After a presentation this week, a senior physician from the audience of our member health systems reached out to discuss a well-trod topic, the future of health reform legislation. But his question led to a more forward-looking concern:

“You talked very little about politics, even though we have an election coming up next year. Are you anticipating that Medicare for All will come up again? And what would the impact be on doctors?”

As we’ve discussed before, we think it’s unlikely that sweeping health reform legislation like Medicare for All (M4A) would make its way through Congress, even if Democrats sweep the 2024 elections—and it’s far too early for health systems to dedicate energy to a M4A strategy.

Healthcare is not shaping up to be a campaign priority for either party, and given the levels of partisan division and expectations that slim majorities will continue, passing significant reform would be highly unlikely.

Although there is bipartisan consensus around a limited set of issues like increasing transparency and limiting the power of PBMs, greater impact in the near term will come from regulatory, rather than legislative, action.

For instance, health systems are much more exposed by the push toward site-neutral payments. How large is the potential hit? One mid-sized regional health system we work with estimated they stand to lose nearly $80M of annual revenue if site-neutral payments are fully implemented—catastrophic to their already slim system margins.

Preparing for this inevitable payment change or the long-term possibility of M4A both require the same strategy: serious and relentless focus on cost reduction.

This still leaves a giant elephant in the room: the long-term impact on the physician enterprise.

As referral-based economics continue to erode, health systems will find it increasingly difficult to maintain current physician salaries, further driving the need to move beyond fee-for-service toward a health system economic model based on total cost of care and consumer value, while building physician compensation around those shared goals.

This week’s graphic highlights increasing tensions between health systems and Medicare Advantage (MA) plans as they battle over what providers see as unsatisfactory payment rates and insurer business practices.

On paper, many providers have negotiated rates with MA plans that are similar to traditional fee-for-service Medicare, but find MA patients are subject to more prior authorizations and denials, as well as delayed discharges to postacute care, whichincreases inpatient length of stay and hospital costs.

A number of health system leaders have reported their revenue capture for MA patients dropped to roughly 80 percent of fee-for-service Medicare rates due to an increase in the mean length of stay for MA patients, caused by carriers narrowing postacute provider networks.

As a result, a growing number of health systems and medical groups have either already exited, or plan to exit, MA networks due to what they see as insufficient reimbursement.

Health systems with a strong regional presence may be able to leverage their market share to get MA payers to play ball. But for health systems in more competitive markets, these hardline negotiation tactics run the risk of payers merely directing their patients elsewhere.

Regardless of market dynamics, providers exiting insurance plans is extremely disruptive for patients, who won’t understand the dynamics of payer-provider negotiations—but will feel frustrated when they can’t see their preferred physicians.

Published last week in the Wall Street Journal, this piece predicts that the era of immense profitability for Medicare Advantage (MA) insurers may be drawing to a close.

MA has experienced rapid growth over the past decade, due both to the pace of Baby Boomers aging into Medicare, and the increasing numbers of beneficiaries choosing MA plans. In 2023, MA surpassed 50 percent of total Medicare enrollment.

Payers readily embraced the MA market because they found they could earn gross margins two to three times higher than from a commercial life.

However, as the rate of enrollment growth begins to slow (the last of the Boomers will turn 65 in 2030), competition between payers increases, and government payments become less generous, the MA business—while still profitable—is poised to become less of a jackpot.

The Gist:While MA has been an outsized driver of profits for insurance companies in recent years,the nation’s two largest MA payers, UnitedHealth Group (UHG) and Humana, have been signaling growing concerns to the market.

UHG announced late last month that its 2024 MA enrollment growth will be less than half of its 2023 rate, and Humana has been engaged in merger talks with Cigna.

As the “gold rush” period ends, MA payers will have to earn their keep by better integrating their various care and data assets, and more carefully managing spending for an aging cohort of seniors with increasingly complex needs, both much harder than riding a demographic wave to easy profits.

Following rumors of a potential merger reported last month by the Wall Street Journal, the paper shared this week that Bloomfield, CT-based Cigna is no longer pursuing an acquisition of Louisville, KY-based Humana.

According to insiders, the $140B merger was scuttled when the two health insurance giants couldn’t agree on price and other terms.

