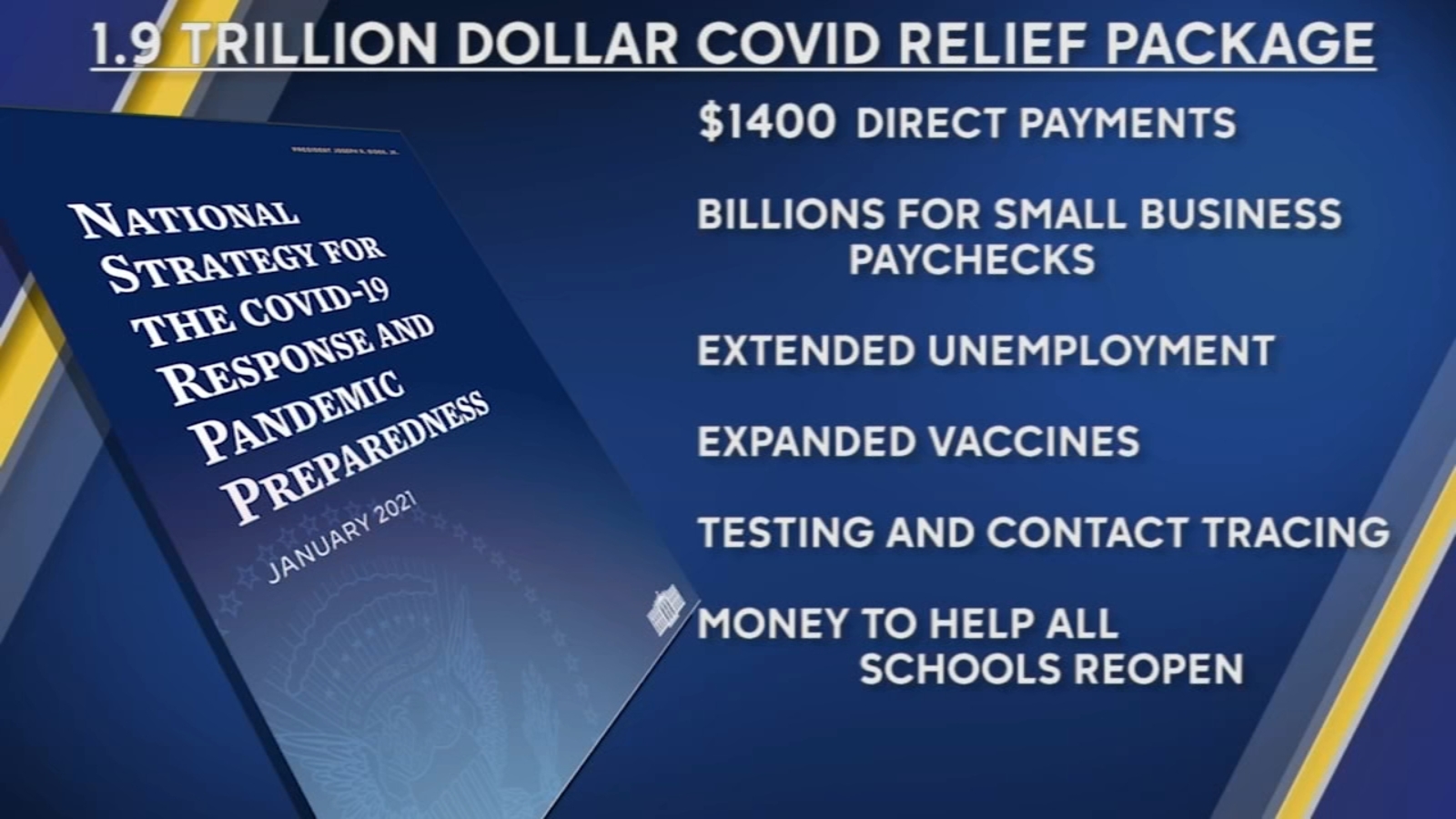

The House on Wednesday passed the mammoth $1.9 trillion COVID-19 relief package, which President Biden is expected to sign Friday.

The House approved the relief package in a starkly partisan 220-211 vote, sending the legislation to the White House and clinching Democrats’ first big legislative victory in the Biden era. No Republicans voted for the package and all but one House Democrat—Rep. Jared Golden of Maine—supported it. The Hill’s Cristina Marcos has more here.

The political split: Unlike the previous relief measures enacted last year, Democrats barely bothered to negotiate with Republicans and pushed the relief package through Congress along party lines using the budget reconciliation process. That allowed them to go as big as they wanted to go without running into a Senate GOP filibuster.

