Thought of the Day: On Effective Leadership

https://wendellpotter.substack.com/p/company-behind-namath-ads-has-long

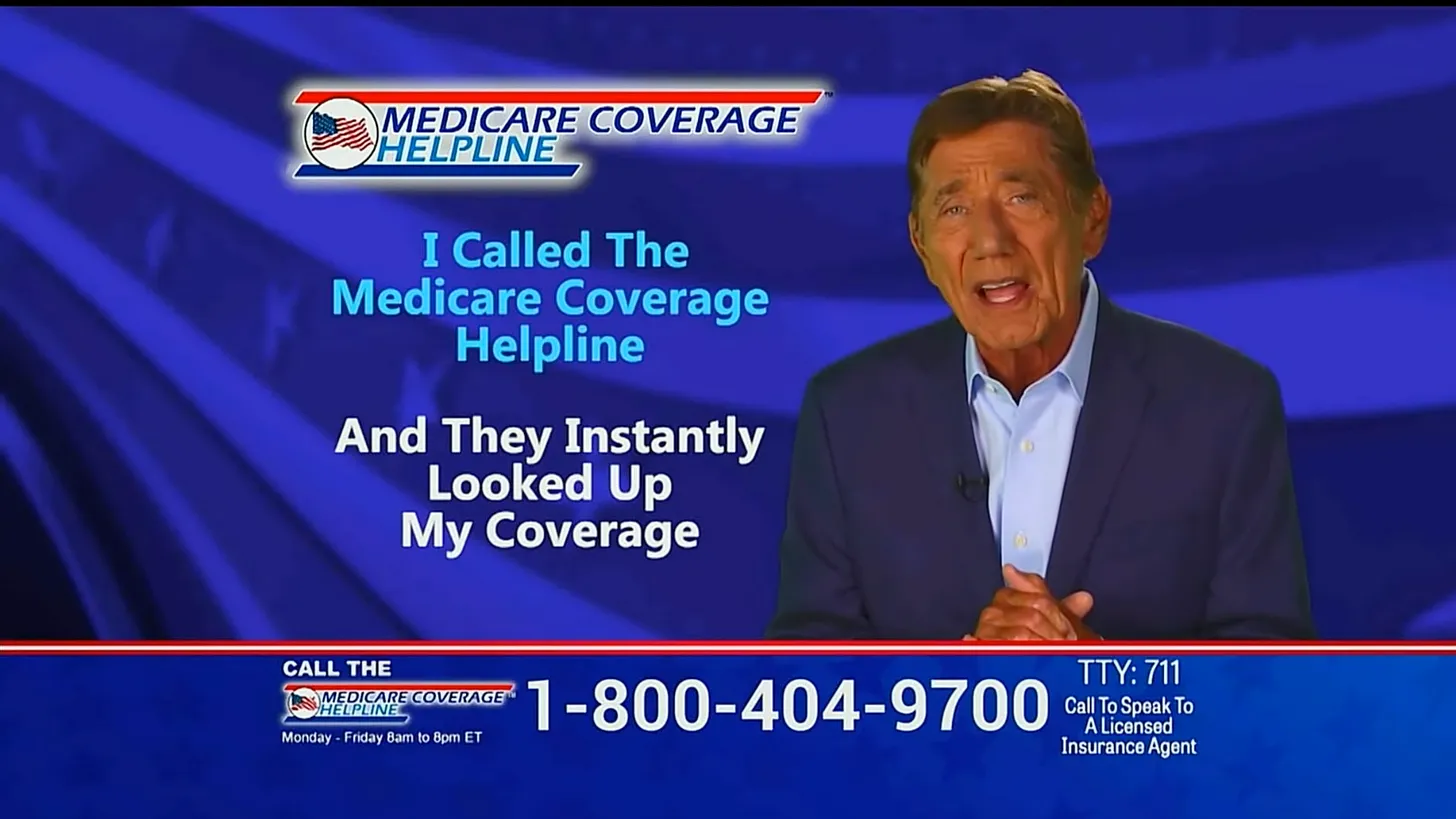

Former New York Jets superstar Joe Namath can be seen every year during Medicare open enrollment hocking plans that tell seniors how great their life would be if only they signed up for a Medicare Advantage plan. From October 15 to December 7 last year alone, Joe Namath ads ran 3,670 times, according to iSpot, which tracks TV advertising.

