Quote of the Day: Yogi Berra on Inflation

https://www.axios.com/2024/05/03/jobs-report-april-us-economy

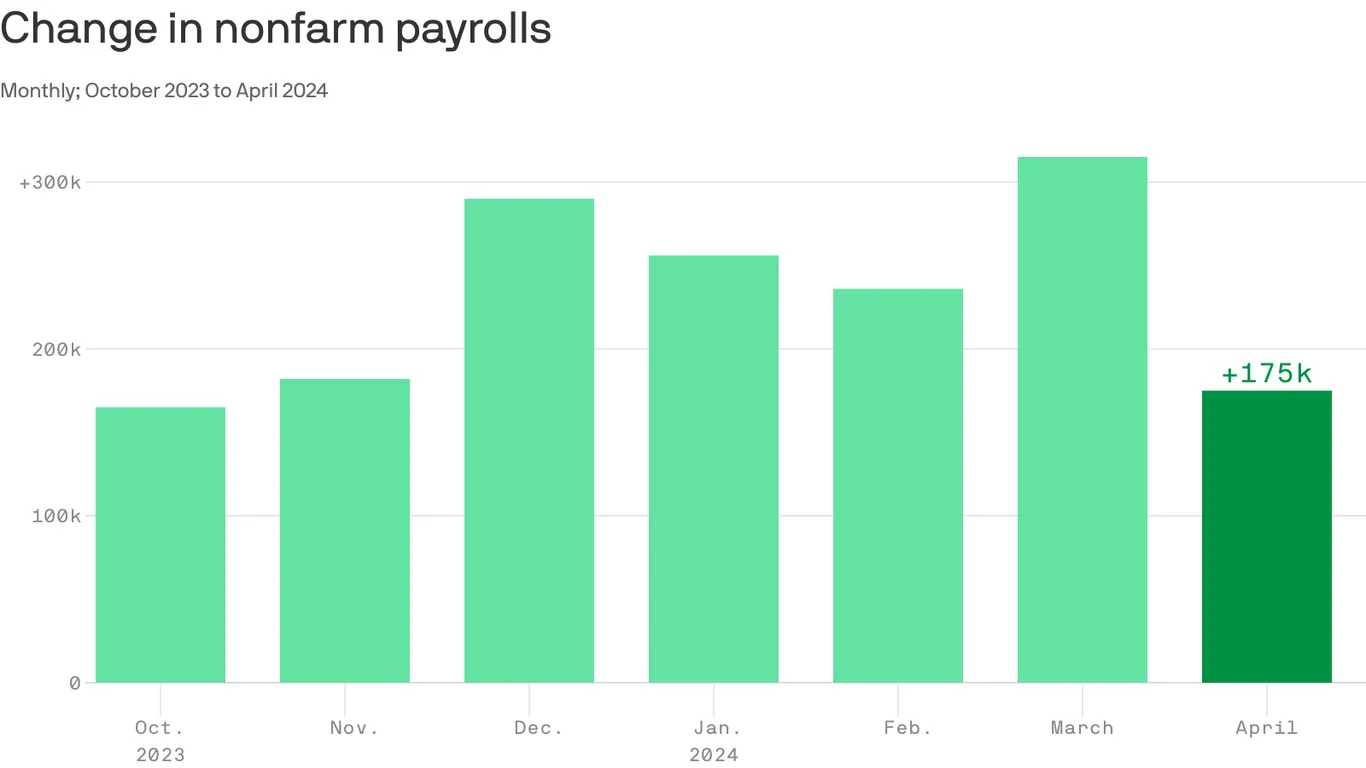

The U.S. economy added 175,000 jobs in April, while the unemployment rate ticked up to 3.9% from 3.8%, the Labor Department said on Friday.

Why it matters:

Jobs growth slowed from the prior month’s hot pace, but the data suggests that the labor market is still chugging along with healthy demand for workers.