Republicans argue the use of a process dodging the filibuster shows Biden wasn’t serious about bringing unity, and House GOP lawmakers on Wednesday warned of the bill’s total cost.

But Democrats think Republicans will pay for their opposition to the popular bill and argued that they would oppose anything Biden proposed.

What’s in the $1.9T COVID-19 relief package: Along with $1,400 direct payments to households, an extension of expanded unemployment benefits, and aid for state and local governments, the package is loaded with other provisions intended to speed up the recovery from the recession and help struggling families fight the impact of COVID-19.

Tax credits: The bill increases the child tax credit for households below certain income thresholds for 2021 and makes it fully refundable, and also expands the earned income tax credit for the year.

Child care: $15 billion for grants to help low-income families afford child care and increases the child and dependent care tax credit for one year.

Pensions: $86 billion to bailout struggling union pension funds.

Transportation: $30 billion to bolster local subway and bus systems, $8 billion for airports, $1.5 billion for furloughed Amtrak workers, and $3 billion for wages at aerospace companies.

Housing: $27.4 billion in emergency rental assistance, another $10 billion to help homeowners avoid foreclosure, $5 billion in vouchers for public housing, $5 billion to tackle homelessness and $5 billion more to help households cover utility bills.

Small businesses: The American Rescue Plan broadens eligibility guidelines for the Paycheck Protection Program, allowing more nonprofit entities to be eligible, adds $15 billion in emergency grants and also sets aside more than $28 billion in funding for restaurants.

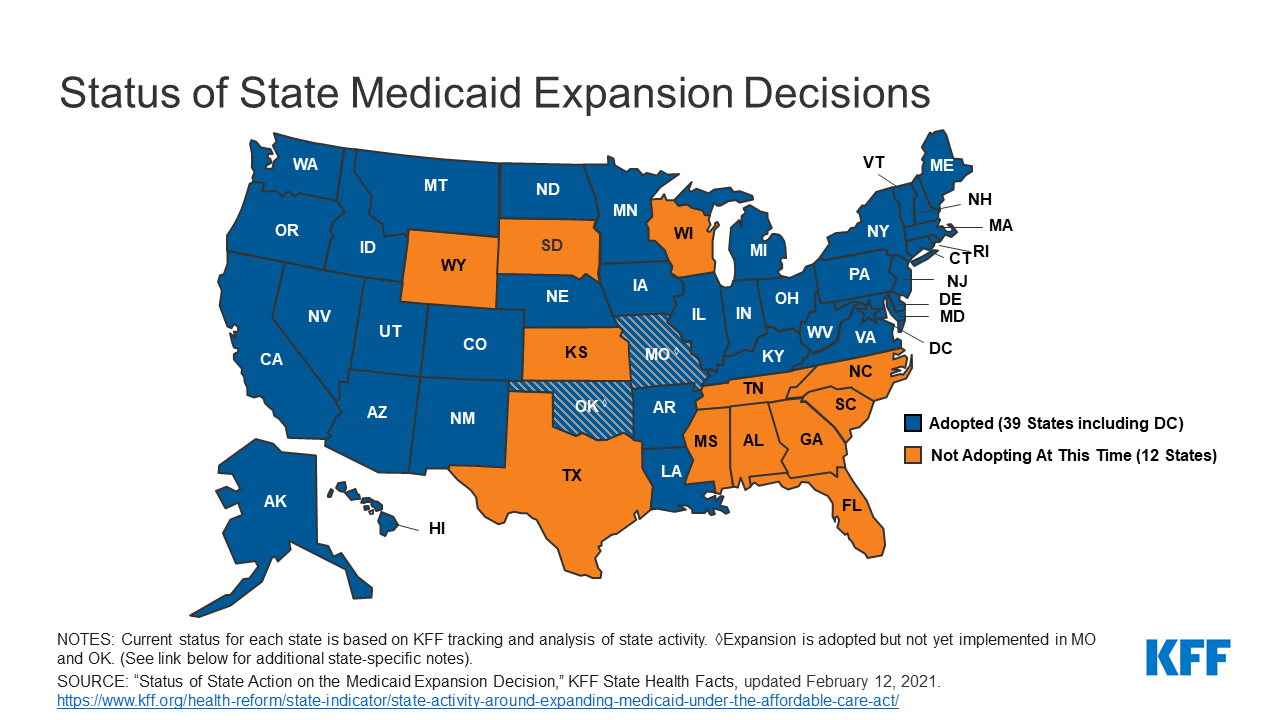

ObamaCare subsidies and Medicaid expansion: The bill increases ObamaCare subsidies through 2022 to make them more generous, a longtime goal for Democrats, and opens up more fully subsidized plans to individuals. It also would provide extra Medicaid funding to states that expand the program and have yet to do so.