But the company behind those ads, now called Blue Lantern Health, and their products, HealthInsurance.com and the Medicare Coverage Helpline, have an expansive rap sheet of misconduct, including prosecutions by the Securities and Exchange Commission and the Federal Trade Commission, and a recent bankruptcy filing that critics say is designed to jettison the substantial legal liabilities the firm has incurred. In September 2023, the company became Blue Lantern; before that, it was called Benefytt; and before that, Health Insurance Innovations. Forty-three state attorneys general had settled with the company in 2018, with it paying a $3.4 million fine. A close associate of the company, Steven Dorfman, has also been prosecuted by the FTC, in addition to the Department of Justice.

Namath himself has a bit of a checkered past when it comes to his business associates—in the early 1970s, he co-owned a bar frequented by members of the Colombo and Lucchese crime families, according to reporting at the time cited in a 2004 biography. Due to the controversy surrounding the bar, Namath was forced by the NFL Commissioner to sell his interest in it. Last year, it was revealed that Namath had employed a prolific pedophile coach at his football camp, also in the 1970s, and the 80-year-old ex-quarterback is now being sued by one of the coach’s victims.

The Namath ads are the main illustration of the behemoth Medicare Advantage marketing industry, which is designed to herd seniors into Medicare Advantage plans that restrict the doctors and hospitals that seniors can go to and the procedures they can access through the onerous “prior authorization” process, and it costs the federal government as much as $140 billion annually compared to traditional Medicare. Over half of seniors—nearly 31 million people—are now in Medicare Advantage, and there is little understanding of the drawbacks of the program. Seniors are aware that they may receive modest gym or food benefits but typically do not realize that they may be giving up their doctors, their specialists, their outpatient clinics, and their hospitals in favor of an in-network alternative that may be lower quality and farther away.

How so many seniors are lured into Medicare Advantage

Blue Lantern—with its powerful private equity owner Madison Dearborn—may be the key to understanding how so many people have been ushered into Medicare Advantage—and the pitfalls that private equity’s rapid entrance into health care can create for ordinary Americans.

While Blue Lantern is just one company, it is a Rosetta Stone for everything that is wrong with American health care today—fraud, profiteering, lawbreaking, no regard for patient care—where only the public comes out the loser.

Blue Lantern uses TV ads and, at least until regulators began poking around, a widespread telemarketing operation, being one of the main firms charged with generating “leads” that are then sold to brokers and insurers, as Medicare Advantage plans are banned from cold-calling. Court filings reviewed by HEALTH CARE Un-Covered allege that after legal discovery, Blue Lantern (then known as Benefytt) at minimum dialed seniors over 17 million times, potentially in violation of federal law that requires telemarketers to properly identify themselves and who they are working for—ultimately, in this case, insurers that generate huge profits from Medicare Advantage.

The Namath ads have been running since 2018 when the company was named Health Insurance Innovations—the same year the FTC began prosecuting Simple Health Plans, along with its then-CEO Steven Dorfman. The Fort Lauderdale Sun-Sentinel identified Health Insurance Innovations as a “successor” to Simple Health Plans. After five years of likely exceptionally costly litigation, for which Dorfman is represented by jet-set law firm DLA Piper, on February 9, the FTC won a $195 million judgment against Simple Health Plans and Dorfman. The FTC alleged in 2019 that Dorfman had lied to the court when he said that he did not control any offshore accounts. The FTC found $20 million, but the real number is probably higher.

Friends in high places

In February 2020, Trump’s Secretary of Health and Human Services, Alex Azar, said that the Namath ads might not “look or sound like the future of health care,” but that they represented “real savings, real options” for older Americans.