Driving the news:

The lower-than-expected job gains were concentrated in health care, social assistance, transportation and warehousing

State of play:

Friday’s data is the latest evidence that the labor market is holding steady — an important development for the broader economy.

https://www.healthcaredive.com/news/health-insurer-medicare-advantage-utilization-2024/707360

The big question coming out of the health insurance earnings season is how much elevated utilization among seniors is carrying over into 2024.

Medicare Advantage medical costs dominated fourth-quarter discussions between health insurers and investors, after higher healthcare utilization popped up like weeds in some segments of each payers’ business.

Yet health insurers’ forecasts for how higher utilization will affect their performance in 2024 are night and day.

Some payers controlled medical costs more effectively than analysts expected, said rising spending shouldn’t affect their outlooks for this year or guided to a stronger 2024 than previously forecast. That group includes UnitedHealth, Centene, Elevance and Cigna.

However, Humana and CVS cut their 2024 earnings outlooks on the heels of last year’s results, and said they expect elevated medical costs to continue this year.

Humana’s outlook is especially grim: The Kentucky-based payer’s earnings expectations for 2024 came in about half as low as analysts had expected.

Even payers that emerged from 2023 with their financial outlooks unscathed said they plan to cut benefits or raise premiums this year. The plan redesigns are to protect margins in MA — a business that historically generates significant profits, but is facing challenges that threaten to kill the golden goose.

MA plans have skyrocketed in popularity. More than half of Medicare seniors are currently signed up for the plans, attracted by benefits like lower monthly premiums and dental and vision coverage. An onslaught of marketing by insurers didn’t hurt, either, as payers jockey for members. Competition is fierce, as MA margins per enrollee can be twice as high as those in other types of plans.

Yet, more members are creating more problems for some insurers because of rising medical utilization. Starting in the second quarter last year, seniors sought out medical care they had delayed during the COVID-19 pandemic, hiking insurers’ spending.

For example, CVS added 800,000 MA enrollees for 2024, mostly nabbed from other payers after CVS aggressively expanded its benefits. But that’s coming back to haunt the Rhode Island-based insurer, which cut its earnings per share outlook for this year due to high medical costs.

There are a few potential explanations for what’s driving the elevated utilization, and why insurers might not have properly forecast the uptick in trend, according to J.P. Morgan analyst Lisa Gill.

Enrollees in MA tend to be healthier than those in traditional Medicare. But as more seniors join MA, the program’s risk population could be skewing sicker, Gill wrote in an early February research note. Insurers could have missed early warning signs of higher acuity as seniors avoided doctor’s offices during the pandemic.

Higher demand could have also existed earlier, but providers might not have been able to address it because of labor shortages that have now ameliorated, Gill said. Similarly, insurers could have added new MA enrollees with less diagnosis history relative to the rest of their population, resulting in lower visibility into their conditions.

Medical loss ratio is a useful metric for understanding how unexpectedly high utilization is affecting insurers.

Medical loss ratio, or MLR, is a percentage of how much in healthcare premiums insurers spend on clinical services and quality improvement. The higher the MLR, the less in premiums insurers are spending on administration or marketing — or retaining as profit. As such, insurers generally try to keep their MLRs low (though within regulatory bounds to avoid sanctions).

MLRs soared in payers’ Medicare businesses in the fourth quarter, as the utilization trends that emerged earlier in 2023 conflated with a typical seasonal rise in medical spending during the winter months.

Insurers chalked the increase in medical costs up to different drivers.

Seniors covered by UnitedHealth and Humana, which together hold almost half of the total MA market share, continued to seek outpatient care in droves in the fourth quarter, including procedures like orthopedic surgeries.

UnitedHealth’s members required more spending on seasonal diseases like the flu, COVID or respiratory virus RSV. Elevance, Centene and CVS also reported elevated outpatient care overall for things like elective procedures, along with higher spend on seasonal needs.

That wasn’t the case for Cigna — which had lower than expected spending on seasonal diseases — and Humana. Humana’s uptick in care was “not respiratory driven,” said CFO Susan Diamond on the payer’s fourth-quarter earnings call in January.