President Joe Biden has an unexpected opening to cut deals with red states to expand Medicaid, raising the prospect that the new administration could extend health protections to millions of uninsured Americans and reach a goal that has eluded Democrats for a decade.

The opportunity emerges as the covid-19 pandemic saps state budgets and strains safety nets. That may help break the Medicaid deadlock in some of the 12 states that have rejected federal funding made available by the Affordable Care Act, health officials, patient advocates and political observers say.

Any breakthrough will require a delicate political balancing act. New Medicaid compromises could leave some states with safety-net programs that, while covering more people, don’t insure as many as Democrats would like. Any expansion deals would also need to allow Republican state officials to tell their constituents they didn’t simply accept the 2010 health law, often called Obamacare.

“Getting all the remaining states to embrace the Medicaid expansion is not going to happen overnight,” said Matt Salo, executive director of the nonpartisan National Association of Medicaid Directors. “But there are significant opportunities for the Biden administration to meet many of them halfway.”

Key to these potential compromises will likely be federal signoff on conservative versions of Medicaid expansion, such as limits on who qualifies for the program or more federal funding, which congressional Democrats have proposed in the latest covid relief bill.

But any deals would bring the country closer to fulfilling the promise of the 2010 law, a pillar of Biden’s agenda, and begin to reverse Trump administration efforts to weaken public programs, which swelled the ranks of the uninsured.

“A new administration with a focus on coverage can make a difference in how these states proceed,” said Cindy Mann, who oversaw Medicaid in the Obama administration and now consults extensively with states at the law firm Manatt, Phelps & Phillips.

Medicaid, the half-century-old health insurance program for the poor and people with disabilities, and the related Children’s Health Insurance Program cover more than 70 million Americans, including nearly half the nation’s children.

Enrollment surged following enactment of the health law, which provides hundreds of billions of dollars to states to expand eligibility to low-income, working-age adults.

However, enlarging the government safety net has long been anathema to most Republicans, many of whom fear that federal programs will inevitably impose higher costs on states.

And although the GOP’s decade-long campaign to “repeal and replace” the health law has largely collapsed, hostility toward it remains high among Republican voters.

That makes it perilous for politicians to embrace any part of it, said Republican pollster Bill McInturff, a partner at Public Opinion Strategies. “A lot of Republican state legislators are sitting in core red districts, looking over their shoulders at a primary challenge,” he said.

Many conservatives have called instead for federal Medicaid block grants that cap how much federal money goes to states in exchange for giving states more leeway to decide whom they cover and what benefits their programs offer.

Many Democrats and patient advocates fear block grants will restrict access to care. But just before leaving office, the Trump administration gave Tennessee permission to experiment with such an approach.

“It’s a frustrating place to be,” said Tom Banning, the longtime head of the Texas Academy of Family Physicians, which has labored to persuade the state’s Republican leaders to drop their opposition to expanding Medicaid.“Despite covid and despite all the attention on health and disparities, we see almost no movement on this issue.”

Some 1.5 million low-income Texans are shut out of Medicaid because the state has resisted expansion, according to estimates by KFF. (KHN is an editorially independent program of KFF.)

An additional 800,000 people are locked out in Florida, which has also blocked expansion.

Two million more are caught in the 10 remaining holdouts: Alabama, Georgia, Kansas, Mississippi, North Carolina, South Carolina, South Dakota, Tennessee, Wisconsin and Wyoming.

Advocates of Medicaid expansion, which is broadly popular with voters, believe they may be able to break through in a handful of these states that allow ballot initiatives, including Mississippi and South Dakota.

Since 2018, voters in Idaho, Nebraska, Utah, Oklahoma and Missouri have backed initiatives to expand Medicaid eligibility, effectively circumventing Republican political leaders.

“The work that we’ve done around the country shows that no matter where people live — red state or blue state — there is overwhelming support for expanding access to health care,” said Kelly Hall, policy director of the Fairness Project, a nonprofit advocacy group that has helped organize the Medicaid measures.

But most of the holdout states, including Texas, don’t allow citizens to put initiatives on the ballot without legislative approval.

And although Florida has an initiative process, mounting a ballot campaign there is challenging, as political advertising is expensive. Unlike in many states, Florida’s leading hospital association hasn’t backed expansion.

Another route for expansion: compromises that could win over skeptical Republican state leaders and still get the green light from the Biden administration.

The Obama administration approved conservative Medicaid expansion in Arkansas, which funneled enrollees into the commercial insurance market, and in Indiana, which forced enrollees to pay more for their medical care.