In March 2020, Health Insurance Innovations (HII) changed its name to Benefytt, and in August 2020, it was acquired by Madison Dearborn Partners. Madison Dearborn has close ties to the Illinois Democratic elite, pumping over $916,000 into U.S. Ambassador to Japan Rahm Emanuel’s campaigns for Congress and mayor of Chicago.

In September 2021, HII settled a $27.5 million class action lawsuit. The 230,000 victims received an average payout of just $80.

In July 2022, the SEC charged HII/Benefytt and its then-CEO Gavin Southwell with making fraudulent representations to investors about the quality of the health plans it was marketing. “HII and Southwell…told investors in earnings calls and investor presentations that HII’s consumer satisfaction was 99.99 percent and state insurance regulators received very few consumer complaints regarding HII. In reality, HII tracked tens of thousands of dissatisfied consumers who complained that HII’s distributors made misrepresentations to sell the health insurance products, charged consumers for products they did not authorize and failed to cancel plans upon consumers’ requests,” the SEC found, with HII/Benefytt and Southwell ultimately paying a $12 million settlement in November 2022.

By August 2022, Benefytt had paid $100 million to settle allegations that it had fraudulently directed people into “sham” health care plans. “Benefytt pocketed millions selling sham insurance to seniors and other consumers looking for health coverage,” the FTC’s Director of Consumer Protection, Samuel Levine, said at the time.

Bankruptcy and another name change

In May 2023, Benefytt declared Chapter 11 bankruptcy—where the company seeks to continue to exist as a going concern, as opposed to Chapter 9, when the company is stripped apart for creditors—in the Southern District of Texas. The plan of bankruptcy was approved in August. The Southern Texas Bankruptcy Court has been mired in controversy in recent months as one of the two judges was revealed to be in a romantic relationship with a woman employed by a firm, Jackson Walker, that worked in concert with the major Chicago law firm Kirkland and Ellis to move bankruptcy cases to Southern Texas and monopolize them under a friendly court. While the other judge on the two-judge panel handled the Benefytt case, Jackson Walker and Kirkland and Ellis were retained by Benefytt, and the fees paid to Jackson Walker by Benefytt were delayed by the court as a result of the controversy.

In September 2023, Benefytt exited bankruptcy and became Blue Lantern.

The August approval of the bankruptcy plan was vocally opposed by a group of creditors who had sued Benefytt over violations of the Telephone Consumer Privacy Act (TCPA). The creditors asserted that Benefytt had substantial liabilities, with millions of calls made where Benefytt did not identify the ultimate seller—Medicare Advantage plans run by UnitedHealth, Humana, and other firms prohibited from directly contacting people they have no relationship with—and violations fined at $1,500 per willful violation.

Attorneys for those creditors stated in a filing reviewed by HEALTH CARE Un-Covered that Madison Dearborn always planned “to steer Benefytt into bankruptcy,” if they were unable to resolve the substantial liabilities they owed under the TCPA.

Madison Dearborn “knew that Benefytt’s TCPA liabilities exceeded its value, but purchased Benefytt anyway, for the purpose of trying to quickly extract as much money and value as they could before those liabilities became due,”

the August 25, 2023, filing stated on behalf of Wes Newman, Mary Bilek, George Moore, and Robert Hossfeld, all plaintiffs in proposed TCPA class action suits. The filing went on to say that the bankruptcy was inevitable “if—after siphoning off any benefit from the illegal telemarketing alleged herein—[Madison Dearborn] could not obtain favorable settlements or dismissals for the telemarketing-related lawsuits against Benefytt.”

Under the bankruptcy plan, Blue Lantern/Benefytt is released from the TCPA claims, but individuals harmed can affirmatively opt-out of the release, which is why the bankruptcy court justified its approval. Over 7 million people—the total numbers in Benefytt’s database, according to the plaintiffs—opting out of the third-party release is an enormous administrative hurdle for plaintiffs’ lawyers to pass, massively limiting the likelihood of success of any class-action litigation against Blue Lantern going forward.