Instead, Cigna announced that it will be focusing on smaller, bolt-on acquisitions, and is reportedly still considering divesting its Medicare Advantage business.

Cigna also announced $10B of stock buybacks to assuage shareholders, who reacted negatively to the rumored deal, dropping the company’s stock price by nearly 10 percent since merger rumors surfaced.

The Gist: While there are several reasons why this deal may have been called off—Wall Street’s adverse reaction, antitrust concerns, leaking of the talks before the parties were ready—this likely isn’t the end of either payer’s pursuit of greater scale, as both stand in UnitedHealth Group’s giant shadow.

Given Cigna and Humana have each had potential mergers with other payers blocked by the courts, and federal antitrust scrutiny is only increasing, we’re wondering if each may be also looking at nontraditional partners (as Humana explored with Walmart in 2018), though the universe of companies with an interest in a vertically-integrated insurance and care business—and deep enough pockets—is small.

The nation’s largest for-profit hospital systems by revenue — HCA Healthcare, Community Health Systems, Tenet Healthcare and Universal Health Services —reported mixed results during the third quarter of 2023, despite announcing strong demand for patient services.

With the exception of HCA, each operator reported lower profits in the third quarter compared with the same period last year. Health systems CHS and HCA reported earnings that fell short of Wall Street expectations for revenue.

Major operators posted declining profits in the third quarter compared to the same period in 2022

Q3 net income in millions, by operator

Health System

Profit

Percent Change YOY

Community Health Systems

$−91

−117%

HCA Healthcare

$1,800

59%

Tenet Healthcare

$101

−23%

Universal Health Services

$167

−9%

Admissions rose across the board compared to the same period last year: Same facility equivalent admissions rose4.1% at HCA , 3.7% at CHS and 0.6% at Tenet,and adjusted admissions at acute hospitals rose 6.8% at UHS.

Although the for-profit operators began cost containment strategies earlier this year — recognizing that rising expenses, including costs of salary and wages, were pressuring hospital profitability post-pandemic — expenses also rose, with growth in salaries and benefit costs once again pressuring most operators’ revenue.

Hospital operators faced new challenges this quarter, executives said, including increased physician staffing fees and what hospital executives characterizedas aggressive behavior from payers.

Hospitals highlight rising physician fees

Rising physician fees were a topic of concern on earnings calls this quarter, with executives reporting fees that were 15% to 40% higher compared with the same period last year.

Third-party staffing firms charge hospitals physician fees, a percentage of physicians’ salaries, on top of the salaries themselves. Physician fees are separate but related to contract labor costs, which plagued hospitals during the COVID-19 pandemic as they attempted to stem staffing shortages.

Hospitals typically contract specialty hospitalist roles — like anesthesiologists, radiologists and emergency department physicians — and incur associated staffing costs.

Physician fees at HCA, the country’s largest hospital chain, grew 20% year over year in the third quarter, according to CFO Bill Rutherford.

Physician fees were up by as much as 40% at UHS — making up 7.6% of totaloperating expenses this quarter and surpassing the company’s initial projections for the year,CEOMarc Miller said during an earnings call. Historically, physician fees accounted for about 6% of UHS’ total expenses.

Likewise, Franklin, Tennessee-based CHS attributed some of its third-quarter losses to “increased rates for outsourced medical specialists,” according to a release on the operator’s earnings.

Tenet CEO Saum Sutaria noted that physician fee expenses were up 15% year over year, but said on an earnings call that the operator had spied rising physician fees during the pandemic, and had begun efforts to contain costs — including restructuring staffing contracts and in-sourcing critical physician services.

As a result, physician fee costs at Tenet had remained “relatively flat” from the second quarter to the third quarter this year, according to the Sutaria.

Physician fee increases may be a delayed consequence of the No Surprises Act, which went into effect in January of last year, experts say.

On an earnings call, UHS CFO Steve Filton said “the industry has largely had to reset itself” in wake of the law. Tenet and CHS executives echoed the sentiment, noting that the law had disrupted staffing firms’ business models and complicated payment processes.