Money is a major focus of current talks in several states, according to health officials, advocates and others involved in efforts across the country.

The health law at first fully funded Medicaid expansion with federal money, but after the first three years, states had to begin paying part of the tab. Now, states must come up with 10% of the cost of expansion.

Even that small share is a challenge for states, many of which are reeling from the economic downturn caused by the pandemic, said David Becker, a health economist at the University of Alabama-Birmingham who has assisted efforts to expand Medicaid in that state.

“The question is: Where do we get the money?” Becker said, noting that some Republicans may be open to expanding Medicaid if the federal government pays the full cost of the expansion, at least for a year or two.

Other efforts to find ways to offset state costs are underway in Kansas and North Carolina, which have Democratic governors whose expansion plans have been blocked by Republican state legislators. Kansas Gov. Laura Kelly this month proposed using money from the sale and taxation of medical marijuana.

Some Democrats in Congress are pushing to revise the health law to provide full federal funding to states that expand Medicaid now. Separately, in the stimulus bill unveiled last week, House Democrats proposed an additional boost in total Medicaid aid to states that expand.

Other Republicans have signaled interest in partly expanding Medicaid, opening the program to people making up to 100% of the federal poverty level, or about $12,900, rather than 138%, or $17,800, as the law stipulated.

The Obama administration rejected this approach, but the idea has gained traction in several states, including Georgia.

It’s unclear what kind of compromises the new administration may consider, as Biden has yet to even nominate someone to oversee the Medicaid program.

Some Democrats say it’s time to give up the search for middle ground with Republicans on Medicaid.

A better strategy, they say, is a new government insurance plan, or public option, for people in non-expansion states, a strategy Biden endorsed on the campaign trail.

“Democrats can no longer countenance millions of Americans living in poverty without insurance,” said Chris Jennings, a Democratic health care strategist who worked in the White House under Presidents Bill Clinton and Barack Obama and served on Biden’s transition team.

“This is why the Biden public option or other new ways to secure affordable, meaningful care should become the order of the day for people living in states like Florida and Texas.”

Young adults were among the most likely to be uninsured prior to the Affordable Care Act, but the law’s Medicaid expansion had a significant impact on those rates, according to a new study.

Research published by Urban Institute, this week shows the uninsured rate for people aged 19 to 25 declined from 30% to 16% between 2011 and 2018, while Medicaid enrollment for this population increased from 11% to 15% in that window.

The coverage increases were felt most keenly between 2013 and 2016, when many of the ACA’s key tenets were carried out, including Medicaid expansion and the launch of the exchanges, according to the study.

“Before the ACA, adolescents in low-income households often aged out of eligibility for public health insurance coverage through Medicaid or the Children’s Health Insurance Program as they entered adulthood,” the researchers wrote. “Further, young adults’ employment patterns made them less likely than older adults to have an offer of employer-sponsored insurance coverage.”

States that expanded Medicaid saw greater declines in the number of young people without insurance, the study found.

On average, the uninsured rates among young people declined from nearly 28% in 2011 to 11% in 2018, according to the analysis. In non-expansion states, however, the uninsured rate decreased from about 33% to nearly 21%.

In expansion states, Medicaid enrollment for people aged 19 to 25 rose from 12% in 2011 to close to 21%, according to the study, while enrollment in non-expansion states remained flat.

Urban’s researchers estimate that Medicaid expansion is linked to a 3.6 percent point decline in uninsurance among young people overall, and had the highest impact on young Hispanic people. Uninsurance decreased by 6 percentage points among Hispanic young people, the study found, and that population had the largest uninsured rate prior to the ACA.

“The effects of Medicaid expansion on young adults’ health insurance coverage and health care access provide evidence of the initial pathways through which Medicaid expansions could improve young adults’ overall health and trajectories of health throughout adulthood,” the researchers wrote.

“Beyond coverage and access to preventive care, Medicaid expansion may affect young adults’ health care use in ways not examined in our report. Thus, ensuring young adults have health insurance coverage and access to affordable care is a critical first step toward long-term health,” they wrote.

Molina’s net income fell sharply in the fourth quarter as the insurer was forced to refund rates to some of its state partners as COVID-19 continues to depress normal care utilization, CEO Joe Zubretsky told investors Thursday.

Although utilization remained curtailed, COVID-19 costs were higher in the fourth quarter than any other quarter in 2020, Zubretsky said. As such, Molina’s medical care ratio for the quarter increased to 90.8% from 86% the prior-year period.

Still, Molina remained in the black for the full year of 2020. Looking ahead, the company expects utilization to improve, though does not expect it to rebound entirely. At the same time, the company expects direct COVID-19 costs to come in lower than last year.