Their attorney, Alex Burke, stated in court that “[t]his bankruptcy is an intentional and preplanned continuation of a fraud.” His statement was before 3,670 more Namath ads ran during 2023 open enrollment.

In response to requests for comment from HEALTH CARE un-covered, the Centers for Medicare and Medicaid Services did not answer questions about Benefytt and why the company was simply not barred from the Medicare Advantage market altogether.

Corporations have used the bankruptcy process in recent years to free themselves from criminal and civil liability, with opioid marketer Purdue Pharma being the most prominent recent example. The Supreme Court is reviewing the legality of Purdue’s third-party releases currently, with a decision expected in late spring.

The role that private equity plays in keeping Benefytt going cannot be overstated.

Without Madison Dearborn or another private equity firm eager to take on such a risky business with such a long history of legal imbroglios, it is almost certain that Benefytt would no longer exist—and the Joe Namath ads would disappear from our televisions. Instead, Madison Dearborn keeps them going, suckering seniors into Medicare Advantage plans.

This is part and parcel of the ongoing colonization by private equity into America’s health care system. Private equity is making a major play into Medicare Advantage.

It has pumped billions of dollars into purchasing hospitals. It has invested in hospice care. It is gobbling up doctors’ groups. It is acquiring ambulance companies. It is hoovering up nurse staffing firms. It is making huge investments into health tech. It is in nursing homes. And it is in health insurance. Nothing about America’s health care system is untouched by private equity.

That’s a problem, experts say.

“I’ve been screaming at the TV every time Joe Namath gets on—it is not an official Medicare website,” said Laura Katz Olson, a professor of political science at Lehigh University who has written on private equity’s role in the health care system.

“Private equity has so much money to deploy, which is far more than they have opportunities to buy. As such, they are desperately looking for opportunities to invest. There’s a lot of money in Medicare Advantage—it’s guaranteed money from the federal government, which makes it perfect for the private equity playbook.”

Eileen Appelbaum, the co-director at the Center for Economic and Policy Research, who has also studied private equity’s role in health care, concurred that private equity was a perfect fit for Medicare marketing organizations.

“I think basically the whole privatized Medicare situation is ready for all kinds of exploitation and misrepresentations and denying people the coverage that they need,” she said. “My email is inundated with these totally misleading ads. Private equity took a look at this and said, “look at that, it’s possible to do something that’s misleading and make a lot of money.”

Madison Dearborn receives a large portion of its capital from public pension funds like the California Public Employees Retirement System (CalPERS) and the Washington State Investment Fund—people who are dependent on Medicare. Appelbaum said that the pension funds exercise little oversight over their investments in private equity. “Pension funds may have the name of the company that they are invested in, they’re told that it’s ‘part of our health care investment portfolio,’ but they don’t find out what they really do until there’s a scandal.

It is amazing that pension funds give so much money to private equity with so little information about how their money is being spent.”

It’s no secret I feel strongly that “Medicare Advantage for All” is not a healthy end goal for universal health care coverage in our country. But I also recognize there are many folks, across the political spectrum, who see the program as one that has some merit. And it’s not going away anytime soon. To say the insurance industry has clout in Washington is an understatement.

As politicians in both parties increase their scrutiny of Medicare Advantage, and the Biden administration reviews proposed reforms to the program, I think it’s important to highlight common-sense, achievable changes with broad appeal that would address the many problems with MA and begin leveling the playing field with the traditional Medicare program.

1. Align prior authorization MA standards with traditional Medicare

Since my mother entered into an MA plan more than a decade ago, I’ve watched how health insurers have applied practices from traditional employer-based plans to MA beneficiaries. For many years, insurers have made doctors submit a proposed course of treatment for a patient to the insurance company for payment pre-approval — widely known as “prior authorization.”