The No Surprises Act prevents patients who unknowingly receive out-of-network care at an in-network facility from being stuck with unexpectedbills. However, the act has had unintended ripple effects, experts say.

Staffing firms and hospitals allege that the arbitration process created to resolve disputes between providers and insurers is unbalanced and incentivizes insurers to withhold reimbursement for care. In an August survey, over half of doctors reported insurers have either ignored decisions made by arbitrators or declined to pay claims in full.

In other cases, a backlog prevents claims from being adjudicated at all. Last year, the CMS found the federal arbitration process had only reached a payment determination in 15% of cases. Federal regulators have been forced to pause and restart the arbitration process multiple times in the wake of federal court decisions challenging arbitration methodology.

Although the act went into effect more than a year ago, many hospitals are just now feeling the strain, saidLoren Adler, associate director at the Brookings Institute’s Schaeffer Initiative on Health Policy.

That’s because most insurers, hospitals and medical groups operate on three-year contracts, according to Adler. Staffing firms, which have struggled since the No Surprises Act was enacted, have passed on costs to hospitals as contracts come up for negotiation and insurers charge firms higher rates.

In the face of rising costs, some hospitals may opt to follow Tenet and CHS and in-source physicians — either to retain contracts with physicians who worked with firms that have folded or because the passing of the No Surprises Act makes outsourcing less attractive.

CHS hired 500 physicians from staffing firm American Physician Partners after the company collapsed in July. CFO Kevin Hammons said on an earnings call that hiring the physicians had saved CHS “approximately $4 million sequentially compared to the subsidy payments previously paid” to the staffing firm.

However, in-sourcing may not be an effective cost containment strategy for all operators. HCA reported it was hemorrhaging money following its first-quarter majority stake purchase of staffing firm Valesco, which brought about 5,000 physicians onto its payroll. HCA CEO Sam Hazen said the system expects to lose $50 million per quarter on the venture through 2024, citing low payments as the primary issue.

Payer problems

Hospital executives also tied quarterly losses to aggressive behavior from insurers during third-quarter earnings calls.

UHS executives said payers were improperly denying high volumes of claims and disrupting payments to its hospitals, with UHS’ Miller characterizing insurers as “increasingly aggressive” during the third quarter. Though insurers had reduced their number of claims audits, denials and patient status changes during the early stages of the pandemic, payers were increasing denials and reviews, according to UHS’ Filton.

Tenet’s Sutaria said that claims denials were “excessive and inappropriate” during a third-quarter earnings call, adding that the hospital system was working to push back on the volume of claims denials.

Their number one strategy is to provide “excellent documentation” to refute denials quickly, Sutaria said.

Still, excessive claims denials can drive up administrative costs for hospitals, according to Matthew Bates, managing director at Kaufman Hall.

“That denial creates a lot more work, because now I have to deal with that bill two, three, four times to get through the denial process,” Bates said. “It starts to rapidly eat into the operating margins… [becoming] both a cashflow problem and an administrative costs burden.”

Executives across the four for-profit operators said they planned to negotiate with insurers to receive more favorable rates and limit the number of denials in subsequent quarters.

HCA’s Hazen said that it was important for HCA to maintain its in-network status with insurers “to avoid the surprise billing and that [independent dispute resolution] process,” but that it would work with its payers to get “reasonable rates” going forward.