“We don’t have any clear indicators that it is something you can reasonably assume is seasonal,” Diamond said.

As for inpatient care, Centene and CVS didn’t report higher utilization of hospital services than expected. Elevance also didn’t say that inpatient trends were contributing to growing costs.

Yet, UnitedHealth and Humana warned investors about rising inpatient costs, which is concerning for insurers given hospital care is more expensive to cover. UnitedHealth blamed pricey COVID admissions, while Humana said it was seeing more short stays in hospitals across the board.

Humana’s Diamond said recent government regulations requiring MA payers to comply with coverage determinations in traditional Medicare could be a potential driver of the higher inpatient spend. The rule requires insurers to cover an inpatient admission if the patient is expected to require hospital care for at least two midnights.

Other insurers said they had planned for the so-called “two-midnight rule.”

On Feb. 6, Centene CFO Drew Asher told investors that the payer had factored the rule into its planning for 2024. Meanwhile, CVS CFO Tom Cowhey said one day later the company had adjusted internally in response to the rule.

The increase in utilization — combined with weaker payment rates, changes to MA quality ratings and a shifting risk adjustment model — have created an updraft for MLRs, especially for insurers with high exposure to MA like Humana and UnitedHealth.

The big question is how much of this utilization will carry over into this year, and whether payers have properly accounted for utilization changes in their plan designs.

Every major insurer besides Elevance expects to record a higher MLR in 2024 than in 2023. Though, the size of the growth ranges from a 0.8 percentage point increase for UnitedHealth to a 2.7 percentage point increase for Humana.

The outlier, Elevance, expects its MLR to remain flat.

In response to the challenging financial environment, payers — even those that excelled in controlling medical costs last year — said they’ve been pulling back benefits, raising premiums or exiting underperforming markets to boost profitability.

That’s true for insurers that expect their MA membership to grow this year (UnitedHealth, CVS), and those that expect it to fall (Cigna) or stay flat (Elevance).

As a result, further growth could be curtailed as payers prioritize margins.

“We are first and foremost focused on recovering margin, and market share gains is a secondary consideration,” Brian Kane, who leads CVS’ health benefits division, told investors during its February earnings call.

“I look at next year as a year that I think the whole industry will possibly reprice. I don’t know how the industry can take this kind of increase in utilization along with regulatory changes that will continue to persist in 2025 and 2026,” Humana CEO Bruce Broussard said on the payer’s earnings call.

Insurers said they could revise plans further in light of MA rates for 2025 that the government proposed midway through the earnings reporting season. The rates represent a renewed effort by regulators to rein in growing spending in Medicare.

Executives with Humana, Centene and CVS all said the payment changes are insufficient to cover cost trends. Humana and Centene said the rule would result in a 1.6% and 1.3% drop in rates, respectively. (That’s before risk scoring, which should result in an overall increase in reimbursement in 2025).

Insurers warned regulators that seniors could see their benefits reduced if they finalize the rates as proposed.

“We’ll just adjust the bids accordingly,” Asher said on Centene’s call. “The products may be a little less attractive for seniors from an industry standpoint if we don’t make a lot of progress on the final rates.”

Runaway inpatient spending in particular caused CVS’ insurance costs to snowball after returning “to patterns we have not seen since the start of the pandemic,” its CFO said.

CVS brought in revenue of $88.4 billion in the quarter, up 4% year over year but significantly below analysts’ expectations. Net income was slashed by almost half compared to the prior-year quarter, to $1.1 billion.

The quarter was “burdened by utilization pressures in Medicare Advantage,” CEO Karen Lynch said on the call.

Starting last year, MA seniors began using higher levels of medical services after a long dry spell during the COVID-19 pandemic. The trend has continued into this year, leaving private insurers that manage the plans scrambling to contain costs.

CVS assumed utilization would moderate somewhat coming into the first quarter, but instead it was “notably above” expectations, according to Lynch.

Outpatient services, like mental health and medical pharmacy, along with supplemental benefits like dental continued to be elevated in the first quarter. However, inpatient utilization was particularly to blame for runaway spending.