While most prior authorization requests are approved, and most of those denied are approved if they are appealed, prior authorization accomplishes two things that increase insurers’ margins.

The practice adds a hurdle between diagnosis and treatment and increases the likelihood that a patient or doctor won’t follow through, which decreases the odds that the insurer will ultimately have to pay a claim. In addition, prior authorization increases the length of time insurers can hold on to premium dollars, which they invest to drive higher earnings. (A considerable percentage of insurers’ profits come from the investments they make using the premiums you pay.)

Last year, the Kaiser Family Foundation found the level of prior authorization requests in MA plans increased significantly in recent years, which is partially the result of the share of services subject to prior authorization increasing dramatically. While most requests were ultimately approved (as they were with employer-based insurance plans), the process delayed care and kept dollars in insurers’ coffers longer.

The outrage generated by older Americans in MA plans waiting for prior authorization approvals has moved the Biden administration to action.

Beginning in 2024, MA plans may be no more restrictive with prior authorization requirements than traditional Medicare.

That’s a significant change and one for which Health and Human Services Secretary Xavier Becerra should be lauded.

But as large provider groups like the American Hospital Association have pointed out, the federal government must remain vigilant in its enforcement of this rule. As I wrote about recently with the implementation of the No Surprises Act, well-intentioned legislation and implementation rules put in place by regulators can have little real-world impact if insurers are not held accountable. It’s important to note, though, that federal regulatory agencies must be adequately staffed and resourced to be able to police the industry and address insurers’ relentless efforts to find loopholes in federal policy to maximize profits. Congress needs to provide the Department of Health and Human Services with additional funding for enforcement activities, for HHS to require transparency and reporting by insurers on their practices, and for stakeholders, especially providers and patients, to have an avenue to raise concerns with insurers’ practices as they become apparent.

2. Protect seniors from marketing scams

If it’s fall, it’s football season. And that means it’s time for former NFL quarterback Joe Namath’s annual call to action on the airwaves for MA enrollment.

As Congresswoman Jan Schakowsky and I wrote about more than a year ago, these innocent-appearing advertisements are misleading at their best and fraudulent at their worst. Thankfully, this is another area the Biden administration has also been watching over the past year.

CMS now prohibits the use of ads that do not mention a specific plan name or that use the Medicare name and logos in a misleading way, the marketing of benefits in a service area where they are not available, and the use of superlatives (e.g., “best” or “most”) in marketing when not substantiated by data from the current or prior year.

As part of its efforts to enforce the new marketing restrictions, the Center for Medicare and Medicaid Services for the first time evaluated more than 3,000 MA ads before they ran in advance of 2024 open enrollment. It rejected more than 1,000 for being misleading, confusing, or otherwise non-compliant with the new requirements. These types of reviews will, I hope, continue.

CMS has proposed a fixed payment to brokers of MA plans that, if implemented, would significantly improve the problem of steering seniors to the highest-paying plan — with the highest compensation for the insurance broker. I think we can all agree brokers should be required to direct their clients to the best product, not the one that pays the broker the most. (That has been established practice for financial advisors for many years.) CMS should see this rule through, and send MA brokers profiteering off seniors packing.

A bonus regulation in this space to consider: banning MA plan brokers from selling the contact information of MA beneficiaries. Ever wonder why grandma and grandpa get so many spam calls targeting their health conditions? This practice has a lot to do with it. And there’s bipartisan support in Congress for banning sales of beneficiary contact information.

In addition, just as drug companies have to mention the potential side effects of their medications, MA plans should also be required to be forthcoming about their restrictions, including prior authorization requirements, limited networks, and potentially high out-of-pocket costs, in their ads and marketing materials.

3. Be real about supplemental benefits

Tell me if this one sounds familiar. The federal government introduced flexibility to MA plans to offer seniors benefits beyond what they can receive in traditional Medicare funded primarily through taxpayer dollars.

Those “supplemental” benefits were intended to keep seniors active and healthy. Instead, insurers have manipulated the program to offer benefits seniors are less likely to use, so more of the dollars CMS doles out to pay for those benefits stay with payers.

