association CEO and president Rick Pollack.

The Supreme Court is expected to return a decision before the end of the term in June.

THE LARGER TREND

The Supreme Court heard oral arguments on November 10, 2020 regarding whether the elimination of the tax penalty made the remainder of the ACA invalid under the law.

The DOJ sided with the Trump Administration and Republican states that brought the legal challenge, while 20 Democratic attorneys general supported the ACA and asked the court for quick resolution.

They were led by California Attorney General Xavier Becerra, who is Biden’s pick to head the Department of Health and Human Services.

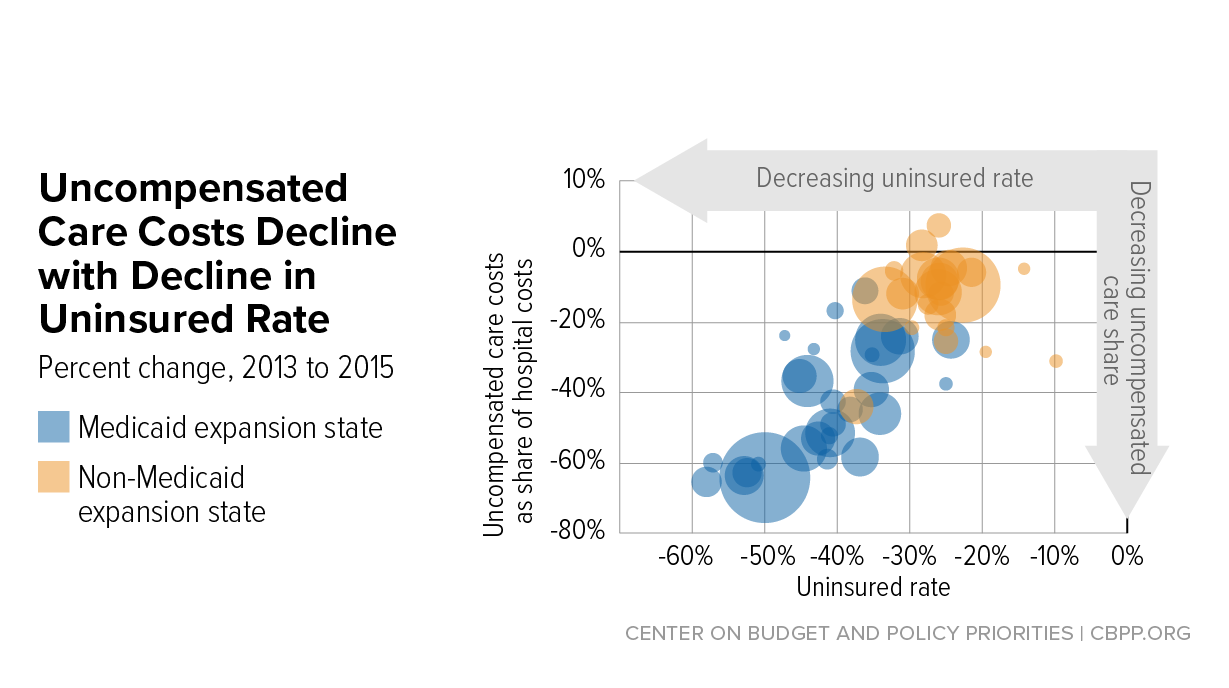

Hospital uncompensated care costs were up from $41.3B in 2018 and $38.4B in 2017, revealing an upward trend, according to AHA data.

Hospital uncompensated care costs increased right before the COVID-19 pandemic hit, according to new data from the American Hospital Association (AHA).

AHA data showed that hospitals incurred a new high of $41.61 billing in uncompensated care costs in 2019, the most recent year for which the group had complete data.

Uncompensated care costs in 2019 were up from $41.3 billion in 2018 and $38.4 billion in 2017 and were the second-highest per AHA records. Hospitals reported the most uncompensated care costs in 2013 when they incurred $46.8 billion.

Hospital uncompensated care costs decreased after the all-time high in 2013, but have recently started to tick back up after holding steady at $38.4 in 2016 and 2017.

In just the last 20 years, hospitals of all types have provided more than $660 billion in uncompensated care to patients, AHA reported. And that figure does not fully account for other ways in which provides provide financial assistance to patients of limited means, the group stated.

Each year, AHA aggregates data on uncompensated care, or care provided for which no reimbursement is received by hospitals from patients or payers. The data comes from the group’s Annual Survey of Hospitals, a comprehensive report of hospital financial data.