Dive Insight:

Insurers have largely remained unbruised from the pandemic, unlike some providers, but the fourth quarter was a different story.

The pandemic took a bite out of Molina’s net income in the fourth quarter as the company reported that figure fell to $34 million from $168 million in Q4 2019.

The biggest contributor to the impact on the bottom line was Medicaid refunds to states, including California, Michigan and Ohio. States have clawed back some of the money they pay insurers like Molina as members continue to defer care, which is a benefit to insurers as they then pay out less.

Molina painted a clearer picture of this scenario during Thursday’s conference call with investors.

For the full year, Molina estimated that medical cost suppression amounted to $620 million while direct COVID-19 costs amounted to $200 million. In other words, curbed utilization continued to outweigh direct COVID-19 costs, resulting in a $420 million benefit from the pandemic, which the company characterized as a surplus.

But states took back a total of $565 million through rate refunds. Overall, the net impact of COVID-19 was a $180 million hit to Molina for 2020 when factoring in other costs.

Looking ahead, executives seemed cautiously optimistic for 2021 but noted headwinds from the pandemic will persist. While the forecast reflects future growth, Zubretsky said, “it is a constrained picture” of the company’s potential earnings.

Some of those headwinds include Medicare risk scores that don’t fully capture the acuity of their Medicare members. As seniors put off care in 2020, companies like Molina were unable to capture diagnosis codes to help them determine how sick members are and the ultimate risk they pose.

Still, there are some bright spots. As the public health emergency is likely to be continued throughout the remainder of the year, it means that redeterminations will remain halted, or, in other words, Medicaid members will not be kicked off coverage.

This was a boon for Molina in 2020, as it allowed them to pick up a significant number of new members. Overall, it was a major catalyst for Medicaid membership growth in 2020, Zubretsky said.

Molina expects care utilization to improve this year but not fully return to normal. Instead, it expects utilization suppression to be about one third of 2020 levels.

Molina, which solely focuses its portfolio on government sponsored and marketplace plans, said it expects to pick up as many as 30,000 additional members during the Affordable Care Act special enrollment period.

Opening up a special enrollment period was one of the first moves made by the new administration in the White House. Zubretsky seems enthused by the recent moves through executive orders and the unfolding bill developments in Congress that are looking to raise premium subsidies on the exchanges.

Those early actions “just couldn’t be better for government sponsored managed care, and we’re pleased to see that progress already being made,” Zubretsky said.

Karen Lynch, the new president and CEO of CVS Health, said during an earnings call on Tuesday that Aetna will reenter the ACA business. The ACA business has improved, she said, and Aetna will rejoin the ACA marketplace, selling individual coverage in 2022.

“We’ll accelerate the pace of progress via targeted investments that will drive consumer-focused strategy,” Lynch said. “We will create future economic benefit for CVS Health and its shareholders.”

Aetna joined other insurers in leaving or downsizing its footprint as premiums rose and insurers lost money.

The ACA market has grown since the exodus and shown strength in 2021, in lower premiums for consumers, steady enrollment numbers and insurers expanding their marketplace reach.

As COVID-19 has cost many their employer-based health insurance, the Biden Administration has opened a new enrollment period that started on February 15 and goes through May 15.

THE LARGER TREND

President Donald Trump and Congressional GOP members attempted to get rid of the Affordable Care Act that was passed into law by his predecessor, President Barack Obama.

Trump’s successor, President Biden, has promised to strengthen the market, even as the Supreme Court considers whether the ACA law remains valid without the individual mandate’s tax penalty. The Supreme Court is expected to hand down a decision by June.

In 2018, Aetna became part of CVS Health in a $69 billion merger.

Starting next week, millions of uninsured Americans will have the opportunity to sign up for coverage on the federal insurance marketplace, the result of President Biden’s executive order to create a 90-day special enrollment period. The graphic above highlights the potential impact of this enrollment period on the uninsured population.

According to a Kaiser Family Foundation analysis, of the nearly 15M uninsured who are marketplace-eligible,nearly 9M qualify for free or subsidized coverage. Enrollment of these individuals will come with added challenges, as they tend to be less educated, younger, more rural, and less likely to speak English, as compared to the general population. An Urban Institute survey foundalmost half of uninsured individuals are unfamiliar with marketplace coverage options, and nearly two-thirds lack an understanding of available financial assistance.

The federal government is dedicating $50M to advertise the special enrollment period, to assist with outreach and education. Given the population most likely to have lost insurance due to the COVID pandemic, this funding will be critical to making sure eligible people take advantage or free or low-cost coverage.