Many seniors in MA plans will see options to enroll in wellness plans, access gym memberships, acquire food vouchers, pick out new sneakers, and even help pay for pet care, believe it or not — all included under their MA plan. Those benefits are paid for by a pot of “rebate” dollars that CMS passes through to plans, with the presumed goal of improving health outcomes through innovative uses.

There is a growing sense, though, that insurers have figured out how to game this system. While some of these offerings seem appealing and are certainly a focus of marketing by insurers, how heavily are they being used? How heavily do insurers communicate to seniors that they have these benefits, once seniors have signed up for them? Are insurers offering things people are actually using? Or are insurers strategically offering benefits that are rarely used?

Those answers are important because MA plans do not have to pay unused rebate dollars back to the federal government.

CMS in 2024 is requiring insurers to submit detailed data for the first time on how seniors are using these benefits. The agency should lean into this effort and ensure plan compliance with the reporting. And as this year rolls on, CMS should be prepared to make the case to Congress that we expect the data to show that plans are pocketing many of these dollars, and they are not significantly improving health outcomes of older Americans.

4. Addressing coding intensity

If you’re a regular reader, you probably know one of my core views on traditional Medicare vs. Medicare Advantage plans. Traditional Medicare has straightforward, transparent payment, while Medicare Advantage presents more avenues for insurers to arbitrarily raise what they charge the government. A good example of this is in higher coding per patient found in MA plans relative to Traditional Medicare.

An older patient goes in to see their doctor. They are diagnosed, and prescribed a course of treatment. Under Traditional Medicare, that service performed by the doctor is coded and reimbursed. The payment is generally the same no matter what conditions or health history that patient brought into the exam room. Straightforward.

MA plans, however, pay more when more codes are added to a diagnosis.

Plans have advertised this to doctors, incentivizing the providers to add every possible code to a submission for reimbursement. So, if that same patient described above has diabetes, but they’re being treated for an unrelated flu diagnosis, the doctor is incentivized by MA to add a code for diabetes treatment. MA plans, in turn, get paid more by the government based on their enrollee’s health status, as determined based on the diagnoses associated with that individual.

Extrapolate that out across tens of millions of seniors with MA plans, and it’s clear MA plans are significantly overcharging the federal government because of over-coding.

One solution I find appealing: similar to fee-for-service, create a new baseline for payments in MA plans to remove the incentive to add more codes to submissions. Proposals I’ve seen would pay providers more than traditional Medicare but without creating the plan-driven incentive for doctors to over-code.

5. Focusing in on Medicare Advantage network cuts in rural areas

Rural America is older and unhealthier than the national average. This should be the area where MA plans should experience the highest utilization.

Instead, we’re seeing that the aggressive practices insurers use to maximize profits force many rural hospitals to cancel their contracts with MA plans. As we wrote about at length in December, MA is becoming a ghost benefit for seniors living in rural communities. The reimbursement rates these plans pay hospitals in rural communities are significantly lower than traditional Medicare. That has further stressed the low margins rural hospitals face.

As Congressional focus on MA grows, I predict more bipartisan recommendations to come forth that address the growing gap between MA plan payments and what hospitals need to be paid in rural areas.

If MA is not accepted by providers in older, rural America, then truly, what purpose does it serve?

Inflation moderated as economists forecasted last month, according to the Federal Reserve’s favored inflation metric, bringing welcome news for investors, home buyers and consumers alike looking for interest rate cuts.

Americans spent 2.4% more in January than they did in January 2023, according to the personal consumption expenditures (PCE) price index released Thursday morning by the Bureau of Economic Analysis.

That meets consensus economist estimates of 2.4% annual PCE inflation and comes in lower than last month’s 2.6%.

It’s the lowest PCE reading since March 2021.

Core PCE inflation, which tracks expenditures for goods and services other than the less sticky food and services inputs, was 2.8% in January, in line with forecasts of 2.8%.

