http://bigstory.ap.org/article/a6c6a83bd9f7435ca6f79423f1240c4d/why-it-matters-health-care

About 9 in 10 Americans now have health insurance, more than at any time in history. But progress is incomplete, and the future far from certain. Millions remain uninsured. Quality is still uneven. Costs are high and trending up again. Medicare’s insolvency is two years closer, now projected in 2028. Every family has a stake.

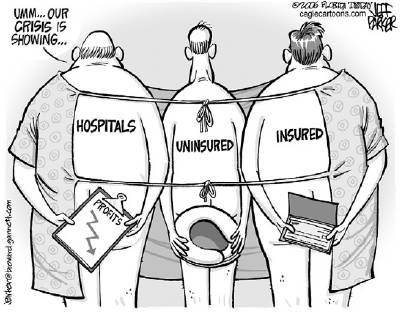

Patients from all over the world come to America for treatment. U.S. research keeps expanding humanity’s ability to confront disease. But the U.S. still spends far more than any advanced country, and its people are not much healthier.

Obama’s progress reducing the number of uninsured may be reaching its limits. Premiums are expected to rise sharply in many communities for people covered by his namesake law, raising concerns about the future.

The health care overhaul did not solve the nation’s longstanding problem with costs. Total health spending is picking up again, underscoring that the system is financially unsustainable over the long run. Employers keep shifting costs to workers and their families.

No one can be denied coverage anymore because of a pre-existing condition, but high costs are still a barrier to access for many, including insured people facing high deductibles and copayments. Prescription drug prices — even for some generics — are another major worry.

The election offers a choice between a candidate of continuity — Clinton — and a Republican who seems to have some core beliefs about health care, but lacks a coherent plan.

If the presidential candidates do not engage the nation in debating the future of health care, it still matters.