Inpatient admissions per thousand in the quarter were up “high-single digits” compared to the same time last year, Cowhey said. A small portion of the growth was expected due to implementation of the CMS’ two-midnight rule that’s resulted in insurers having to cover more inpatient admissions. But overall, admissions “meaningfully exceeded” expectations for the quarter, according to the CFO.

“Inpatient seasonality returned to patterns we have not seen since the start of the pandemic,” Cowhey said.

Executives stressed that some of those costs appear to be seasonal and shouldn’t carry into the rest of the year. Inpatient utilization patterns are similar to what CVS’ insurance arm Aetna saw in normal years before the COVID-19 pandemic, and appear to be moderating in April, according to Lynch.

Still, the higher utilization caused the insurer’s medical loss ratio — a marker of spending on patient care — to soar to 90.4% in the first quarter, compared to 84.6% during the same time last year.

Overall, medical costs in the quarter were about $900 million higher than CVS expected, Cowhey said.

CVS’ results suggest the insurer “severely underestimated utilization of new members,” TD Cowen analyst Charles Rhyee wrote in a Wednesday morning note. “Investors already had lowered expectations for MA, but actual results and impact to guidance is likely way worse than expected.”

CVS added more MA members coming into 2024 than any other U.S. health insurer, according to an analysis by consultancy Chartis. That growth caused CVS’ membership to grow 1.1 million members in the first quarter compared to the end of 2023, to 26.8 million individuals.

Revenue in CVS’ health benefits segment, which houses its insurer Aetna, subsequently inflated to $32.2 billion, up 21% compared to the fourth quarter of 2023.

Despite the boom, higher medical costs slashed the segment’s operating income, as did the impact of lower quality ratings in MA.

Lower quality or “star” ratings for 2024 cut steeply into CVS’ reimbursement. Aetna’s largest contract fell from 4.5 stars to 3.5 stars for 2024, causing the payer to lose out on about $800 million in revenue.

As a result of the pressures, “we think [MA] will lose a significant amount of money this year,” Cowhey said.

Following the quarter, CVS lowered its full-year financial expectations for earnings per share on a GAAP and adjusted basis, and for cash flow from operations.

CVS expects to notch an MLR of 89.8% in 2024, up 2.1 percentage points from its previous guidance, because of continued medical utilization pressures, Cowhey said.

Moving into 2025, CVS does expect to recover most of what it lost this year from the star ratings changes. But the insurer faces another setback: MA payment rates recently finalized for 2025 that insurers are slamming as a cut, despite only a modest decrease in base rates.

On the call, Lynch maligned the rates as “insufficient” and a “significant added disruption” in the program.

Like its other peers with major MA footprints, CVS plans to focus on improving profits at the potential expense of members. That includes hiking premiums and exiting counties where Aetna thinks it can’t improve profits in the near term. Aetna could lose members as a result, but the size of eventual losses will in large part depend on what the insurer’s competitors do, according to CVS executives.

Other major MA payers have said they will take similar steps to hike profits.

CVS also dealt with lower visibility into its claims in the quarter because of the massive cyberattack on claims clearinghouse Change Healthcare earlier this year. Change took its systems offline as a result, hamstringing providers’ payments across the U.S. and making it harder for insurers to predict how much they might have to spend on their members’ medical costs.

CVS established a reserve of nearly $500 million for claims it estimates were lodged in the quarter but it has yet to receive. Cowhey said the insurer is “confident” about the adequacy of its reserves.

In the rapidly evolving landscape of U.S. healthcare, the tug-of-war between payers and providers is continually intensifying, raising the stakes on the strategic maneuvers that shape the industry’s financial and operational dynamics.

The crux of the issue lies in the increasingly sophisticated strategies employed by insurance companies to deny claims: a move that ostensibly aims to safeguard their bottom lines, often at the expense of provider sustainability and patient access.