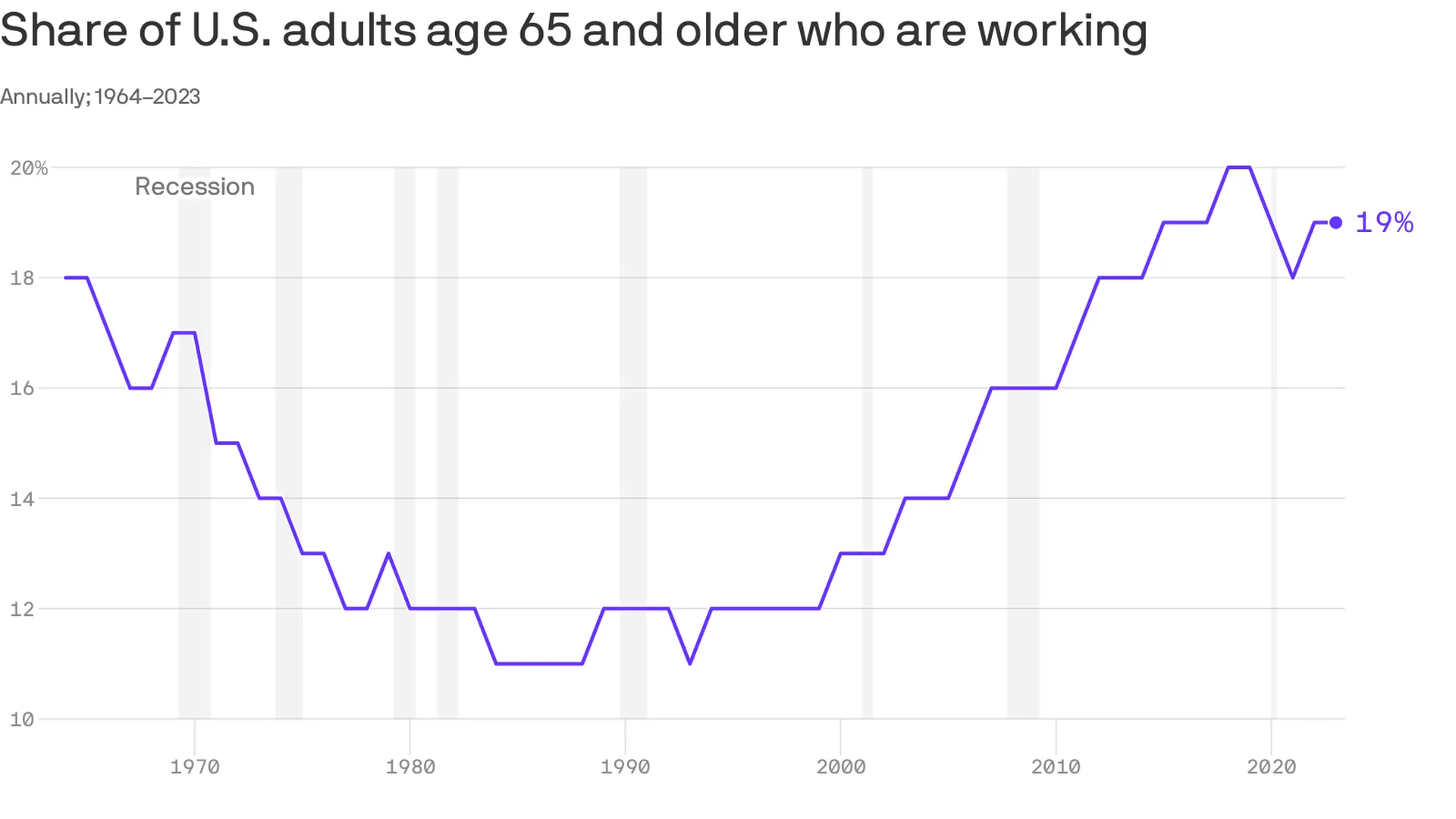

An increasing number of Americans age 65 and older are working — and earning higher wages, per a study from the Pew Research Center out Thursday.

Why it matters:

This is good for the economy, especially as the U.S. population ages — but whether or not it’s good for older Americans is a bit more subjective.

Zoom in:

The share of older adults working has been steadily increasing since the late 1980s, with a detour during the pandemic as older folks retired in greater numbers. Several forces are driving the shift:

Older workers are increasingly likely to have a four-year degree, and typically workers with more education are more likely to be employed.

Technology has made many jobs less physically taxing, so older workers are more likely to take them.

Meanwhile, changes in the Social Security law pushed many to continue working past 65 to get their full retirement benefits.

At the same time, there’s been a shift away from pension plans, which typically force people out of a job at a certain age, into 401(k) style plans that are less restrictive (and less generous, critics say).

By the numbers:

Last year, the typical 65+ worker earned $22 an hour, up from $13 (in 2022 dollars)in 1987. That’s about $3 less than the average for those age 25-64, and the number includes wages of full- and part-time workers.