Ahead of a Supreme Court hearing in March to consider the legality of imposing work requirements as a condition of gaining Medicaid coverage, the Centers for Medicare and Medicaid Services (CMS) were expected to inform states on Friday of plans to rescind the controversial Trump administration policy.

Under the previous administration, ten states had applied for and were approved to use waiver authority to impose work requirements on Medicaid enrollees, and several other states were in the process of submitting applications. Critics (including us) have long held that such requirements, while nominally intended to introduce an element of “personal responsibility” to the safety-net coverage program for low-income Americans, actually serve to hinder access to care, and jeopardize the health status of already vulnerable populations; in addition, the added expense of program infrastructure often exceeds anticipated cost savings.

The policy was a favored project of former CMS administrator Seema Verma, who helped craft a similar program for the state of Indiana before joining the Trump administration. Among states granted waiver authority to impose work requirements, only Arkansas ever fully implemented the policy, before the legality of the waivers was challenged successfully in lower courts.

The Biden administration’s recision of work requirements is part of a broader reversal of Trump-era healthcare policies. This week the Justice Department notified the Supreme Court that it was switching sides in the closely watched case questioning the constitutionality of the Affordable Care Act (ACA), although the court has already heard the case and is expected to rule this spring. Starting Monday, the Biden team will also reopen the federal insurance marketplace for a special enrollment period, bolstering funding for outreach to ensure those eligible are aware of coverage options. And as part of its proposed COVID relief legislation, the administration plans toincrease subsidies to help individuals buy coverage on the exchanges, and to increase funding to support state Medicaid programs—policies that got a boost this week from a broad coalition of healthcare industry groups, including health plans, doctors, and hospitals.

As the administration rounds out its health policy team, we’d expect a continuedfocus on strengthening the core pillars of the ACA, along with a greater focus on ensuring health equity and addressing disparities. Meanwhile, two key positions remain unfilled: CMS administrator and commissioner of the Food and Drug Administration (FDA). These slots will likely remain open until the looming confirmation battle over Biden’s nominee for Secretary of Health and Human Services (HHS), California Attorney General Xavier Becerra, has been settled.

Thursday was healthcare day at the Biden White House, the latest in a series of themed days during which the President has issued executive orders on topics ranging from COVID response to climate change to racial equity.

Facing a closely divided Congress, the new administration has focused so far on actions it can take unilaterally to advance its agenda, and as President Biden described it at a signing ceremony yesterday, his healthcare agenda is centered on “restoring the Affordable Care Act and restoring Medicaid to the way it was” prior to the Trump administration.

The new executive order reopens the HealthCare.gov insurance marketplace for a “special enrollment period”, lasting from mid-February to mid-May, allowing approximately 15M uninsured Americans in 36 states (including 3M who lost employer-based insurance due to COVID) to sign up for coverage, many subsidized by the federal government.

The order also instructs agencies to review many of the regulatory changes made by the Trump administration, including loosening restrictions on short-term insurance plans, and allowing states to use waivers to implement Medicaid work requirements. (Also included in Thursday’s action was a measure to immediately rescind the ban on taxpayer funding for abortion-related counseling by international nonprofits, the so-called “Mexico City rule”.)

Actually unwinding those Trump-era changes will take months (or possibly years) of regulatory work to accomplish, but Biden’s executive order puts that work in motion. Attention now turns to Congress, which the Biden team hopes will provide funding for increased subsidies for coverage on the Obamacare exchanges, along with allocating money for the administration’s aggressive COVID response plan.

Yesterday’s executive order is best understood as the starting gun for the lengthy legislative and regulatory process that lies ahead, as the Biden administration tries to bolster the 2010 health reform law, and stamp its mark on American healthcare.

The nearest-term 2021 actions will likely center on bolstering the ACA and Medicaid, after the Trump administration took aim at both.

Even with Democrats’ surprise flipping of the Senate, enacting big healthcare policies in Congress will be a heavy lift given the razor-thin margin in that body and division within the party on strategy.

A clearer path for incoming president Joe Biden is to focus on reversing policies enacted by President Donald Trump at the executive level.Trump’s tenure has been defined in large part by a chipping away at key tenets of the Affordable Care Act, curtailing the Medicaid program and sweeping deregulations critics allege harm consumer protections.

The nearest-term actions the incoming administration is likely to take will center on bolstering the landmark health law and Medicaid, both of which has drawn more bipartisan backing in recent years. Below are what the Biden health administration is likely to roll back quickly after inauguration Wednesday.

Boosting Affordable Care Act marketplace

One of Biden’s first moves may be to open a special enrollment period to sign up for coverage during COVID-19, combined with more outreach and enrollment assistance, Cynthia Cox, director of the ACA program at the Kaiser Family Foundation, said.