The rise in denial rates is more than a mere statistic; it’s a symptom of a broader systemic challenge that calls for strategic foresight and robust expertise. In this intricate environment, providers face numerous administrative challenges, working to balance clinical decisions with financial sustainability.

Drawn from in-depth proprietary analytics, clinical regulatory expertise and decades of experience, CorroHealth addresses what is needed to successfully combat payer denial tactics. Broader industry trends, such as the shift towards value-based care and the increasing emphasis on patient-centric models, will continue to disrupt the historic provider business model. CorroHealth’s insights offer a beacon for steering through these turbulent waters. Their strategic recommendations, from optimizing contract negotiations to leveraging data analytics to managing payer denials, to formalizing escalation paths, reflect a comprehensive approach to mitigating the adverse effects of ever-shifting payer denial tactics.

Delving deeper into the anatomy of payer denials reveals a long-term pattern of deliberate complexity designed to wear down provider resilience. By dissecting the layers of denial management, from initial claim submission to final resolution, CorroHealth uncovers pivotal areas where targeted interventions dramatically shift outcomes in favor of healthcare providers.

This process involves a granular analysis of denial codes, predictive analytics to pre-empt possible denials and rigorous training staff to maneuver through the intricate appeals process effectively.

Taking a proactive stance towards payer contract management, their approach emphasizes the importance of scrutinizing the fine print and negotiating terms that anticipate and mitigate denial strategies. CorroHealth advocates on the providers’ behalf for clearer definitions of medical necessity, timely filing limits and transparent appeal processes. By equipping providers with negotiation tactics grounded in comprehensive data analysis and a deep understanding of payer methodologies, their contracts become a tool for protection against denials, rather than a source of vulnerability.

Woven throughout this work is CorroHealth’s commitment to advancing the dialogue between payers and providers toward a more equitable healthcare system. Through forums, partnerships and collaborative initiatives, CorroHealth bridges the gap between these two entities, fostering an environment where mutual understanding and respect pave the way for innovative solutions to longstanding challenges.

Hospitals and health systems require an experienced partner to navigate the complexities of the healthcare landscape, balancing financial sustainability with top-tier patient care. CorroHealth offers a comprehensive suite of solutions to address challenges associated with payer denials, enabling providers to recover lost revenues and uphold the fundamental goal of accessible, high-quality patient care. Beyond financial strategies and operational adjustments, the narrative calls for a more productive and transparent dialogue between payers and providers. This aims to encourage an ecosystem where financial sustainability and high-quality patient care are complementary facets of holistic healthcare delivery.

Facing these challenges, the importance of strategic partnerships becomes increasingly vital for healthcare providers. Such alliances are indispensable in maneuvering through the complex healthcare landscape and are strengthened by CorroHealth’s comprehensive understanding of the payer-provider dynamic and dedication to fostering innovation. A collaborative approach is essential for progressing towards a healthcare system characterized by greater equity and efficiency.

The industry stands at an existential crossroads. The insights and strategies shared by CorroHealth serve as a testament to the company’s expertise and its dedication to shaping a future where healthcare is accessible, affordable and effective for all.

Walgreens’ decision to slash VillageMD’s clinical footprint has reverberated to the financial accounts of the primary care chain’s minority owner — Cigna.

Overall, Cigna’s first-quarter performance was solid, especially amid the mixed results of its insurer peers, analysts said. The Connecticut-based payer grew its revenue 23% year over year to $57.3 billion.

Yet Cigna’s bet on VillageMD is a new thorn in its side, as the investment’s value becomes increasingly bogged down by Walgreens’ operational decisions, along with broader challenges in the primary care sector.

Walgreens began closing underperforming VillageMD centers last year in a bid to force the segment to profitability, and quickly blew past its initial goal of 60 closures. Now, the retailer expects to close 160 clinics overall, majorly downsizing VillageMD’s footprint.

That decision is reverberating to the financial accounts of VillageMD’s minority owner — Cigna.

“The writedown was largely driven by some broader market dislocation that is hitting the space … as well as Village determining that they are going to pull in supply lines and constrain some of the growth in some of the new clinics that they were establishing,” CEO David Cordani told investors on a Thursday morning call.