It’s similarly the lowest core PCE reading since March 2021 and checks in significantly lower than January 2023’s 4.7% inflation.

Core PCE inflation, which is Fed Chairman Jerome Powell’s inflation measure of choice, is still well above the Fed’s long-term 2% target.

Earlier this month, PCE’s sister consumer price index (CPI) revealed far worse CPI inflation than economists projected, sending the S&P 500 stock index to its biggest loss in almost 12 months as sticky inflation would likely cause the Fed to delay the much-anticipated rate cuts until more tangible progress toward 2% inflation is apparent. CPI measures the average prices nationwide of a predetermined basket of goods and services, while PCE measures how much Americans actually spend monthly, earning the latter policymakers’ affection as it arguably paints a better picture of the health of Americans’ wallets.

The series of hotter than anticipated inflation data has dramatically pushed back expectations of when and by how much the Fed will slash rates in 2024. Higher inflation typically keeps rates higher for longer, making loans such as mortgages more expensive, exemplified by mortgage rates more than doubling over the last two years to their highest levels since the turn of the century.

The futures market currently prices in June as the most likely date of the first cut and 75 basis points of cuts as the most likely outcome, according to the CME Group’s FedWatch Tool, much softer than a month ago’s implied forecasts of the first reduction coming in May and 125 basis points of cuts.

STAT News today published an op-ed I coauthored with Dr. Philip Verhoef, president of Physicians for a National Health Program, making the point that investors are among the growing number of stakeholders who are souring on big, for-profit insurance companies like the ones I used to work for (Cigna and Humana).

We focused specifically on investors’ concerns about the continued profitability of Medicare Advantage plans most of the big insurers own and operate.

Several companies have lost billions of dollars in market capitalization over the past several weeks as they have reported what they maintain is higher than usual utilization of health care goods and services by seniors enrolled in MA plans.

Today, the companies–especially UnitedHealth Group, the market leader with 7.6 million Medicare Advantage enrollees–are losing billions more in market cap on the news, broke yesterday by the Wall Street Journal, that the Department of Justice is investigating UnitedHealth’s many acquisitions over the years.

UnitedHealth and most of the other companies are no longer just insurance companies. They’ve moved rapidly into health care delivery by buying physician practices and clinics, and three of them, UnitedHealth, Cigna and CVS/Aetna, control 80% of the pharmacy benefit management business.

As Phil and I wrote in our op-ed:

Investors in MA insurance companies experienced a rude awakening in late January, with insurer stocks plummeting in the face of earnings reports showing profits falling far below expectations in the last quarter of 2023. Companies like CVS Health and UnitedHealth Group saw losses of 5.2% and 6.2% respectively, while Humana, whose business model relies heavily on the MA program, fell an astonishing 14.2%. These insurers cited higher than average health care utilization rates as the culprit and warned that 2024 would likely see more of the same. At the same time, private equity investment in MA has fallen, showing waning confidence in the program.

We went on to note that both Democrats and Republicans in Congress are increasingly concerned about MA insurers’ business practices and, among other things, have introduced bills to crack down on egregious overpayments to MA plans.

The WSJ reported yesterday that the Justice Department has launched an antitrust investigation into UnitedHealth, which has become not only the country’s biggest U.S. health insurer but also a leading manager of drug benefits “and a sprawling network of doctor groups.”

The Journal’s Anna Wilde Mathews and Dave Michaels wrote that:

The investigators have in recent weeks been interviewing healthcare-industry representatives in sectors where UnitedHealth competes, including doctor groups, according to people with knowledge of the meetings.

The DOJ’s investigation of UnitedHealth is wide-ranging. Among other things, according to the Journal, “investigators have asked whether and how the tie-up between UnitedHealthcare [the insurance division] and Optum’s medical groups might affect its compliance with federal rules that cap how much a health-insurance company retains from the premiums it collects. (Optum is the company’s division that encompasses the pharmacy benefit manager Optum Rx and the many clinics and physician practices it owns.)