Uncompensated care is the sum of a hospital’s bad debt and financial assistance it provides, AHA explained.

Bad debt occurs when a hospital does not expect to obtain reimbursement for care provided, such as when patients are unable to pay their financial responsibility and do not qualify for financial assistance or are unwilling to pay their bills.

Hospitals also provide varying levels of financial assistance, AHA added. Financial assistance supports patients who cannot afford to pay and qualify for support from the hospital based on policies it has established based on the facility’s mission, financial condition, and geographic location, among other factors.

Combined, bad debt and financial assistance charges total a hospital’s uncompensated care charges, which is then multiplied by a hospital’s cost-to-charge ratio to determine total uncompensated care costs.

AHA noted that it expressed uncompensated care in costs versus charges because of significant variations in hospital payer mixes. Publishing the information as costs rather than charges enables better comparison across hospitals, the group said.

Nearly half of hospitals (48 percent) have seen bad debt and uncompensated care increase recently as a result of the ongoing COVID-19 pandemic, an analysis from consulting firm Kaufman Hall revealed.

More than 40 percent of hospitals also reported increases in percentage of uninsured or self-pay patients (44 percent) and the percentage of Medicaid patients (41 percent), which both contribute to unfunded or underfunded care at hospitals.

“The challenges brought on by the COVID-19 pandemic have affected nearly every aspect of hospital financial and clinical operations,” Lance Robinson, a managing director at Kaufman Hall, said at the time. “Organizations have responded to the challenge by adjusting their operations and strengthening important community relationships.”

Hospital uncompensated care costs – and bad debt as a result – are likely to increase in 2020 as hospitals come to terms with the impact COVID-19 has had on their financial health.

Already, hospitals have lost an estimated $323 billion in 2020 as a result of the COVID-19 pandemic, according to earlier projections from AHA.

About half of US hospitals also started the year in the red, AHA and Kaufman Hall stated in a recent report. The organizations predicted that hospital margins would sink to -7 percent in the second half of 2020 without comprehensive financial support from the government, but could decrease to a low of -11 percent if COVID-19 continued to periodically surge as it has.

On January 14, 2021, Planned Parenthood Southeast and the Feminist Women’s Health Center filed a lawsuit challenging the Trump administration’s approval of Georgia’s waiver under Section 1332 of the Affordable Care Act (ACA). The lawsuit was filed in federal district court in DC. This post summarizes that legal challenge as well as parts of President Biden’s recent proposed pandemic relief package that relate to the ACA and coverage. The $1.9 trillion American Rescue Plan includes several coverage-related proposals and would follow the pandemic relief passed by Congress in December 2020.

Regular readers know that the Trump administration—through the Centers for Medicare and Medicaid Services (CMS) and the Treasury Department—approved a broad waiver request from Georgia under Section 1332 of the ACA. The approved waiver authorizes the state to establish a reinsurance program for plan year 2022 and eliminate the use of HealthCare.gov beginning with plan year 2023. CMS and Treasury approved the waiver application on November 1, 2020. The history of Georgia’s waiver application and approval is summarized in prior posts as well as in the complaint filed in the lawsuit.

The reinsurance portion of the waiver is straightforward; of the 16 states with an approved Section 1332 waiver, all but one state has established a state-based reinsurance program. But the second part of the waiver application, known as the Georgia Access Model, is far more controversial. This is the broadest waiver yet to be approved under Section 1332 and relies on interpretations of Section 1332 made in much-criticized Trump-era guidance from 2018.

Critics have long argued that Georgia’s proposal fails to satisfy Section 1332’s procedural and substantive guardrails, meaning it could not be lawfully approved by the Trump administration. Given this controversy, legal challenges to the waiver approval were expected.

Planned Parenthood Southeast and the Feminist Women’s Health Center—represented by Democracy Forward—filed a lawsuit in federal district court in DC on January 14, 2021. The lawsuit alleges that the Trump administration’s 2018 guidance and approval of Georgia’s waiver are unlawful because these actions violate Section 1332 of the ACA and the Administrative Procedure Act (APA). The lawsuit also cites many of the Trump administration’s ongoing efforts to undermine the ACA as evidence that the 2018 guidance and waiver approval are part of a pattern of ACA sabotage.