However Cigna’s priorities for VillageMD remain unchanged, management said. Cigna is still aiming to link VillageMD’s primary care centers to its own clinical assets to build a high-quality provider network that can serve its own patients, and those of health plan and employer clients.

The partnership has already launched in four markets, and the companies plan to continue scaling, according to Cordani.

“At the macro level our strategic direction in terms of what we are seeking to innovate with Village has not changed despite the writedown of the asset,” Cordani said, though “no one likes a writedown of the asset.”

In the quarter, Cigna’s health benefits segment emerged unscathed by headwinds that buffeted other major payers: notably, spending and regulatory pressure in Medicare Advantage.

Seniors in the privately-run Medicare plans began returning for medical care in droves starting last year, sending insurer spending soaring. Meanwhile, the government is tamping down on reimbursement growth.

Yet the majority of Cigna’s business is with employer clients, which served as a “well-underwritten shelter from the MA storms,” TD Cowen analyst Gary Taylor wrote in a Thursday morning note.

Cigna is planning on getting out of Medicare coverage altogether, having agreed in January to sell its Medicare business to Chicago-based insurer Health Care Service Corporation. That deal remains on track, executives said, after a key waiting period for antitrust regulators to challenge the deal came and went in mid-April. The divestiture is expected to close in early 2025.

Cigna’s medical loss ratio — a marker of how much in premiums insurers spend on patient care — was 79.9% in the quarter, better than analysts had expected. Cigna did see higher utilization in areas like inpatient care for employer-sponsored members in the quarter, but the payer’s pricing decisions for its plans covered the trend, executives said.

Cigna cut its MLR guidance for 2024, along with raising earnings expectations. The insurer now expects an MLR between 81.7% and 82.5% this year, suggesting management is confident in their ability to control medical costs, J.P. Morgan analyst Lisa Gill wrote in a Thursday note.

Meanwhile, Evernorth’s revenue increased by more than a third year over year in the first quarter thanks to the migration of Centene’s lucrative prescription drug contract.

CVS, which previously held the contract, cited its loss as a factor in declining revenue and income for its pharmacy benefit management business on Wednesday.

Cordani specifically called out specialty pharmacy — which already represents a major portion of Evernorth’s revenue — as an “accelerated growth opportunity” for the business.

Roughly a week ago, Evernorth announced it will have an interchangeable Humira biosimilar for $0 out-of-pocket cost for eligible patients of its specialty pharmacy arm, Accredo.

Currently, 100,000 Accredo patients use Humira or a biosimilar for the frequently prescribed immune disease drug, which has long been the top-selling drug for its manufacturer AbbVie. In addition, all of its PBM clients and patients will have access to the biosimilars, according to Cordani.

Evernorth has also taken steps to ramp up coverage of GLP-1s, expensive diabetes drugs that have soared in popularity for weight loss. In March, the company announced cost-sharing agreement for GLP-1s covered in a condition management program, to insulate health plan and employer clients from the soaring costs of the medication.

The program has seen “strong interest,” and Evernorth has enrolled more than 1 million people in it to date, Cordani said.

Since 2022, S&P Global Ratings has tracked an increase in violations of debt agreements as macro economic pressures and low operating margins challenge providers.

Financial covenant violations among nonprofits began to increase at the onset of the COVID-19 pandemic.

In the early stages of the pandemic, violations were often tied to one-time pressures on operating income, such as mandatory stoppages of services.

However, violations have since evolved and now reflect nonprofits’ struggles with ongoing labor shortages and inflationary pressures, according to the report.

Although some nonprofits have recovered financially after notching worst-ever operating performances in 2022, high expenses and labor challenges continue to plague hospitals, including a “labordemic” of both clinical and nonclinical staff that could persist through 2024 and beyond.

Providers in the speculative rating category were more likely to have violated financial covenants over the past two years and accounted for 60% of violations in S&P’s rated universe.