Beyond COVID-19, it’s likely the Biden administration will restore federal spending on navigation, marketing and outreach for exchange plans. For example, the Trump administration reduced the minimum number of navigator programs in each state using the federal marketplace to one. Biden could return it to two, and might also bring back the requirement that navigators have a physical presence in their service area.

Biden is also likely to unilaterally shore up standards for brokers, and take steps to bolster the exchange website healthcare.gov.

The Trump administration in December proposed a rule encouraging states to privatize their health insurance marketplaces instead of using healthcare.gov, which will make it more difficult for consumers to shop between plans and could divert people to subpar coverage, Tara Straw, senior policy analyst at the Center on Budget and Policy Priorities, wrote in a December blog post.

The rule doubles down on the administration’s approval of a Georgia waiver to privatize its marketplace in November, but would allow states to follow suit and rely entirely on third-party brokers without a waiver.

That rule is not yet final, so Biden’s HHS will likely remove it from the Federal Register to avoid fragmenting marketplace functions.

Biden could also beef up consumer protections and standards for web brokers, which also sell skimpy short-term health insurance and other non-ACA-compliant coverage.

Biden is also likely to re-expand the annual enrollment period. In 2017, the Trump administration shortened the annual enrollment period to 45 days. Biden’s HHS could use rulemaking to return that period to three full months.

The incoming administration could also reverse previous CMS guidance on Section 1332 waivers that let states subvert or sidestep ACA protections on coverage and cost. The Trump administration proposed a rule in November to codify the waiver standards in regulation but — despite a recent wave of proposed and final regulations as the Trump administration hustles to preserve its health agenda — the rule has not yet been finalized, so HHS could remove it from the Federal Register as well.

By nixing the rule, Biden could also help reverse Trump administration cuts from 2018 that slashed user fees on healthcare.gov plans. The November proposed rule would further decimate the fees, which finance a large swath of marketplace operating expenses, to 2.25% in 2022, versus 3% in 2021 and 3.5% last year.

One key tenet of Biden’s health agenda is to expand ACA subsidies to more low-income Americans, something he can’t do without Congress.However, Biden could use administrative processes to reverse a Trump-era method for indexing marketplace subsidies that kicked in for the 2020 plan year, which led to a small reduction in the financial aid.

Dialing back short-term and association health plans

Biden’s HHS could also roll back the controversial expansion of short-term health plans, bare-bones coverage that isn’t required to cover the 10 essential health benefits under the ACA.

Short-term plans were created as inexpensive stop-gap insurance that could last for up to three months, giving consumers peace of mind while they shopped more comprehensive coverage. However, in 2018, the Trump administration expanded the duration of the plans to 12 months, with a three-year renewal period, and also allowed all consumers — not just those who couldn’t afford other options — to purchase them.

HHS touted the expansion as giving consumers more options, while noting they weren’t meant for everyone. A yearlong investigation by House Democrats found the plans widely discriminate against women and people with pre-existing conditions, and had major coverage limitations leaving unwitting consumers susceptible to surprise medical bills.

The Biden administration could enact stricter limits against the sale of the plans. Through additional rulemaking, HHS could limit future enrollment or make it harder to renew short-term coverage, enact stronger consumer protections or beef up standards to limit their sale.

Though actions around limiting new people coming into the plans are likely, Biden may wait to see if Congress takes up the issue, experts say.

A growing number of Americans in the individual healthcare market have subscribed the inexpensive coverage amid skyrocketing medical costs. Roughly 3 million consumers bought the plans in 2019, a 27% growth from 2018, the investigation found. The explosive growth in use makes it a bit less likely Biden’s HHS would pursue immediate, unilateral movement in the space, for fear of kicking Americans off their coverage.

Biden could also reverse Trump’s regulatory changes that have been friendly to association health plans, which allow small businesses or groups to band together to offer coverage. Though the ACA enhanced oversight of the coverage, the Trump administration in June 2018 issued a rule exempting them from rules regulating individual and small-group employer coverage.

As a result, association health plans were allowed to exclude or charge more on the basis of gender, age or other factors.

A federal court invalidated the rule later that year, and some states took legislative or regulatory actions to discourage the use of association health plans. However, the plans —which cover an estimated 3 million Americans — are still not required to cover all essential health benefits, making them a likely target for the Biden administration.

“It is something that we’re going to see some action on pretty soon, but it’s challenging. You don’t want to take those plans away from people, especially during a pandemic,” Cox said.

Expanding Medicaid coverage, eligibility

The Trump administration has given red states new avenues to constrict their Medicaid programs, which provide safety-net health insurance to some 75 million Americans.