Be smart:

Before Social Security existed, older people worked — a lot. In the 1880s, about three-fourths of older men were employed, said Richard Fry, senior researcher at Pew. They also didn’t live as long.

Meanwhile, the 65+ age group is a fast-growing one — by 2032 all the baby boomers will be in this category, per the BLS’s projections, and their increased workforce participation is good for an economy that is struggling with long-term labor shortages.

The big picture:

“If people are working longer because they find purpose in their jobs and want to stay engaged, that’s good for them individually,” said Nick Bunker, head of economic research at Indeed Hiring Lab.

It’s also good for the productive capacity of the economy, and the firms where they work. “Older folks have lots of experience and knowledge to pass down,” he said.

Yes, but: If there are people who want to retire, but can’t because of financial constraints, “that’s bad,” he added.

What to watch:

The share of older adults working peaked before the pandemic — will it surpass those levels?

The number hasn’t bounced back as much as anticipated partly because older Americans benefited hugely from the stock market surge and real estate gains of the past few years — and didn’t need to work anymore.

Starbucks is softening its stance toward unionization after years of pushing back.

Why it matters:

It’s a potentially huge shift for the chain and a signal of the staying power of the labor movement that surged in the wake of the pandemic.

“They know this isn’t going away,” said Nick Setyan, an equity analyst at Wedbush who covers Starbucks. He called the company’s new posture “capitulation.”

Setyan said recent worker walkouts were a turning point. Also, at least five more stores this month voted to unionize.

Zoom out:

Union organizing efforts have been a public relations headache for Starbucks since at least 2021 when a store in Buffalo became the first to vote for a union. Meanwhile, pressure from labor regulators isn’t slowing.

Zoom in:

Starbucks’ strategy shift began in March whenLaxman Narasimhan took the CEO reins from founder Howard Schultz, who had repeatedly clashed with workers over unionizing. The new CEO spoke of the need to care for customer-facing staff, per Reuters.

It’s accelerated over the past week — last Friday, Starbucks vice president Sara Kelly sent a letter to Workers United (the union that reps workers), saying the company wanted to restart bargaining.

The union has yet to bargain a contract. Starbucks now says it wants an agreement by next year.

On Wednesday, the company released an audit on its labor relations practices that was commissioned by Starbucks — after a shareholder vote forced its hand — and conducted by a former management-side lawyer.

Though the report asserted Starbucks didn’t have an “anti-union playbook,” it did find the company was unprepared to deal with its unionizing workforce and acknowledged that store managers made mistakes in how they handled the situation.

The report offers recommendations for improvement — including better training. Change starts with “tone from the top,” the audit says, suggesting that the company should reach agreements with the union “expeditiously.”

What happened:

Starbucks initially believed it could fend off unionization by messaging about best-in-class wages and benefits, Setyan said, noting that it’s true the chain offers better compensation than competitors.

“Internally, they felt kind of aggrieved,” he said, that workers who management perceived as well-compensated would want to organize.

For a while it seemed like the messaging campaign was working, but the Red Cup Rebellion walkout last month and a flurry of new union votes changed minds.

Starbucks has historically been very sensitive to public relations — and it became clear pushing back isn’t great for its image, Setyan said.

The other side:

Union representatives are skeptical of Starbucks’ new position.

“We are hopeful your letter is indeed the beginning of a sincere effort, and not a publicity move in the face of pressure from partners, Wall Street, shareholders, and others,” Workers United president Lynne Fox, said in a letter to Kelly last week.

What to watch:

If Starbucks’ change in tone is a sign that the company will finally come to terms with these workers, and agree to a contract, or just a shift in its public stance while it continues efforts to avoid a deal.