HEALTH CARE un-covered explained last month how UnitedHealth essentially is paying itself billions of dollars every month and circumventing the intent of a federal law that requires insurers to spend at least 80% of premium dollars on their health plan enrollees’ health care.

I know from sources within the Justice Department that investigators saw that piece, as well as the comprehensive analysis we published earlier of the scores of acquisitions UnitedHealth has made in recent years that have enabled it to catapult to the top five of the Fortune 500 list of American companies.

Those sources told me that the DOJ is very concerned about the consolidation within both the health insurance business and the hospital industry. Many U.S. hospitals, in an ongoing effort to negotiate from an enhanced position of strength with UnitedHealth and the other vertically integrated insurers, have merged with each other in recent years and become part of huge health-care delivery systems.

At the close of trading on the New York Stock Exchange yesterday, shares of UnitedHealth Group’s share were down $11.90 or 2.27%. Investors are continuing to head for the exits today. As I write this, the company’s stock price has fallen another $20 (4%) to $494.00. That’s way down from the company’s 52-week high of $554.70.

Shares of most of the other big publicly traded insurers (Centene, Cigna, CVS/Aetna, Elevance, Humana and Molina) are also down, ranging from $.83 at CVS to $11.51 at Humana.

Ruth Gottesman’s monumental $1 billion contribution to the Albert Einstein College of Medicine marks a groundbreaking moment, ensuring free tuition for both present and future students. David Begnaud delves into the significance of this generous gift and talks to a student directly impacted by this life-changing donation.

U.S. Hospital YTD Operating Margin Index November 2021-December 2023

The observations and questions from this chart are both interesting and required reading for hospital executives:

The above questions and observations have proven interesting, and the ongoing numbers have proven quite useful in many quarters of healthcare. But recently I was talking with Erik Swanson, who is the leader of the Kaufman Hall Flash Report and our executive behind the data, numbers, and statistics. Erik and I were speculating about all of the above observations, but our key speculation was whether the 2023 operating margin results actually reflected a hospital financial turnaround or, in fact, were there “numbers behind the numbers” that told a different and much more nuanced story. So Erik and I asked different questions and took a much deeper dive into the Flash Report numbers. The results of that dive were quite telling:

The point here is that data, numbers, and statistics matter both to setting long-term social health policy agendas and to the strategic management of complex provider organizations. But the other point is that the quality and depth of the analysis is an equally important part of the process. A first glance at the numbers may suggest one set of outcomes. However, a deeper, more careful and penetrating analysis may reveal critical quantitative conclusions that are much more telling and sophisticated and can accurately guide first-class organizational decision-making. Hopefully the analytics here are a good example of this very point.

https://mailchi.mp/f9bf1e547241/gist-weekly-february-23-2024?e=d1e747d2d8

Walgreens announced this week that it will be shutting down all of its Florida-based VillageMD primary care clinics. Fourteen clinics in the Sunshine State have already closed, with the remaining 38 expected to follow by March 15.

This move comes in the wake of a $1B cost-cutting initiative announced by Walgreens executives last fall, which included plans to shutter at least 60 VillageMD clinics across five markets in 2024.

Last month VillageMD exited the Indiana market, where it was operating a dozen clinics.

Despite downsizing its primary-care footprint, Walgreens says it remains committed to its expansion into the healthcare delivery sector, having invested $5.2B in VillageMD in 2021 and purchased Summit Health-CityMD for $9B through VillageMD in 2023.

The Gist: Having made significant investments in provider assets, Walgreens now faces the difficult task of creating an integrated and sustainable healthcare delivery model, which takes time.

Unlike long-established healthcare providers who feel more loyal to serving their local communities, nontraditional healthcare providers like Walgreens can more easily pick and choose markets based on profitability.

While this move is disruptive to VillageMD patients in Florida and the other markets it’s exiting, Walgreens seems to be answering to its investors, who have been dissatisfied with its recent earnings.