Biden will likely first revise state demonstration waiver policies to expand coverage. Among other measures, Biden could get rid of past CMS guidance allowing states to play with Medicaid eligibility through work requirements, controversial programs tying coverage eligibility to work or volunteering hours, and to cap program funding.

Tennessee this month became the first state to receive a federal green light to convert its Medicaid funding to a block grant, following controversial CMS guidance issued early last year. Republicans tout block grants as a way to lower costs, while Democrats oppose the models as capped funding could lead to restricted benefits down the line, especially during times of emergency like a pandemic or natural disaster.

It’s more difficult to roll back a waiver if it’s already been approved, but Biden could put restrictions on it or reverse the decision before it goes into effect, experts say, though Tennessee would have an opportunity to object.

There are also actions Biden could take to reinstate certain beneficiary protections, which would require regulatory changes, KFF researchers say. Those include revising or stopping pending proposals that would change how Medicaid eligibility is determined in a way that would probably result in previously eligible people losing coverage by enacting more documentation requirements; change the government’s methodology for recouping improper payments; and reduce enhanced federal funding for eligibility workers.

Biden’s administration could also tweak regulations that have already been finalized, including the final Medicaid managed care rule for 2020 that relaxed network adequacy, beneficiary protections and quality oversight.

Hospital uncompensated care costs were up from $41.3B in 2018 and $38.4B in 2017, revealing an upward trend, according to AHA data.

Hospital uncompensated care costs increased right before the COVID-19 pandemic hit, according to new data from the American Hospital Association (AHA).

AHA data showed that hospitals incurred a new high of $41.61 billing in uncompensated care costs in 2019, the most recent year for which the group had complete data.

Uncompensated care costs in 2019 were up from $41.3 billion in 2018 and $38.4 billion in 2017 and were the second-highest per AHA records. Hospitals reported the most uncompensated care costs in 2013 when they incurred $46.8 billion.

Hospital uncompensated care costs decreased after the all-time high in 2013, but have recently started to tick back up after holding steady at $38.4 in 2016 and 2017.

In just the last 20 years, hospitals of all types have provided more than $660 billion in uncompensated care to patients, AHA reported. And that figure does not fully account for other ways in which provides provide financial assistance to patients of limited means, the group stated.

Each year, AHA aggregates data on uncompensated care, or care provided for which no reimbursement is received by hospitals from patients or payers. The data comes from the group’s Annual Survey of Hospitals, a comprehensive report of hospital financial data.

Uncompensated care is the sum of a hospital’s bad debt and financial assistance it provides, AHA explained.

Bad debt occurs when a hospital does not expect to obtain reimbursement for care provided, such as when patients are unable to pay their financial responsibility and do not qualify for financial assistance or are unwilling to pay their bills.

Hospitals also provide varying levels of financial assistance, AHA added. Financial assistance supports patients who cannot afford to pay and qualify for support from the hospital based on policies it has established based on the facility’s mission, financial condition, and geographic location, among other factors.

Combined, bad debt and financial assistance charges total a hospital’s uncompensated care charges, which is then multiplied by a hospital’s cost-to-charge ratio to determine total uncompensated care costs.

AHA noted that it expressed uncompensated care in costs versus charges because of significant variations in hospital payer mixes. Publishing the information as costs rather than charges enables better comparison across hospitals, the group said.

Nearly half of hospitals (48 percent) have seen bad debt and uncompensated care increase recently as a result of the ongoing COVID-19 pandemic, an analysis from consulting firm Kaufman Hall revealed.

More than 40 percent of hospitals also reported increases in percentage of uninsured or self-pay patients (44 percent) and the percentage of Medicaid patients (41 percent), which both contribute to unfunded or underfunded care at hospitals.

“The challenges brought on by the COVID-19 pandemic have affected nearly every aspect of hospital financial and clinical operations,” Lance Robinson, a managing director at Kaufman Hall, said at the time. “Organizations have responded to the challenge by adjusting their operations and strengthening important community relationships.”

Hospital uncompensated care costs – and bad debt as a result – are likely to increase in 2020 as hospitals come to terms with the impact COVID-19 has had on their financial health.

Already, hospitals have lost an estimated $323 billion in 2020 as a result of the COVID-19 pandemic, according to earlier projections from AHA.

About half of US hospitals also started the year in the red, AHA and Kaufman Hall stated in a recent report. The organizations predicted that hospital margins would sink to -7 percent in the second half of 2020 without comprehensive financial support from the government, but could decrease to a low of -11 percent if COVID-19 continued to periodically surge as it has.