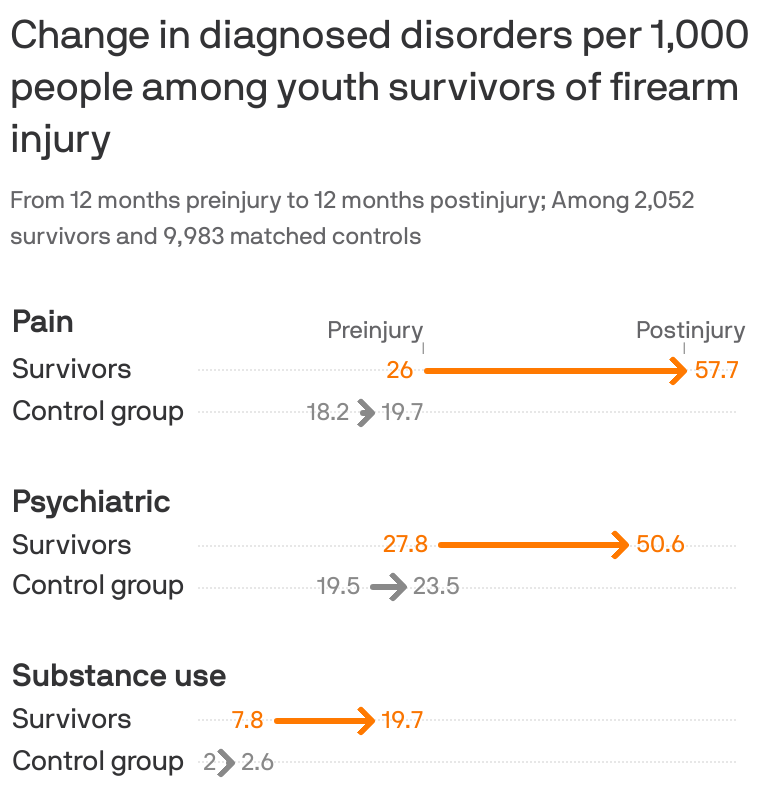

Young survivors of shootings face a litany of physical, psychiatric and substance abuse disorders that can combine to drive up their health costs almost 2,000%, according to new research.

The big picture:

Guns have become the leading cause of death among kids, but many more survive being shot. Their needs offer a rare and detailed look at the cumulative consequences of gun violence and the burden it places on survivors, their families and the health system.

By the numbers:

Using a trove of claims data for employer-sponsored insurance, researchers in Health Affairs compared over 2,000 child and adolescent shooting survivors and 6,000 family members with much larger control groups that did not suffer gun injury between 2007-2021.

In the year after being shot, survivors had a 117% increase in pain disorders including musculoskeletal pain and headaches compared with the control group, with a 293% increase for those more severely wounded.

There was a 68% increase in psychiatric disorders, such as PTSD and mood disorders, with a 321% increase among those with worse injuries.

Substance use disorders rose 144% percent — and cases rose regardless of the severity of the injury.

Emergency room visits for gun injuries among kids doubled during the pandemic, according to separate research published Monday in Pediatrics.

There is also an impact on families’ mental health and even the types of care they got in the aftermath of a child surviving a shooting, researchers found in the Health Affairs study.

Diagnosed psychiatric disorders among mothers and fathers increased by about 30% — and the increases were much larger among parents of children who died.

Mothers had a 75% increase in mental health visits, while other routine care like office visits and lab tests declined slightly for themselves and the siblings of survivors.

That was consistent with a “crowding out” effect when more acute health care needs arise, researchers said.

What they’re saying:

“Our study shines light on the substantial effects incurred not just directly by victims and survivors of gun violence, but indirectly by parents and siblings who, we found, often relinquish their own routine health care to the more acute health needs of the family,” senior study author Chana Sacks, co-director of the MGH Gun Violence Prevention Center, said in a statement.

Survivors’ health care costs also soared 17-fold to nearly $35,000 on average over the course of a year. Two-thirds of the cost was in the first month after being shot, while survivors used more health care across the board — including more visits to doctor’s offices, ER trips, imaging and mental health services.

Insurers covered the vast majority of the care, but families were on hook for about 5% of the cost.

Between the lines:

Researchers looked at claims data for workplace health insurance only, so the results don’t include kids without insurance or those enrolled in Medicaid — a major source of coverage, especially for children of color.