In particular, the plaintiffs argue that the 2018 guidance and waiver approval are contrary to Section 1332, exceed the scope of the agencies’ authority (by allowing states to waive non-waivable provisions of the ACA), and are arbitrary and capricious. They also argue that the waiver approval failed to satisfy procedural requirements under the ACA and APA because Georgia and the Trump administration “rushed through the process without adequate time for public comment and without adequate clarification of how the state intends to approach key issues.” Here, the lawsuit points to the fact that Georgia went through four iterations of its waiver application, that its application was incomplete, and that only eight comments (less than one half of one percent) of the 1,826 total comments submitted during the most recent federal public comment period were in support of the Georgia Access Model.

As such, the plaintiffs ask the court to vacate both the approved waiver and the 2018 guidance and declare that they are unlawful. They also ask that the federal government be enjoined from taking further action on Georgia’s waiver or considering other waivers under the 2018 guidance. The plaintiffs acknowledge that the reinsurance portion of the waiver is uncontroversial and that the focus of the lawsuit is on the Georgia Access Model; however, the plaintiffs challenge approval of the waiver as a whole and ask the court to set aside the waiver in whole or in part. The plaintiffs have not sued Georgia, although it is possible that Georgia may ask to intervene in the litigation to defend its interests.

Much of the lawsuit turns on how the Trump administration interpreted the statutory guardrails under Section 1332 and long-standing concerns about direct enrollment and enhanced direct enrollment. Federal officials can grant a Section 1332 waiver only if a state demonstrates that their proposal meets certain statutory “guardrails.” These guardrails ensure that a waiver proposal will 1) provide coverage that is at least as comprehensive as ACA coverage ( “comprehensiveness” guardrail); 2) provide coverage and cost-sharing protections that are at least as affordable as ACA requirements (“affordability” guardrail); 3) provide coverage to at least a comparable number of residents as under the ACA ( “coverage” guardrail); and 4) not increase the federal deficit. The Obama administration issued guidance in 2015 on its interpretation of these guardrails.

In 2018, the Trump administration replaced that guidance and adopted its own interpretation, which many argued was inconsistent with Section 1332. The 2018 guidance tried to pave the way for the Trump administration to approve waivers where only some coverage under the waiver (instead of all coverage) satisfied the comprehensiveness and affordability guardrails. Under this view, waivers could be approved even if only some coverage under the waiver was as comprehensive, as affordable, and as available as coverage provided under the ACA. The 2018 guidance would also allow waivers to expand access to plans that do not have to meet the ACA’s requirements. (Separately, the Trump administration issued a final rule to codify the 2018 guidance’s interpretations into regulations.)

The lawsuit argues that the Georgia Access Model violates all four statutory guardrails because it will “drastically underperform the ACA.” The waiver proposal could lead to net enrollment losses in Georgia, which violates the coverage guardrail. The waiver could lead some consumers to enroll in non-ACA plans (such as short-term plans) with benefit gaps, which violates the comprehensiveness guardrail. And consumers will have to pay higher premiums and out-of-pocket costs through higher broker commissions, reduced competition, and adverse selection against the ACA markets, which violates the affordability guardrail and potentially the deficit neutrality guardrail (since higher ACA premiums mean higher federal outlays in the form of premium tax credits).

As health care providers in Georgia, Planned Parenthood Southeast and the Feminist Women’s Health Center allege they will be harmed for several reasons. They argue that the Georgia Access Model will make it more difficult and expensive for their patients to obtain health insurance. Fewer patients with health insurance will result in higher levels of uncompensated care. More uncompensated care will strain the plaintiffs’ resources and limit other services, such as community outreach. The loss of coverage resulting from the waiver will leave their patients in worse health and develop more complex treatment needs, making it more expensive for plaintiffs to treat those patients as a result. And approval of the waiver will make it more complicated for the plaintiffs to assist their patients with enrollment.

The lawsuit was assigned to Judge James E. Boasberg of the federal district court for DC. Health policy watchers know Judge Boasberg as the judge who repeatedly invalidated the Trump administration’s approval of state Section 1115 waivers with work and community engagement requirements. He is thus no stranger to assessing the legality of waiver approvals under the APA and other federal statutes.

The lawsuit will proceed, and the Biden administration will be responsible for filing a response in court. One potential option could be for the Biden administration to ask the court for a stay while it revisits the approved waiver and perhaps holds another round of public comment on the most recent version of the waiver (which, as the lawsuit points out, was never submitted for public comment). The Biden administration could consider any new comments in reevaluating approval of the Georgia Access Model.