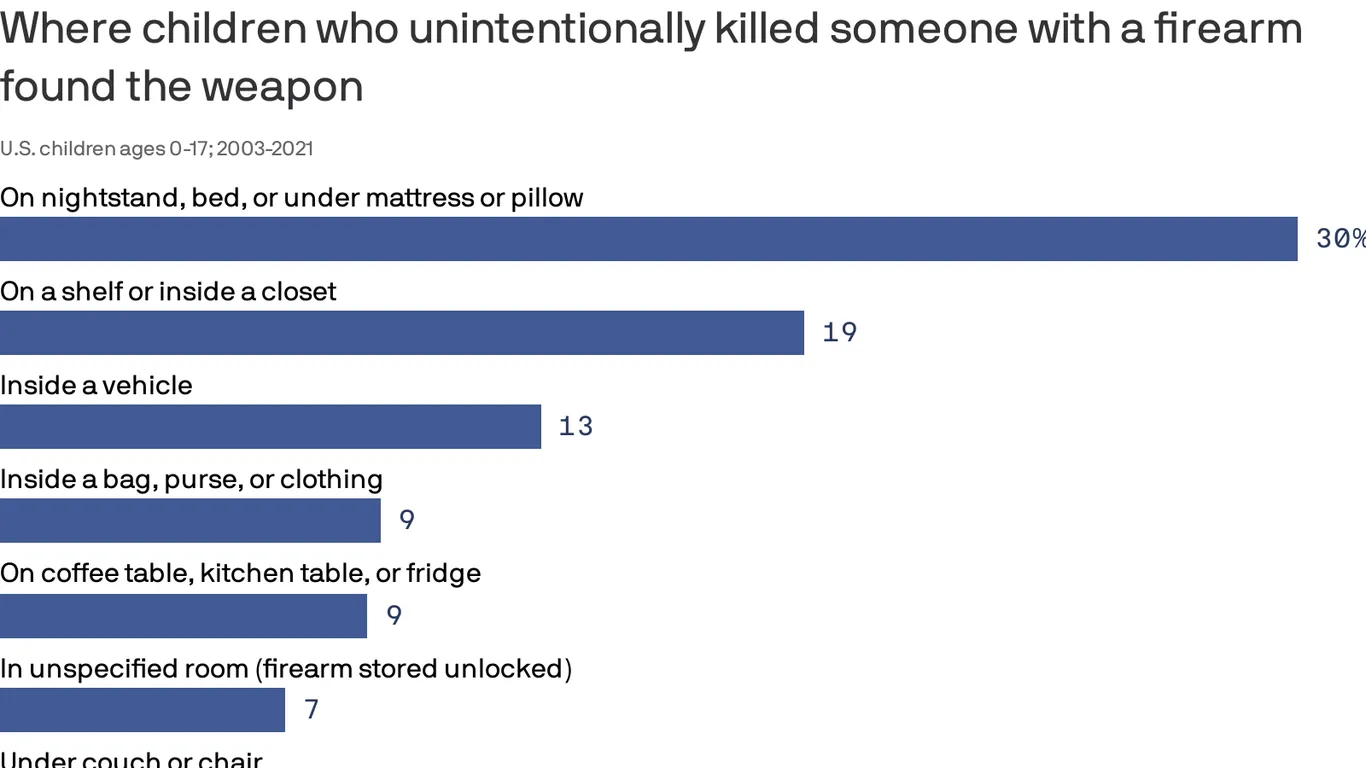

Children and teens involved in unintentional fatal shootings most commonly found the gun inside or on top of a nightstand, under a mattress or pillow, or on top of a bed, according to a new federal study.

Why it matters:

The data from the Centers for Disease Control and Prevention, which covers nearly 20 years of deadly firearm accidents among America’s youth, demonstrates why putting a gun out of sight or out of reach is not “safe storage,” federal researchers said.

It underscores the need for policymakers, health experts and parents to promote safe gun storage, they said.

Using data recorded between 2003 and 2021 by the National Violent Death Reporting System, researchers identified more than 1,250 unintentional gun deaths among kids.

The vast majority involved guns that were unlocked (76%), and most of those unlocked firearms were also loaded (91%).

Two-thirds (67%) of unintentional gun injury deaths among kids occurred when the shooter was playing with the gun or showing it to others.

In 30% of deaths, guns were found around nightstands and other sleeping areas.

Guns were also most commonly found on top of a shelf or inside a closet (18.6%) or inside a vehicle (12.5%).