If the federal government newly concludes that the proposal fails to satisfy the substantive guardrails, it could have grounds to amend, suspend, or terminate Georgia’s waiver, so long as certain procedures are followed. This is because the terms and conditions of the waiver agreement between the federal government and Georgia (as well as implementing regulations) always give the federal government “the right to suspend or terminate a waiver, in whole or in part, any time before the date of expiration, if the Secretaries determine that the state materially failed to comply with the terms” of the waiver.

Georgia’s waiver agreement includes some unique terms and conditions relative to waivers in other states. Those terms seem designed to limit the federal government’s ability to suspend or terminate Georgia’s waiver. But the federal government can do so as long as it complies with relevant procedures. This includes notifying Georgia of its determination, providing an effective date, and citing reasons for the amendment or termination (i.e., why the Georgia Access Model fails to satisfy Section 1332’s substantive guardrails). Georgia would have 90 days to respond, with the possibility of providing a corrective action plan to come into compliance with the waiver conditions. Georgia must also be given an opportunity to be heard and challenge the suspension or termination.

Alternatively, the Biden administration could regularly assess and monitor the state’s compliance with the terms and conditions and its progress, or lack thereof, in implementing the Georgia Access Model. Federal officials do this with all waivers. Under the waiver approval, Georgia must, for instance, satisfy requirements related to funding, reporting and evaluation, development of an outreach and communications plan, and operational standards for eligibility determinations. If Georgia fails to comply with these terms and conditions, that too would be grounds to initiate the process to amend or terminate parts or all of Georgia’s waiver.

On January 14, a few days before taking office, President Biden issued a 19-page fact sheet outlining his proposed American Rescue Plan to contain the COVID-19 virus and stabilize the economy. The announcement praised the bipartisan package adopted in December 2020 as “a step in the right direction” but notes that Congress did not go far enough to fully address the pandemic and economic fallout. Following Inauguration Day, Biden is expected to lay out an additional economic recovery plan.

Among many other initiatives, the comprehensive $1.9 trillion plan would provide funding for a national vaccination program, create a new public health jobs program, provide funding for schools to reopen safely, extend and expand emergency paid leave, extend and expand unemployment benefits, raise the minimum wage, and deliver $1,400 in support for people across the country. The Biden plan also calls for preserving and expanding health insurance, noting that 30 million people were uninsured even before the pandemic and that millions may have lost job-based coverage in 2020.

First, the American Rescue Plan calls for Congress to provide COBRA subsidies through the end of September. Presumably, these subsidies would be available from the beginning of 2021, rather than subsidizing premiums from 2020. COBRA subsidies during an economic emergency are not new. Congress subsidized COBRA premiums during the 2008 recession, with mixed results. Full COBRA subsidies were included in the original Heroes Act passed by the U.S. House of Representatives in May 2020, although not in the revised Heroes Act that was passed by the House in October 2020. But neither bill was ever taken up by the U.S. Senate. It is not clear from the fact sheet whether the Biden administration is aiming for full COBRA subsidies where the government would pay 100 percent of the premiums for COBRA coverage for laid-off workers and furloughed employees—or some other amount (e.g., 80 percent of premiums).

Second, the American Rescue Plan would accomplish one of candidate Biden’s key campaign promises by expanding and increasing the value of premium tax credits under the ACA. Democrats in Congress have repeatedly passed legislation that would accomplish what the American Rescue Plan fact sheet seems to call for. For instance, the Patient Protection and Affordable Care Enhancement Act—passed by the House in July 2020—would have expanded the availability of premium tax credits to those whose income is above 400 percent of the federal poverty level and made those credits more generous by reducing the level of income that an individual must contribute towards their health insurance premiums to 8.5 percent for those with the highest incomes. This subsidy expansion and enhancement would improve the affordability of coverage for millions of Americans who purchase coverage in the individual market.

Beyond COBRA and ACA subsidies, the American Rescue Plan calls for additional funding for veterans’ health care needs and for the Substance Abuse and Mental Health Services Administration and the Health Resources and Services Administration to expand access to behavioral health services. The proposal would also increase the federal Medicaid assistance percentage (FMAP) to 100 percent for the administration of COVID-19 vaccines to help ensure that all Medicaid enrollees will be vaccinated. The proposal does not appear to otherwise mention Medicaid, which is serving as a key safety net as incomes have dropped for millions of Americans, despite bipartisan support for an enhanced FMAP during the pandemic.